표면처리 화학제품 시장(-2032년) : 제품 유형별(도금 화학제품, 화성 피막 처리제, 양극산화처리 화학제품, 부동태화 화학제품, 페인트 박리제, 클리너), 처리법별, 기재별, 최종 이용 산업별, 지역별

Surface Treatment Chemical Market by Product Type (Plating Chemicals, Conversion Coating, Anodizing Chemicals, Passivation Chemicals, Paint Strippers, Cleaners), Treatment Method, Base Material, End-Use Industry, and Region - Global Forecast to 2032

상품코드:1854902

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 292 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

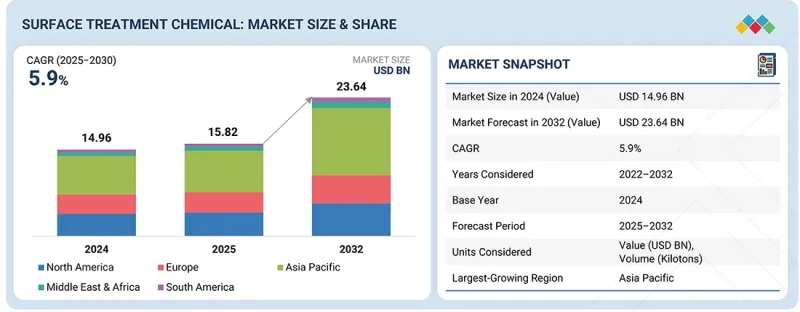

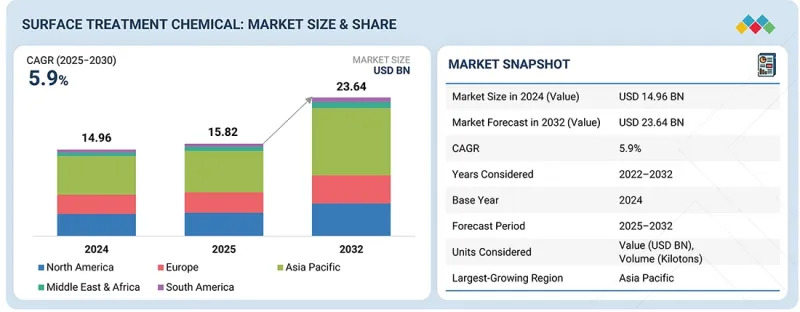

표면처리 화학제품 시장 규모는 2025년 158억 2,000만 달러에서 예측 기간 동안 CAGR 5.9%로 증가하여 2032년에는 236억 4,000만 달러로 성장할 것으로 예측됩니다.

조사 범위

조사 대상 연도

2022-2032년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)·킬로톤

부문

제품 유형·처리법·기재·최종 이용 산업·지역별

대상 지역

유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미

페인트 이형제는 표면처리 화학제품 시장에서 4번째로 빠른 성장이 예상되는 제품 유형입니다. 그 이유는 금속, 목재, 복합재료 등의 표면에서 도막이나 잔류물을 제거하는 데 필수적인 역할을 하기 때문입니다. >페인트 이형제는 자동차, 항공우주, 건설, 산업 유지보수 등 도장, 코팅, 수선의 전처리 공정에 널리 사용되고 있습니다. 화학적 도료 이형제는 견고한 도막을 빠르고 균일하게 용해할 수 있어 작업 시간을 단축하고 고품질 마무리를 실현합니다. 이러한 높은 효율성으로 인해 대규모 제조 및 재생 공정에서 필수적인 화학제품으로 자리매김하고 있습니다.

기술적으로 최근 도료 이형제는 용제계, 알칼리계, 바이오 기반 화학 기술을 활용하여 기재를 손상시키지 않고 고분자 코팅을 분해하는 구조를 채택하고 있습니다. 이를 통해 스틸, 알루미늄, 복합재, 플라스틱 등 다양한 소재에 대응할 수 있습니다. 또한, 저VOC, 크롬 프리 등 환경 및 안전 규제에 대한 적합성도 확보하고 있습니다. 높은 효율성, 광범위한 재료 적응력, 법규 준수의 삼박자가 갖추어져 있기 때문에 페인트 이형제 규모는 여전히 시장에서 두 번째로 큰 규모를 유지하고 있습니다.

