Cloud OSS/BSS Market by OSS (Network Management & Orchestration, Resource Management, Analytics & Assurance, Service Design & Fulfilment), BSS (Billing & Revenue Management, Product Management, Customer Management) - Global Forecast to 2032

상품코드:1927590

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 350 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

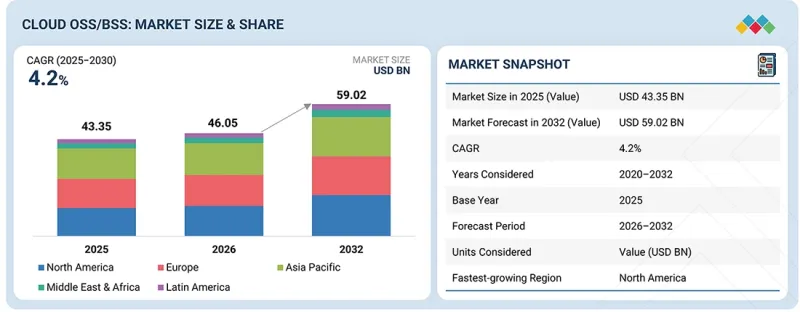

클라우드 OSS/BSS 시장 규모는 2026년에 460억 5,000만 달러로 추정되고, 2032년까지 연평균 복합 성장률(CAGR) 4.2%로 590억 2,000만 달러에 이를 것으로 예측됩니다.

통신사업자(CSP)가 동적이고 가상화된 네트워크를 관리하기 위해 민첩하고 프로그래밍 가능한 플랫폼을 찾는 가운데, SDN(소프트웨어 정의 네트워크)과 NFV(네트워크 기능 가상화)의 확산으로 클라우드 기반 OSS/BSS 솔루션의 도입이 가속화되고 있습니다. 도입이 가속화되고 있습니다.

조사 범위

조사 대상 기간

2020년-2032년

기준 연도

2025년

예측 기간

2026년-2032년

대상 단위

가치(100만/10억 달러)

부문

컴포넌트별, 클라우드 유형별, 사업자 유형별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

개인화된 서비스 및 번들 제공에 대한 수요가 증가함에 따라 고객 경험을 향상시키는 맞춤형 OSS/BSS 솔루션에 대한 관심도 높아지고 있습니다. 서비스 포트폴리오와 IT 아키텍처가 더욱 복잡해지는 가운데, 클라우드 네이티브 OSS/BSS 플랫폼은 실시간 운영과 효율적인 서비스 제공을 지원하는 데 필요한 유연성, 확장성, 자동화를 제공합니다.

통신 서비스 제공업체들이 변화를 가속화하기 위해 관리형 성과 기반 파트너십을 점점 더 많이 요구함에 따라, 서비스 부문은 예측 기간 동안 클라우드 OSS/BSS 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이러한 추세를 촉진하는 주요 요인으로는 신속한 도입의 필요성, 클라우드 네이티브 솔루션의 지속적인 최적화, 사내 개발 및 운영 부담의 감소 등이 있습니다. AI 및 컨테이너화 플랫폼의 인력 부족과 복잡성에 직면한 CSP는 파트너가 주도하는 관리 서비스와 통합 지원을 선호합니다.

또한, 규제 준수 요건, SLA 보장, 가동률, 변경 관리 능력 등 클라우드 기반 OSS/BSS 서비스가 제공할 수 있는 요소도 고객의 선택을 돕고 있습니다. 최근 사례로, Amdocs는 Globe와 다년간의 매니지드 서비스 계약을 확대하여 오케스트레이션, 수익화, 자동화를 포함한 OSS/BSS 운영을 관리함으로써 서비스 배포를 가속화하고 운영 부담을 경감하는 데 성공했습니다. 또 다른 계약으로 에릭슨은 버티 에어텔과 다년간의 매니지드 서비스 계약을 체결하고 네트워크와 운영을 관리하기로 했습니다. 이는 통신사업자가 파트너 중심의 서비스 제공을 선호한다는 것을 강조하는 것입니다. 이러한 계약은 CSP가 성과 기반 매니지드 서비스를 선호하는 이유를 보여주며, 서비스 분야가 가장 높은 CAGR을 나타낼 것이라는 견해를 뒷받침합니다.

