Rigid Endoscopes Market by Type (Laparoscopes, Arthroscopes, Cystoscopes), Clinical Usage (Diagnostic, Surgical), Application (Laparoscopy, Cystoscopy, Arthroscopy, Other), End User (Hospitals, ASCs, Clinics), Region - Global Forecast to 2030

상품코드:1861054

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 241 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

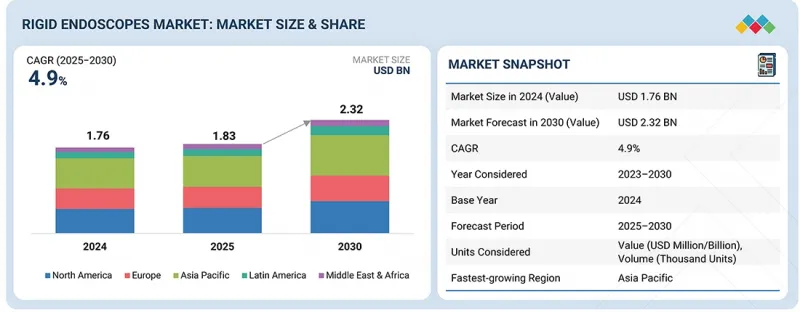

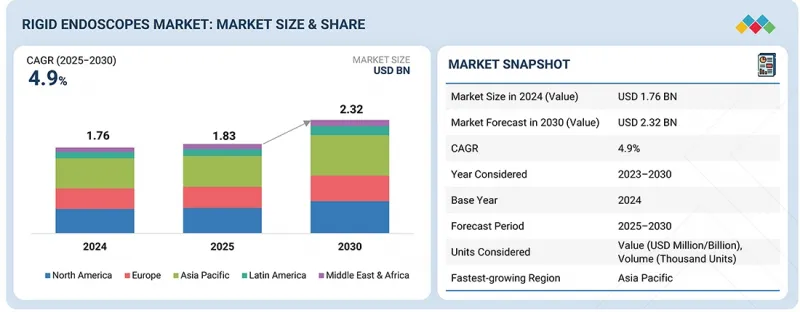

세계의 경성 내시경 시장 규모는 2025년 18억 3,000만 달러에서 2030년에는 23억 2,000만 달러에 이를 것으로 예측되고, 예측 기간 중 연평균 복합 성장률(CAGR)은 4.9%로 전망되고 있습니다.

경성 내시경 시장의 성장은 만성 질환의 유병률 증가, 최소 침습 수술에 대한 수요 증가, 이미징 및 광학 기술의 발전으로 인해 발생합니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

유형별, 임상 용도별, 용도별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

의료 인프라의 확대, 시술 건수 증가, 의료 관광 증가로 인해 신흥 시장에 비즈니스 기회가 존재하며, 첨단 내시경 솔루션의 도입이 가능해졌습니다. 그러나 바이러스 감염 위험, 적절한 멸균 및 재처리 부족, 높은 시술 비용 등의 문제에 직면해 있으며, 특히 자원이 부족한 지역에서는 보급이 제한적일 수 있습니다.

예측 기간 동안 경성 내시경 시장에서 관절경 부문은 가장 빠른 속도로 성장할 것으로 예측됩니다.

경성 내시경 시장은 유형별로 복강경, 비뇨기 내시경, 부인과 내시경, 관절경, 세포경, 신경 내시경, 기타 경성 내시경으로 분류됩니다. 이 중 비뇨기 내시경 부문은 2024년 근골격계 질환의 유병률 증가, 특히 고령화되는 세계 인구 증가로 인해 시장 점유율 2위를 차지할 것으로 예측됩니다. WHO에 따르면 60세 이상 인구는 2023년 11억 명에서 2030년 14억 명으로 증가할 것으로 예상되며, 관절 관련 질환의 위험이 높은 환자층이 형성될 것으로 예측됩니다. CDC의 보고에 따르면, 관절염의 유병률은 연령에 따라 급증하여 18-34세 성인의 3.6%에서 75세 이상 성인의 53.9%에 달할 전망입니다. 관절경 검사는 관절 손상 진단 및 치료, 회복 시간 단축, 수술 결과 개선을 위한 정확하고 덜 침습적인 솔루션을 제공하며, 환자의 선호도와 시술의 채택을 촉진합니다. 또한, 고화질 영상의 발전, 수술기구의 개선, 정형외과 전문의의 인식이 높아짐에 따라 관절경 채택이 더욱 가속화되고 있으며, 이 분야는 경성 내시경 시장 중 가장 빠르게 성장하고 있습니다.

임상 용도별로 경성 내시경 시장은 진단용과 수술용으로 나뉩니다. 이 중 외과적 용도 부문이 2024년 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 복강경, 관절경, 비뇨기과, 산부인과, 이비인후과 등 여러 전문분야에서 최소침습적 시술의 채택이 증가하고 있기 때문입니다. 경성 내시경은 뛰어난 광학 투명성, 고해상도 및 4K 가시성, 수술 기구 및 수술실 워크플로우와 원활하게 통합되는 견고하고 오토클레이브가 가능한 설계를 제공하여 이러한 중재의 핵심 플랫폼 역할을 합니다. 최소침습수술에 대한 선호도가 높아지는 것은 입원일수 단축, 수술 후 합병증 감소, 환자의 빠른 회복, 임상결과 개선 등의 장점으로 인해 수술 건수 및 경성경 시장 수요에 직접적인 영향을 미치고 있습니다.

