농업용 로봇 시장 : 로봇 유형별, 용도별, 제공별, 최종 용도별, 농업 환경별, 농장 규모별, 지역별 예측(-2030년)

Agricultural Robots Market by Robot Type, Application, Offering, End Use, Farming Environment, Farm Size, and Region - Global Forecast to 2030

상품코드:1877347

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 375 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

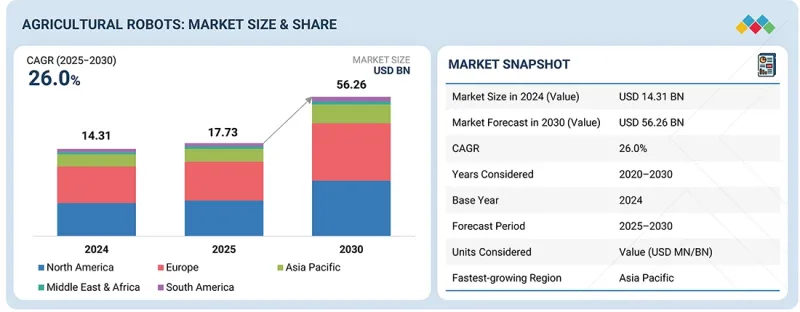

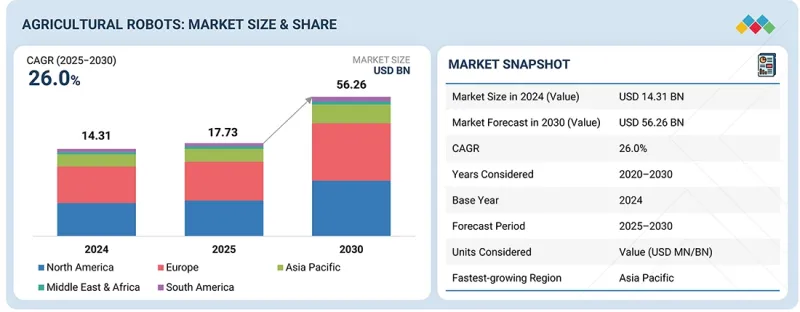

세계의 농업용 로봇 시장 규모는 2025년에 177억 3,000만 달러 규모에 달할 것으로 예측됩니다.

예측 기간 중 CAGR은 26.0%로 2030년까지 562억 6,000만 달러에 달할 것으로 전망됩니다. 농업용 로봇에 대한 인공지능(AI)의 채용은 데이터 구동형으로 효율적인 농업 운영으로의 전환을 가속화하고 있습니다. AI를 통해 로봇은 씨앗, 작물 감시, 제초, 수확 등의 복잡한 작업을 인간의 개입을 최소화하면서 정밀하게 수행할 수 있습니다.

조사 범위

조사 대상 기간

2025-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

금액(100만 달러)

부문

로봇 유형별, 용도별, 최종 용도별, 농업 환경별, 제공별, 농장 규모별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미 및 기타 지역

머신러닝과 컴퓨터 비전을 활용함으로써 이러한 시스템은 자원 활용 최적화, 수확량 예측 정확도 향상 및 운영 비용 절감을 실현합니다. 자율주행 트랙터와 무인 항공기에 대한 AI 통합은 대규모 농장에서 의사결정과 확장성을 강화합니다. 기술 비용이 낮아짐에 따라 AI 구동형 농업용 로봇은 지속가능하고 생산성이 높고 탄력적인 농업 비즈니스 운영을 위한 전략적 추진력이 되고 있습니다.

무인 항공기(UAV) 부문은 현대 농업의 범용성과 효율성으로 인해 농업용 로봇 시장에서 점유율을 차지하고 있습니다. 드론이라고도 불리는 UAV는 작물 모니터링, 농장 매핑, 정밀 살포, 토양 분석에 널리 활용되고 있습니다. 고해상도 카메라, 멀티스펙트럼 센서, AI 탑재 분석 기능을 장비하여 작물의 건강 상태, 해충 피해, 관개 요구에 대한 실시간 지식을 제공합니다. 광범위한 신속하고 비용 효율적인 커버리지 능력을 통해 노동력 수요를 줄이면서 생산성을 향상시킵니다. 정밀농업, 데이터구동형 의사결정, 지속가능한 농업기술에 대한 수요 증가가 세계적인 농업운영에 있어서 UAV의 급속한 보급을 추진하고 있습니다.

농업용 로봇 시장에서의 필드 농업 분야는 자동화와 정밀 농업 실천의 보급 확대를 배경으로 예측 기간 동안 현저한 성장률을 나타낼 것으로 예측됩니다. 대규모 농장에서는 파종, 심기, 제초, 관개, 수확 등의 작업에 로봇과 자율 기계가 점점 도입되고 있습니다. 이러한 기술은 작업 효율 향상, 노동력 의존도 저감, 물·비료·농약을 포함한 자원 이용 최적화를 실현합니다. AI, 머신러닝, IoT 대응 센서의 발전으로 정확성과 의사 결정 능력이 더욱 향상되었습니다. 보다 높은 수확량과 지속가능한 농업 기법에 대한 수요 증가는 이 분야의 세계적인 견조한 성장을 이끌 것으로 예측됩니다.

북미는 선진기술의 조기 도입과 확립된 정밀농업의 실천에 의해 농업용 로봇 시장에서 큰 점유율을 차지할 것으로 예측됩니다. 이 지역은 농업 자동화에 대한 강력한 투자, 정부의 지원책, AI 및 로봇 기술을 활용한 솔루션에 대한 높은 인지도 등의 이점을 가지고 있습니다. 생산성 향상, 자원 이용 최적화, 노동력 의존도 저감을 위해 자율주행 트랙터, 드론, AI 탑재 로봇을 농가가 활용하는 경우가 증가하고 있습니다. 또한 주요 시장 기업의 존재와 로보틱스 및 IoT 기술의 지속적인 혁신이 결합되어 스마트하고 지속 가능한 농업 솔루션의 도입에 있어 북미가 주도적인 지역으로서의 지위를 더욱 강화하고 있습니다.

본 보고서에서는 세계의 농업용 로봇 시장에 대해 조사했으며 로봇 유형별, 용도별, 제공별, 농업 환경별, 농장 규모별, 최종 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서론

거시경제지표

시장 역학

미충족 수요(Unmet Needs)와 백스페이스

연결된 시장과 부문 간 기회

새로운 비즈니스 모델과 생태계의 변화

Tier 1/2/3 기업의 전략적 움직임

제6장 업계 동향

Porter's Five Forces 분석

밸류체인 분석

생태계 분석

가격 분석

무역 분석

주된 회의와 이벤트(2024-2026년)

고객사업에 영향을 주는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

미국 관세의 영향 - 농업용 로봇 시장(2025년)

제7장 기술, 특허, 디지털, AI 도입으로 파괴적 혁신

주요 신기술

AI 탑재 컴퓨터 비전과 딥러닝

공중 지상 협조 시스템(UAV-UGV 통합)

스웜 로봇

RTK GPS와 고정밀 측위

보완적 기술

IoT 센서와 스마트 필드 감시 시스템

5G 연결 및 엣지 컴퓨팅

클라우드 기반 농장 관리 플랫폼

기술/제품 로드맵

단기(2025-2027년) | 기반 구축과 조기 상업화

중기(2027-2030년)|확장과 표준화

장기적(2030-2035년 이후) | 대규모 상업화와 파괴적 변화

특허 분석

미래의 응용

AI/생성형 AI가 농업용 로봇 시장에 미치는 영향

성공 사례와 실세계에의 응용

제8장 규제 상황

지역 규제 및 규정 준수

농업기계의 세계기준

북미

유럽연합(EU)

아시아태평양

기타 지역

업계 표준

제9장 고객정세와 구매행동

의사결정 프로세스

구매자의 이해관계자와 구매평가기준

채용 장벽과 내부 과제

시장 수익성

제10장 농업용 로봇 시장(로봇 유형별)

서론

무인 항공기

착유 로봇

무인 트랙터

자동화 수확 시스템

기타

제11장 농업용 로봇 시장(용도별)

서론

수확 관리

밭농사 및 작물 관리

낙농 및 가축 관리

토양 및 관개 관리

재고 및 공급망 관리

기타

제12장 농업용 로봇 시장(제공별)

서론

하드웨어

소프트웨어

서비스

제13장 농업용 로봇 시장(농업 환경별)

서론

실외

실내

제14장 농업용 로봇 시장(농장 규모별)

서론

소규모 농장(100헥타르 미만)

중규모 농장(100헥타르 이상 500헥타르 미만)

