Laser Interferometer Market by Technique (Homodyne, Heterodyne), Type (Michelson, Fabry-Perot, Fizeau, Mach-Zehnder, Sagnac, Twyman-green), Component (Laser, Photodetector, Optical), Application (Surface Topology, Biomedical) - Global Forecast to 2030

상품코드:1854900

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 247 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

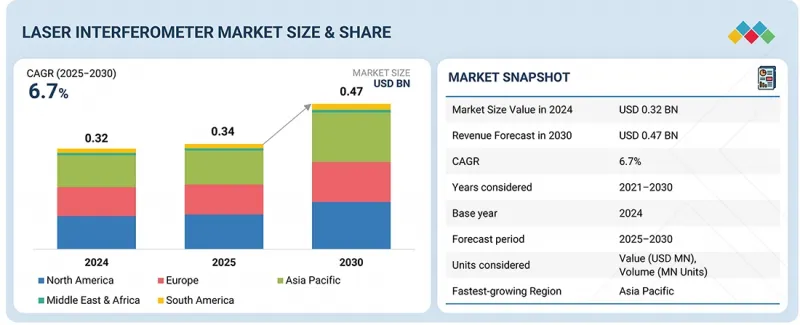

레이저 간섭계 시장 규모는 예측 기간 동안 CAGR 6.7%로 증가하여 2025년 3억 4,000만 달러에서 2030년에는 4억 7,000만 달러로 성장할 것으로 예측됩니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(달러)

부문

기술, 유형, 구성요소, 용도, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

반도체 소자의 소형화 진전은 레이저 간섭계의 수요를 크게 끌어올리고 있습니다. 나노미터 수준까지 미세화가 진행되면서 초정밀, 초정밀, 고신뢰성 측정기술이 필수적이기 때문입니다. 레이저 간섭계는 서브나노미터의 정밀도를 실현하여 반도체 제조업체가 웨이퍼 표면의 평탄도, 균일성, 결함을 고정밀도로 측정, 검사 및 제어할 수 있습니다. 이는 디바이스 성능을 보장하는 데 필수적인 요소입니다. 또한, 레이저 간섭계는 MEMS 개발에도 중요한 역할을 하고 있으며, 표면 형상의 정확한 측정을 통해 미세 부품의 신뢰성을 보장하고 있습니다. 또한, 반도체 산업이 3D 스태킹 및 시스템 인 패키지(SiP)와 같은 첨단 패키징 기술로 전환함에 따라 고정밀 정렬 및 치수 측정에 대한 필요성이 더욱 커지고 있습니다. 다층 구조 장치에서는 각 층의 두께, 위치, 정합성을 간섭계로 확인하는 것이 효율성과 기능성과 직결되기 때문입니다.

또한, 새로운 반도체 재료, 공정, 아키텍처가 속속 등장하면서 간섭계 제조업체들은 반도체 업계와의 협업을 통해 기술 혁신을 추진하고 시스템 기능을 지속적으로 발전시키고 있습니다. 이러한 시너지를 통해 끊임없이 진화하는 생산 과제에 대응하는 맞춤형 측정 솔루션을 만들 수 있습니다. 레이저 간섭계의 비접촉식 고해상도 측정 능력은 반도체 품질을 보장하고 차세대 전자 제품 개발을 촉진하며 세계 레이저 간섭계 시장의 성장을 촉진하는 데 필수적인 도구로 자리 매김하고 있습니다.

"헤테로다인 부문이 2025년부터 2030년까지 큰 비중을 차지할 것으로 전망"

그 이유는 뛰어난 측정 정확도와 활용성 때문입니다. 헤테로다인 간섭계는 고해상도의 변위 및 속도 측정을 실현하여 항공우주, 자동차, 반도체, 정밀 엔지니어링 등의 산업에서 필수적인 도구입니다. 특히, 웨이퍼 노광 장비의 위치 조정이나 MEMS 테스트와 같은 초정밀도가 요구되는 환경에서 위상 노이즈 감소와 실시간 안정적인 데이터 수집 능력이 중요하게 여겨지고 있습니다. 제조업에서는 공작기계의 캘리브레이션, 로봇의 얼라이먼트, 동적 진동 분석 등에 활용이 확대되고 있으며, 생산성 향상과 오차 감소에 기여하고 있습니다. 또한, 나노기술 및 미세부품의 활용 확대에 따라 서브나노미터 단위의 측정이 가능한 헤테로다인 간섭계에 대한 수요가 증가하고 있습니다. 또한, 연구기관이나 대학에서도 광학 실험이나 재료 연구에 도입이 진행되고 있습니다. 레이저의 안정성 향상과 소형화, 저비용화도 보급을 촉진하고 있으며, 향후 고정밀화, 고자동화, 고신뢰성을 요구하는 산업에서 헤테로다인 방식은 계속해서 주류의 지위를 유지할 것으로 보입니다.