아시아태평양은 예측 기간 동안 경성 내시경 시장에서 가장 높은 성장률을 보일 것으로 예측됩니다.

세계 경질 내시경 시장은 5개 주요 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)으로 구분됩니다. 이 중 아시아태평양이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. 이는 주로 중국, 인도 등 인구 대국의 의료 인프라 정비, 의료비 지출 증가, 질병 조기 발견에 대한 인식이 높아졌기 때문입니다. 이들 국가들은 특히 암, 폐질환, 비뇨기재환 등 만성질환 증가를 관리하기 위해 진단 및 수술 역량을 강화하기 위해 많은 투자를 하고 있습니다. 일본에서는 전국민 의료보험제도가 확립되어 있어 고도의 내시경 수술에 대한 폭넓은 접근성이 확보되어 있습니다. 또한, 의료 관광 증가, 정부의 유리한 이니셔티브, 최소 침습 기술의 채택 증가는 시장 침투를 가속화하여 아시아태평양을 세계 경직성 내시경 시장에서 고성장 지역으로 만들고 있습니다.

세계의 경성 내시경 시장에 대해 조사했으며, 유형별, 임상용도별, 용도별, 최종사용자별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

업계 동향

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

무역 분석

규제 분석

특허 분석

2025-2026년 주요 컨퍼런스 및 이벤트

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

인접 시장 분석

미충족 요구/최종사용자 기대

AI/생성형 AI가 경성 내시경 시장에 미치는 영향

2025년 미국 관세가 경성 내시경 시장에 미치는 영향

제6장 경성 내시경 시장(유형별)

서론

복강경

비뇨기과 내시경

부인과 내시경

관절경

방광경

신경 내시경

기타

제7장 경성 내시경 시장(임상 용도별)

서론

외과

진단

제8장 경성 내시경 시장(용도별)

서론

복강경 검사

비뇨기과 내시경

관절경 검사

신경 내시경

기타

제9장 경성 내시경 시장(최종사용자별)

서론

병원

외래수술센터(ASC)

클리닉

기타

제10장 경성 내시경 시장(지역별)

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

호주

한국

기타

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타

제11장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

기업 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오

제12장 기업 개요

주요 시장 진출기업

OLYMPUS CORPORATION

KARL STORZ SE & CO. KG

STRYKER

SMITH+NEPHEW

B. BRAUN SE

MEDTRONIC

NIPRO

RICHARD WOLF GMBH

CONMED CORPORATION

ARTHREX, INC.

기타 기업

FUJIFILM CORPORATION

HOLOGIC, INC.

SHANGRAO WS MEDTECH CO., LTD.

ATMOS MEDIZINTECHNIK GMBH & CO. KG

HENKE-SASS WOLF

RUDOLF MEDICAL GMBH+CO. KG

ENDOMED SYSTEMS GMBH

TELEFLEX INCORPORATED

INTEGRATED ENDOSCOPY

NEOSCOPE INC.

ECLERIS

NANCHANG WOEK MEDICAL TECHNOLOGY CO., LTD

KASHMIR SURGICAL WORKS

OPTOMIC

HIPP ENDOSKOP SERVICE GMBH

제13장 부록

LSH

영문 목차

영문목차

The global rigid endoscopes market is projected to reach USD 2.32 billion by 2030, growing from USD 1.83 billion in 2025, at a CAGR of 4.9% during the forecast period. The growth of the rigid endoscopes market is driven by the rising prevalence of chronic diseases, increasing demand for minimally invasive surgeries, and advancements in imaging and optics technology.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Type, Clinical Usage, Application, End User, and Region

Regions covered

North America, Europe, APAC, RoW

Opportunities exist in emerging markets due to the expansion of healthcare infrastructure, increasing procedural volumes, and rising medical tourism, which enable the adoption of advanced endoscopic solutions. However, market growth faces challenges from risks of viral infections, lack of proper sterilization and reprocessing, and high procedural costs, which may limit widespread adoption, particularly in resource-constrained regions.

The arthroscopes segment is expected to grow at the fastest rate in the rigid endoscopes market during the forecast period.

By type, the rigid endoscopes market is segmented into laparoscopes, urology endoscopes, gynecology endoscopes, arthroscopes, cytoscopes, neuroendoscopes, and other rigid endoscopes. Among these, the urology endoscopes segment accounted for the second-largest market share in 2024, owing to the increasing prevalence of musculoskeletal disorders, particularly among the aging global population. According to the WHO, the number of people aged 60 and above is projected to rise from 1.1 billion in 2023 to 1.4 billion by 2030, creating a substantial patient pool at higher risk for joint-related conditions. Age-related degenerative diseases such as osteoarthritis are becoming more common, with the CDC reporting that arthritis prevalence increases sharply with age-from 3.6% in adults aged 18-34 to 53.9% in individuals 75 and older-driving demand for minimally invasive orthopedic interventions. Arthroscopy offers a precise, less invasive solution for diagnosing and treating joint injuries, reducing recovery time, and improving surgical outcomes, which enhances patient preference and procedural adoption. Additionally, advancements in high-definition imaging, improved surgical instruments, and growing awareness among orthopedic specialists are further accelerating the adoption of arthroscopes, positioning this segment for the fastest growth within the rigid endoscopes market.

The surgical usage segment accounted for the largest share of the rigid endoscopes market in 2024.

By clinical usage, the rigid endoscopes market has been divided into diagnostic & surgical usage. Among these, the surgical usage segment accounted for the largest share of the market in 2024. This is due to the increasing adoption of minimally invasive procedures across multiple specialties, including laparoscopy, arthroscopy, urology, gynecology, and ENT. Rigid endoscopes serve as the core platform for these interventions, offering superior optical clarity, high-definition and 4K visualization, and robust, autoclavable designs that integrate seamlessly with surgical instruments and operating room workflows. The growing preference for minimally invasive surgeries is driven by benefits such as shorter hospital stays, reduced post-operative complications, faster patient recovery, and enhanced clinical outcomes, which directly influence procedure volumes and market demand for rigid scopes.

Asia Pacific is projected to grow at the highest rate in the rigid endoscopes market during the forecast period.

The global rigid endoscopes market is segmented into five major regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Among these, the Asia Pacific region is projected to grow at the highest rate during the forecast period. This is primarily due to the development of healthcare infrastructure, increasing healthcare expenditure, and rising awareness of early disease detection across populous nations such as China and India. These countries are investing heavily to enhance diagnostic and surgical capabilities, particularly to manage the rising cases of chronic diseases, such as cancer, pulmonary, and urological disorders. Japan's well-established healthcare system with universal insurance coverage ensures wide accessibility to advanced endoscopic procedures. Moreover, increasing medical tourism, favorable government initiatives, and the rising adoption of minimally invasive technologies are accelerating market penetration, making the Asia Pacific a high-growth region in the global rigid endoscopes market.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1 -40%, Tier 2 -30%, and Tier 3 -30%

By Designation: C-level -50%, Director level -30%, and Others -20%

By Region: North America -30%, Europe - 25%, Asia Pacific -20%, Latin America -15%, and Middle East & Africa -10%

Notes:

Companies are classified into tiers based on their total revenue. The tiers are as follows: Tier 1 = >USD 10.0 billion, tier 2 = USD 1.0 billion to USD 10.0 billion, and tier 3 = <USD 1.0 billion

C-level primaries include CEOs, CFOs, COOs, and VPs.

Others include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The players operating in the rigid endoscopes market include Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Stryker (US), Medtronic (Ireland), Smith+Nephew (UK), B Braun SE (Germany), CONMED Corporation (US), Arthrex Inc. (US), Nipro (Japan), FUJIFILM Corporation (Japan), Hologic, Inc. (US), Shangrao WS Medtech Co., Ltd (China), Henke-Sass, Wolf (Germany), RUDOLF Medical GmbH + Co. KG (Germany), EndoMed Systems GmbH (Germany), Teleflex Incorporated (US), Integrated Endoscopy (US), NeoScope, Inc. (US), Ecleris (US), Nanchang WOEK Medical Technology Co., Ltd (China), Richard Wolf GmbH. (Germany), ATMOS MedizinTechnik GmbH & Co. KG (Germany), Kashmir Surgical Works. (India), Optomic (Spain), and HIPP ENDOSKOP SERVICE GMBH (Germany)

Research Coverage

This report examines the rigid endoscopes market by type, application, end user, and region. The report also examines key factors (including drivers, restraints, opportunities, and challenges) influencing market growth and provides an in-depth analysis of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends. It forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as smaller entrants to gauge the market's pulse, which, in turn, will help them gain a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

Analysis of key drivers (increasing investments, funds, and grants by government and other organizations, growing focus of hospitals to expand endoscopic units, increasing preference for minimally invasive surgeries, rising need for endoscopy to diagnose & treat target diseases), restraints (high overhead costs of endoscopy procedures, increased risk of getting infections during endoscopic procedures), opportunities (rapidly developing healthcare sector in emerging countries), challenges (increasing number of product recalls, lack of sterilization & reprocessing)

Market Penetration: Complete knowledge of the spectrum of products presented by the major companies in the rigid endoscopes market

Product Development/Innovation: Comprehensive understanding of the forthcoming trends, research and development initiatives, and product launches within the rigid endoscopes market

Market Development: Complete knowledge about profitable developing regions

Market Diversification: Exhaustive knowledge of new goods, expanding geographies, and current changes in the rigid endoscopes industry helps to diversify the market

Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players like Olympus Corporation (Japan), Karl Storz SE & CO. KG (Germany), Stryker (US), Nipro (Japan), EndoMed Systems GmbH (Germany), Richard Wolf GmbH. (Germany), Ambu A/S (Denmark), Smith+Nephew (UK), and others.