대규모 농장(500헥타르 이상)

제15장 농업용 로봇 시장(최종 용도별)

서론

농산물

유제품 및 축산

제16장 농업용 로봇 시장(지역별)

서론

북미

미국

캐나다

멕시코

유럽

프랑스

독일

이탈리아

네덜란드

영국

기타

아시아태평양

중국

인도

일본

한국

호주

기타

남미

브라질

아르헨티나

기타

기타 지역

중동

아프리카

제17장 경쟁 구도

개요

주요 진입기업의 전략/강점

연간 수익 분석(2020-2024년)

시장 점유율 분석(2024년)

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

기업평가와 재무지표

제품 비교

경쟁 시나리오와 동향

제18장 기업 프로파일

주요 진출기업

DEERE & COMPANY

CNH INDUSTRIAL NV

AGCO CORPORATION

TRIMBLE INC.

DJI

BOUMATIC

LELY INTERNATIONAL

EAGLENXT

KUBOTA CORPORATION

DELAVAL

HARVEST CROO ROBOTICS

NAIO TECHNOLOGIES

ECOROBOTIX

AGROBOTS

ROBOTICS PLUS

기타 기업

AUTONOMOUS TRACTOR CORPORATION

FFROBOTICS

DRONEDEPLOY

YANMAR CO.

CLEARPATH ROBOTICS, INC.

BONSAI ROBOTICS INC.

AIGEN

TEVEL AEROBOTICS TECHNOLOGIES LTD.

SWARMFARM

MONARCH TRACTOR

제19장 인접 시장과 관련 시장

제20장 부록

KTH

영문 목차

영문목차

The global market for agricultural robots is estimated to be valued at USD 17.73 billion in 2025. It is projected to reach USD 56.26 billion by 2030, at a CAGR of 26.0% during the forecast period. The adoption of artificial intelligence (AI) in agricultural robots is accelerating the shift toward data-driven and efficient farming operations. AI enables robots to perform complex tasks such as seeding, crop monitoring, weeding, and harvesting with precision and minimal human intervention.

Scope of the Report

Years Considered for the Study

2025-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million)

Segments

By Robot Type, Application, End Use, Farming Environment, Offering, Farm Size, and Region

Regions covered

North America, Europe, Asia Pacific, South America, and RoW

By leveraging machine learning and computer vision, these systems optimize resource utilization, improve yield prediction, and reduce operational costs. The integration of AI with autonomous tractors and drones enhances decision-making and scalability across large farms. As technology costs decline, AI-driven agricultural robots are becoming a strategic enabler for sustainable, productive, and resilient agri-business operations.

"The unmanned aerial vehicles segment holds the highest market share in the robot type segment of the agricultural robots market."

The unmanned aerial vehicle (UAV) segment leads the agricultural robots market in terms of market share due to its versatility and efficiency in modern farming. UAVs, also known as drones, are widely used for crop monitoring, field mapping, precision spraying, and soil analysis. Equipped with high-resolution cameras, multispectral sensors, and AI-enabled analytics, they provide real-time insights into crop health, pest infestations, and irrigation needs. Their ability to cover large areas quickly and cost-effectively reduces labor requirements while enhancing productivity. The growing demand for precision agriculture, data-driven decision-making, and sustainable farming practices is driving the rapid adoption of UAVs across global agricultural operations.

"The field farming application segment is projected to grow at a significant rate during the forecast period."

The field farming application segment in the agricultural robots market is projected to grow at a significant rate during the forecast period, driven by increasing adoption of automation and precision agriculture practices. Robots and autonomous machinery are increasingly deployed for activities such as seeding, planting, weeding, irrigation, and harvesting across large-scale farms. These technologies improve operational efficiency, reduce labor dependency, and optimize resource utilization, including water, fertilizers, and pesticides. Advances in AI, machine learning, and IoT-enabled sensors further enhance accuracy and decision-making. The growing demand for higher crop yields and sustainable farming practices is expected to drive robust growth in this segment globally.

North America is expected to hold a significant share of the agricultural robots market.

