Automotive Rubber Seals Market by Component (Glass Run Channels, Roof Ditch Molding, Door, Front Windshield, Hood & Trunk Seals, Glass), Material (TPE, PVC, Silicone, EPDM Rubber), Vehicle Type (ICE, Electric), and Region - Global Forecast to 2032

상품코드:1858527

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 315 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

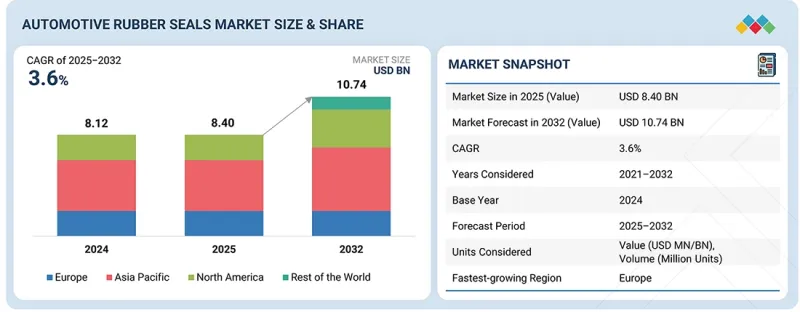

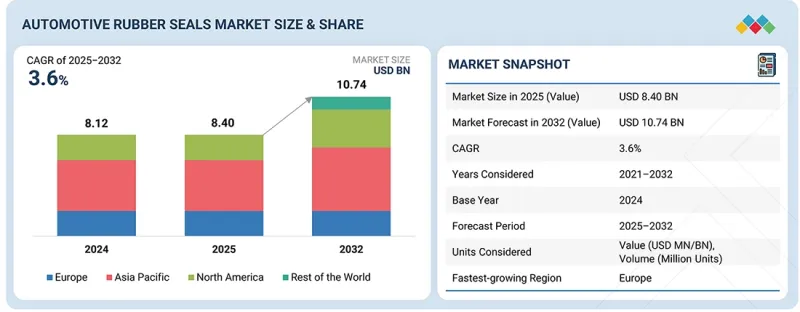

세계의 자동차용 고무 실 시장 규모는 2025년 84억 달러에서 2032년까지 107억 4,000만 달러에 달할 것으로 예측되며, CAGR로 3.6%의 성장이 전망됩니다.

세계 전기자동차용 고무 실 시장 규모는 2025년 13억 2,000만 달러에서 2032년까지 32억 3,000만 달러에 달할 것으로 예상되며, 연평균 13.7%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 자동차의 공기역학, NVH(소음, 진동, 충격) 성능 향상, 물과 먼지의 침투 방지에 대한 수요 증가는 자동차 고무 실 시장의 기술 혁신을 촉진하고 있습니다. 전기자동차 보급이 확대됨에 따라 차량 내부의 기밀성을 보장하고, 배터리 인클로저의 무결성을 향상시키며, 열 관리를 지원하는 첨단 실링 솔루션의 채택이 더욱 가속화되고 있습니다. Cooper Standard, Toyoda Gosei, Henniges Automotive 등 주요 공급업체들은 EV 아키텍처에 맞는 통합형 실링 모듈, 다중 소재 복합재, 경량화 설계로 대응하고 있습니다. 예를 들어 Toyota Gosei의 2024년개발은 EV 배터리 팩용 센서 내장형 다층 실링에 초점을 맞추고 있으며, Cooper Standard는 ADAS 센서 하우징용 모듈식 실링 플랫폼을 확장하고 있습니다.

조사 범위

조사 대상 연도

2021-2032년

기준연도

2024년

예측 기간

2025-2032년

단위

10억 달러/100만 달러, 100만 대/100만 LBS

부문

컴포넌트, 차종, 전기자동차, 재료 유형, 지역

대상 지역

아시아태평양, 유럽, 북미, 기타 지역

유럽과 중국 등 지역에서는 보행자 안전과 소음 배출 기준을 중시하는 규제가 있으며, OEM은 압축성과 탄성을 최적화한 정밀 설계의 유리 런채널, 도어 실, 트렁크 실을 채택하고 있습니다. 주요 이슈로는 원자재 비용 상승과 공급망 불안정성이 지속가능한 엘라스토머와 폐쇄 루프 재활용 시스템에 대한 관심을 높이고 있습니다. 이러한 추세는 공급업체들에게 첨단 폴리머 블렌딩, AI를 통한 설계 최적화, 디지털 통합 실링 시스템 등 차량 조립의 복잡성과 수명주기 비용을 절감할 수 있는 혁신의 기회를 제공합니다.

