전력 조절 장치 시장 : 유형별, 상별, 최종 사용자별, 정격 전력별, 지역별 예측(-2030년)

Power Conditioning Unit Market by Type (Active, Passive), Phase (Single, Three), End User (Industrial & Manufacturing, Commercial, Utilities, Transportation, Residential, Healthcare), Power Rating, and Region - Global Forecast to 2030

상품코드:1881229

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 258 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

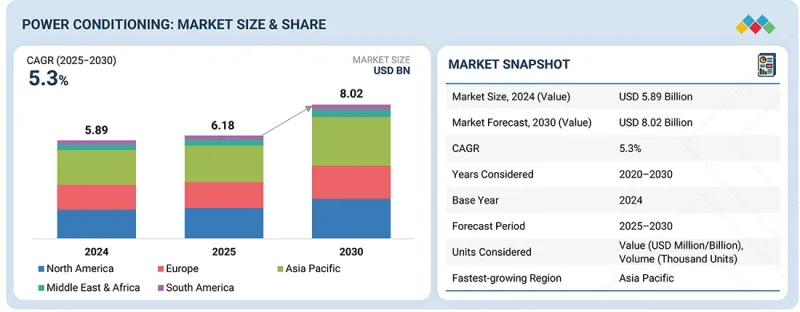

세계의 전력 조절 장치 시장 규모는 2025년 61억 8,000만 달러에서 2030년까지 80억 2,000만 달러에 이를 것으로 예상되며 CAGR로 5.3%를 나타낼 것으로 전망됩니다.

산업, 상업 및 주택 응용 분야에서 안정적이고 고품질의 전력에 대한 수요가 증가함에 따라 전력 조절 장치 시장은 성장 궤도를 타고 있습니다.

조사 범위

조사 대상 기간

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액, 1,000대

부문

유형, 상, 정격 전력, 최종 사용자

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 남미

신재생에너지 통합, 전기자동차 인프라, 데이터센터의 급속한 확대로 중단 없는 깨끗한 전력공급을 보장하는 첨단 전력조정 시스템에 대한 수요가 높아지고 있습니다. 에너지 효율을 촉진하는 정부의 지원책과 전력 품질 규제의 엄격화가 시장 채용을 더욱 가속화하고 있습니다. 전압 조정, 고조파 필터링 및 디지털 모니터링의 기술적 진보는 시스템의 신뢰성과 성능을 향상시키고 있습니다. 한편, 장비 제조업체, 유틸리티자 및 경영자의 파트너십은 대규모 배포와 장기적인 서비스 기회를 촉진하고 있습니다.

"상별로는 단상 부문이 2024년 2위 시장 점유율을 차지했습니다."

상별에서 단상 부문은 2024년에 두 번째로 큰 시장 점유율을 차지했습니다. 이 시스템은 주로 산업 용도에 비해 전력 수요가 비교적 낮은 주택, 소규모 사무실, 소매점, 경상업시설에서 사용됩니다. 가전, 홈 오토메이션 시스템, 소규모 재생에너지 설비의 채용의 확대에 따라, 전압의 안정성과 기기의 보호를 확보하는 단상 조절 장치 수요가 높아지고 있습니다. 게다가 컴팩트한 설계, 설치의 용이성, 비용 효율성이 뛰어나 분산형 부하가 작은 전력 용도에 최적이며, 신흥 경제권에서 안정적인 수요를 유지하고 있습니다.

"아시아태평양이 2024년 최대 점유율을 차지했습니다."

아시아태평양은 중국, 인도, 일본, 한국 등 국가의 급속한 산업화, 도시화, 제조 및 상업 인프라의 확대로 2024년 전력 조절 장치 시장에서 가장 큰 점유율을 차지했습니다. 전자, 자동차, 데이터센터 등의 부문에서 신뢰할 수 있는 고품질 전력에 대한 수요 증가는 전력조정시스템의 채용을 크게 촉진하고 있습니다. 신재생에너지 통합과 스마트 그리드 인프라에 대한 투자 증가는 이 지역 시장 성장을 더욱 강화하고 있습니다. 에너지 효율과 안정적인 전력 공급을 촉진하는 정부의 이니셔티브는 첨단 조정 기술의 개발을 장려하고 있습니다. 또한 비용 효율적인 솔루션을 제공하는 현지 제조업체의 강력한 존재가 시장에 대한 접근성을 높입니다. 이 지역에서 진행 중인 디지털 전환과 전력을 중시하는 업계의 성장은 전력 조절 장치 공급업체에게 강력한 기회를 창출하고 있습니다.

본 보고서는 세계의 전력 조절 장치 시장에 대해 조사 분석하여 주요 성장 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 주요 요약

제3장 중요한 지견

전력 조절 장치 시장 기업에게 매력적인 기회

전력 조절 장치 시장 : 지역별

전력 조절 장치 시장 : 정격전력별

전력 조절 장치 시장 : 상별

전력 조절 장치 시장 : 유형별

전력 조절 장치 시장 : 최종 사용자별

전력 조절 장치 시장 : 유형별, 지역별

제4장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

미충족 수요(Unmet Needs)와 화이트 스페이스

미충족 수요(Unmet Needs) : 전력 조절 장치 시장의 고객요구

화이트 스페이스 : 시장 주도의 기회

상호 연결된 시장 및 부문 간 기회

상호 연결된 시장

부문 간 기회

Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

Porter's Five Forces 분석

거시경제지표

서론

GDP의 동향과 예측

글로벌 유틸리티 산업 동향

글로벌 운송 산업 동향

공급망 분석

원재료 분석

최종 제품의 분석

생태계 분석

가격 설정 분석

전력 조절 장치의 참고 가격대 : 정격 전력별(2024년)

전력 조절 장치의 평균 판매 가격 동향 : 지역별(2021-2024년)

무역 분석

수입 시나리오(HS 코드 8535)

수출 시나리오(HS 코드 8535)

주요 컨퍼런스 및 이벤트(2025-2026년)

고객사업에 영향을 주는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

미국 관세의 영향(2025년) - 전력 조절 장치 시장

서론

주요 관세율

가격의 영향 분석

국가/지역에 미치는 영향

최종 사용자에게 미치는 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래의 용도

주요 신기술

액티브 고조파 필터

SVC, STATCOM

IoT 통합 스마트 UPS 시스템

보완 기술

에너지 저장 시스템

스마트 그리드와 첨단 측정

기술/제품 로드맵

단기(2025-2027년) | 기반 구축과 조기 상업화

중기(2027-2030년)|확장과 표준화

장기(2030-2035년 이후) | 대규모 상업화와 파괴적 변화

특허 분석

서론

조사 방법

문서의 유형

특허 활동의 인사이트

특허의 법적 지위

관할분석

주요 출원자

Qualcomm이 보유한 주요 특허 목록

SAMSUNG ELECTRONICS CO LTD가 보유한 주요 특허 목록

미래의 용도

스마트 그리드 : 차세대 그리드 안정성과 전압 최적화

데이터센터 : 에너지 효율이 높고 고조파가 적은 전력 인프라

전기자동차 충전 시스템 : 급속 충전의 신뢰성과 전력 품질 향상

신재생에너지 통합 : 그리드에 연결된 태양광 발전과 풍력 발전 최적화

산업 자동화 : 로보틱스와 공정 제어에 이용하는 고정밀 전력 조정

전력 조절 장치 시장에 대한 AI/생성형 AI의 영향

주요 이용 사례와 시장의 장래성

전력 조절 장치 시장에서의 OEM 모범 사례

전력 조절 장치 시장에서의 AI 도입에 관한 사례 연구

상호 연결된 생태계와 시장 기업에 미치는 영향

AI 통합 전력 조절 장치 채용에 대한 고객의 준비상황

성공 사례와 실제 적용 사례

ABB : 예지보전, 스마트 UPS, 그리드 최적화

SCHNEIDER ELECTRIC : ECOSTRUXURE POWER MONITORING/AUTOMATION

EATON : UPS와 산업용 전력 시스템

제7장 규제 정세와 지속가능성에 관한 대처

지역 규제 및 규정 준수

규제기관, 정부기관, 기타 조직

업계 표준

지속가능성에 대한 노력

지속가능성 대처에 대한 규제정책의 영향

인증, 라벨, 환경 기준

제8장 고객정세와 구매행동

서론

의사결정 프로세스

구매 프로세스에 관여하는 주요 이해관계자와 그 평가 기준

구매 프로세스의 주요 이해 관계자

구입 기준

채용 장벽과 내부 과제

다양한 최종 사용자의 미충족 수요(Unmet Needs)

시장의 수익성

잠재적인 수익

비용역학

마진 기회 : 최종 사용자별

제9장 전력 조절 장치 시장 : 유형별

서론

액티브

패시브

제10장 전력 조절 장치 시장 : 상별

서론

단상

삼상

제11장 전력 조절 장치 시장 : 정격전력별

서론

10KVA 이하

10-50KVA

50-150KVA

150KVA 초과

제12장 전력 조절 장치 시장 : 최종 사용자별

서론

산업 및 제조

상업

유틸리티

운송

주택

의료

제13장 전력 조절 장치 시장 : 지역별

서론

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

아시아태평양

중국

일본

인도

기타 아시아태평양

중동 및 아프리카

GCC

남아프리카

기타 중동 및 아프리카

남미

브라질

아르헨티나

베네수엘라

기타 남미

제14장 경쟁 구도

개요

주요 참가 기업의 전략/강점(2021년 8월-2025년 9월)

수익 분석(2020-2024년)

시장 점유율 분석(2024년)

기업 평가 및 재무 지표

브랜드/제품 비교

EATON

SCHNEIDER ELECTRIC

FUJI ELECTRIC CO., LTD.

EMERSON ELECTRIC CO.

AMETEK INC.

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제15장 기업 프로파일

주요 기업

EMERSON ELECTRIC CO.

AMETEK INC.

EATON

SCHNEIDER ELECTRIC

FUJI ELECTRIC CO., LTD.

ABB

MITSUBISHI ELECTRIC POWER PRODUCTS, INC.

ROCKWELL AUTOMATION

DELTA ELECTRONICS, INC.

LS ELECTRIC

POWER SYSTEMS & CONTROLS, INC.

TRYSTAR

NXT POWER, LLC

ASHLEY EDISON INTERNATIONAL LTD

QUALITY TRANSFORMER & ELECTRONICS, INC.

기타 기업

SERVOMAX LIMITED

FARMAX TECHNOLOGIES PVT.LTD

STACO ENERGY PRODUCTS CO.

SINALDA UK LIMITED

ACUMENTRICS

ELINEX POWER SOLUTIONS BV

MEIDENSHA CORPORATION

SPECTRUMSTAB INDIA PVT.LTD.

STATCON ELECTRONICS INDIA LIMITED

NISSIN ELECTRIC CO., LTD.

제16장 조사 방법

제17장 부록

KTH

영문 목차

영문목차

The global power conditioning unit market is projected to reach USD 8.02 billion by 2030 from USD 6.18 billion in 2025, registering a CAGR of 5.3%. The power conditioning unit market is on a growth trajectory driven by the increasing need for stable, high-quality power across industrial, commercial, and residential applications.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value, Volume (Thousand Units)

Segments

Type, Phase, Power rating, End User (Industry & Manufacturing Facilities, Commercial, Utilities, Transportation, Residential, Heal

Regions covered

North America, Europe, Asia Pacific, the Middle East & Africa, and South America

The rapid expansion of renewable energy integration, electric vehicle infrastructure, and data centers is boosting demand for advanced power conditioning systems to ensure an uninterrupted and clean power supply. Supportive government initiatives promoting energy efficiency, coupled with stricter power quality regulations, are further accelerating market adoption. Technological advancements in voltage regulation, harmonic filtration, and digital monitoring enhance system reliability and performance, while partnerships between equipment manufacturers, utilities, and industrial operators foster large-scale deployments and long-term service opportunities.

"By phase, the single-phase segment accounted for the second largest market share in 2024."

By phase, the single-phase segment accounted for the second-largest market share in 2024. These systems are primarily used in residential buildings, small offices, retail outlets, and light commercial facilities where the power demand is relatively lower compared to industrial applications. The growing adoption of electronic appliances, home automation systems, and small-scale renewable installations has fueled demand for single-phase conditioners to ensure voltage stability and equipment protection. Additionally, their compact design, ease of installation, and cost-effectiveness make them ideal for decentralized and small-load power applications, sustaining their steady demand across emerging economies.

"By type, the passive segment accounted for the largest market in 2024."

By type, the passive power conditioner segment accounted for the second-largest market share in 2024. Passive power conditioners are widely used in applications where basic voltage regulation, noise filtering, and surge protection are required without active electronic components. Their simple design, high reliability, and low maintenance needs make them a preferred choice for small-scale and cost-sensitive installations across residential, commercial, and light industrial sectors. Growing demand for affordable power quality solutions, particularly in developing regions with unstable grid conditions, continues to support the adoption of passive power conditioners in the global market. The rising integration of passive units in consumer electronics and office equipment enhances their utility in safeguarding sensitive devices. Increasing focus on cost optimization and energy-efficient infrastructure also contributes to the steady market growth of this segment.

"Asia Pacific accounted for the largest region in 2024."

Asia Pacific held the largest share in the power conditioning unit market in 2024, driven by rapid industrialization, urbanization, and the expansion of manufacturing and commercial infrastructure across countries such as China, India, Japan, and South Korea. The growing demand for reliable and high-quality power in sectors like electronics, automotive, and data centers has significantly boosted the adoption of power conditioning systems. Increasing investments in renewable energy integration and smart grid infrastructure further strengthen market growth in the region. Government initiatives promoting energy efficiency and stable power supply are encouraging the deployment of advanced conditioning technologies. Additionally, the strong presence of local manufacturers offering cost-effective solutions enhances market accessibility. The region's ongoing digital transformation and growth in power-sensitive industries continue to create robust opportunities for power conditioning unit suppliers.

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 57%, Tier 2 - 29%, and Tier 3 - 14%

By Designation: C-Level Executives - 35%, Directors - 20%, and Others - 45%

By Region: North America - 20%, Europe - 15%, Asia Pacific - 30%, Middle East & Africa - 25%, and South America - 10%

Note: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million. Others include sales managers, engineers, and regional managers.

ABB (Switzerland), Eaton (Ireland), Schneider Electric (France), Mitsubishi Electric Power Products Inc. (US), Emerson Electric Co. (US), Delta Electronics, Inc. (Taiwan), Power Systems & Controls, Inc. (US), Trystar (US), AMETEK Inc. (US), Fuji Electric Co., Ltd. (Japan), Rockwell Automation (US), NXT Power, LLC (US), Quality Transformer & Electronics, Inc. (US), Servomax Limited (India), Farmax Technologies Pvt. Ltd. (India), STACO ENERGY PRODUCTS CO. (US), LS ELECTRIC (South Korea), ASHLEY EDISON INTERNATIONAL LTD (UK), Singadia UK Limited (UK), SPECTRUMSTAB INDIA PVT. LTD. (India), Acumentrics (US), Statcon Electronics India Limited (India), Elinex Power Solutions B.V. (Netherlands), MEIDENSHA CORPORATION (Japan), and NISSIN ELECTRIC Co., Ltd. (Japan) are some of the key players in the power conditioning unit market. The study includes an in-depth competitive analysis of these key players in the market, with their company profiles, recent developments, and key market strategies.

Study Coverage

The report defines, describes, and forecasts the power conditioning unit market type (active power conditioner, passive power conditioner), phase (single phase, three phase), power rating (<=10 kVA, 10-50 kVA, 50-150 kVA, >150 kVA), end user (industry & manufacturing facility, commercial, utilities, transportation, residential, healthcare), and region (North America, Europe, Asia Pacific, Middle East & Africa and South America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the power conditioning unit market. A thorough analysis of the key industry players has provided insights into their business overview, solutions, and services; key strategies such as contracts, partnerships, agreements, expansion, Joint ventures, collaborations, and acquisitions; and recent developments associated with the market. This report covers the competitive analysis of upcoming startups in the power conditioning unit market ecosystem.

Key Benefits of Buying the Report

The report includes the analysis of key drivers (rising adoption of renewable and distributed energy growth is boosting demand for efficient power conditioning, burgeoning semiconductor industry is driving demand for advanced power conditioning solutions), restraints (integration challenges with existing infrastructure restrain the adoption of new power conditioners, competition from alternative solutions), opportunities (rising data center demand and IoT growth drive the need for reliable, high-availability power conditioning systems, increasing demand for clean and stable power in critical infrastructure such as healthcare, IT, and defense is creating new growth revenues) and challenges (high costs of power conditioners may limit adoption among small and medium-sized businesses, Compliance and Regulatory Standards Influence market adoption).

Product Development/Innovation: Power conditioning unit market players are actively developing advanced technologies to enhance power quality, reliability, and efficiency across diverse applications. In design and components, innovations such as high-frequency transformers, silicon carbide (SiC) and gallium nitride (GaN) semiconductors, and advanced harmonic filters are improving response times and energy efficiency. Manufacturers also integrate digital monitoring systems, IoT connectivity, and AI-based analytics to enable predictive maintenance and real-time performance optimization. In renewable and grid-connected systems, next-generation power conditioners are being engineered to handle voltage fluctuations, harmonics, and intermittent loads more effectively. Furthermore, modular and scalable architectures are gaining traction, allowing flexible deployment across industrial, commercial, and residential sectors while reducing overall lifecycle costs.

Market Development: In March 2024, Schneider Electric invested USD 140 million to expand its US manufacturing capabilities, focusing on critical infrastructure and data center solutions. The investment includes USD 85 million to transform a 500,000-square-foot facility in Mt. Juliet, Tennessee, and upgrade operations in Smyrna, Tennessee, producing custom electrical switch gear, medium-voltage power distribution products, and power conditioning equipment.

Market Diversification: The report offers a comprehensive analysis of the strategies employed by power conditioners solutions provider players to facilitate market diversification. It outlines innovative products and operating models, as well as new partnership frameworks across various regions, underpinned by technology-driven business lines. The findings emphasize opportunities for expansion beyond traditional operations, identifying geographical areas and customer segments that are currently served but remain underserved and are suitable for strategic entry.

Competitive Assessment: The report provides in-depth assessment of market shares, growth strategies, and service offerings of leading players such as ABB (Switzerland), Eaton (Ireland), Schneider Electric (France), Mitsubishi Electric Power Products Inc. (US), Emerson Electric Co. (US), Delta Electronics, Inc. (Taiwan), Power Systems & Controls, Inc. (US), Trystar (US), AMETEK Inc. (US), Fuji Electric Co., Ltd. (Japan), Rockwell Automation (US), NXT Power, LLC (US), Quality Transformer & Electronics, Inc. (US), and Servomax Limited (India), among others, in the power conditioning unit market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIONS SHAPING POWER CONDITIONING UNIT MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POWER CONDITIONING UNIT MARKET

3.2 POWER CONDITIONING UNIT MARKET, BY REGION

3.3 POWER CONDITIONING UNIT MARKET, BY POWER RATING

3.4 POWER CONDITIONING UNIT MARKET, BY PHASE

3.5 POWER CONDITIONING UNIT MARKET, BY TYPE

3.6 POWER CONDITIONING UNIT MARKET, BY END USER

3.7 POWER CONDITIONING UNIT MARKET, BY TYPE AND REGION

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Expansion of renewable and distributed energy systems

4.2.1.2 Booming semiconductor industry

4.2.2 RESTRAINTS

4.2.2.1 Limited demand from SMEs due to budget constraints

4.2.2.2 Availability of substitute technologies

4.2.3 OPPORTUNITIES

4.2.3.1 Rising demand for data centers and IoT devices

4.2.3.2 Escalating need for clean and stable power supply in healthcare, IT, and defense infrastructure

4.2.4 CHALLENGES

4.2.4.1 Complexities associated with reengineering legacy systems for future-ready power infrastructure

4.2.4.2 Hidden cost of compliance and inconsistent regulatory standards

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS: CUSTOMER REQUIREMENTS IN POWER CONDITIONING UNIT MARKET

4.3.2 WHITE SPACES: MARKET-DRIVEN OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN GLOBAL UTILITIES INDUSTRY

5.2.4 TRENDS IN GLOBAL TRANSPORTATION INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.3.1 RAW MATERIAL ANALYSIS

5.3.2 FINAL PRODUCT ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 INDICATIVE PRICING RANGE OF POWER CONDITIONING UNITS, BY POWER RATING, 2024

5.5.2 AVERAGE SELLING PRICE TREND OF POWER CONDITIONING UNITS, BY REGION, 2021-2024

5.6 TRADE ANALYSIS

5.6.1 IMPORT SCENARIO (HS CODE 8535)

5.6.2 EXPORT SCENARIO (HS CODE 8535)

5.7 KEY CONFERENCES AND EVENTS, 2025-2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 DATA CENTER ACHIEVES COST SAVINGS AND MINIMIZES DOWNTIME THROUGH ADVANCED POWER CONDITIONING SOLUTIONS

5.10.2 MANUFACTURING FACILITY ENHANCES PRODUCTION EFFICIENCY BY DEPLOYING INTELLIGENT POWER CONDITIONERS

5.10.3 SOLAR POWER PLANT ENHANCES SOLAR UTILIZATION BY INTEGRATING ADVANCED POWER CONDITIONERS INTO GRID-TIED INVERTERS

5.11 IMPACT OF 2025 US TARIFF - POWER CONDITIONING UNIT MARKET

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRIES/REGIONS

5.11.4.1 US

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 ACTIVE HARMONIC FILTERS

6.1.2 STATIC VAR COMPENSATORS AND STATIC SYNCHRONOUS COMPENSATORS

6.1.3 IOT-INTEGRATED SMART UPS SYSTEMS

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 ENERGY STORAGE SYSTEMS

6.2.2 SMART GRID AND ADVANCED METERING

6.3 TECHNOLOGY/PRODUCT ROADMAP

6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION