반도체 세라믹 패키징 재료 시장 : 재료별, 패키징 기술별, 최종 이용 산업별, 지역별 - 예측(-2030년)

Semiconductor Ceramic Packaging Materials Market by Material, Packaging Technology, End-use Industry, & Region - Global Forecast to 2030

상품코드:1881221

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 272 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

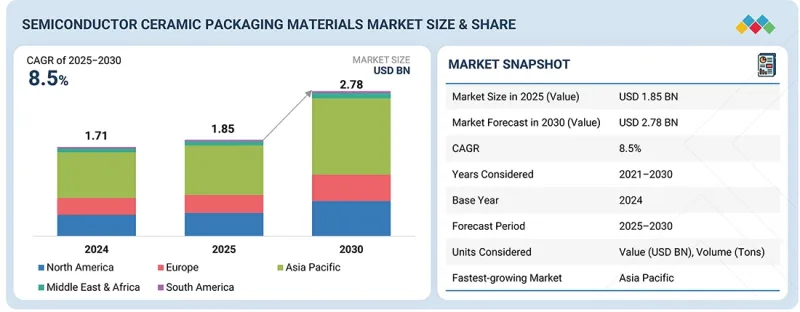

반도체 세라믹 패키징 재료 시장 규모는 2025년 18억 5,000만 달러에서 2030년까지 27억 8,000만 달러로 성장하고, 예측 기간 중에 CAGR 8.5%를 나타낼 전망입니다.

조사 범위

조사 대상 기간

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

가치(100만/10억 달러), 톤

부문

재료별, 패키징 기술별, 최종 이용 산업별, 지역별

대상 지역

아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미

현대 전자기기의 복잡성 및 소형화에 따라 열을 안정적으로 관리하고 신호의 무결성을 유지할 수 있는 패키징이 요구됨에 따라 반도체 세라믹 패키징 재료에 대한 수요가 증가하고 있습니다. 전기자동차, 산업 자동화, 첨단 의료기기 등 고출력, 고주파 용도의 채용 확대에 따라 열전도율과 기계적 강도가 우수한 소재의 필요성이 증가하고 있습니다.

또한, 고밀도 멀티칩 모듈 및 시스템 인 패키지 설계로의 전환에 따라 정밀한 조립과 장기적인 신뢰성을 지원하는 세라믹이 요구되고 있습니다. 무독성, 내구성, 안정성이 뛰어난 소재에 대한 환경 규제와 법규 강화도 기존 패키징재보다 세라믹을 유리하게 만들고 있습니다. 이러한 기술적, 산업적, 규제적 압력이 결합되어 시장 수요의 지속적인 성장을 가속하고 있습니다.

알루미나는 다양한 응용 분야에서 입증된 신뢰성, 범용성, 비용 효율성으로 인해 반도체용 세라믹 패키지 재료 시장에서 가장 큰 점유율을 차지하고 있습니다. 우수한 열전도율, 뛰어난 전기 절연성, 높은 기계적 강도를 결합하여 저전력 및 고파워 반도체 소자의 성능 요구 사항을 모두 충족시킬 수 있습니다. 알루미나는 동시 소성 및 금속화 기술을 포함한 기존 제조 공정과 호환되며, 결함을 최소화하면서 확장 가능한 생산을 가능하게 합니다. 다른 재료와 비교하여 쉽게 구할 수 있고 원자재 비용이 상대적으로 낮기 때문에 대량 시장 응용 분야에서 선호되는 선택이 되고 있습니다. 또한, 열 사이클 및 가혹한 환경 조건에서의 안정성은 장치의 장기적인 성능을 보장하고 시장에서의 우위를 더욱 공고히 합니다.

