자동차 디지털 콕핏 시장 : 기기별, 용도별, 차량 유형별, EV 유형별, 디스플레이 유형별, 디스플레이 사이즈별(-2032년)

Automotive Digital Cockpit Market by Equipment, Application, Vehicle Type, EV Type, Display Type, Display Size - Global Forecast to 2032

상품코드:1914124

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 377 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

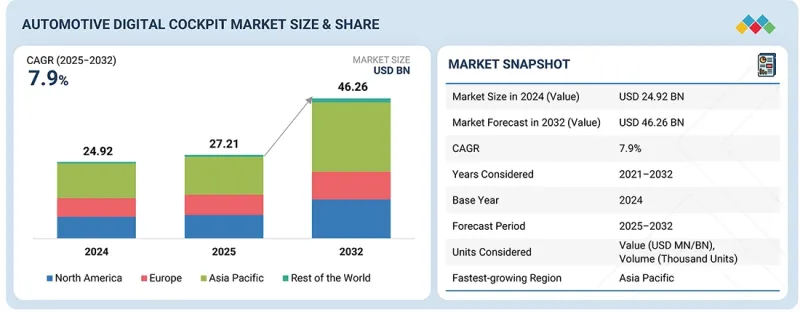

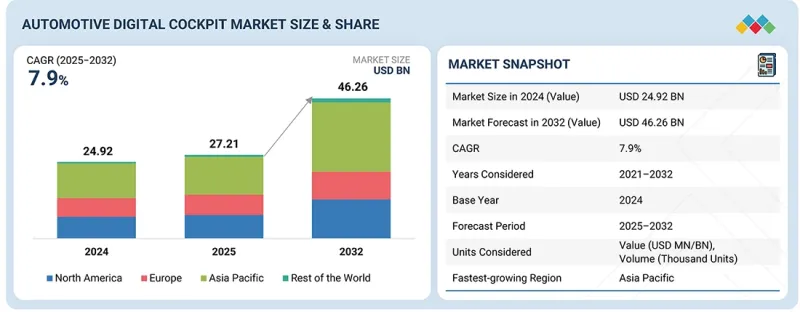

자동차 디지털 콕핏 시장 규모는 2025년 272억 1,000만 달러에 달했고, CAGR 7.9%로 성장하고, 2032년에는 462억 6,000만 달러에 이를 것으로 예측됩니다.

조사 범위

조사 기간

2021-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

가치(달러)

부문

장비, 용도, 차량 유형, EV 유형, 디스플레이 유형, 디스플레이 크기

대상 지역

북미, 유럽, 아시아태평양 및 세계 기타 지역

자동차 제조업체가 주요 지역 전체에서 연결성이 높고 소프트웨어 중심 차량 플랫폼으로의 전환을 가속화하고 있기 때문에 시장은 계속 성장하고 있습니다. 대형 디스플레이, 통합형 인포테인먼트 시스템, 디지털 클러스터, 지능형 드라이버 모니터링의 소비자 채택이 증가하고 있는 것은 대중차와 고급차 모두에서 조종석 업그레이드를 추진하고 있습니다. 그래픽 처리, 중앙 집중식 컴퓨팅, 클라우드 연계 서비스의 발전으로 보다 풍부한 인터페이스와 지속적인 개선이 가능합니다. 전기자동차의 생산 확대는 에너지 분석과 실시간 제어 기능을 제공하는 조종석 시스템에 대한 수요를 더욱 높이고 있습니다. 디지털 조종실의 혁신, 음성 상호작용, 멀티스크린 레이아웃에 대한 적극적인 투자가 차내 경험 향상에 기여하고 있습니다. 운전자의 주의력과 안전성에 대한 규제의 초점 확대도 신형차 도입에 있어서의 첨단 조종석 기술의 통합을 뒷받침하고 있습니다.

"디스플레이 크기별로는 5-10인치가 2024년 최대 점유율을 차지"

컴팩트 카, 미들 클래스 자동차, 일부 프리미엄 차종에 대한 광범위한 채택이 이것을 견인하고 있습니다. 이 부문은 시인성, 비용 효율성, 대시보드에 대한 적응성의 적절한 균형을 제공하며 디지털 계기 클러스터, 인포테인먼트 디스플레이 및 보조 제어 화면의 핵심을 담당합니다. 자동차 제조업체가 5-10인치 디스플레이를 선호하는 이유는 내비게이션, 미디어, 경보, 시스템 진단 등 중요한 차량 기능을 지원하면서 높은 저렴함과 생산 확장성을 유지할 수 있기 때문입니다. 터치 응답성, 밝기 제어, 고해상도 시각화를 통해 시스템 비용을 늘리지 않고도 사용자 경험을 개선했습니다. 조종석 설계가 소프트웨어 정의 아키텍처로 전환하는 동안 5-10인치 디스플레이는 현대 컴퓨팅 플랫폼 및 연결 서비스와 높은 호환성을 유지합니다.

"EV 유형별로 BEV 부문이 예측 기간 동안 가장 빠른 성장률을 보여줄 전망"

EV 생산량 증가와 디지털 퍼스트의 자동차 플랫폼으로의 전환은 전동 파워트레인을 보완하는 첨단 조종석 솔루션의 필요성을 촉진하고 있습니다. EV 사용자는 충전 상태 파악, 에너지 관리 데이터, 경로 최적화 및 성능 업데이트를 제공하는 기능이 풍부한 캐빈 인터페이스를 요구합니다. 이러한 추세로 고해상도 스크린, 스마트 클러스터, 클라우드 지원 인포테인먼트 시스템의 사용이 증가하고 있습니다. 자동차 제조업체는 조종석 기능과 핵심 전력 관리 작업을 통합하기 위해 도메인 컨트롤러 기반 아키텍처를 표준화합니다. 정책 인센티브와 충전 네트워크의 급속한 확대가 보다 정교한 조종석 구성으로의 전환을 가속화하고 있습니다. 기계적 제약이 적은 EV 플랫폼은 멀티 스크린과 몰입형 인터페이스의 통합을 용이하게 합니다. 세계 EV 보급률이 꾸준히 상승하는 가운데 강력한 디스플레이와 HMI 포트폴리오를 갖춘 기술 공급자는 EV 개발 파이프라인 전반에서 크게 성장할 수 있는 입장에 있습니다.

"용도별로 인포테인먼트 부문이 2032년 최대 점유율을 차지할 전망"

커넥티드 서비스와 개인화된 미디어 경험에 대한 수요가 높아지는 가운데 2032년에는 인포테인먼트 부문이 가장 큰 점유율을 차지할 것으로 예측됩니다. 자동차 제조업체는 네비게이션, 미디어, 통화, 메시지 기능, 스마트폰 연계, 차량 설정을 단일 인터페이스에 통합하는 플랫폼을 우선적으로 채택하고 있습니다. 그래픽 처리 기술의 발전과 소프트웨어 정의 콕핏 아키텍처는 OTA를 통한 지속적인 기능 업그레이드를 가능하게 합니다. 처리 능력, 그래픽 렌더링, 클라우드 통합의 발전으로 자연스러운 음성 상호 작용, 예측 제안, 중단없는 미디어 액세스 등의 고급 기능이 실현되었습니다. OEM사는 또한 인포테인먼트를 고수익 채널로 하는 구독형 서비스를 확대하고 있습니다. 디지털 편의성과 몰입형 인터랙션에 대한 기대가 높아지는 가운데, 인포테인먼트 시스템은 2032년까지 주요 용도로서의 지위를 유지할 전망입니다.

본 보고서에서는 세계 자동차 디지털 콕핏 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분, 지역별, 주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

미개척 시장 및 미충족 수요 분석

상호 연결된 시장 및 산업 간 기회

Tier 1/2/3 기업의 전략적 움직임

제5장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래의 응용

기술 분석

기술 로드맵

특허 분석

미래의 응용

AI/생성형 AI가 자동차 디지털 콕핏 시장에 미치는 영향

성공 사례와 실세계에의 응용

제6장 지속가능성과 규제상황

지역 규제 및 규정 준수

지속가능성에 대한 노력

지속가능성에 미치는 영향과 규제 정책의 노력

인증, 라벨, 환경 기준

제7장 고객정세와 구매행동

의사결정 프로세스

이해관계자와 구매평가기준

채택 장벽과 내부 과제

다양한 최종 사용자 산업의 미충족 요구

시장 수익성

제8장 업계 동향

거시경제지표

생태계 분석

공급망 분석

가격 분석

고객의 사업에 영향을 미치는 동향과 혼란

투자 및 자금조달 시나리오

이용 사례별 자금 조달

2026-2027년 주요 회의 및 이벤트

무역 분석

사례 연구 분석

2025년 미국 관세의 영향

OEM 및 공급업체 프로그램의 전략적 변화

OEM 분석

XPENG

NIO

LEAPMOTOR

GEELY ZEEKR

TATA MOTORS

VOLKSWAGEN AUDI

BMW

STELLANTIS

MERCEDES BENZ

FORD MOTOR COMPANY

GENERAL MOTORS

제9장 자동차 디지털 콕핏 시장 : 기기별

디지털 악기 클러스터

디지털 센터 콘솔

인포테인먼트 유닛

후석 인포테인먼트 유닛

조수석 인포테인먼트 유닛

헤드업 디스플레이(HUD)