"자동차 승용차는 예측 기간 중 고무 실 시장의 가장 큰 부문이 될 것으로 예측됩니다."

승용차 부문은 자동차 고무 실 시장에서 가장 큰 점유율을 차지하고 있습니다. 이는 생산량 증가, 편안함, 안전성, NVH 감소를 위한 실링 시스템의 광범위한 사용, 차량내 정숙성, 공기역학적 특성, 내구성을 향상시키는 고급 유리 런채널, 루프 그루브 몰딩, 인캡슐레이션 실에 대한 수요 증가에 기인합니다. 유리 런 채널, 도어 실, 후드 실, 트렁크 실, 허리띠 실 등의 실은 자동차의 수명주기 동안 차량의 무결성과 탑승자의 편안함을 유지하는 데 중요한 역할을 합니다. ICE 차량의 중요한 설계 우선순위는 엔진 열을 견딜 수 있는 우수한 열 안정성, 연료 및 오일에 대한 내노출성, 다양한 운전 조건에서 장기적인 압축 영구 변형 저항성 등이 있습니다.

승용차의 경우, 유리 런 채널은 NVH 감소, 방수, 원활한 창문의 작동에 중요한 역할을 하므로 고무 실의 가장 큰 수요를 차지하며, 그 다음으로 도어 실과 허리 벨트 실이 차내의 편안함과 안전에 필수적입니다. 유리 밀봉은 프리미엄 모델의 프레임리스 도어와 파노라마 윈드쉴드로의 전환으로 인해 가장 빠르게 성장하고 있는 분야입니다. 아시아태평양은 중국, 일본, 인도의 승용차 생산량이 많고, 비용 효율성과 내구성의 균형을 중시하는 OEM의 지원을 받아 수요를 주도하고 있습니다. 이 부문의 성장을 지원하는 것은 미드 부문과 프리미엄 부문의 ICE 차량에 대한 지속적인 수요, 도시화, 자동차 수명 증가입니다. 그러나 원자재 가격 변동과 진화하는 배기가스 관련 캐빈 실링 요구사항에 대응하는 것은 여전히 중요한 과제입니다.

"유리 밀봉은 예측 기간 중 소형 상용차 고무 실 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다."

소형 상용차(LCV)의 유리 밀봉에 대한 수요는 내구성, 내후성 및 열악한 운영 환경에서의 안전에 대한 요구가 증가함에 의해 촉진요인으로 작용하고 있습니다. Ford Transit, Mercedes Sprinter와 같은 밴에서 볼 수 있듯이 잦은 정차와 진동이 발생하는 도심 물류 차량에서는 소음을 최대 5dB까지 줄이고, 유리의 박리를 방지하는 내충격성 접착이 요구되므로 앞 유리의 내구성이 강화됩니다.

세계의 자동차용 고무 실 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

자동차용 고무 실 시장에서의 매력적인 기회

자동차용 고무 실 시장 : 컴포넌트별

자동차용 고무 실 시장 : 차종별(ICE)

자동차용 고무 실 시장 : 지역별

제5장 시장 개요

서론

고객 비즈니스에 영향을 미치는 동향과 혼란

시장 역학

촉진요인

억제요인

기회

과제

가격결정 분석

평균 판매 가격 동향 : 차종별

평균 판매 가격 동향 : 지역별

HS 코드

수출 시나리오

수입 시나리오

에코시스템 분석

원재료 공급업체

자동차용 고무 실 제조업체

자동차 OEM

애프터마켓

공급망 분석

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

규제 상황

규제기관, 정부기관, 기타 조직

주요 규제

자동차용 고무 실 시장의 주요 규격

사례 연구 분석

주요 컨퍼런스와 이벤트(2025-2026년)

자동차용 고무 실 시장에 대한 AI/생성형 AI의 영향

주요 이해관계자와 구입 기준

제6장 ICE 차용 고무 실 시장 : 컴포넌트별

서론

GLASS RUN CHANNELS

ROOF DITCH MOLDING

도어 실

프런트 윈드실드 실

리어 윈드실드 실

후드 실

트렁크 실

허리 벨트 실

유리 봉지

중요 인사이트

제7장 전기자동차 용고무 실 시장 : 컴포넌트별

서론

GLASS RUN CHANNELS

ROOF DITCH MOLDING

도어 실

윈드실드 실

리어 윈드실드 실

후드 실

트렁크 실

허리 벨트 실

유리 봉지

중요 인사이트

제8장 자동차용 고무 실 시장 : 차종별(ICE)

서론

승용차

소형 상용차

대형 상용차

중요 인사이트

제9장 자동차용 고무 실 시장 : EV 유형별

서론

BEV

PHEV

중요 인사이트

제10장 자동차용 고무 실 시장 : 재료별

서론

TPE/TPV

PVC

실리콘계 실

EPDM 고무

중요 인사이트

제11장 자동차용 고무 실 시장 : 지역별

서론

아시아태평양

거시경제 전망

중국

인도

일본

한국

기타 아시아태평양

유럽

거시경제 전망

독일

프랑스

영국

스페인

기타 유럽

북미

거시경제 전망

미국

캐나다

멕시코

기타 지역

거시경제 전망

브라질

러시아

기타

제12장 경쟁 구도

개요

주요 참여 기업의 전략/강점(2021-2025년)

시장 점유율 분석(2024년)

매출 분석

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오

제13장 기업 개요

주요 기업

COOPER STANDARD

TOYODA GOSEI CO., LTD.

HUTCHINSON SA

SAARGUMMI GROUP

NISHIKAWA RUBBER CO., LTD.

HWASEUNG R&A

MINTH GROUP CO., LTD.

MAGNA INTERNATIONAL, INC.

PPAP

GUIZHOU GUIHANG AUTOMOTIVE COMPONENTS CO., LTD.

JIANXIN ZHAO'S GROUP CORPORATION(JZGC)

기타 기업

SFC SOLUTIONS

JIANGYIN HAIDA RUBBER AND PLASTIC CO LTD

KINUGAWA RUBBER INDUSTRIAL CO., LTD.

FALTEC CO., LTD.

INOAC CORPORATION

INDUSTRIE ILPEA SPA

AISIN SHIROKI

INGRESS AUTOVENTURES INDIA PRIVATE LIMITED

NOBO RUBBER PRODUCTS CO., LTD

제14장 MARKETSANDMARKETS에 의한 제안

북미가 자동차용 고무 실 제조업체의 전략적 허브가 된다.

첨단 소재와 디지털 제조에 의한 EV 중심 실링 솔루션의 우선화

자동차용 고무 실에서 멀티 매트리얼 시스템, 유리 봉지, 디지털 생산 기술에 대한 전략적 투자

결론

제15장 부록

KSA

영문 목차

영문목차

The automotive rubber seals market is projected to grow from USD 8.40 billion in 2025 to reach USD 10.74 billion by 2032, with a CAGR of 3.6%. The automotive rubber seals market for electric vehicles is projected to grow from USD 1.32 billion in 2025 to reach USD 3.23 billion by 2032, with a CAGR of 13.7%. Rising demand for improved vehicle aerodynamics, NVH (Noise, Vibration, Harshness) performance, and water/dust ingress protection drives innovation in the automotive rubber seals market. Increasing EV penetration further accelerates the adoption of advanced sealing solutions that ensure cabin airtightness, improve battery enclosure integrity, and support thermal management. Leading suppliers such as Cooper Standard, Toyoda Gosei, and Henniges Automotive are responding with integrated sealing modules, multi-material composites, and lightweight designs tailored for EV architectures. For instance, Toyoda Gosei's 2024 developments focus on multi-layer sealing with embedded sensor capability for EV battery packs, while Cooper Standard is expanding modular sealing platforms for ADAS sensor housings.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Billion/Million), Volume (Million Units & Million LBS)

Segments

Component, Vehicle Type, Electric Vehicle, Material Type, and Region

Regions covered

Asia Pacific, Europe, North America, and the Rest of the World

Regulatory emphasis on pedestrian safety and noise emission standards in regions such as Europe and China is pushing OEMs to adopt precision-engineered glass run channels, door seals, and trunk seals with optimized compression and resilience properties. Key challenges include rising raw material costs and supply chain volatility, which drive interest in sustainable elastomers and closed-loop recycling systems. These trends create opportunities for suppliers to innovate in advanced polymer blends, AI-assisted design optimization, and digitally integrated sealing systems that reduce vehicle assembly complexity and lifecycle cost.

"Passenger car automotive is projected to be the largest segment of the rubber seals market during the forecast period."