반도체 세라믹 패키징 재료 시장에서 가장 큰 비중을 차지하고 있는 분야는 소비자용 전자제품으로, 이 분야가 신뢰성과 내구성이 뛰어난 반도체 부품에 대한 대량 수요를 주도하고 있기 때문입니다. 스마트폰, 노트북, 태블릿, 오디오 기기, 웨어러블 기술 등 전 세계적으로 전자기기 소비가 빠르게 증가함에 따라 잦은 사용과 다양한 환경 조건에서도 성능을 유지할 수 있는 패키징재에 대한 요구가 증가하고 있습니다. 제조업체는 장기적인 안정성을 보장하고 기기 고장을 최소화할 수 있는 부품을 우선적으로 채택함으로써 브랜드 평가와 고객 만족을 뒷받침하고 있습니다. 첨단 디스플레이, 처리 능력, 연결 기능 등 다양한 제품군과 지속적인 기술 혁신이 세라믹 패키징재 수요의 주요 견인차 역할을 하고 있습니다.

표면 실장 패키지(Leadless)는 기존의 관통 홀 방식에 비해 반도체 소자를 보다 정밀하고 효율적으로 실장할 수 있어 반도체 세라믹 패키징 재료 시장에서 가장 큰 점유율을 차지하고 있습니다. 이 기술은 인쇄 회로 기판에 부품의 고밀도 실장을 지원하여 첨단 전자기기의 컴팩트한 설계와 신호 무결성 향상을 실현합니다. 또한 기계적 안정성을 높이고 솔더 조인트의 고장 위험을 줄이기 위해 자동차, 항공우주, 고성능 컴퓨팅 분야에서의 응용에 매우 중요합니다. 또한, 리드리스 표면실장기술은 자동화된 제조 및 검사 공정과 호환되어 생산 속도와 일관성 향상에 기여합니다. 소형화, 고주파 동작, 안정적인 열 관리 지원 능력으로 인해 이 패키징 기술은 현대 반도체 용도에서 최적의 선택이 되어 시장 성장을 주도하고 있습니다.

아시아태평양은 반도체 세라믹 패키징 재료 시장에서 가장 큰 점유율을 차지하고 있습니다. 이 지역이 반도체 조립, 테스트, 패키징 업무의 세계적인 거점이기 때문입니다. 첨단 패키징 기술 연구개발에 대한 적극적인 투자가 고성능 세라믹 소재 수요를 견인하고 있습니다. 중국, 대만, 한국 등의 국가에 집중된 전자제품 제조 클러스터는 효율적인 생산과 새로운 패키징 솔루션의 신속한 도입을 가능하게 합니다. 또한, 지역 사업 및 제휴 관계를 구축하는 국제 반도체 기업의 존재감이 높아지고 있는 것도 세라믹 소재의 소비 확대에 기여하고 있습니다. 지원적인 산업 정책, 수출 지향적 생산, 그리고 첨단 전자제품에 대한 국내 수요 증가는 이 지역 시장 우위를 더욱 강화시키고 있습니다.

세계의 반도체 세라믹 패키징 재료 시장에 대해 조사했으며, 재료별/패키징 기술별/최종 이용 산업별/지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

생성형 AI

반도체 세라믹 패키징 재료 시장에 대한 영향

제6장 업계 동향

서론

고객의 비즈니스에 영향을 미치는 동향/혼란

공급망 분석

2025년 미국 관세의 영향-반도체 세라믹 패키징 재료 시장

투자 환경과 자금조달 시나리오

가격 분석

생태계 분석

기술 분석

특허 분석

무역 분석

2026-2027년 주요 컨퍼런스 및 이벤트

관세 및 규제 상황

기준과 규제 상황

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 전망

사례 연구 분석

제7장 반도체 세라믹 패키징 재료 시장(재료별)

서론

알루미나

질화알루미늄

질화규소

탄화규소

산화베릴륨

기타

제8장 반도체 세라믹 패키징 재료 시장(패키징 기술별)

서론

스루홀 패키지

표면 실장 패키지 - LEADED

표면 실장 패키지 - LEADLESS

첨단 소형 패키지

기타 패키징 기술

제9장 반도체 세라믹 패키징 재료 시장(최종 이용 산업별)

서론

가전

자동차

건강 관리

IT 및 통신

항공우주 및 방위

기타 최종 이용 산업

제10장 반도체 세라믹 패키징 재료 시장(지역별)

서론

아시아태평양

중국

일본

인도

한국

대만

기타

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

프랑스

영국

스페인

기타

중동 및 아프리카

GCC 국가

남미

아르헨티나

브라질

기타

제11장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

시장 점유율 분석, 2024년

매출 분석, 2021년-2024년

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

브랜드/제품 비교

기업 평가와 재무 지표

경쟁 시나리오와 동향

제12장 기업 개요

주요 시장 진출기업

KYOCERA CORPORATION

CERAMTEC GMBH

COORSTEK

MORGAN ADVANCED MATERIALS

NGK INSULATORS, LTD.