예측 기간 동안 하이브리드 클라우드 부문은 클라우드 기반 OSS/BSS 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이러한 성장은 통신 서비스 제공업체(CSP)가 유연성, 데이터 주권, 레거시 시스템과 최신 클라우드 네이티브 플랫폼 간의 원활한 통합을 제공하는 도입 모델을 점점 더 필요로 하고 있기 때문입니다. 하이브리드 클라우드 아키텍처는 CSP가 기밀 데이터와 핵심 업무에 대한 관리 권한을 유지하면서 퍼블릭 클라우드 환경의 확장성, 민첩성, 혁신성을 활용할 수 있도록 지원합니다. 또한, 단계적 전환을 촉진하고, 벤더 종속성을 최소화하며, 세계 시장의 다양한 규제 및 운영 요구사항에 대응합니다. 또한, 하이브리드 클라우드는 업무 중단 없이 통합 과금, 서비스 오케스트레이션, 고객 경험 관리와 같은 중요한 OSS/BSS 기능을 현대화할 수 있습니다. 예를 들어, 텔레포니카는 구글 클라우드를 활용한 클라우드 기반 OSS/BSS 현대화를 확대하고, 하이브리드 클라우드 모델을 채택하여 핵심 BSS 워크로드를 On-Premise 시스템과 퍼블릭 클라우드 인프라 모두에서 실행하는 하이브리드 클라우드 모델을 채택하고 있습니다. 이번 도입은 단계적 마이그레이션, 데이터 주권, 여러 사업 지역에 걸친 실시간 서비스 관리를 지원합니다. 이러한 접근 방식은 통신 사업자들이 하이브리드 클라우드 도입을 점점 더 선호하는 이유를 뒷받침하며, 예측 기간 동안 하이브리드 클라우드 부문이 가장 높은 CAGR로 성장할 것이라는 전망을 강화합니다.

북미는 대규모 5G 투자, 모바일 데이터 트래픽 증가, 실시간 서비스 수익화에 대한 수요 증가를 배경으로 예측 기간 동안 클라우드 기반 OSS/BSS 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. AT&T, Verizon, T-Mobile 등 주요 통신사업자(CSP)들은 클라우드 기반 OSS/BSS 플랫폼을 채택하여 디지털 전환을 추진하고 있습니다. 예를 들어, Verizon은 Oracle과 협력하여 서비스 민첩성과 고객 경험을 향상시키기 위해 최신 클라우드 네이티브 OSS/BSS 스택을 도입하고 있습니다. 이러한 움직임은 북미 통신사업자들 사이에서 확장 가능하고 AI를 지원하는 OSS/BSS 기능에 대한 수요가 증가하고 있으며, 이는 기존의 하이퍼스케일러 생태계와 디지털 혁신 및 인프라 현대화를 강조하는 규제 프레임워크에 의해 더욱 강화되고 있습니다. 더욱 강화되고 있습니다.

이 지역의 성숙한 통신 인프라와 통신 서비스 제공업체(CSP)와 기술 제공업체 간의 전략적 제휴가 결합되어 OSS/BSS 혁신에 매우 유리한 환경을 형성하고 있습니다. 넷크래커와 텔레넷의 하이브리드 클라우드 BSS 도입 사례와 같은 협업은 클라우드 네이티브 플랫폼이 대규모 운영 효율화, 실시간 과금, 원활한 서비스 오케스트레이션을 실현할 수 있는 능력을 입증하고 있습니다. 이러한 도입 사례는 하이브리드 클라우드와 퍼블릭 클라우드 모델이 트래픽이 많은 네트워크 환경과 복잡한 서비스 생태계를 관리하는 데 효과적이라는 것을 입증하고 있습니다. 북미 서비스 제공업체들이 자동화, 확장성, 고객 중심주의에 대한 우선순위를 계속 높여가고 있는 가운데, 클라우드 기반 OSS/BSS 플랫폼은 차세대 연결성과 디지털 서비스 제공을 위한 기반이 되고 있습니다. 이러한 지속적인 모멘텀은 이 지역을 현대적 OSS/BSS 프레임워크로의 전환을 주도하는 주요 원동력으로 자리매김하고 있습니다.

클라우드 기반 OSS/BSS 시장의 주요 진출기업으로는 Amdocs(미국), Salesforce(미국), NEC(일본), Ericsson(스웨덴), Oracle(미국), Huawei(중국), Hewlett Packard Enterprise(미국), Optiva(캐나다), Nokia(캐나다), Cloudville(캐나다), ZTE Corporation(중국), Comarch(중국), Subex(인도), Sterling Optiva(캐나다),Nokia(핀란드),Kloudville(캐나다),ZTE Corporation(중국),Comarch(핀란드),Subex(인도),Sterlite Technologies Limited(인도),InfoVista(미국), Comviva(인도), Cerillion(영국), Tecnotree(핀란드), Whale Cloud(중국), Hughes Network Systems(미국), Mavenir Systems(미국), Infosys(인도), Wipro(인도), Alepo(미국), Infosys(인도), Wipro(인도), Alepo(미국), MATRIXX Software(미국), Ciena(미국), Aria Systems(미국), Bill Perfect(미국), Telgoo5(미국), NMSWorks Software(인도), Wavelo(미국), ChikPea(미국), BlueCat(미국)), BlueCat(미국), Kentik(미국), Knot Solutions(인도), BluLogix(미국), Totogi(미국), BeQuick(미국) 등이 있습니다. 이들 기업은 클라우드 기반 OSS/BSS 시장에서의 사업 기반 확대를 위해 파트너십, 계약, 협업, 신제품 출시 및 기능 강화, 인수 등의 성장 전략을 추진해 왔습니다.

조사 범위

본 시장 조사에서는 클라우드 기반 OSS/BSS 시장 규모를 다양한 부문별로 분석하였습니다. 컴포넌트별, 클라우드 유형별, 사업자 유형별, 지역별 등 각 부문 시장 규모와 성장 가능성을 추정하는 것을 목적으로 하고 있습니다. 주요 시장 진입업체에 대한 상세한 경쟁 분석, 기업 프로파일, 제품 및 서비스 제공에 대한 주요 관찰 사항, 최근 동향, 시장 전략에 대한 내용도 포함하고 있습니다.

이 보고서는 세계 클라우드 OSS/BSS 시장 시장 리더와 신규 시장 진출기업에게 세계 클라우드 OSS/BSS 시장의 수익 및 하위 부문에 대한 가장 정확한 추정치를 제공합니다. 또한, 이해관계자들이 경쟁 구도를 이해하고, 비즈니스를 적절히 포지셔닝하고, 적절한 시장 진출 전략을 수립할 수 있는 깊은 인사이트를 얻을 수 있도록 돕습니다. 또한, 시장 동향에 대한 인사이트와 주요 촉진요인, 제약, 과제, 기회에 대한 정보를 이해관계자들에게 제공합니다.

1. 주요 촉진요인(맞춤형 클라우드 기반 OSS/BSS 솔루션 도입 증가, 5G 확산에 따른 클라우드 기반 OSS/BSS 수요 급증, 통합 과금 시스템에 대한 수요 증가, CAPEX 및 OPEX 절감 니즈 증가) 분석, 억제요인(솔루션 도입을 저해하는 데이터 데이터 프라이버시 우려, 분절된 레거시 인프라), 클라우드 기반 OSS/BSS 시장 성장에 영향을 미치는 기회(통신 산업을 변화시키는 클라우드 기술 채택, 차세대 운영 시스템 및 소프트웨어 프레임워크를 통한 통신 산업 성장, IoT 수익화 및 마케팅 혁신의 다음 단계로의 전환), 과제(방대한 고객 거래량 및 네트워크 관리의 복잡성, 클라우드 네이티브 OSS/BSS 솔루션 도입을 위한 기술 숙련도 부족)에 대해 분석했습니다.

2. 제품 개발 및 혁신 : 클라우드 기반 OSS/BSS 시장의 향후 기술 동향, 연구개발 활동, 신제품 및 서비스 출시에 대한 상세 분석

3. 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 본 보고서는 다양한 지역의 클라우드 기반 OSS/BSS 시장을 분석합니다.

4. 시장 다각화 : 클라우드 기반 OSS/BSS 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 투자에 관한 종합적인 정보

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

연결된 시장과 분야간 기회

Tier1/2/3참여 기업 전략적 움직임

제5장 업계 동향

Porter의 Five Forces 분석

거시경제 전망

공급망 분석

생태계 분석

가격 분석

2026년 주요 컨퍼런스 및 이벤트

고객의 비즈니스에 영향을 미치는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세의 영향-클라우드 OSS/BSS 시장

제6장 기술, 특허, 디지털, AI 도입 별 전략적 파괴

주요 기술

보완적 기술

기술 로드맵

특허 분석

AI/생성형 AI가 클라우드 OSS/BSS 시장에 미치는 영향

성공 사례와 실세계에의 응용

제7장 규제 상황

지역 규제와 컴플라이언스

규제기관, 정부기관, 기타 조직

업계표준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구매 프로세스에 관여하는 주요 이해관계자와 그 평가 기준

채택 장벽과 내부 과제

다양한 최종 이용 산업 미충족 요구

제9장 클라우드 OSS/BSS 시장(컴포넌트별)

솔루션

서비스

제10장 클라우드 OSS/BSS 시장(클라우드 유형별)

퍼블릭 클라우드

프라이빗 클라우드

하이브리드 클라우드

제11장 클라우드 OSS/BSS 시장(사업자 별)

모바일 오퍼레이터

고정 오퍼레이터

제12장 클라우드 OSS/BSS 시장(지역별)

북미

북미 : 클라우드 OSS/BSS 시장 성장 촉진요인

미국

캐나다

유럽

유럽 : 클라우드 OSS/BSS 시장 성장 촉진요인

영국

독일

프랑스

이탈리아

기타

아시아태평양

아시아태평양 : 클라우드 OSS/BSS 시장 성장 촉진요인

중국

일본

인도

기타

중동 및 아프리카

중동 및 아프리카 : 클라우드 OSS/BSS 시장 성장 촉진요인

사우디아라비아

아랍에미리트

남아프리카공화국

기타

라틴아메리카

라틴아메리카 : 클라우드 OSS/BSS 시장 성장 촉진요인

브라질

멕시코

기타

제13장 경쟁 구도

개요

주요 시장 진출기업 경쟁 전략/강점, 2024년-2025년

매출 분석, 2021년-2025년

시장 점유율 분석, 2025년

브랜드/제품 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2025년

기업 평가 매트릭스 : 스타트업/중소기업, 2025년

기업 평가와 재무 지표

경쟁 시나리오

제14장 기업 개요

주요 시장 진출기업

AMDOCS

SALESFORCE

NEC

ERICSSON

ORACLE

HUAWEI

HPE

OPTIVA

NOKIA

KLOUDVILLE

ZTE

COMARCH

SUBEX

INFOVISTA

COMVIVA

CERILLION

WHALE CLOUD

HUGHES

MAVENIR

STL

TECNOTREE

INFOSYS

WIPRO

ALEPO

MATRIXX SOFTWARE

CIENA

ARIA SYSTEMS

스타트업/중소기업

BILL PERFECT

TELGOO5

NMSWORKS SOFTWARE

WAVELO

CHIKPEA

BLUECAT

KENTIK

KNOT SOLUTIONS

BLULOGIX

TOTOGI

BEQUICK

제15장 조사 방법

제16장 부록

LSH

영문 목차

영문목차

The cloud OSS/BSS market is estimated at USD 46.05 billion in 2026 and is projected to reach USD 59.02 billion by 2032, at a CAGR of 4.2%. The widespread adoption of SDN and NFV is accelerating the uptake of cloud OSS/BSS solutions, as CSPs seek agile, programmable platforms to manage dynamic, virtualized networks.