The passenger car segment holds the largest share of the automotive rubber seals market, due to higher production volumes, extensive use of sealing systems for comfort, safety, and NVH reduction, and a rise in demand for advanced glass run channels, roof ditch moldings, and encapsulated seals to improve cabin quietness, aerodynamics, and durability. Seals such as glass run channels, door seals, hood seals, trunk seals, and waist belt seals play a critical role in maintaining vehicle integrity and occupant comfort over the vehicle lifecycle. Key design priorities for ICE vehicles include superior thermal stability to withstand engine heat, fuel and oil exposure resistance, and long-term compression set resistance under varied operating conditions.

In passenger cars, glass run channels account for the largest demand in rubber seals due to their critical role in NVH reduction, waterproofing, and smooth window operation, followed by door seals and waist belt seals, which are essential for cabin comfort and safety. Glass encapsulation is the fastest-growing application, driven by the shift toward frameless doors and panoramic windshields in premium models. Regionally, Asia Pacific leads demand, supported by high passenger car production in China, Japan, and India, coupled with OEM focus on balancing cost efficiency with durability. Growth in this segment is supported by continued demand for mid- and premium-segment ICE vehicles, urbanization, and increasing vehicle lifespans. However, volatility in raw material prices and compliance with evolving emission-related cabin sealing requirements remain key challenges.

"Glass encapsulation is projected to account for the largest share in the light commercial vehicle rubber seals market during the forecast period."

The demand for glass encapsulation in light commercial vehicles (LCVs) is driven by growing requirements for durability, weatherproofing, and safety in demanding operational environments. Enhancing windshield durability for urban logistics fleets, where frequent stops and vibrations demand impact-resistant bonding that reduces noise by up to 5 dB and prevents glass delamination, as seen in vans like the Ford Transit and Mercedes Sprinter. Encapsulation supports aerodynamic efficiency by sealing edges against wind resistance, improving fuel economy by 2-3% in high-mileage applications like delivery services. Regulatory frameworks such as ECE R43 (glazing safety) further drive demand for precision-engineered encapsulation systems, while trends toward modular sealing assemblies enable faster vehicle assembly and repairability.

"North America is projected to be the second-fastest-growing market during the forecast period."

North America ranks as the second-fastest-growing market for automotive rubber seals due to its surging electric vehicle production, EVs, which require 20-30% more sealing volume per vehicle than ICE models. The region's stringent emissions regulations, such as California's Advanced Clean Trucks rule mandating 55% zero-emission sales by 2035, accelerate the need for durable, lightweight rubber seals to prevent leaks in high-pressure EV systems, boosting market value. Glass encapsulation is the fastest-growing segment in automotive rubber seals, driven by the adoption of rear windshields, frameless doors, and premium glazing designs, while glass run channels and door seals continue to anchor the largest demand base. Passenger cars remain the largest vehicle type for rubber seals due to their volume. Premium cars and SUVs contain larger body structures, require complex sealing systems, and higher sealing intensity per unit. Thus, North America's automotive rubber seals market will continue to expand, driven by EV growth, regulatory pressures, and evolving vehicle designs, with opportunities concentrated in advanced sealing solutions for premium passenger cars and SUVs that combine durability, lightweight materials, and enhanced NVH performance.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

By Company Type: OEMs - 20%, Automotive Rubber Seal Manufacturers - 80%

By Designation: CXOs - 35%, Managers - 25%, and Executives - 40%

By Region: North America - 35%, Europe - 20%, Asia Pacific - 30% and Rest of the World - 15%

The automotive rubber seals market is dominated by established players, including Cooper Standard Automotive (US), Toyoda Gosei Co., Ltd. (Japan), Hutchinson SA (France), Nishikawa Rubber Co., Ltd. (Japan), and SaarGummi Automotive (Germany). These companies actively manufacture and develop new and advanced rubber seals, have R&D facilities, and offer best-in-class products to their customers.

Research Coverage:

The market study covers the automotive rubber seals market by component (Glass run channels, roof ditch molding, door seals, front windshield seals, rear windshield seals, hood seals, trunk seals, waist belt seals, glass encapsulation), Vehicle Type (Passenger cars, light commercial vehicles, heavy commercial vehicles), Electric Vehicle (BEV, PHEV), Material Type (TPE, PVC, silicone-based seals, EPDM rubber), and Region (North America, Europe, Asia Pacific and Rest of the World). It also covers the competitive landscape and company profiles of the major automotive rubber seals market players.