"북미가 2024년 최대 점유율을 차지"

그 배경에는 첨단 제조업의 집적, 높은 R&D 투자, 정밀 측정 기술의 광범위한 채택이 있습니다. 이 지역의 우위는 주로 항공우주, 자동차, 반도체, 의료 등의 분야에서의 리더십에 기인하며, 이들 산업은 고정밀 검사 및 테스트 장비가 필수적입니다. 미국의 반도체 제조업체와 주요 항공우주 기업들은 엄격한 품질 및 성능 기준을 충족하기 위해 간섭계 솔루션을 일찍이 도입한 것으로 알려져 있습니다. 또한, 전기자동차(EV) 및 자율주행 기술에 대한 수요 증가로 인해 캘리브레이션, 부품 테스트, 표면 토폴로지 측정 등의 분야에서 레이저 간섭계 수요가 더욱 증가하고 있습니다. 북미에는 강력한 기술 제공업체 및 연구기관 생태계가 존재하여 간섭계 기술의 지속적인 혁신을 촉진하고 있습니다. 또한, 정부의 첨단 제조 이니셔티브와 계측 및 산업 자동화에 대한 투자도 시장 성장을 촉진하고 있습니다. 또한, 광학 및 레이저 시스템 분야의 세계적인 리더 기업들이 미국에 기반을 두고 있는 것도 공급 체계와 기술 개발을 강화하는 요인입니다. 이러한 혁신력, 탄탄한 산업 기반, 조기 도입 문화로 인해 북미는 2024년에도 레이저 간섭계 시장에서 선두 자리를 유지할 것으로 보입니다.

세계의 레이저 간섭계 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정과 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

밸류체인 분석

생태계 분석

고객의 사업에 영향을 미치는 동향/혼란

가격 분석

기술 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

무역 분석

특허 분석

2025-2026년의 주요 회의와 이벤트

관세와 규제 상황

AI/생성형 AI가 레이저 간섭계 시장에 미치는 영향

2025년 미국 관세가 레이저 간섭계 시장에 미치는 영향

제6장 레이저 간섭계 구성요소

레이저 광원

광검출기

광학 소자

제어 시스템

소프트웨어

제7장 레이저 간섭계 측정 기술

위상 측정

주파수 측정

진폭 측정

비행 시간 측정

제8장 레이저 간섭계 설계

벤치탑 시스템

휴대용/핸드헬드 시스템

인라인/프로세스 시스템

모듈러 시스템

비행 시간형 시스템

제9장 레이저 간섭계 시장 : 유형별

마이켈슨 간섭계

파브리페로 간섭계

피조 간섭계

마하젠더 간섭계

사냑 간섭계

트와이만그린 간섭

제10장 레이저 간섭계 시장 : 기술별

호모다인

헤테로다인

제11장 레이저 간섭계 시장 : 용도별

표면 토폴로지

엔지니어링

응용 과학

바이오메디컬

반도체 검출

제12장 레이저 간섭계 시장 : 산업별

자동차

항공우주 및 방위

산업

의료

일렉트로닉스·반도체

통신

제13장 레이저 간섭계 시장 : 지역별

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

영국

독일

프랑스

이탈리아

기타

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

한국

기타

기타 지역

기타 지역의 거시경제 전망

중동

아프리카

남미

제14장 경쟁 구도

개요

주요 진출 기업의 전략/강점

매출 분석

시장 점유율 분석

기업 평가와 재무 지표

제품 비교

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 스타트업/중소기업

경쟁 시나리오

제15장 기업 개요

주요 기업

RENISHAW PLC

KEYSIGHT TECHNOLOGIES

ZEISS GROUP

ZYGO CORPORATION

BRUKER

MAHR GMBH

MOLLER-WEDEL OPTICAL GMBH

QED TECHNOLOGIES

SIOS MEBTECHNIK GMBH

TOSEI ENGINEERING CORP.

AUTOMATED PRECISION INC(API)

기타 기업

PRATT AND WHITNEY MEASUREMENT SYSTEMS, INC.

SMARACT GMBH

LASERTEX

LUNA

4D TECHNOLOGY CORP.

APRE INSTRUMENTS

ADLOPTICA OPTICAL SYSTEMS GMBH

LOGITECH

HOLMARC OPTO-MECHATRONICS LTD.

ATTOCUBE SYSTEMS GMBH

HIGHFINESSE GMBH

XONOX TECHNOLOGY GMBH

THORLABS, INC.

LASERTEC CORPORATION

FUJIFILM HOLDINGS CORPORATION

OLYMPUS CORPORATION

제16장 부록

KSM

영문 목차

영문목차

The laser interferometer market is projected to grow from USD 0.34 billion in 2025 to USD 0.47 billion by 2030, at a CAGR of 6.7% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Technique, Type, Component, Application and Region

Regions covered

North America, Europe, APAC, RoW

The growing trend of semiconductor device miniaturization is significantly boosting the demand for laser interferometers, as shrinking feature sizes to the nanometre scale require precise and reliable metrology tools. Laser interferometers provide sub-nanometre accuracy, enabling semiconductor manufacturers to measure, inspect, and control wafer surfaces for flatness, uniformity, and defects, which are crucial for ensuring device performance. They are equally vital in supporting the development of micro-electromechanical systems (MEMS), where accurate surface topology measurements ensure the reliability of miniature components. With the semiconductor industry shifting toward advanced packaging techniques such as 3D stacking and system-in-package (SiP), the need for precision alignment and measurement becomes even more critical. Multi-layer device architectures rely on interferometers to verify the thickness, placement, and alignment of each layer, directly impacting efficiency and functionality.

Additionally, as new semiconductor materials, processes, and architectures emerge, interferometer manufacturers continuously advance system capabilities, fostering innovation through collaboration with the semiconductor industry. This synergy enables the creation of tailored metrology solutions to meet evolving production challenges. The ability of laser interferometers to deliver non-contact, high-resolution measurements positions them as indispensable tools for ensuring semiconductor quality, driving next-generation electronics development, and fuelling growth in the global laser interferometer market.

"Heterodyne segment is likely to contribute a major share of the laser interferometer market from 2025 to 2030."

The heterodyne segment is likely to contribute a major share of the laser interferometer market from 2025 to 2030, owing to its superior measurement accuracy and versatility across diverse applications. Heterodyne interferometers offer high-resolution displacement and velocity measurements, making them invaluable in industries such as aerospace, automotive, semiconductor, and precision engineering. Their ability to minimize phase noise and provide stable, real-time data is especially important in environments requiring ultra-high precision, such as wafer lithography alignment and microelectromechanical systems (MEMS) testing. In manufacturing, heterodyne systems are increasingly used for machine tool calibration, robotic alignment, and dynamic vibration analysis, all of which are critical to ensuring productivity and minimizing operational errors. The growing use of nanotechnology and miniaturized components is also amplifying demand for heterodyne interferometers due to their ability to measure at the sub-nanometre scale. Furthermore, research and academic institutions are expanding their adoption of these systems for advanced optical experiments and material studies. Continuous innovations in laser stability, coupled with the trend toward compact, cost-efficient heterodyne solutions, are further boosting adoption. As industries pursue higher precision, tighter tolerances, and greater automation, heterodyne interferometers are set to remain the dominant choice, solidifying their large market share during the forecast period.

"Surface topology application segment is expected to record a significant CAGR in the laser interferometer market from 2025 to 2030."

The surface topology application segment is projected to record a significant CAGR in the laser interferometer market between 2025 and 2030, driven by the rising demand for ultra-precise surface characterization across industries. Surface topology measurement enables manufacturers to detect minute irregularities, roughness, and flatness on critical components, ensuring reliability and compliance with stringent quality standards. In the semiconductor industry, where wafer surfaces must achieve near-perfect flatness, laser interferometers play a crucial role in reducing defects and improving yield rates. Similarly, in optics and photonics, accurate measurement of lens and mirror surfaces ensures optimal performance of imaging systems. Automotive and aerospace manufacturers are also investing in surface topology solutions to validate advanced materials and components used in electric vehicles, aircraft engines, and lightweight structures. With the growing adoption of additive manufacturing and nanotechnology, the need for non-contact, high-resolution, and real-time surface topology inspection is accelerating. Advances in laser stability and digital imaging technologies further enhance the efficiency of these interferometers. The increasing integration of AI-driven analysis for faster defect detection and automation-friendly solutions is also supporting growth. Collectively, these factors position surface topology as one of the fastest-growing application segments in the laser interferometer market over the forecast period.

"North America accounted for the largest share of the laser interferometer market in 2024."

North America accounted for the largest share of the laser interferometer market in 2024, supported by its strong base of advanced manufacturing industries, high R&D spending, and widespread adoption of precision measurement technologies. The region's dominance is largely attributed to its leadership in aerospace, automotive, semiconductor, and healthcare sectors, all of which require high-accuracy inspection and testing tools. U.S.-based semiconductor manufacturers, along with major aerospace companies, have been early adopters of interferometer solutions to meet stringent quality and performance standards. The growing demand for electric vehicles and autonomous driving technologies has further increased the need for laser interferometers in calibration, component testing, and surface topology measurements. Additionally, North America has a robust ecosystem of technology providers and research institutions driving continuous innovation in laser interferometry. The region also benefits from favourable government support for advanced manufacturing initiatives and increasing investments in metrology and industrial automation. Healthcare applications, including optical diagnostics and ophthalmology, add another dimension to market growth. Furthermore, the presence of global leaders in laser and optical systems in the US strengthens supply capabilities and technological advancements. With its combination of innovation, strong end-user industries, and early adoption trends, North America maintained its lead in the laser interferometer market in 2024.

By Company Type: Tier 1 - 26%, Tier 2 - 32%, and Tier 3 - 42%

By Designation: C-level Executives - 40%, Managers - 30%, and Others - 30%

By Region: North America - 34%, Europe - 25%, Asia Pacific- 30%, and RoW - 11%

Prominent players profiled in this report include Renishaw plc (UK), Keysight Technologies (US), ZEISS Group (Germany), Zygo Corporation (US), and Bruker (US).

Report Coverage

The report defines, describes, and forecasts the laser interferometer market based on type (michelson interferometer, fabry-perot interferometer, fizeau interferometer, mach-zehnder interferometer, sagnac interferometer, twyman-green interferometer), technique (homodyne, heterodyne), application (surface topology, engineering, applied science, biomedical, semiconductor detection), vertical (automotive, aerospace & defense, industrial, healthcare, electronics & semiconductor, telecommunications) and region (North America, Europe, Asia Pacific, RoW). It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the market growth. It also analyzes competitive developments such as acquisitions, product launches, expansions, and actions carried out by the key players to grow in the market.

Reasons to Buy This Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue for the overall laser interferometer market and the subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

Analysis of key drivers (Surging demand for precision in manufacturing and quality control, Growing trend of miniaturization of semiconductor devices, Extremely tight tolerances in aerospace & defence and automotive verticals), restraints (High ownership and maintenance costs, Adverse impact of environmental conditions on measurement accuracy, Availability of alternative measurement tools, Risks associated with constant technological upgrades and obsolescence of existing equipment), opportunities (Industrialization in emerging markets, Integration of laser interferometry with automated production lines,

cloud-based platforms, and Industry 4.0 technologies, growing emphasis on developing more user-friendly and cost-effective models, elevating demand for advanced medical devices, and challenges (Requirement for skilled personnel to handle complex operations) of the laser interferometer market

Product development /Innovation: Detailed insights into upcoming technologies, research & development activities, and new product launches in the laser interferometer market

Market Development: Comprehensive information about lucrative markets; the report analyses the laser interferometer market across various regions

Market Diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the laser interferometer market

Competitive Assessment: In-depth assessment of market share, growth strategies, and offering of leading players, including Renishaw plc (UK), Keysight Technologies (US), ZEISS Group (Germany), Zygo Corporation (US), Bruker (US), Mahr GmbH (Germany), MOLLER-WEDEL OPTICAL GMBH (Switzerland), QED Technologies (US), SIOS MeBtechnik GmbH (Germany), in the laser interferometer market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of primary interview participants

2.1.3.2 Breakdown of primaries

2.1.3.3 Key data from primary sources

2.1.3.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LASER INTERFEROMETER MARKET

4.2 LASER INTERFEROMETER MARKET, BY APPLICATION

4.3 LASER INTERFEROMETER MARKET, BY VERTICAL

4.4 LASER INTERFEROMETER MARKET, BY TECHNIQUE

4.5 LASER INTERFEROMETER MARKET IN ASIA PACIFIC, BY VERTICAL AND COUNTRY

4.6 LASER INTERFEROMETER MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing need for precise manufacturing and quality control

5.2.1.2 Growing trend of miniaturization of semiconductor devices

5.2.1.3 Requirement for extremely tight tolerances in aerospace & defense and automotive verticals

5.2.2 RESTRAINTS

5.2.2.1 High ownership and maintenance costs

5.2.2.2 Adverse impact of environmental conditions on measurement accuracy

5.2.2.3 Availability of alternative measurement tools

5.2.2.4 Risks associated with constant technological upgrades and obsolescence of existing equipment

5.2.3 OPPORTUNITIES

5.2.3.1 Rapid industrialization in emerging markets

5.2.3.2 Integration of laser interferometry with automated production lines, cloud-based platforms, and Industry 4.0 technologies

5.2.3.3 Growing emphasis on developing user-friendly and cost-effective models

5.2.3.4 Mounting demand for advanced medical devices

5.2.4 CHALLENGES

5.2.4.1 Requirement for skilled personnel to handle complex operations

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.6 PRICING ANALYSIS

5.6.1 AVERAGE SELLING PRICE OF FABRY-PEROT LASER INTERFEROMETERS, BY KEY PLAYER, 2024

5.6.2 PRICING RANGE OF LASER INTERFEROMETERS, BY TYPE, 2024

5.6.3 AVERAGE SELLING PRICE TREND OF LASER INTERFEROMETERS, BY REGION, 2021-2024

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Laser sources

5.7.1.2 Beam splitters

5.7.2 COMPLEMENTARY TECHNOLOGIES

5.7.2.1 Coordinate measuring machines

5.7.2.2 Liner encoders

5.7.3 ADJACENT TECHNOLOGIES

5.7.3.1 Fourier transform infrared spectroscopy

5.7.3.2 Optical coherence tomography

5.8 PORTER'S FIVE FORCES ANALYSIS

5.8.1 THREAT OF NEW ENTRANTS

5.8.2 THREAT OF SUBSTITUTES

5.8.3 BARGAINING POWER OF SUPPLIERS

5.8.4 BARGAINING POWER OF BUYERS

5.8.5 INTENSITY OF COMPETITIVE RIVALRY

5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.9.2 BUYING CRITERIA

5.10 CASE STUDY ANALYSIS

5.10.1 US DEPARTMENT OF DEFENSE USES LASER INTERFERENCE STRUCTURING SYSTEM TO PREPARE SURFACES FOR PROTECTIVE COATINGS

5.10.2 MATERIAL INSPECTION MACHINES USE WHITE-LIGHT INTERFEROMETRY TO ACHIEVE FAST PRECISION MEASUREMENTS

5.10.3 SCIENTISTS FROM GERMANY DEMONSTRATE ATOM INTERFEROMETRY IN SPACE TO MEASURE GRAVITATIONAL FORCE

5.10.4 MACHINE REPAIR SPECIALIST INVESTS IN MULTI-AXIS CALIBRATORS TO EXPAND ITS SERVICES

5.10.5 BOST REDUCES MACHINE SETUP TIME BY 50% USING RENISHAW'S MACHINE CALIBRATOR AND LASER INTERFEROMETER

5.11 TRADE ANALYSIS

5.11.1 IMPORT SCENARIO (HS CODE 903149)

5.11.2 EXPORT SCENARIO (HS CODE 903149)

5.12 PATENT ANALYSIS

5.13 KEY CONFERENCES AND EVENTS, 2025-2026

5.14 TARIFF AND REGULATORY LANDSCAPE

5.14.1 TARIFF ANALYSIS

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.14.3 STANDARDS AND REGULATIONS