Scope of the Report

Years Considered for the Study

2020-2032

Base Year

2025

Forecast Period

2026-2032

Units Considered

Value (USD Million/Billion)

Segments

By component, by cloud type , by operator type

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and Latin America

Rising demand for personalized services and bundled offerings is also driving interest in customized OSS/BSS solutions that enhance the customer experience. As service portfolios and IT architectures grow more complex, cloud-native OSS/BSS platforms offer the flexibility, scalability, and automation needed to support real-time operations and efficient service delivery.

"By component, the services segment is expected to grow with the highest CAGR during the forecast period."

The services segment is forecast to post the highest CAGR in the cloud OSS/BSS market over the forecast period, as communication service providers increasingly seek managed, outcome-based partnerships to accelerate transformation. Key drivers of this trend include the need for rapid deployment, continuous optimization of cloud-native solutions, and reduced in-house development and operational burden. CSPs facing talent constraints and complexity with AI and containerized platforms prefer partner-led managed services and integration support.

Clients are also driven by regulatory compliance requirements, SLA guarantees, uptime, and change management capabilities that cloud-based OSS/BSS services can deliver. A recent example is Amdocs' expansion of a multi-year managed services agreement with Globe to provide managed OSS/BSS operations, including orchestration, monetization, and automation, to accelerate service rollout and reduce the operational burden. In another deal, Ericsson signed a multi-year managed services contract with Bharti Airtel to manage networks and operations, underscoring the operator's preference for partner-led delivery. These engagements show why CSPs favor managed, outcome-based services, supporting the view that the services component will record the highest CAGR.

"By cloud type, the hybrid cloud segment is expected to grow at the highest CAGR during the forecast period."

The hybrid cloud segment is projected to register the highest CAGR in the cloud OSS/BSS market during the forecast period. This growth is driven by communication service providers' (CSPs) growing need for deployment models that offer flexibility, data sovereignty, and seamless integration between legacy systems and modern cloud-native platforms. Hybrid cloud architecture enables CSPs to retain control over sensitive data and core operations while benefiting from the scalability, agility, and innovation of public cloud environments. It also facilitates phased migration, minimizes vendor lock-in, and accommodates diverse regulatory and operational requirements across global markets. Moreover, hybrid cloud enables the modernization of critical OSS/BSS functions, such as converged charging, service orchestration, and customer experience management, without disrupting operations. For instance, Telefonica expanded its cloud OSS/BSS modernization with Google Cloud, adopting a hybrid cloud model to run core BSS workloads across on-premises systems and public cloud infrastructure. The deployment supports phased migration, data sovereignty, and real-time service management across multiple operating regions. This approach underscores why CSPs increasingly favor hybrid cloud deployments, reinforcing expectations that the hybrid cloud segment will grow at the highest CAGR during the forecast period.

"North America will register the highest growth rate during the forecast period."

North America is expected to post the highest CAGR in the cloud OSS/BSS market during the forecast period, driven by substantial 5G investments, rising mobile data traffic, and growing demand for real-time service monetization. Leading communication service providers (CSPs) such as AT&T, Verizon, and T-Mobile are advancing their digital transformation by adopting cloud-based OSS/BSS platforms. For instance, Verizon has partnered with Oracle to deploy a modern, cloud-native OSS/BSS stack to improve service agility and the customer experience. These developments underscore rising demand among North American operators for scalable, AI-enabled OSS/BSS capabilities, further supported by a well-established hyperscaler ecosystem and regulatory frameworks that emphasize digital innovation and infrastructure modernization.

The region's mature telecom infrastructure, combined with strategic alliances between CSPs and technology providers, creates a highly conducive environment for OSS/BSS innovation. Collaborations such as the Netcracker and Telenet hybrid cloud BSS deployment demonstrate the ability of cloud-native platforms to deliver enhanced operational efficiency, real-time billing, and seamless service orchestration at scale. These implementations validate the effectiveness of hybrid and public cloud models in managing high-volume network environments and complex service ecosystems. As North American service providers continue to prioritize automation, scalability, and customer-centricity, cloud OSS/BSS platforms are becoming a foundational element in enabling next-generation connectivity and digital service delivery. This sustained momentum positions the region as a key driver of the global shift toward modern OSS/BSS frameworks.