Key Benefits of Purchasing this Report

The study offers a detailed competitive analysis of the key players in the market, including their company profiles, important insights into product and business offerings, recent developments, and primary market strategies. The report will assist market leaders and new entrants with estimates of revenue figures for the overall automotive rubber seals market and its subsegments. It helps stakeholders understand the competitive landscape and gain additional insights to position their businesses better and develop effective go-to-market strategies. Additionally, the report provides information on key market drivers, restraints, challenges, and opportunities, helping stakeholders keep track of market dynamics.

The report provides insights into the following points:

Analysis of key drivers (Safety & regulatory pressure, electrification & NVH standards, aesthetic & lightweighting trends), restraints (Raw material volatility, complex assembly & fitment tolerances), opportunities (EV growth in Asia Pacific, advanced encapsulation & smart glass integration), and challenges (Balancing performance vs. cost, integration with autonomous & connected vehicles) influencing the growth of the automotive rubber seals market.

Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the automotive rubber seals market

Market Development: Comprehensive information about lucrative markets - the report analyzes the automotive rubber seals market across various regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the automotive rubber seals market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading market players, such as Cooper Standard Automotive (US), Toyoda Gosei Co., Ltd. (Japan), Hutchinson SA (France), Nishikawa Rubber Co., Ltd. (Japan), and SaarGummi Automotive (Germany)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary interviewees from demand and supply sides

2.1.2.2 Breakdown of primary interviews

2.1.2.3 Primary participants

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.3 DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.4.1 DEMAND-SIDE AND SUPPLY-SIDE FACTOR ANALYSES

2.5 RESEARCH ASSUMPTIONS & RISK ASSESSMENT

2.5.1 NUMBER OF COMPONENTS CONSIDERED IN VEHICLE TYPES

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE RUBBER SEALS MARKET

4.2 AUTOMOTIVE RUBBER SEALS MARKET, BY COMPONENT

4.3 AUTOMOTIVE RUBBER SEALS MARKET, BY VEHICLE TYPE (ICE)

4.4 AUTOMOTIVE RUBBER SEALS MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3 MARKET DYNAMICS

5.3.1 DRIVERS

5.3.1.1 Rising adoption of EVs and strict NVH standards

5.3.1.2 Stringent regulatory standards for automotive rubber seals

5.3.1.3 ADAS and glass encapsulation innovation

5.3.2 RESTRAINTS

5.3.2.1 OEM vertical integration risk

5.3.3 OPPORTUNITIES

5.3.3.1 Growth of EVs in Asia Pacific

5.3.3.2 Push toward sustainability and recyclability

5.3.4 CHALLENGES

5.3.4.1 Aligning performance requirements with cost-efficiency

5.3.4.2 Integration between autonomous driving technologies and connected vehicle systems

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE

5.4.2 AVERAGE SELLING PRICE TREND, BY REGION

5.5 HS CODE

5.5.1 EXPORT SCENARIO

5.5.2 IMPORT SCENARIO

5.6 ECOSYSTEM ANALYSIS

5.6.1 RAW MATERIAL SUPPLIERS

5.6.2 AUTOMOTIVE RUBBER SEAL MANUFACTURERS

5.6.3 AUTOMOTIVE OEMS

5.6.4 AFTERMARKET

5.7 SUPPLY CHAIN ANALYSIS

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Multi-material co-extrusion

5.8.1.2 Precision extrusion and injection molding with integrated sensor channels

5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10.2 KEY REGULATIONS

5.10.3 KEY STANDARDS FOR AUTOMOTIVE RUBBER SEALS MARKET

5.11 CASE STUDY ANALYSIS

5.11.1 SAGA DEVELOPED CUSTOM HIGH-TEMPERATURE RUBBER SEALS FORMULATED WITH SPECIALIZED ELASTOMER BLENDS

5.11.2 EASTERN SEALS CONDUCTED MATERIAL COMPATIBILITY ANALYSIS AND RECOMMENDED FLUOROELASTOMER (FKM/VITON) COMPOUNDS FOR FUELS, OILS, AND HEAT

5.11.3 EASTERN SEALS CONDUCTED MATERIAL PERFORMANCE REVIEW AND RECOMMENDED HIGH-PERFORMANCE FLUOROELASTOMER (FKM/VITON) COMPOUNDS WITH ENHANCED RESISTANCE FOR FUELS, OILS, AND HEAT

5.11.4 COOPER STANDARD DEVELOPED CUSTOM EPDM AND TPV-BASED SEALING SYSTEMS ENGINEERED FOR DURABILITY IN HEAVY-DUTY APPLICATIONS

5.11.5 NUOVA GUARNI BETA DEVELOPED CIRCULAR ECONOMY APPROACH FOR SEAL PRODUCTION USING THERMOPLASTIC ELASTOMERS (TPE) AND BIO-BASED EPDM COMPOUNDS

5.12 KEY CONFERENCES & EVENTS, 2025-2026

5.13 IMPACT OF AI/GEN AI ON AUTOMOTIVE RUBBER SEALS MARKET

5.14 KEY STAKEHOLDERS & BUYING CRITERIA

5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.14.2 BUYING CRITERIA

6 AUTOMOTIVE RUBBER SEALS MARKET FOR ICE VEHICLES, BY COMPONENT

6.1 INTRODUCTION

6.2 GLASS RUN CHANNELS

6.2.1 FOCUS ON ADVANCED SEALING AND DESIGN INTEGRATION TO DRIVE MARKET

6.3 ROOF DITCH MOLDING

6.3.1 NEED FOR ENHANCING AERODYNAMICS AND WEATHERPROOFING IN MODERN VEHICLES TO DRIVE GROWTH

6.4 DOOR SEALS

6.4.1 FOCUS ON FRAMELESS DOORS, LARGER GLAZING, AND ENHANCED BODY STYLING TO DRIVE MARKET

6.5 FRONT WINDSHIELD SEALS

6.5.1 FOCUS ON ADVANCED WINDSHIELD FUNCTIONS TO DRIVE MARKET

6.6 REAR WINDSHIELD SEALS

6.6.1 FOCUS ON STRUCTURAL INTEGRITY, WATER TIGHTNESS, AND ACOUSTIC PERFORMANCE TO DRIVE MARKET

6.7 HOOD SEALS

6.7.1 FOCUS ON REINFORCED EPDM AND HYBRID MATERIALS TO DRIVE MARKET

6.8 TRUNK SEALS

6.8.1 FOCUS ON DUST PROTECTION AND VIBRATION DAMPING TO DRIVE MARKET

6.9 WAIST BELT SEALS

6.9.1 INCREASING DEMAND FOR FRAMELESS DOOR DESIGNS AND PANORAMIC GLASS INTEGRATION TO DRIVE MARKET

6.10 GLASS ENCAPSULATION

6.10.1 DEMAND FOR PRECISE FIT AND LONG-TERM DURABILITY TO DRIVE MARKET

6.11 KEY PRIMARY INSIGHTS

7 AUTOMOTIVE RUBBER SEALS MARKET FOR ELECTRIC VEHICLES, BY COMPONENT

7.1 INTRODUCTION

7.2 GLASS RUN CHANNELS

7.2.1 ADOPTION OF PREMIUM EVS TO DRIVE DEMAND FOR ADVANCED GLASS RUN CHANNELS

7.3 ROOF DITCH MOLDING

7.3.1 FOCUS ON ENABLING AERODYNAMIC EFFICIENCY AND INTEGRATED FUNCTIONALITY IN EVS TO DRIVE MARKET

7.4 DOOR SEALS

7.4.1 FOCUS ON MULTI-LAYER ELASTOMERIC PROFILES FOR VIBRATION DUMPING TO DRIVE MARKET

7.5 FRONT WINDSHIELD SEALS

7.5.1 FOCUS ON HYBRID ELASTOMERIC PROFILES WITH AIRTIGHT SEALING TO DRIVE MARKET

7.6 REAR WINDSHIELD SEALS

7.6.1 FOCUS ON LARGE, CURVED REAR GLASS PANELS TO DRIVE MARKET

7.7 HOOD SEALS

7.7.1 FOCUS ON LIGHTWEIGHT AND LOW-COMPRESSION HOOD SEALS IN EVS TO DRIVE MARKET

7.8 TRUNK SEALS

7.8.1 FOCUS ON LARGE REAR HATCHES FOR AERODYNAMIC EFFICIENCY TO DRIVE MARKET

7.9 WAIST BELT SEALS

7.9.1 DEMAND FOR FRAMELESS DOOR DESIGNS AND EXPENSIVE GLAZING TO DRIVE MARKET

7.10 GLASS ENCAPSULATION

7.10.1 RAPID ADOPTION OF RUBBER SEALS IN SUVS AND PREMIUM SEDANS TO DRIVE MARKET

7.11 KEY PRIMARY INSIGHTS

8 AUTOMOTIVE RUBBER SEALS MARKET, BY VEHICLE TYPE (ICE)

8.1 INTRODUCTION

8.2 PASSENGER CAR

8.2.1 EXPANDING PRODUCTION AND PREMIUMIZATION TO FUEL DEMAND FOR RUBBER SEALS

8.3 LIGHT COMMERCIAL VEHICLE

8.3.1 FOCUS ON ENHANCING E-COMMERCE AND LAST-MILE DELIVERY TO DRIVE DEMAND

8.4 HEAVY COMMERCIAL VEHICLE

8.4.1 INCREASED INFRASTRUCTURE DEVELOPMENT AND EXPANSION OF FREIGHT TRANSPORTATION TO DRIVE MARKET

8.5 KEY PRIMARY INSIGHTS

9 AUTOMOTIVE RUBBER SEALS MARKET, BY EV TYPE

9.1 INTRODUCTION

9.2 BEV

9.2.1 HIGH DEMAND FOR PRECISION SEALING IN BATTERY AND CABIN SYSTEMS TO DRIVE MARKET

9.3 PHEV

9.3.1 GROWING DEMAND FOR HYBRID SPECIFIC SEALING SOLUTIONS TO DRIVE MARKET

9.4 KEY PRIMARY INSIGHTS

10 AUTOMOTIVE RUBBER SEALS MARKET, BY MATERIAL

10.1 INTRODUCTION

10.2 TPE/TPV

10.2.1 FOCUS ON ENABLING LIGHTWEIGHT, MULTIFUNCTIONAL SEALING SOLUTIONS FOR PREMIUM EVS TO DRIVE MARKET

10.3 PVC

10.3.1 NEED FOR COST-EFFECTIVE SEALING SOLUTIONS FOR ENTRY-LEVEL AND HIGH-VOLUME VEHICLES TO BOOST GROWTH

10.4 SILICONE-BASED SEALS

10.4.1 DEMAND FOR HIGH-PERFORMANCE SOLUTIONS FOR PREMIUM AND LUXURY VEHICLES TO DRIVE MARKET

10.5 EPDM RUBBER

10.5.1 USE OF CORE MATERIAL TO DRIVE PERFORMANCE AND DURABILITY IN AUTOMOTIVE SEALS

10.6 KEY PRIMARY INSIGHTS

11 AUTOMOTIVE RUBBER SEALS MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 MACROECONOMIC OUTLOOK

11.2.2 CHINA

11.2.2.1 Local manufacturing and mass production of EVs to drive market

11.2.3 INDIA

11.2.3.1 Rise in domestic weatherstrip manufacturers to drive market

11.2.4 JAPAN

11.2.4.1 Investment in R&D for advanced rubber seal technologies to drive market

11.2.5 SOUTH KOREA

11.2.5.1 Partnerships between OEMs and local manufacturers to drive market

11.2.6 REST OF ASIA PACIFIC

11.3 EUROPE

11.3.1 MACROECONOMIC OUTLOOK

11.3.2 GERMANY

11.3.2.1 Consumer preference for high-performance and technologically advanced seals to drive market

11.3.3 FRANCE

11.3.3.1 Presence of global and domestic manufacturers to drive market

11.3.4 UK

11.3.4.1 Introduction of advanced technologies and products to drive market

11.3.5 SPAIN

11.3.5.1 Shift toward EVs to drive demand for automotive rubber seals

11.3.6 REST OF EUROPE

11.4 NORTH AMERICA

11.4.1 MACROECONOMIC OUTLOOK

11.4.2 US

11.4.2.1 Rising integration of advanced technologies to drive market

11.4.3 CANADA

11.4.3.1 Focus on setting up strong manufacturing and engineering facilities to drive market

11.4.4 MEXICO

11.4.4.1 Smart home integration and expansion of residential landscapes to drive market

11.5 REST OF THE WORLD

11.5.1 MACROECONOMIC OUTLOOK

11.5.2 BRAZIL

11.5.2.1 Local partnerships and supply contracts to drive market

11.5.3 RUSSIA

11.5.3.1 Increasing use for high-quality door seals in passenger cars and light commercial vehicles to drive market

11.5.4 OTHERS

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025