운전자 모니터링 시스템

주요 산업 인사이트

제10장 자동차 디지털 콕핏 시장 : 차량 유형별

승용차

소형 상용차(LCV)

대형 상용차(HCV)

주요 산업 인사이트

제11장 자동차 디지털 콕핏 시장 : EV 유형별

배터리 전기자동차(BEV)

플러그인 하이브리드 전기자동차(PHEV)

주요 산업 인사이트

제12장 자동차 디지털 콕핏 시장 : 용도별

인포테인먼트

드라이버 모니터링과 어시스턴스

차량 및 쾌적성 제어 시스템

주요 산업 인사이트

제13장 자동차 디지털 콕핏 시장 : 디스플레이 사이즈별

5인치 미만

5-10인치

10인치 초과

주요 산업 인사이트

제14장 자동차 디지털 콕핏 시장 : 디스플레이 유형별

액정 디스플레이(LCD)

유기 LED(OLED)

박막 트랜지스터 액정 디스플레이(TFT-LCD)

주요 산업 인사이트

제15장 자동차 디지털 콕핏 시장 : 지역별

아시아태평양

중국

인도

일본

한국

태국

기타

북미

미국

캐나다

멕시코

유럽

독일

프랑스

이탈리아

스페인

영국

러시아

기타

기타 지역

브라질

이란

기타

제16장 경쟁 구도

주요 진입기업의 전략/강점

시장 점유율 분석

수익 분석

기업평가와 재무지표

브랜드 / 제품 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업 / 중소기업

경쟁 시나리오

제17장 기업 프로파일

주요 기업

CONTINENTAL AG

ROBERT BOSCH GMBH

HARMAN INTERNATIONAL

VISTEON CORPORATION

DENSO CORPORATION

VALEO

MITSUBISHI ELECTRIC CORPORATION

TOMTOM INTERNATIONAL BV

APTIV

LG ELECTRONICS

FORVIA

MAGNA INTERNATIONAL INC.

HYUNDAI MOBIS

ALPS ALPINE CO., LTD.

기타 기업

QUALCOMM TECHNOLOGIES, INC.

NXP SEMICONDUCTORS

MARELLI HOLDINGS CO., LTD.

ZF FRIEDRICHSHAFEN AG

PIONEER CORPORATION

SONY CORPORATION

INFINEON TECHNOLOGIES AG

JVCKENWOOD CORPORATION

FUJITSU LIMITED

FORYOU CORPORATION

MAGNETI MARELLI SPA

제18장 조사 방법

제19장 부록

SHW

영문 목차

영문목차

The automotive digital cockpit market is projected to grow from USD 27.21 billion in 2025 to USD 46.26 billion in 2032 at a CAGR of 7.9%.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Million/Billion)

Segments

Equipment, Application, Vehicle Type, EV Type, Display Type, Display Size

Regions covered

North America, Europe, Asia Pacific, and Rest of the world

The market is growing as automakers accelerate the shift to connected, software-driven vehicle platforms across all major regions. The rising consumer adoption of large displays, integrated infotainment systems, digital clusters, and intelligent driver monitoring is driving cockpit upgrades in both mass-market and premium vehicles. Advancements in graphics processing, centralized computing, and cloud-linked services are enabling richer interfaces and continuous feature enhancements. Growing electric vehicle production is further increasing demand for cockpit systems that provide energy insights and real-time control functions. Strong investments in digital cockpit innovation, voice interaction, and multiscreen layouts are improving in-cabin experiences. Expanding regulatory focus on driver attention and safety is also supporting the integration of advanced cockpit technologies across new model launches.

"The 5-10" display segment accounted for the largest share of the automotive digital cockpit market in 2024."

The 5-10" display segment accounted for the largest share of the automotive digital cockpit market in 2024, driven by its extensive deployment across compact, mid-range, and selected premium vehicles. This segment offers the right mix of clarity, cost efficiency, and dashboard adaptability, making it central to digital instrument clusters, infotainment displays, and auxiliary control screens. Automakers favor 5-10" displays because these displays support essential vehicle functions such as navigation, media, alerts, and system diagnostics while maintaining strong affordability and production scalability. Enhancements in touch responsiveness, brightness control, and high-resolution visuals have improved user experience without raising system expense. As cockpit designs shift toward software-defined architectures, 5-10" displays remain highly compatible with modern compute platforms and connected services.

"The BEV segment is projected to register the fastest growth during the forecast period."

The battery electric vehicle (BEV) segment is expected to register the fastest growth in the automotive digital cockpit market during the forecast period. Increasing EV output and the transition to digital-first automotive platforms are driving the need for advanced cockpit solutions that complement electric powertrains. EV users seek feature-rich cabin interfaces that provide charging insights, energy management data, route optimization, and performance updates. This trend is increasing the use of high-resolution screens, smart clusters, and cloud-enabled infotainment systems. Automakers are standardizing domain controller-based architectures to unify cockpit functions with core power management operations. Policy incentives and rapid expansion of charging networks are accelerating the shift toward more sophisticated cockpit setups. EV platforms, with fewer mechanical limitations, also support easier integration of multiscreen and immersive interfaces. With global EV penetration rising steadily, technology providers with strong display and HMI portfolios are positioned to capture substantial growth across EV development pipelines.

"The infotainment segment is projected to hold the largest share of the automotive digital cockpit market in 2032."

The infotainment segment is expected to hold the largest share of the automotive digital cockpit market in 2032 as demand grows for connected services and personalized media experiences. Automakers are prioritizing platforms that integrate navigation, media, calls, and messaging, smartphone features, and vehicle settings within a single interface. Advancements in graphics processing and software-defined cockpit architectures enable continuous feature upgrades through over-the-air updates. Advancements in processing capability, graphic rendering, and cloud integration are enabling advanced functions such as natural voice interaction, predictive suggestions, and uninterrupted media access. OEMs are also expanding subscription-based offerings that make infotainment a high-value revenue channel. With rising expectations for digital convenience and immersive interaction, infotainment systems are set to remain the dominant application segment by 2032.

"The Asia Pacific is projected to hold the largest share of the automotive digital cockpit market in 2032."

The Asia Pacific accounted for the largest share of the automotive digital cockpit market in 2032. Strong vehicle production in China, India, Japan, and South Korea, combined with rapid EV adoption, is driving substantial demand for advanced cockpit systems. Automakers in the region are integrating digital clusters, infotainment units, passenger displays, and driver monitoring systems to meet rising customer expectations for connected and intelligent in-cabin experiences. Government support for electrification, connectivity standards, and safety compliance is further accelerating technology uptake. With continuous investments in software-defined vehicle platforms and cockpit electronics, the Asia Pacific region remains a crucial market for digital cockpit solutions.

Extensive primary interviews have been conducted with key industry experts in the automotive digital cockpit market to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

By Company Type -OEM - 45%, Tier 1 - 35%, and Others - 20%

By Designation -Directors- 35%, C- C-level Executives - 35%, and Others - 30%

By Region - Asia Pacific - 32%, Europe - 28%, North America - 36%, and RoW - 4%

The automotive digital cockpit market is dominated by a few globally established players, such as Continental AG, Robert Bosch GmbH, Denso Corporation, Visteon Corporation, and HARMAN International. The study includes an in-depth competitive analysis of these key players in the automotive digital cockpit market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the automotive digital cockpit market. It forecasts its size by equipment (infotainment unit, rear infotainment unit, passenger infotainment unit, HUD, digital instrument cluster, digital center console, driver monitoring system), by electric vehicle type (battery electric vehicle and plug in hybrid electric vehicle), by vehicle type (passenger car, light commercial vehicle, heavy commercial vehicle), by display type (LCD, OLED, TFT LCD), by display size (<5", 5 to 10", >10"), and by application (infotainment, driver monitoring & assistance, vehicle and comfort control system). It also discusses market drivers, restraints, opportunities, and challenges. The report provides detailed market analysis across four key regions (North America, Europe, the Asia Pacific, and the Rest of the World). The report includes a review of the supply chain and the competitive landscape of key players operating in the automotive digital cockpit ecosystem.

Key Benefits of Buying the Report:

Analysis of key drivers (growing consumer demand for premium in-cabin experiences, rising shift toward software-defined vehicles), restraints (high cost of advanced cockpit electronics), opportunities (growth in multimodal HMI, AR visualization, and interior sensing systems, increasing adoption of highway driving assist technology), challenges (increasing cybersecurity, data governance, and OTA coordination pressures, managing OTA complexity across distributed cockpit and vehicle compute units)

Service Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product launches in the automotive digital cockpit market

Market Development: Comprehensive information about lucrative markets by analyzing the automotive digital cockpit market across varied regions

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the automotive digital cockpit market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Continental AG, Robert Bosch GmbH, Denso Corporation, Visteon Corporation, and HARMAN International

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN AUTOMOTIVE DIGITAL COCKPIT MARKET

2.4 HIGH-GROWTH SEGMENTS IN AUTOMOTIVE DIGITAL COCKPIT MARKET

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE DIGITAL COCKPIT MARKET

3.2 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY EQUIPMENT

3.3 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY VEHICLE TYPE

3.4 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY APPLICATION

3.5 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY DISPLAY SIZE

3.6 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY EV TYPE

3.7 AUTOMOTIVE DIGITAL COCKPIT MARKET, BY DISPLAY TYPE