Breakdown of primaries

The study draws on insights from industry experts, including solution vendors and Tier 1 companies. The breakdown of the primaries is as follows.

By Company Type: Tier 1 - 38%, Tier 2 - 43%, and Tier 3 - 19%

By Designation: C-level - 35%, Directors - 15%, and Others - 50%

By Region: North America - 50%, Europe - 15%, APAC - 30%, ROW - 5%

The major players in the cloud OSS/BSS market include Amdocs (US), Salesforce (US), NEC (Japan), Ericsson (Sweden), Oracle (US), Huawei (China), Hewlett Packard Enterprise (US), Optiva (Canada), Nokia (Finland), Kloudville (Canada), ZTE Corporation (China), Comarch (Finland), Subex (India), Sterlite Technologies Limited (India), InfoVista (US), Comviva (India), Cerillion (UK), Tecnotree (Finland), Whale Cloud (China), Hughes Network Systems (US), Mavenir Systems (US), Infosys (India), Wipro (India), Alepo (US), MATRIXX Software (US), Ciena (US), Aria Systems (US), Bill Perfect (US), Telgoo5 (US), NMSWorks Software (India), Wavelo (US), ChikPea (US), BlueCat (US), Kentik (US), Knot Solutions (India), BluLogix (US), Totogi (US), and BeQuick (US). These players have pursued growth strategies, including partnerships, agreements, and collaborations; new product launches and enhancements; and acquisitions, to expand their footprint in the cloud OSS/BSS market.

Research Coverage

The market study covers the cloud OSS/BSS market size across different segments. It aims to estimate market size and growth potential across segments, including component, cloud type, operator type, and region. The study includes an in-depth competitive analysis of leading market players, their company profiles, key observations on product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with the closest available estimates of the global Cloud OSS/BSS market's revenue and subsegments. It will also help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. Moreover, the report will provide stakeholders with insights into the market's pulse and information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. Analysis of key drivers (increasing adoption of tailored cloud OSS/BSS solutions, Increasing 5G adoption to surge demand for cloud OSS/BSS, growing demand for convergent billing systems, growing need to reduce CAPEX and OPEX), restraints (concerns over data privacy hindering adoption of solutions, fragmented legacy infrastructure), opportunities (adoption of cloud technologies to transform telecom industry, growth of telecom industry with next-generation operation systems and software framework, operators taking service innovation to next level for monetizing and marketing IoT), and challenges (high volume of customer transactions and increasing complexities in network management, lack of technical proficiency for implementing cloud-native OSS/BSS solutions) influencing the growth of the cloud OSS/BSS market

2. Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the cloud OSS/BSS market

3. Market Development: Comprehensive information about lucrative markets - the report analyzes the cloud OSS/BSS market across various regions

4. Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the cloud OSS/BSS market

5. Competitive Assessment: In-depth assessment of market share, growth strategies and service offerings of leading players - Amdocs (US), Salesforce (US), NEC (Japan), Ericsson (Sweden), Oracle (US), Huawei (China), Hewlett Packard Enterprise (US), Optiva (Canada), Nokia (Finland), Kloudville (Canada), ZTE Corporation (China), Comarch (Finland), Subex (India), Sterlite Technologies Limited (India), InfoVista (US), Comviva (India), Cerillion (UK), Tecnotree (Finland), Whale Cloud (China), Hughes Network Systems (US), Mavenir Systems (US), Infosys (India), Wipro (India), Alepo (US), MATRIXX Software (US), Ciena (US), Aria Systems (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN CLOUD OSS/BSS MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CLOUD OSS/BSS MARKET

3.2 CLOUD OSS/BSS MARKET, BY COMPONENT AND REGION

3.3 CLOUD OSS/BSS MARKET, BY SOLUTION

3.4 CLOUD OSS/BSS MARKET, BY CLOUD TYPE

3.5 CLOUD OSS/BSS MARKET, BY OPERATOR TYPE

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Growing adoption of tailored cloud OSS/BSS solutions

4.2.1.2 Increasing 5G adoption to surge demand for cloud OSS/BSS

4.2.1.3 Rising demand for convergent billing systems

4.2.1.4 Growing need to reduce CAPEX and OPEX

4.2.2 RESTRAINTS

4.2.2.1 Concerns over data privacy

4.2.2.2 Fragmented legacy infrastructure

4.2.3 OPPORTUNITIES

4.2.3.1 Adoption of cloud technologies in telecom industry

4.2.3.2 Integration of next-generation operating systems and software frameworks in telecom industry

4.2.3.3 Operators advancing service innovation to unlock IoT monetization

4.2.4 CHALLENGES

4.2.4.1 High volume of customer transactions and increasing complexities in network management

4.2.4.2 Lack of technical proficiency for implementing cloud-native OSS/BSS solutions

4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.3.1 INTERCONNECTED MARKETS

4.3.2 CROSS-SECTOR OPPORTUNITIES

4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC OUTLOOK

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN CLOUD OSS/BSS MARKET

5.3 SUPPLY CHAIN ANALYSIS

5.3.1 SOLUTION PROVIDERS

5.3.2 CONNECTIVITY PROVIDERS

5.3.3 SYSTEM INTEGRATORS

5.3.4 SERVICE PROVIDERS

5.3.5 END USERS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF CLOUD OSS/BSS INTEGRATED SOLUTIONS, BY KEY PLAYERS, 2025

5.5.1.1 Average selling price of cloud OSS/BSS integrated solutions, by key players, 2025

5.5.2 INDICATIVE PRICING ANALYSIS OF CLOUD BSS SOLUTIONS, BY KEY PLAYERS, 2025

5.5.2.1 Indicative pricing analysis of cloud BSS solutions, by key players, 2025

5.6 KEY CONFERENCES AND EVENTS, 2026

5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 CASE STUDY ANALYSIS

5.9.1 MULTI-VENDOR 5G SERVICE AND NETWORK ORCHESTRATION TO ACCELERATE SERVICE LIFECYCLE

5.9.2 AI-DRIVEN OPERATIONS ENGINE TO REDUCE ORDER FALLOUT AND ACCELERATE REMEDIATION

5.9.3 RAPID SD-WAN SERVICE LAUNCH USING CLOUD BUSINESS-PLATFORM APPROACH

5.9.4 UNIFIED REAL-TIME MONETIZATION FOR 5G AND CONVERGED SERVICES

5.9.5 SCALABLE CLOUD BILLING REPLACEMENT TO SUPPORT HIGH-VOLUME PAYMENTS AND PROCESSING

5.10 IMPACT OF 2025 US TARIFF - CLOUD OSS/BSS MARKET

5.10.1 INTRODUCTION

5.10.2 KEY TARIFF RATES

5.10.3 PRICE IMPACT ANALYSIS

5.10.3.1 Strategic shifts and emerging trends

5.10.4 IMPACT ON COUNTRIES/REGIONS

5.10.4.1 US

5.10.4.2 China

5.10.4.3 Europe

5.10.4.4 Asia Pacific (excluding China)

5.10.5 IMPACT ON END-USER INDUSTRIES

5.10.5.1 Telecommunication service providers (CSPs/Telcos)

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

6.1 KEY TECHNOLOGIES

6.1.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

6.1.2 MICROSERVICES AND CLOUD NATIVE ARCHITECTURES

6.1.3 DIGITAL TWIN

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 DEVOPS AND CONTINUOUS INTEGRATION/CONTINUOUS DEPLOYMENT

6.2.2 MULTI-ACCESS EDGE COMPUTING

6.2.3 OPEN APIS AND INTEROPERABILITY STANDARDS

6.3 TECHNOLOGY ROADMAP

6.3.1 SHORT-TERM (2026-2027) | FOUNDATION & EARLY COMMERCIALIZATION