MARUWA CO., LTD.

AGC INC.

MATERION CORPORATION

TOKUYAMA CORPORATION

FERROTEC CORPORATION

기타 기업

GREAT CERAMIC

ADTECH CERAMICS

XIAMEN MASCERA TECHNOLOGY CO., LTD.

ORTECH, INC.

ADVANCED CERAMIC MATERIALS

STC MATERIAL SOLUTIONS

NISHIMURA ADVANCED CERAMICS CO., LTD.

JAPAN FINE CERAMICS CO., LTD.

WUXI SPECIAL CERAMIC ELECTRICAL CO., LTD.

JINGHUI INDUSTRY LTD.

FUJIAN HUAQING ELECTRONIC MATERIAL TECHNOLOGY CO., LTD.

HEBEI SUOYI NEW MATERIAL TECHNOLOGY CO., LTD.

NTK CERATEC CO., LTD.

XIAMEN INNOVACERA ADVANCED MATERIALS CO., LTD

XIAMEN FINE CERAMICS TECHNOLOGY CO., LTD.

제13장 부록

LSH

영문 목차

영문목차

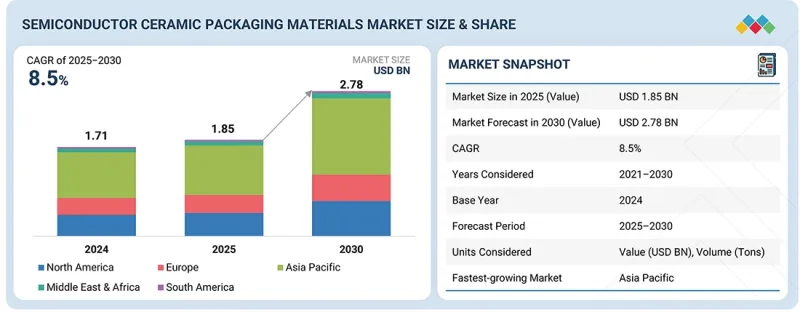

The semiconductor ceramic packaging materials market size is projected to grow from USD 1.85 billion in 2025 to USD 2.78 billion by 2030, registering a CAGR of 8.5% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion), Volume (Tons)

Segments

Material, Packaging Technology, End-use Industry, and Region

Regions covered

Asia Pacific, North America, Europe, the Middle East & Africa, and South America

The demand for semiconductor ceramic packaging materials is increasing due to the growing complexity and miniaturization of modern electronic devices, which require packaging that can reliably manage heat and maintain signal integrity. Rising adoption of high-power and high-frequency applications, such as electric vehicles, industrial automation, and advanced medical devices, is driving the need for materials with superior thermal conductivity and mechanical strength.

Additionally, the shift toward high-density multi-chip modules and system-in-package designs requires ceramics that can support precise assembly and long-term reliability. Increasing environmental and regulatory requirements for non-toxic, durable, and stable materials also favor ceramics over traditional packaging. These combined technological, industrial, and regulatory pressures are collectively fueling sustained growth in market demand.

"By material, the alumina segment is anticipated to account for the largest market share during the forecast period"

Alumina accounts for the largest share in the semiconductor ceramic packaging materials market due to its proven reliability, versatility, and cost-effectiveness across a wide range of applications. Its combination of good thermal conductivity, excellent electrical insulation, and high mechanical strength allows it to meet the performance requirements of both low- and high-power semiconductor devices. Alumina is compatible with established manufacturing processes, including co-firing and metallization techniques, enabling scalable production with minimal defects. Its widespread availability and relatively lower raw material cost compared to other materials make it a preferred choice for mass-market applications. Additionally, alumina's stability under thermal cycling and harsh environmental conditions ensures long-term device performance, reinforcing its dominant position in the market.

"By end-use industry, the consumer electronics segment is anticipated to account for the largest market share during the forecast period"

Consumer electronics account for the largest share of the semiconductor ceramic packaging materials market because the sector drives high-volume demand for reliable and durable semiconductor components. Rapid growth in global electronics consumption, including smartphones, laptops, tablets, audio devices, and wearable technology, increases the need for packaging materials that can maintain performance under frequent use and varying environmental conditions. Manufacturers prioritize components that ensure long-term stability and minimize device failure, supporting brand reputation and customer satisfaction. The wide variety of products and continuous technological upgrades in this industry, including advanced displays, processing power, and connectivity features, make consumer electronics the primary driver of ceramic packaging material demand.

"By packaging technology, the surface mount packages - leadless segment is anticipated to account for the largest market share during the forecast period"

Surface mount packages- leadless account for the largest share in the semiconductor ceramic packaging materials market because they allow for more precise and efficient assembly of semiconductor devices compared to traditional through-hole methods. This technology supports higher component density on printed circuit boards, enabling compact designs and improved signal integrity in advanced electronics. It also enhances mechanical stability and reduces the risk of solder joint failures, which is critical for applications in automotive, aerospace, and high-performance computing. Additionally, leadless surface mount technology is compatible with automated manufacturing and inspection processes, improving production speed and consistency. Its ability to support miniaturization, high-frequency operation, and reliable thermal management makes this packaging technology the preferred choice for modern semiconductor applications, driving its growth in the market.

"Asia Pacific is anticipated to account for the largest market share during the forecast period"

Asia Pacific holds the largest share in the semiconductor ceramic packaging materials market because the region is a global hub for semiconductor assembly, testing, and packaging operations. Strong investments in research and development of advanced packaging technologies drive demand for high-performance ceramic materials. The concentration of electronics manufacturing clusters in countries like China, Taiwan, and South Korea enables efficient production and rapid adoption of new packaging solutions. Additionally, the growing presence of international semiconductor companies establishing regional operations and partnerships increases the consumption of ceramic materials. Supportive industrial policies, export-oriented production, and rising domestic demand for advanced electronics further strengthen the region's market dominance.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the semiconductor ceramic packaging materials market, and information was gathered from secondary research to determine and verify the market size of several segments.

By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

By Designation: Managers- 15%, Directors - 20%, and Others - 65%

By Region: North America - 30%, Europe - 25%, Asia Pacific - 35%, the Middle East & Africa -5%, and South America- 5%

The semiconductor ceramic packaging materials market comprises major KYOCERA Corporation (Japan), CeramTec GmbH (Germany), CoorsTek (US), Materion Corporation (US), Resonac Holdings Corporation (Japan), NGK INSULATORS, LTD. (Japan), AGC Inc. (Japan), Morgan Advanced Materials (UK), MARUWA Co., Ltd. (Japan), and Tokuyama Corporation (Japan). The study includes an in-depth competitive analysis of these key players in the semiconductor ceramic packaging materials market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the semiconductor ceramic packaging materials market on the basis of material, packaging technology, end-use industry, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the semiconductor ceramic packaging materials market.

Key Benefits of Buying This Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the semiconductor ceramic packaging materials market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of drivers (expansion of automotive electronics and EV power modules boosting ceramic packaging adoption), restraints (high cost of ceramic packaging materials compared to polymer or metal-based packaging), opportunities (regional localization of semiconductor manufacturing encouraging investment), and challenges (limited design flexibility of ceramic materials makes fabricating complex geometries challenging) influencing the growth of semiconductor ceramic packaging materials market.

Market Penetration: Comprehensive information on the semiconductor ceramic packaging materials offered by top players in the global semiconductor ceramic packaging materials market.

Product Development/Innovation: Detailed insights on upcoming technologies, expansions, and partnerships in the semiconductor ceramic packaging materials market.

Market Development: Comprehensive information about lucrative emerging markets, the report analyzes the markets for semiconductor ceramic packaging materials market across regions.

Market Capacity: Production capacity of the companies is provided wherever available with upcoming capacities for the semiconductor ceramic packaging materials market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the semiconductor ceramic packaging materials market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key primary sources

2.1.2.3 Key players for primary interviews

2.1.2.4 Breakdown of interviews with experts

2.1.2.5 Key industry insights

2.2 BASE NUMBER CALCULATION

2.2.1 SUPPLY-SIDE ANALYSIS

2.2.2 DEMAND-SIDE ANALYSIS

2.3 GROWTH FORECAST

2.3.1 SUPPLY SIDE

2.3.2 DEMAND SIDE

2.4 MARKET SIZE ESTIMATION

2.4.1 BOTTOM-UP APPROACH

2.4.2 TOP-DOWN APPROACH

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTION

2.7 GROWTH FORECAST

2.8 RISK ASSESSMENT

2.9 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET

4.2 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY MATERIAL

4.3 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY PACKAGING TECHNOLOGY

4.4 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY END-USE INDUSTRY

4.5 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Expansion of automotive electronics and EV power modules

5.2.1.2 Growth in 5G infrastructure and RF devices

5.2.2 RESTRAINTS

5.2.2.1 Higher cost of ceramic packaging materials than polymer or metal-based packaging

5.2.3 OPPORTUNITIES

5.2.3.1 Regional localization of semiconductor manufacturing encouraging investment

5.2.3.2 Advanced multilayer ceramic materials for emerging 2.5D/ 3D semiconductor packaging

5.2.4 CHALLENGES

5.2.4.1 Difficulty in bonding to dissimilar materials

5.2.4.2 Limited design flexibility makes fabricating complex geometries challenging

5.3 GENERATIVE AI

5.3.1 INTRODUCTION

5.4 IMPACT ON SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET

6 INDUSTRY TRENDS

6.1 INTRODUCTION

6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.3 SUPPLY CHAIN ANALYSIS

6.4 IMPACT OF 2025 US TARIFF -SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET

6.4.1 INTRODUCTION

6.4.2 KEY TARIFF RATES

6.4.3 PRICE IMPACT ANALYSIS

6.4.4 IMPACT ON REGION

6.4.4.1 North America

6.4.4.2 Europe

6.4.4.3 Asia Pacific

6.4.5 IMPACT ON END-USE INDUSTRY

6.5 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE TREND OF SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY REGION, 2021-2024

6.6.2 AVERAGE SELLING PRICE TREND OF SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY MATERIAL, 2021-2024

6.6.3 AVERAGE SELLING PRICE TREND OF SEMICONDUCTOR CERAMIC PACKAGING MATERIALS, BY KEY PLAYER, 2024

6.7 ECOSYSTEM ANALYSIS

6.8 TECHNOLOGY ANALYSIS

6.8.1 KEY TECHNOLOGIES

6.8.2 COMPLEMENTARY TECHNOLOGIES

6.8.3 ADJACENT TECHNOLOGIES

6.9 PATENT ANALYSIS

6.9.1 METHODOLOGY

6.9.2 PATENTS GRANTED WORLDWIDE, 2015-2024

6.9.2.1 Patent publication trends

6.9.3 INSIGHTS

6.9.4 LEGAL STATUS OF PATENTS

6.9.5 JURISDICTION ANALYSIS

6.9.6 TOP APPLICANTS

6.9.7 LIST OF MAJOR PATENTS

6.10 TRADE ANALYSIS

6.10.1 IMPORT SCENARIO (HS CODE 85419000)

6.10.2 EXPORT SCENARIO (HS CODE 85419000)

6.11 KEY CONFERENCES AND EVENTS, 2026-2027

6.12 TARIFF AND REGULATORY LANDSCAPE

6.12.1 TARIFF ANALYSIS

6.13 STANDARDS AND REGULATORY LANDSCAPE

6.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.13.2 STANDARDS

6.14 PORTER'S FIVE FORCES ANALYSIS

6.14.1 THREAT OF NEW ENTRANTS

6.14.2 THREAT OF SUBSTITUTES

6.14.3 BARGAINING POWER OF SUPPLIERS

6.14.4 BARGAINING POWER OF BUYERS

6.14.5 INTENSITY OF COMPETITIVE RIVALRY

6.15 KEY STAKEHOLDERS AND BUYING CRITERIA

6.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.15.2 BUYING CRITERIA

6.16 MACROECONOMIC OUTLOOK

6.16.1 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

6.17 CASE STUDY ANALYSIS

6.17.1 LOW THERMAL RESISTANCE PACKAGING FOR HIGH POWER ELECTRONICS

6.17.2 EFFECTS OF BETA-SI3N4 SEEDS ON MICROSTRUCTURE AND PERFORMANCE OF SI3N4 CERAMICS IN SEMICONDUCTOR PACKAGE

6.17.3 PREPARATION OF DIAMOND FILM SUBSTRATES ON ALN CERAMIC AND THEIR PERFORMANCE IN LED PACKAGING

7 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY MATERIAL

7.1 INTRODUCTION

7.2 ALUMINA

7.2.1 HIGH-TEMPERATURE PERFORMANCE IN SEMICONDUCTOR DEVICES TO DRIVE DEMAND

7.3 ALUMINUM NITRIDE

7.3.1 SUPERIOR THERMAL AND ELECTRICAL PROPERTIES TO DRIVE MARKET

7.4 SILICON NITRIDE

7.4.1 HIGH MECHANICAL STRENGTH AND THERMAL SHOCK RESILIENCE TO DRIVE DEMAND

7.5 SILICON CARBIDE

7.5.1 MATERIAL ADVANCEMENTS TO DRIVE HIGH DENSITY AND THERMALLY STABLE CHIP PACKAGING

7.6 BERYLLIUM OXIDE

7.6.1 EFFICIENT HEAT DISSIPATION TO DRIVE NEXT-GENERATION HIGH-POWER PACKAGE DESIGNS

7.7 OTHER MATERIALS

7.7.1 BORON NITRIDE

7.7.2 ZIRCONIA

8 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY PACKAGING TECHNOLOGY

8.1 INTRODUCTION

8.2 THROUGH-HOLE PACKAGES

8.2.1 ENHANCED DEVICE DURABILITY AND THERMAL PERFORMANCE TO DRIVE DEMAND

8.3 SURFACE MOUNT PACKAGES - LEADED

8.3.1 EFFICIENT ASSEMBLY AND RELIABLE PERFORMANCE TO DRIVE DEMAND

8.4 SURFACE MOUNT PACKAGES - LEADLESS

8.4.1 SUPERIOR ELECTRICAL PERFORMANCE AND EFFICIENT MANUFACTURING TO DRIVE DEMAND

8.5 ADVANCED MINIATURIZED PACKAGES

8.5.1 HIGH-PERFORMANCE INTEGRATION AND EFFICIENT CONNECTIVITY TO DRIVE MARKET

8.6 OTHER PACKAGING TECHNOLOGIES

8.6.1 FLIP-CHIP CERAMIC PACKAGES

8.6.2 MULTI-CHIP MODULES

9 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 CONSUMER ELECTRONICS

9.2.1 INCREASE IN ADVANCED CERAMIC PACKAGING ADOPTION FOR HIGH-PERFORMANCE, RELIABLE DEVICES

9.3 AUTOMOTIVE

9.3.1 RISE IN VEHICLE PRODUCTION TO DRIVE MARKET

9.4 HEALTHCARE

9.4.1 EXPANSION OF HEALTHCARE MARKETS TO DRIVE DEMAND FOR HIGH-PERFORMANCE PACKAGING MATERIALS

9.5 IT & TELECOMMUNICATION

9.5.1 5G AND DIGITAL INFRASTRUCTURE EXPANSION TO DRIVE DEMAND

9.6 AEROSPACE & DEFENSE

9.6.1 NEXT-GENERATION AEROSPACE TECHNOLOGIES TO DRIVE HIGH-PERFORMANCE PACKAGING ADOPTION

9.7 OTHER END-USE INDUSTRIES

9.7.1 RAIL & TRANSPORTATION

9.7.2 RENEWABLE ENERGY

10 SEMICONDUCTOR CERAMIC PACKAGING MATERIALS MARKET, BY REGION

10.1 INTRODUCTION

10.2 ASIA PACIFIC

10.2.1 CHINA

10.2.1.1 Rapid growth of 5G infrastructure and consumer electronics market

10.2.2 JAPAN

10.2.2.1 Continuous investment in R&D for semiconductor packaging materials

10.2.3 INDIA

10.2.3.1 Government incentives through India Semiconductor Mission

10.2.4 SOUTH KOREA

10.2.4.1 Presence of major semiconductor manufacturers like Samsung and SK hynix

10.2.5 TAIWAN

10.2.5.1 Leadership in semiconductor manufacturing

10.2.6 REST OF ASIA PACIFIC

10.3 NORTH AMERICA

10.3.1 US

10.3.1.1 Strong semiconductor, aerospace, and defense industries

10.3.2 CANADA

10.3.2.1 Expansion of technology infrastructure

10.3.3 MEXICO

10.3.3.1 Emergence as manufacturing hub to drive demand

10.4 EUROPE

10.4.1 GERMANY

10.4.1.1 Growth in automotive manufacturing and ADAS integration

10.4.2 ITALY

10.4.2.1 Industrial automation and IoT electronics growth

10.4.3 FRANCE

10.4.3.1 High investment in medical electronics demanding hermetic ceramic packages

10.4.4 UK

10.4.4.1 Government initiatives for semiconductor sovereignty

10.4.5 SPAIN

10.4.5.1 Support for local semiconductor and electronics production

10.4.6 REST OF EUROPE

10.5 MIDDLE EAST & AFRICA

10.5.1 GCC COUNTRIES

10.5.1.1 Saudi Arabia

10.5.1.1.1 Saudi Arabia's Vision 2030 spurs investment

10.5.1.2 UAE

10.5.1.2.1 National Strategy for Advanced Industries (Operation 300bn)

10.5.1.3 Rest of GCC countries

10.5.1.4 South Africa

10.5.1.4.1 Expansion in automotive component manufacturing

10.5.1.5 Rest of Middle East & Africa

10.6 SOUTH AMERICA

10.6.1 ARGENTINA

10.6.1.1 Industrial modernization and import substitution

10.6.2 BRAZIL

10.6.2.1 Growing industrial and consumer electronics production

10.6.3 REST OF SOUTH AMERICA

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3 MARKET SHARE ANALYSIS, 2024

11.4 REVENUE ANALYSIS, 2021-2024

11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.5.1 STARS

11.5.2 EMERGING LEADERS

11.5.3 PERVASIVE PLAYERS

11.5.4 PARTICIPANTS

11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.5.5.1 Company footprint

11.5.5.2 Region footprint

11.5.5.3 Material footprint

11.5.5.4 Packaging technology footprint

11.5.5.5 End-use industry footprint

11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

11.6.1 PROGRESSIVE COMPANIES

11.6.2 RESPONSIVE COMPANIES

11.6.3 DYNAMIC COMPANIES

11.6.4 STARTING BLOCKS

11.6.5 COMPETITIVE BENCHMARKING

11.6.5.1 Detailed list of key startups/SMEs

11.6.5.2 Competitive benchmarking of key startups/SMEs

11.7 BRAND/PRODUCT COMPARISON

11.8 COMPANY VALUATION AND FINANCIAL METRICS

11.9 COMPETITIVE SCENARIO AND TRENDS

11.9.1 DEALS

11.9.2 EXPANSIONS

11.9.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

12.1 KEY PLAYERS

12.1.1 KYOCERA CORPORATION

12.1.1.1 Business overview

12.1.1.2 Products/Solutions/Services offered

12.1.1.3 Recent developments

12.1.1.3.1 Deals

12.1.1.3.2 Expansions

12.1.1.4 MnM view

12.1.1.4.1 Key strengths

12.1.1.4.2 Strategic choices

12.1.1.4.3 Weaknesses and competitive threats

12.1.2 CERAMTEC GMBH

12.1.2.1 Business overview

12.1.2.2 Products/Solutions/Services offered

12.1.2.3 MnM view

12.1.2.3.1 Key strengths

12.1.2.3.2 Strategic choices

12.1.2.3.3 Weaknesses and competitive threats

12.1.3 COORSTEK

12.1.3.1 Business overview

12.1.3.2 Products/Solutions/Services offered

12.1.3.3 Recent developments

12.1.3.3.1 Others

12.1.3.4 MnM view

12.1.3.4.1 Key strengths

12.1.3.4.2 Strategic choices

12.1.3.4.3 Weaknesses and competitive threats

12.1.4 MORGAN ADVANCED MATERIALS

12.1.4.1 Business overview

12.1.4.2 Products/Solutions/Services offered

12.1.4.3 Recent developments

12.1.4.3.1 Others

12.1.4.4 MnM view

12.1.4.4.1 Key strengths

12.1.4.4.2 Strategic choices

12.1.4.4.3 Weaknesses and competitive threats

12.1.5 NGK INSULATORS, LTD.

12.1.5.1 Business overview

12.1.5.2 Products/Solutions/Services offered

12.1.5.3 MnM view

12.1.5.3.1 Key strengths

12.1.5.3.2 Strategic choices

12.1.5.3.3 Weaknesses and competitive threats

12.1.6 MARUWA CO., LTD.

12.1.6.1 Business overview

12.1.6.2 Products/Solutions/Services offered

12.1.6.3 MnM view

12.1.6.3.1 Key strengths

12.1.6.3.2 Strategic choices

12.1.6.3.3 Weaknesses and competitive threats

12.1.7 AGC INC.

12.1.7.1 Business overview

12.1.7.2 Products/Solutions/Services offered

12.1.7.3 Recent developments

12.1.7.3.1 Others

12.1.7.4 MnM view

12.1.7.4.1 Key strengths

12.1.7.4.2 Strategic choices

12.1.7.4.3 Weaknesses and competitive threats

12.1.8 MATERION CORPORATION

12.1.8.1 Business overview

12.1.8.2 Products/Solutions/Services offered

12.1.8.3 MnM view

12.1.8.3.1 Key strengths

12.1.8.3.2 Strategic choices

12.1.8.3.3 Weaknesses and competitive threats

12.1.9 TOKUYAMA CORPORATION

12.1.9.1 Business overview

12.1.9.2 Products/Solutions/Services offered

12.1.9.3 Recent developments

12.1.9.3.1 Expansions

12.1.9.4 MnM view

12.1.9.4.1 Key strengths

12.1.9.4.2 Strategic choices

12.1.9.4.3 Weaknesses and competitive threats

12.1.10 FERROTEC CORPORATION

12.1.10.1 Business overview

12.1.10.2 Products/Solutions/Services offered

12.1.10.3 Recent developments

12.1.10.3.1 Expansions

12.1.10.4 MnM view

12.1.10.4.1 Key strengths

12.1.10.4.2 Strategic choices

12.1.10.4.3 Weaknesses and competitive threats

12.2 OTHER PLAYERS

12.2.1 GREAT CERAMIC

12.2.2 ADTECH CERAMICS

12.2.3 XIAMEN MASCERA TECHNOLOGY CO., LTD.

12.2.4 ORTECH, INC.

12.2.5 ADVANCED CERAMIC MATERIALS

12.2.6 STC MATERIAL SOLUTIONS

12.2.7 NISHIMURA ADVANCED CERAMICS CO., LTD.

12.2.8 JAPAN FINE CERAMICS CO., LTD.

12.2.9 WUXI SPECIAL CERAMIC ELECTRICAL CO., LTD.

12.2.10 JINGHUI INDUSTRY LTD.

12.2.11 FUJIAN HUAQING ELECTRONIC MATERIAL TECHNOLOGY CO., LTD.

12.2.12 HEBEI SUOYI NEW MATERIAL TECHNOLOGY CO., LTD.