5.15 IMPACT OF AI/GEN AI ON LASER INTERFEROMETER MARKET

5.15.1 INTRODUCTION

5.15.2 TOP AI/GEN AI USE CASES

5.15.2.1 Wafer metrology & lithography alignment

5.15.2.2 Satellite component testing

5.15.2.3 Optical coherence tomography (OCT)

5.15.2.4 Real-time fault detection

5.15.2.5 Precision tool calibration

5.16 IMPACT OF 2025 US TARIFF ON LASER INTERFEROMETER MARKET

5.16.1 INTRODUCTION

5.16.2 KEY TARIFF RATES

5.16.3 PRICE IMPACT ANALYSIS

5.16.4 IMPACT ON COUNTRIES/REGIONS

5.16.4.1 US

5.16.4.2 Europe

5.16.4.3 Asia Pacific

5.16.5 IMPACT ON VERTICALS

6 COMPONENTS OF LASER INTERFEROMETERS

6.1 INTRODUCTION

6.2 LASER SOURCES

6.3 PHOTODETECTORS

6.4 OPTICAL ELEMENTS

6.5 CONTROL SYSTEMS

6.6 SOFTWARE

7 MEASUREMENT TECHNIQUES OF LASER INTERFEROMETERS

7.1 INTRODUCTION

7.2 PHASE MEASUREMENT

7.3 FREQUENCY MEASUREMENT

7.4 AMPLITUDE MEASUREMENT

7.5 TIME-OF-FLIGHT MEASUREMENT

8 DESIGNS OF LASER INTERFEROMETERS

8.1 INTRODUCTION

8.2 BENCHTOP SYSTEMS

8.3 PORTABLE/HANDHELD SYSTEMS

8.4 IN-LINE/PROCESS SYSTEMS

8.5 MODULAR SYSTEMS

8.6 TIME-OF-FLIGHT SYSTEMS

9 LASER INTERFEROMETER MARKET, BY TYPE

9.1 INTRODUCTION

9.2 MICHELSON INTERFEROMETERS

9.2.1 ABILITY TO IMPROVE METROLOGY WITH ACCURATE CALIBRATION STANDARDS TO CONTRIBUTE TO SEGMENTAL GROWTH

9.3 FABRY-PEROT INTERFEROMETERS

9.3.1 VERSATILITY IN ADVANCED OPTICAL APPLICATIONS TO SEGMENTAL MARKET GROWTH

9.4 FIZEAU INTERFEROMETERS

9.4.1 RISING DEVELOPMENT TO ENABLE HIGH-PRECISION OPTICAL MEASUREMENTS AND ADDRESS VIBRATION CHALLENGES TO DRIVE MARKET

9.5 MACH-ZEHNDER INTERFEROMETERS

9.5.1 HIGH DEMAND FOR FIBER-OPTIC COMMUNICATION SYSTEMS AND ELECTRONIC DEVICES TO BOOST ADOPTION

9.6 SAGNAC INTERFEROMETERS

9.6.1 USE OF INERTIAL NAVIGATION SYSTEMS AND GYROSCOPES IN AIRCRAFT AND AUV MANUFACTURING TO FOSTER SEGMENTAL GROWTH

9.7 TWYMAN-GREEN INTERFEROMETERS

9.7.1 RAPID ADVANCEMENTS TO ENABLE FAST, VIBRATION-IMMUNE MEASUREMENTS TO AUGMENT SEGMENTAL GROWTH

10 LASER INTERFEROMETER MARKET, BY TECHNIQUE

10.1 INTRODUCTION

10.2 HOMODYNE

10.2.1 ABILITY TO MEASURE SMALL DISPLACEMENTS AND VIBRATIONS IN INDUSTRIAL APPLICATIONS TO DRIVE MARKET

10.3 HETERODYNE

10.3.1 RISING ADOPTION TO MEASURE HIGH-FREQUENCY VIBRATIONS TO FUEL MARKET GROWTH

11 LASER INTERFEROMETER MARKET, BY APPLICATION

11.1 INTRODUCTION

11.2 SURFACE TOPOLOGY

11.2.1 NEED TO UNDERSTAND SURFACE FEATURES AT MICROSCOPIC LEVEL TO BOOST SEGMENTAL GROWTH

11.3 ENGINEERING

11.3.1 REQUIREMENT FOR HIGH-PRECISION MEASUREMENTS IN QUALITY CONTROL, R&D, AND MANUFACTURING APPLICATIONS TO DRIVE MARKET

11.4 APPLIED SCIENCE

11.4.1 DEMAND FOR PRECISE, SENSITIVE, AND SPECIFIC MEASUREMENTS IN APPLIED SCIENCE FIELDS TO EXPEDITE SEGMENTAL GROWTH

11.5 BIOMEDICAL

11.5.1 EXTENSIVE USE IN IMAGING AND DIAGNOSTIC APPLICATIONS TO ACCELERATE SEGMENTAL GROWTH

11.6 SEMICONDUCTOR DETECTION

11.6.1 STRINGENT PRECISION AND QUALITY CONTROL REQUIREMENTS TO CONTRIBUTE TO SEGMENTAL GROWTH

12 LASER INTERFEROMETER MARKET, BY VERTICAL

12.1 INTRODUCTION

12.2 AUTOMOTIVE

12.2.1 FOCUS ON ENHANCING MANUFACTURING PRECISION TO BOOST SEGMENTAL GROWTH

12.3 AEROSPACE & DEFENSE

12.3.1 NEED TO ENSURE OPTIMAL PRECISION AND RELIABILITY OF SYSTEMS TO FUEL SEGMENTAL GROWTH

12.4 INDUSTRIAL

12.4.1 REQUIREMENT FOR ADVANCED VIBRATION AND DYNAMIC ANALYSIS OF MACHINERY TO FOSTER SEGMENTAL GROWTH

12.5 HEALTHCARE

12.5.1 HIGH EMPHASIS ON SAFETY AND EFFICACY OF MEDICAL DEVICES TO DRIVE MARKET

12.6 ELECTRONICS & SEMICONDUCTOR

12.6.1 INCREASING DEMAND FOR NANOSCALE DEVICES TO AUGMENT SEGMENTAL GROWTH

12.7 TELECOMMUNICATIONS

12.7.1 RISING NEED FOR FASTER AND RELIABLE DATA COMMUNICATION SERVICES TO CREATE LUCRATIVE GROWTH OPPORTUNITIES

13 LASER INTERFEROMETER MARKET, BY REGION

13.1 INTRODUCTION

13.2 NORTH AMERICA

13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

13.2.2 US

13.2.2.1 Rising adoption of high-precision engineering components to drive market

13.2.3 CANADA

13.2.3.1 Mounting demand for commercial vehicles to create lucrative market growth opportunities

13.2.4 MEXICO

13.2.4.1 Increasing investment in manufacturing sector to foster market growth

13.3 EUROPE

13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

13.3.2 UK

13.3.2.1 Booming automotive and aerospace industries to contribute to market growth

13.3.3 GERMANY

13.3.3.1 Prominent presence of automobile companies to spur demand

13.3.4 FRANCE

13.3.4.1 Rising deployment of Industry 4.0 and smart manufacturing techniques to support market growth

13.3.5 ITALY

13.3.5.1 Growing focus on precision measurement and industrial innovation to expedite market growth

13.3.6 REST OF EUROPE

13.4 ASIA PACIFIC

13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

13.4.2 CHINA

13.4.2.1 Rapid industrialization and urbanization to accelerate market growth

13.4.3 JAPAN

13.4.3.1 Rising implementation of just-in-time manufacturing approach to augment market growth

13.4.4 INDIA

13.4.4.1 Expanding industrial landscape to accelerate market growth

13.4.5 SOUTH KOREA

13.4.5.1 Rising semiconductor and electronics manufacturing to create market growth opportunities

13.4.6 REST OF ASIA PACIFIC

13.5 ROW

13.5.1 MACROECONOMIC OUTLOOK FOR ROW

13.5.2 MIDDLE EAST

13.5.2.1 Thriving aerospace sector to contribute to market growth

13.5.3 AFRICA

13.5.3.1 Growing focus on quality control in industrial sectors to boost market growth

13.5.4 SOUTH AMERICA

13.5.4.1 Steady rise of industrialization to foster market growth

14 COMPETITIVE LANDSCAPE

14.1 OVERVIEW

14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

14.3 REVENUE ANALYSIS, 2020-2024

14.4 MARKET SHARE ANALYSIS, 2024

14.5 COMPANY VALUATION AND FINANCIAL METRICS

14.6 PRODUCT COMPARISON

14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

14.7.1 STARS

14.7.2 EMERGING LEADERS

14.7.3 PERVASIVE PLAYERS

14.7.4 PARTICIPANTS

14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

14.7.5.1 Company footprint

14.7.5.2 Region footprint

14.7.5.3 Technique footprint

14.7.5.4 Vertical footprint

14.7.5.5 Application footprint

14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024