"예측 기간 동안 전기 및 전자 산업이 가장 빠르게 성장하는 최종사용자 산업이 될 것"

이는 전자기기의 고밀도화, 소형화, 고성능화가 진행됨에 따라 표면처리의 정확성, 신뢰성, 내구성이 요구되고 있기 때문입니다. 표면처리 화학제품은 인쇄회로기판, 커넥터, 반도체, 케이스 등에서 접착력, 내식성, 전기절연성을 확보하기 위해 필수적입니다. 특히, 고밀도 부품에 대한 정밀 코팅, 열 관리 및 절연 특성 강화, 저 VOC, 할로겐 프리, RoHS 준수 등 환경 규제 대응이 수요를 견인하고 있습니다. 또한, 5G 인프라, IoT 기기, EV 전자제품, 산업 자동화 등 고부가가치 용도의 급격한 확대도 특수 표면처리 화학제품의 수요를 증가시키고 있습니다. 이러한 기술적, 규제적 요인이 결합되어 전기 및 전자 분야는 시장에서 세 번째로 큰 최종사용자 산업 부문으로 확고한 입지를 구축했습니다.

"유럽 지역이 예측 기간 동안 시장 점유율 2위를 차지할 것으로 예상"

유럽은 자동차, 항공우주, 산업기계, 전자 등 첨단 산업 분야가 발달하여 세계 표면처리 화학제품 시장에서 2위의 점유율을 차지하고 있습니다. 이 지역에는 Volkswagen, Airbus, BMW, Siemens 등 주요 OEM이 밀집해 있으며, 방청, 내마모성, 외관 품질 향상을 위해 고도의 표면처리 기술을 널리 채택하고 있습니다. 특히, 프랑스, 독일, 영국의 항공우주 산업은 엄격한 안전 및 성능 기준이 적용되어 고기능성 코팅제 및 도금 화학제품에 대한 수요가 높은 분야입니다. 또한, REACH 규정(화학제품 등록, 평가, 허가, 제한)과 ELV 지침(자동차 폐기 규제)과 같은 유럽의 독자적인 환경 규제가 저VOC, 6가 크롬이 없는 친환경 화학제품으로의 전환을 가속화하고 있습니다. 이를 통해 Henkel, BASF, Chemetall, PPG Industries 등 주요 기업들이 지속가능한 고성능 표면처리 솔루션을 개발 및 공급하는 허브로 자리매김하고 있습니다. 그 결과, 유럽은 지속가능성과 기술 혁신을 겸비한 시장 거점으로서 앞으로도 표면처리 화학제품 분야에서 강력한 영향력을 유지할 것으로 전망됩니다.

세계의 표면처리 화학제품 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 지표

밸류체인 분석

생태계 분석

사례 연구 분석

규제 상황

기술 분석

고객의 사업에 영향을 미치는 동향/혼란

무역 분석

주요 회의와 이벤트

가격 분석

투자와 자금 조달 시나리오

특허 분석

2025년 미국 관세의 영향

제6장 표면처리 화학제품 시장 : 제품 유형별

도금 화학제품

화성 피막 처리제

양극산화처리 화학제품

부동태화 화학제품

페인트 박리제

클리너

기타

제7장 표면처리 화학제품 시장 : 처리법별

전기도금

화학처리

용사

용융 도금

기타

제8장 표면처리 화학제품 시장 : 기재별

금속

플라스틱

목재

유리

복합재료

기타

제9장 표면처리 화학제품 시장 : 최종 이용 산업별

운송

건설

전기·전자공학

포장

산업기계

섬유

기타

제10장 표면처리 화학제품 시장 : 지역별

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

기타

아시아태평양

중국

일본

인도

한국

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

기타

제11장 경쟁 구도

개요

주요 진출 기업의 전략/강점

매출 분석

시장 점유율 분석

기업 평가와 재무 지표

제품 비교 분석

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업/중소기업

경쟁 시나리오

제12장 기업 개요

주요 기업

HENKEL AG & CO. KGAA

CHEMETALL GMBH

PPG INDUSTRIES, INC.

MKS ATOTECH

ELEMENT SOLUTIONS INC

NIPPON PAINT HOLDINGS CO., LTD.

NIHON PARKERIZING CO., LTD.

AXALTA COATING SYSTEMS, LLC

NOF CORPORATION

DOW

THE SHERWIN-WILLIAMS COMPANY

AKZO NOBEL N.V.

기타 주요 기업

QUAKER HOUGHTON

MCGEAN-ROHCO INC.

EVONIK

JCU INTERNATIONAL, INC.

CHEMBOND MATERIAL TECHNOLOGIES PVT. LTD.

CHEMISCHE WERKE KLUTHE GMBH

DUBOIS CHEMICALS

WUHAN JADECHEM INTERNATIONAL TRADE CO., LTD.

SURTEC

CHEMTECH SURFACE FINISHING PVT. LTD.

AUROMEX CO., LTD.

VANCHEM PERFORMANCE CHEMICALS

AD INTERNATIONAL B.V.

COLUMBIA CHEMICAL

ASTENA HOLDINGS CO., LTD.

ARTEK SURFIN CHEMICALS LTD.

GRAUER & WEIL(INDIA) LIMITED

제13장 부록

KSM

영문 목차

영문목차

The surface treatment chemical market is projected to grow from USD 15.82 Billion in 2025 to USD 23.64 Billion by 2032, at a CAGR of 5.9% during the forecast period.

Scope of the Report

Years Considered for the Study

2022-2032

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Kilotons)

Segments

By Product Type, By Treatment Method, By Base Material, By End-Use Industry, and Region

Regions covered

Europe, North America, Asia Pacific, the Middle East & Africa, and South America

Paint strippers is expected to be fourth fastest growing product type in the surface treatment chemical market due to their critical role in removing coatings, paints, and surface residues from metal, wood, and composite substrates across multiple industries. They are widely used in automotive, aerospace, construction, and industrial maintenance for surface preparation before painting, coating, or repair. The effectiveness of chemical paint strippers in dissolving tough coatings quickly and uniformly reduces labor time and ensures high-quality finishing, making them indispensable in large-scale manufacturing and refurbishment operations.

Technically, modern paint strippers leverage solvents, alkaline solutions, and innovative bio-based chemistries that penetrate and break down polymeric coatings without damaging the substrate. This versatility allows them to handle diverse materials-steel, aluminum, composites, and plastics-while meeting stricter environmental and safety regulations, such as low-VOC and chromium-free formulations. The combination of high efficiency, broad material compatibility, and regulatory compliance drives strong demand, maintaining paint strippers as the second-largest segment in the surface treatment chemical market..

''In terms of value, plastic as base material is expected to be the fastest growing of the overall surface treatment chemical market.''

Plastics hold the fastest growing market as a base material in the surface treatment chemical market due to several unique technical and industrial factors. The rapid adoption of high-performance engineering plastics (such as PEEK, Nylon, and polyimides) in sectors like automotive, electronics, and medical devices has increased the need for specialized chemical treatments to enhance surface functionality, such as scratch resistance, chemical resistance, and thermal stability.

Plastics often require anti-static, hydrophobic, or hydrophilic surface properties, depending on the application-necessitating advanced chemical treatments like plasma-assisted or chemical etching processes. As industries shift toward lightweighting and flexible components, more intricate plastic geometries are used, demanding precise and uniform surface treatments that only specialized chemical solutions can achieve. Increasing regulatory pressure for environmentally safe and non-toxic surface treatment solutions in consumer-facing plastic products has encouraged the use of engineered chemicals that provide performance without compromising safety or compliance.

"During the forecast period, electrical & electronics end use industry is projected to have fastest growing market."

The Electrical & Electronics sector accounts for the fastest growing end-use segment in the surface treatment chemical market, driven by the increasing complexity, miniaturization, and performance requirements of modern electronic devices. Surface treatment chemicals play a critical role in ensuring reliable adhesion, corrosion resistance, and electrical insulation for components such as printed circuit boards, connectors, semiconductors, and housings. Demand is underpinned by the need for precise coating deposition on high-density components, enhanced thermal management and dielectric properties, and compliance with global environmental and safety regulations, including low-VOC, halogen-free, and RoHS standards. The rapid adoption of high-value applications, including 5G infrastructure, IoT devices, EV electronics, and industrial automation, further drives the use of specialized surface treatment chemistries tailored to diverse substrates. Collectively, these technical and regulatory factors solidify Electrical & Electronics as the third-largest end-use segment in the surface treatment chemical market.

"During the forecast period, the surface treatment chemical market in Europe region is projected to have second largest market share."

Europe holds the second-largest share of the global surface treatment chemical market, supported by its well-established automotive, aerospace, industrial machinery, and electronics sectors. The region is home to leading OEMs such as Volkswagen, Airbus, BMW, and Siemens, all of which require advanced surface treatment solutions for corrosion protection, wear resistance, and improved aesthetic finishes. The aerospace hubs in France, Germany, and the UK are particularly significant, as the stringent performance and safety standards in aviation necessitate the use of high-performance coatings and plating chemicals. Another driver is Europe's strict regulatory framework, such as REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) and ELV (End-of-Life Vehicles) directives, which have accelerated the adoption of eco-friendly, low-VOC, and hexavalent-chromium-free surface treatment formulations. This has prompted innovation from major players like Henkel AG & Co. KGaA, BASF SE, Chemetall GmbH, and PPG Industries, positioning Europe as a hub for sustainable and advanced solutions.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies Chemetall gmbH (Germany), Henkel AG & Co. KGaA (Germany), Nippon Paint Holdings Co., Ltd. (Japan), PPG INDUSTRIES, INC. (US), Nihon Parkerizing Co., Ltd. (Japan), MKS Atotech (Germany), Element Solutions Inc (US), Axalta Coating Systems , LLC (US), Dow (US), The Sherwin-Williams Compant (US), AkzoNobel (Netherlands).

Research Coverage

This research report categorizes the surface treatment chemical market by product type (Plating Chemicals, Conversion Coating, Anodizing Chemicals, Passivation Chemicals, Paint Strippers, Cleaners Others), by treatment Method (Electroplating, Chemical Treatment, Thermal Spraying, Hot Dipping and Other), by Base Material (Metals, Plastics, Wood, Glass and Composites). End-Use Industry Region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the surface treatment chemical market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the surface treatment chemical market are all covered. This report includes a competitive analysis of upcoming startups in the surface treatment chemical market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall surface treatment chemical market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Robust demand from automotive sectors, Semiconductor growth creating demand in the market), restraints (Stringent compliance standards pose barriers to surface treatment chemical market), opportunities (Technological advancements in smart treatments, Growing adoption of lightweight aluminum alloys in EVs driving need for specialized pretreatment and coating solutions) and challenges (High costs and technical hurdles in adopting surface treatment chemicals)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the surface treatment chemical market.

Market Development: Comprehensive information about lucrative markets - the report analyses the surface treatment chemical market across varied regions.

Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the surface treatment chemical market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Chemetall gmbH (Germany), Henkel AG & Co. KGaA (Germany), Nippon Paint Holdings Co., Ltd. (Japan), PPG INDUSTRIES, INC. (US), Nihon Parkerizing Co., Ltd. (Japan), MKS Atotech (Germany), Element Solutions Inc (US), Axalta Coating Systems , LLC (US), Dow (US), The Sherwin-Williams Compant (US), AkzoNobel (Netherlands) among others in the surface treatment chemical market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants-demand and supply sides

2.1.2.2 Key data from primary sources

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 FORECAST NUMBER CALCULATION

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 OPPORTUNITIES FOR PLAYERS IN SURFACE TREATMENT CHEMICALS MARKET

4.2 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE

4.3 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD

4.4 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL

4.5 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY

4.6 SURFACE TREATMENT CHEMICALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Robust demand from automotive sector

5.2.1.2 Semiconductor industry growth creating demand

5.2.1.3 Industrialization and infrastructure growth in emerging economies

5.2.2 RESTRAINTS

5.2.2.1 Stringent compliance standards

5.2.3 OPPORTUNITIES

5.2.3.1 Technological advancements in smart treatments

5.2.3.2 Growing adoption of lightweight aluminum alloys in EVs demanding specialized pretreatment and coating solutions

5.2.4 CHALLENGES

5.2.4.1 High costs and technical hurdles in adopting surface treatment chemicals

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 BARGAINING POWER OF SUPPLIERS

5.3.2 BARGAINING POWER OF BUYERS

5.3.3 THREAT OF NEW ENTRANTS

5.3.4 THREAT OF SUBSTITUTES

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS & BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GLOBAL GDP TRENDS

5.6 VALUE CHAIN ANALYSIS

5.6.1 RAW MATERIAL SUPPLIERS

5.6.2 MANUFACTURERS

5.6.3 DISTRIBUTORS

5.6.4 END USERS

5.7 ECOSYSTEM ANALYSIS

5.8 CASE STUDY ANALYSIS

5.8.1 HOUGHTON DELIVERS SUSTAINABLE SURFACE SOLUTIONS FOR AUTOMOTIVE AND AEROSPACE INDUSTRIES

5.8.2 DUBOIS TRANSFORMS PRETREATMENT CHALLENGES INTO SUSTAINABLE RESULTS

5.8.3 YAMAHA AND METALUMEN ACHIEVE NEXT-LEVEL PERFORMANCE WITH VANCHEM SOLUTIONS

5.9 REGULATORY LANDSCAPE

5.9.1 REGULATIONS

5.9.1.1 Europe

5.9.1.2 Asia Pacific

5.9.1.3 North America

5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10 TECHNOLOGY ANALYSIS

5.10.1 KEY TECHNOLOGIES

5.10.1.1 Enabling 2.xD/3D packaging through chemistry

5.10.1.2 Advanced functional and nanostructured coatings

5.10.2 COMPLEMENTARY TECHNOLOGIES

5.10.2.1 Laser-assisted surface preparation

5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.12 TRADE ANALYSIS

5.12.1 EXPORT SCENARIO

5.12.2 IMPORT SCENARIO

5.13 KEY CONFERENCES AND EVENTS, 2025-2027

5.14 PRICING ANALYSIS

5.14.1 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY REGION, 2022-2024

5.14.2 AVERAGE SELLING PRICE TREND OF SURFACE TREATMENT CHEMICALS, BY APPLICATION, 2022-2024

5.14.3 AVERAGE SELLING PRICES OF SURFACE TREATMENT CHEMICALS OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

5.15 INVESTMENT AND FUNDING SCENARIO

5.16 PATENT ANALYSIS

5.16.1 APPROACH

5.16.2 DOCUMENT TYPES

5.16.3 PUBLICATION TRENDS, 2014-2024

5.16.4 INSIGHTS

5.16.5 LEGAL STATUS OF PATENTS

5.16.6 JURISDICTION ANALYSIS FROM 2014 TO 2024

5.16.7 TOP COMPANIES/APPLICANTS

5.16.8 TOP 10 PATENT OWNERS (US) 2014-2024

5.17 IMPACT OF 2025 US TARIFF - SURFACE TREATMENT CHEMICALS MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON KEY COUNTRIES/REGIONS

5.17.4.1 North America

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE INDUSTRIES

6 SURFACE TREATMENT CHEMICALS MARKET, BY PRODUCT TYPE

6.1 INTRODUCTION

6.2 PLATING CHEMICAL

6.2.1 ENHANCED CORROSION RESISTANCE, WEAR RESISTANCE, AND ELECTRICAL CONDUCTIVITY

6.3 CONVERSION COATING

6.3.1 RELIABLE PRETREATMENT FOR AUTOMOTIVE AND INDUSTRIAL METALS

6.4 ANODIZING CHEMICAL

6.4.1 TRANSFORMING SURFACES WITH INNOVATIVE ANODIZING CHEMICALS

6.5 PASSIVATION CHEMICAL

6.5.1 PASSIVATION FOR HIGH-INTEGRITY STAINLESS STEEL APPLICATIONS

6.6 PAINT STRIPPER

6.6.1 PROTECTING SUBSTRATES WHILE REMOVING COATINGS

6.7 CLEANERS

6.7.1 INDUSTRIAL CLEANERS THAT PROTECT AND PREPARE SURFACES

6.8 OTHER PRODUCT TYPES

7 SURFACE TREATMENT CHEMICALS MARKET, BY TREATMENT METHOD

7.1 INTRODUCTION

7.2 ELECTROPLATING

7.2.1 ENHANCING DURABILITY AND FUNCTIONALITY WITH ELECTROPLATING

7.3 CHEMICAL TREATMENT

7.3.1 IMPROVING PAINT ADHESION AND COATING DURABILITY

7.4 THERMAL SPRAYING

7.4.1 PROTECTIVE AND FUNCTIONAL COATINGS FOR EXTREME ENVIRONMENTS

7.5 HOT DIPPING

7.5.1 RELIABLE IN APPLICATIONS WHERE DURABILITY AND LOW MAINTENANCE ARE ESSENTIAL

7.6 OTHER TREATMENT METHODS

8 SURFACE TREATMENT CHEMICALS MARKET, BY BASE MATERIAL

8.1 INTRODUCTION

8.2 METALS

8.2.1 ADVANCED METAL PRETREATMENT FOR HIGH-QUALITY FINISHES

8.3 PLASTICS

8.3.1 IMPROVING WETTABILITY AND ADHESION ON POLYOLEFINS

8.4 WOOD

8.4.1 PROTECTING WOOD WHILE MAINTAINING TEXTURE AND FINISH

8.5 GLASS

8.5.1 SUPERIOR ADHESION AND ELECTRICAL PERFORMANCE FOR GLASS

8.6 COMPOSITES

8.6.1 HIGH-PRECISION TREATMENTS FOR ENHANCED COMPOSITE ADHESION

8.7 OTHER BASE MATERIALS

9 SURFACE TREATMENT CHEMICALS MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 TRANSPORTATION

9.2.1 RUST PROTECTION AS CORE TRANSPORTATION PRIORITY

9.3 CONSTRUCTION

9.3.1 IMPROVING INFRASTRUCTURE RESILIENCE THROUGH SURFACE TREATMENTS

9.4 ELECTRICAL & ELECTRONICS

9.4.1 PROTECTING ELECTRONICS WITH CORROSION-RESISTANT COATINGS

9.5 PACKAGING

9.5.1 RISING IMPORTANCE OF SURFACE PREPARATION FOR PACKAGING MATERIALS

9.6 INDUSTRIAL MACHINERY

9.6.1 SURFACE CLEANING AND PREPARATION FOR HEAVY-DUTY APPLICATIONS

9.7 TEXTILES

9.7.1 EXPANDING APPLICATIONS OF FUNCTIONAL TEXTILE TREATMENTS

9.8 OTHER END-USE INDUSTRIES

10 SURFACE TREATMENT CHEMICALS MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 US

10.2.1.1 Growing demand for automobiles influenced by EV sales to drive market

10.2.2 CANADA

10.2.2.1 Government investment to reduce import reliance to benefit automotive sector

10.2.3 MEXICO

10.2.3.1 Manufacturing and nearshoring to drive industrial market

10.3 EUROPE

10.3.1 GERMANY

10.3.1.1 Fast growth of electrical & electronics industry to drive market

10.3.2 FRANCE

10.3.2.1 Transportation and construction to drive market