North America is expected to hold a significant share in the agricultural robots market due to early adoption of advanced technologies and well-established precision farming practices. The region benefits from strong investment in agrarian automation, supportive government initiatives, and high awareness of AI- and robotics-driven solutions. Farmers are increasingly using autonomous tractors, drones, and AI-enabled robots to enhance productivity, optimize resource utilization, and reduce labor dependency. Additionally, the presence of key market players and continuous innovation in robotics and IoT technologies further strengthen North America's position as a leading region in the adoption of smart and sustainable agricultural solutions.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the agricultural robots market:

By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

By Designation: Directors- 20%, Managers - 50%, Executives- 30%

By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15% and Rest of the World -10%

Prominent companies in the market include Deere & Company (US), DJI (China), CNH Industrial NV (Netherlands), AGCO Corporation (US), Delaval (Sweden), Trimble Inc. (US), Boumatic Robotic (Netherlands), Lely (Netherlands), AgJunction (US), AgEagle Aerial Systems (US), Yanmar Co. (Japan), Deepfield Robotics (Germany), Ecorobotix (Switzerland), Harvest Automation (US), and Naio Technologies (France).

Other players include Robotics Plus (Zealand), Kubota Corporation (Japan), Harvest Cro Robotics (US), Autonomous Tractor Corporation (US), Clearpath Robotics (Canada), Dronedeploy (US), Agrobots (Spain), FFRobotics (Israel), Fullwood Joz (UK), and Monarch Tractors (US).

Research Coverage:

This research report categorizes the agricultural robots market by robot type (unmanned aerial vehicles/drones, milking robotics, driverless tractor, automated harvesting robots), (harvest management, field & crop management, dairy & livestock management, inventory & supply chain management, soil & irrigation management, weather tracking & forecasting), end use (farm produce, dairy & livestock), farming environment (indoor, outdoor), offering (hardware, software, services), farm size (small-sized farm, mid-sized farms, large sized farms) and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report encompasses detailed information regarding the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the agricultural robots market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments related to the agricultural robots market. This report provides a competitive analysis of emerging startups in the agricultural robots market ecosystem. Furthermore, the study also covers industry-specific trends, including technology analysis, ecosystem and market mapping, patent analysis, and regulatory landscape, among others.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall agricultural robots and the subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market, providing them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (increasing demand for food), restraints (supply chain disruption), opportunities (technological innovations), and challenges (regulatory barriers) influencing the growth of the agricultural robots market.

New product launch/Innovation: Detailed insights on research & development activities and new product launches in the agricultural robots market.

Market Development: Comprehensive information about lucrative markets - the report analyzes the agricultural robots market across varied regions.

Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the agricultural robots market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Deere & Company (US), DJI (China), CNH Industrial NV (Netherlands), AGCO Corporation (US), Delaval (Sweden), and other players in the agricultural robots market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE AND SEGMENTATION

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.3.6 STAKEHOLDERS

1.4 SUMMARY OF STRATEGIC CHANGES IN MARKET

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key primary participants

2.1.2.3 Breakdown of primary interviews

2.1.2.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.2.3 BASE NUMBER CALCULATION

2.3 MARKET FORECAST APPROACH

2.3.1 SUPPLY SIDE

2.3.2 DEMAND SIDE

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

3.3 DISRUPTIVE TRENDS SHAPING MARKET

3.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AGRICULTURAL ROBOTS MARKET

4.2 AGRICULTURAL ROBOTS MARKET, BY OFFERING AND REGION

4.3 AGRICULTURAL ROBOTS MARKET, BY FARM SIZE

4.4 AGRICULTURAL ROBOTS MARKET, BY APPLICATION

4.5 AGRICULTURAL ROBOTS MARKET, BY END USE

4.6 AGRICULTURAL ROBOTS MARKET, BY FARMING ENVIRONMENT

4.7 AGRICULTURAL ROBOTS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MACROECONOMIC INDICATORS

5.2.1 REDUCTION IN ARABLE LAND

5.2.2 RAPID DIGITALIZATION

5.2.3 LIVESTOCK POPULATION TRENDS

5.3 MARKET DYNAMICS

5.3.1 INTRODUCTION

5.3.2 DRIVERS

5.3.2.1 Advancement in technologies

5.3.2.2 Sustainability goals accelerate adoption of agricultural robots

5.3.2.3 Surging labor costs and labor shortages

5.3.2.4 Increasing number of dairy, poultry, and swine farms

5.3.3 RESTRAINTS

5.3.3.1 High initial cost of automation for small farms

5.3.3.2 Technological barriers pertaining to fully autonomous robots

5.3.3.3 Complex and unstructured farm environments

5.3.3.4 Lack of training activities in operating agricultural robots

5.3.4 OPPORTUNITIES

5.3.4.1 Untapped market potential and scope for automation in agriculture

5.3.4.2 Controlled Environment Agriculture (CEA) to drive adoption of agricultural robots

5.3.4.3 High adoption of aerial data collection tools in agriculture

5.3.4.4 Adoption of software, data, and service-based business models

5.3.5 CHALLENGES

5.3.5.1 Lack of standardization and regulation of agricultural robot technologies globally

5.3.5.2 High cost and complexity of fully autonomous robots

5.3.5.3 Integration challenges with existing farm equipment

5.3.5.4 Lack of technical knowledge among farmers

5.4 UNMET NEEDS AND WHITE SPACES

5.4.1 UNMET NEEDS IN AGRICULTURAL ROBOTS MARKET

5.4.2 WHITE SPACE OPPORTUNITIES

5.5 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

5.5.1 INTERCONNECTED MARKETS

5.5.2 CROSS-SECTOR OPPORTUNITIES

5.6 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

5.6.1 EMERGING BUSINESS MODELS

5.6.2 ECOSYSTEM SHIFTS

5.7 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5.7.1 KEY MOVES AND STRATEGIC FOCUS

6 INDUSTRY TRENDS

6.1 PORTER'S FIVE FORCES ANALYSIS

6.1.1 THREAT OF NEW ENTRANTS

6.1.2 THREAT OF SUBSTITUTES

6.1.3 BARGAINING POWER OF SUPPLIERS

6.1.4 BARGAINING POWER OF BUYERS

6.1.5 INTENSITY OF COMPETITIVE RIVALRY

6.2 VALUE CHAIN ANALYSIS

6.2.1 RESEARCH AND PRODUCT DEVELOPMENT

6.2.2 DEVICE AND COMPONENT MANUFACTURERS

6.2.3 SYSTEM INTEGRATORS

6.2.4 SERVICE PROVIDERS

6.2.5 END USERS

6.2.6 POST-SALES SERVICES

6.3 ECOSYSTEM ANALYSIS

6.3.1 DEMAND SIDE

6.3.2 SUPPLY SIDE

6.4 PRICING ANALYSIS

6.4.1 AVERAGE SELLING PRICE, BY KEY PLAYER

6.4.2 AVERAGE SELLING PRICE TREND, BY REGION

6.5 TRADE ANALYSIS

6.5.1 EXPORT SCENARIO OF HS CODE 8433

6.5.2 IMPORT SCENARIO OF HS CODE 8433

6.6 KEY CONFERENCES AND EVENTS, 2024-2026

6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.8 INVESTMENT AND FUNDING SCENARIO

6.9 CASE STUDY ANALYSIS

6.9.1 KUBOTA-KILTER COLLABORATION ON AX-1 ULTRA-PRECISE WEEDING ROBOT

6.9.2 ENHANCING SOFT-FRUIT HARVESTING THROUGH PLATFORM-AGNOSTIC ROBOTICS INTEGRATION

6.9.3 AIGEN'S ELEMENT GEN2 ROBOTIC CREW FOR WEED CONTROL

6.10 IMPACT OF 2025 US TARIFF - AGRICULTURAL ROBOTS MARKET

6.10.1 INTRODUCTION

6.10.2 KEY TARIFF RATES

6.10.3 PRICE IMPACT ANALYSIS

6.10.4 IMPACT ON COUNTRY/REGION

6.10.4.1 US

6.10.4.2 Europe

6.10.4.3 Asia Pacific

6.10.5 IMPACT ON END-USE INDUSTRIES

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

7.1 KEY EMERGING TECHNOLOGIES

7.1.1 AI-POWERED COMPUTER VISION & DEEP LEARNING

7.1.2 AERIAL-GROUND COLLABORATIVE SYSTEMS (UAV-UGV INTEGRATION)

7.1.3 SWARM ROBOTICS

7.1.4 RTK GPS & HIGH-PRECISION POSITIONING

7.2 COMPLEMENTARY TECHNOLOGIES

7.2.1 IOT SENSORS AND SMART FIELD MONITORING SYSTEMS

7.2.2 5G CONNECTIVITY AND EDGE COMPUTING

7.2.3 CLOUD-BASED FARM MANAGEMENT PLATFORMS

7.3 TECHNOLOGY/PRODUCT ROADMAP

7.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION