Endoscopy Equipment Market by Product (Endoscopes (Flexible, Rigid, Robot-assisted, Capsule), Visualization Systems, Accessories, Others), Application (Laparoscopy, Cystoscopy), End User (Hospitals, ASCs, Clinics), and Region - Global Forecast to 2030

상품코드:1829983

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 593 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

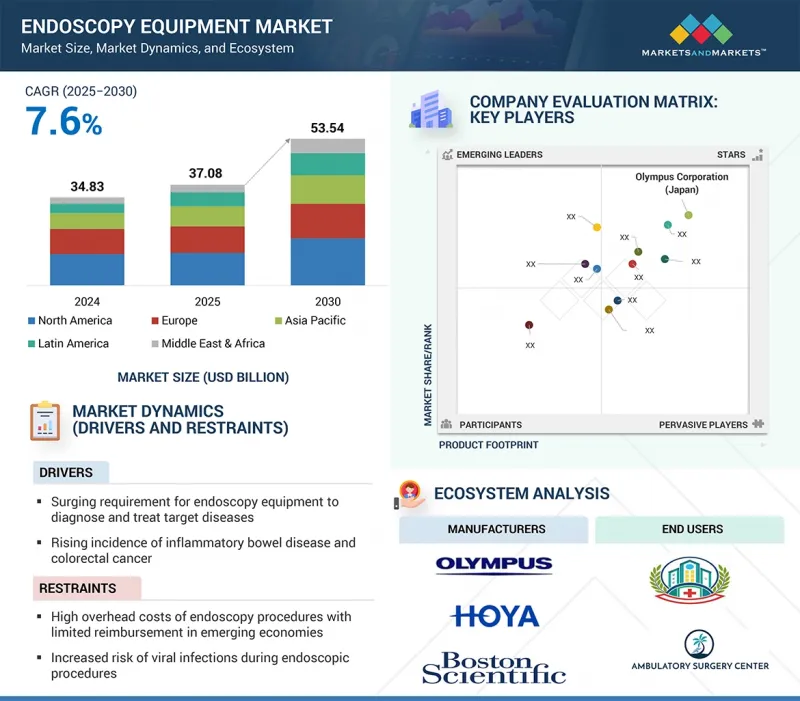

세계의 내시경 장비 시장 규모는 2025년 370억 8,000만 달러에서 2030년까지 535억 4,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 7.6%의 성장이 전망됩니다.

시장 성장은 대장암, 염증성 장질환과 같은 대상 질환을 진단하고 관리하는 내시경 수술에 대한 수요 증가에 의해 촉진될 것입니다. 시장 기회는 감염 관리 문제를 해결하는 데 도움이 되는 일회용 내시경의 채택 확대에서 비롯됩니다. 또한, 신흥 경제권의 의료 인프라의 급속한 확장은 아직 개발되지 않은 잠재력을 보여주고 있습니다. 이들 지역에서는 투자가 증가하고, 의료 접근성이 개선되고, 환자 치료의 표준이 발전하고 있습니다.

조사 범위

조사 대상 연도

2023-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러/10억 달러

부문

제품, 용도, 최종사용자, 지역

대상 지역

북미, 아시아태평양, 라틴아메리카, 중동 및 아프리카

그러나 높은 기기 비용, 재처리와 무관한 교차 오염의 위험, 대체 진단 기술의 가용성 등이 시장 성장을 저해하고 있습니다. 또한, 일부 지역에서는 숙련된 전문가 부족과 규제 문제로 인해 더 넓은 시장으로 침투하는 데 어려움을 겪고 있습니다.

"연성 내시경 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

제품별로 내시경 장비 시장은 내시경, 시각화 시스템, 기타 내시경 장비, 액세서리로 구분됩니다. 내시경 부문은 다시 연성 내시경, 경성 내시경, 로봇 보조 내시경, 캡슐 내시경으로 구분됩니다. 이 중 연성 내시경은 적용 범위가 넓고 조작성이 뛰어나며 저침습적 진단 및 치료 수술에 선호되어 2024년 가장 큰 시장 점유율을 차지했습니다. 이러한 우위는 예측 기간 동안 지속될 것으로 예측됩니다.

연성 내시경은 소화기, 폐, 비뇨기, 부인과 등의 분야에서 널리 사용되고 있으며, 경성 내시경에 비해 환자의 편안함과 복잡한 해부학적 구조에 대한 접근성을 제공합니다. 높은 정확도와 고해상도 영상을 제공할 수 있어 질병의 조기 발견과 효과적인 치료가 가능하여 의료진들 사이에서 채택이 확대되고 있습니다. 전 세계적으로 소화기 질환의 부담 증가, 암 검진 프로그램, 외래 내시경 수술에 대한 선호도 증가로 인해 수요가 더욱 증가하고 있습니다. 또한, 일회용 및 일회용 연성 내시경과 같은 지속적인 기술 혁신은 교차 오염 및 재처리 비용에 대한 우려를 해결하고 병원 및 외래수술센터(ASC)에 매우 매력적으로 다가오고 있습니다. 이러한 요인으로 인해 연성 내시경은 내시경 장비 시장에서 가장 지배적인 부문이 되었습니다.

"복강경 부문은 예측 기간 동안 두 번째로 큰 시장을 차지할 것으로 예측됩니다. "

복강경 검사 부문은 2024년 시장 점유율 2위를 차지할 것으로 예상되며, 예측 기간 동안에도 선두를 차지할 것으로 예측됩니다. 이는 여러 치료 분야에서 선호되는 수술적 접근법으로 널리 채택되고 있기 때문입니다. 예를 들어, National Library of Medicine(2023년 10월)에 따르면 복강경 수술은 기존 개복 수술에 비해 수술 시간 단축, 출혈량 감소, 빠른 회복, 입원 기간 단축 등 통계적으로 유의미한 이점을 보여 환자와 의료진에게 매우 유리합니다.

비만의 급속한 증가는 복강경 비만 치료에 대한 수요를 더욱 가속화하고 있습니다. 흉터 감소와 빠른 회복에 대한 환자들의 선호도가 높아지면서 이 부문의 성장세가 지속되고 있으며, 내시경 장비 시장에서 두 번째로 큰 기여를 하고 있습니다.

"아시아태평양이 가장 빠르게 성장하고 북미가 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예상했습니다. "

세계 내시경 장비 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카의 5개 주요 지역으로 분류됩니다. 이 중 아시아태평양은 의료 인프라의 발달, 의료비 증가, 중국 및 인도의 질병 조기 발견에 대한 인식 증가로 인해 가장 빠른 성장이 예상되고 있습니다. 이들 국가들은 특히 암, 심혈관 질환 등 만성질환 환자 증가를 관리하기 위해 진단 및 수술 능력 강화에 많은 투자를 하고 있습니다. 일본에서는 전국민 의료보험제도로 의료제도가 발달하여 선진화된 내시경 수술에 대한 폭넓은 접근성이 확보되어 있습니다. 또한, 의료관광 증가, 정부의 적극적인 노력, 저침습적 기술의 채택 증가 등이 시장 침투를 가속화하고 있으며, 아시아태평양은 세계 내시경 장비 시장에서 고성장 지역으로 부상하고 있습니다.

세계의 내시경 장비 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

내시경 장비 시장 개요

북미 내시경 장비 시장 : 최종사용자별, 국가별

지역 구성 : 내시경 장비 시장

지역 구성 : 내시경 장비 시장(2025년-2030년)

내시경 장비 시장 : 신흥 국가 시장 vs. 선진국 시장(2025년·2030년)

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

산업 동향

AI와 영상 유도 솔루션

디지털 플랫폼과 접속성 통합

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 결정 분석

평균 판매 가격 동향 : 주요 기업별

평균 판매 가격 동향 : 지역별

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

무역 분석

HS코드 901890 수입 데이터

HS코드 901890 수출 데이터

주요 컨퍼런스 및 이벤트(2025년-2026년)

사례 연구 분석

규제 상황

규제 분석

규제기관, 정부기관 및 기타 조직

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

인접 시장 분석

미충족 요구

내시경 장비 시장에 대한 AI의 영향

서론

내시경 장비 에코시스템에서의 AI 시장 잠재력

AI 이용 사례

AI를 도입하고 있는 주요 기업

내시경 장비 시장에서 생성형 AI의 전망

2025년 미국 관세의 영향

서론

주요 관세율

가격 영향 분석

지역에 대한 영향

최종 이용 산업에 대한 영향

제6장 내시경 장비 시장 : 유형별

서론

시각화 시스템

내시경

기타 내시경 장비

액세서리

제7장 내시경 장비 시장 : 용도별

서론

소화관 내시경

복강경

비뇨과 내시경(방광경 검사)

관절경 검사

산부인과 내시경

기관지경

이비인후과 내시경

종격경

기타 용도

제8장 내시경 장비 시장 : 최종사용자별

서론

병원

외래수술센터(ASC)

진료소

기타 최종사용자

제9장 내시경 장비 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

호주

한국

기타 아시아태평양

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타 중동 및 아프리카

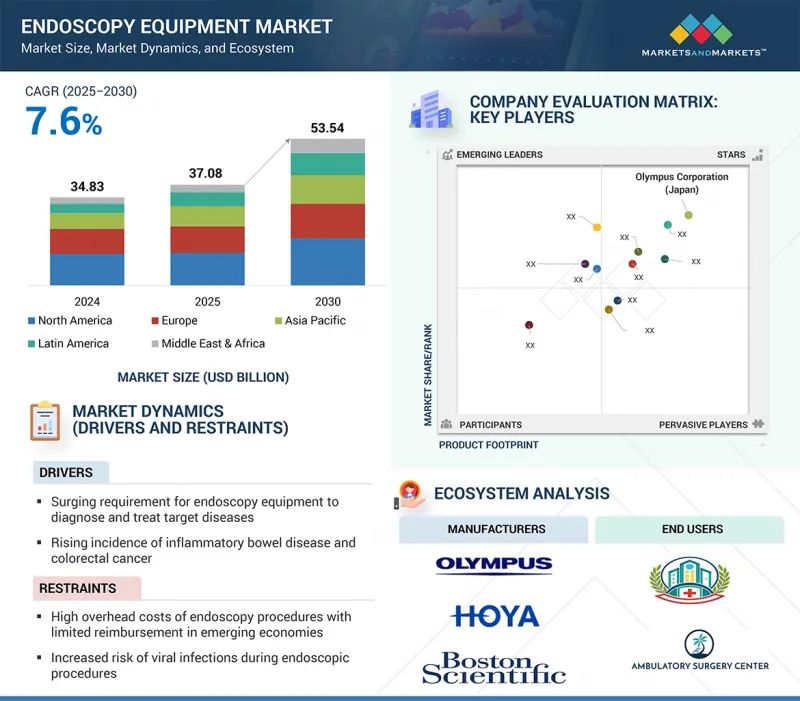

제10장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

매출 분석(2020년-2024년)

시장 점유율 분석(2024년)

기업 평가와 재무 지표

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제11장 기업 개요

주요 기업

OLYMPUS CORPORATION

KARL STORZ SE & CO. KG

BOSTON SCIENTIFIC CORPORATION

STRYKER

FUJIFILM CORPORATION

JOHNSON & JOHNSON

MEDTRONIC

HOYA CORPORATION

NIPRO

SMITH+NEPHEW

STERIS

AMBU A/S

RICHARD WOLF GMBH

INTUITIVE SURGICAL OPERATIONS, INC.

B. BRAUN SE

기타 기업

HOLOGIC, INC.

CONMED CORPORATION

TELEFLEX INCORPORATED

SONOSCAPE MEDICAL CORP.

ENDOMED SYSTEMS GMBH

HUNAN VATHIN MEDICAL INSTRUMENT CO., LTD.

CAPSOVISION, INC.

ATMOS MEDIZINTECHNIK GMBH & CO. KG

LABORIE

ZHUHAI PUSEN MEDICAL TECHNOLOGY CO., LTD.

제12장 부록

LSH

영문 목차

영문목차

The global endoscopy equipment market is projected to grow from USD 37.08 billion in 2025 to USD 53.54 billion by 2030, at a CAGR of 7.6% during the forecast period. The growth of the endoscopy equipment market is driven by the rising demand for endoscopic procedures to diagnose and manage target conditions such as colorectal cancer and inflammatory bowel diseases, fueled by increasing disease prevalence and the need for early, minimally invasive interventions. Market opportunities are emerging from the growing adoption of single-use endoscopes, which help address infection control concerns. Additionally, the rapid expansion of healthcare infrastructure in emerging economies presents untapped potential. These regions are experiencing increased investments, improved access to healthcare, and evolving standards of patient care.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

Product, Application, End User, and Region

Regions covered

Europe, North America, Asia Pacific, Latin America, Middle East, and Africa

However, market growth is restrained by high device costs, risk of cross-contamination despite reprocessing, and the availability of alternative diagnostic techniques. Additionally, a lack of skilled professionals and regulatory challenges in some regions hamper broader market penetration.

"Flexible endoscopes segment is expected to hold the largest market share during the forecast period"

Based on product, the endoscopy equipment market is segmented into endoscopes, visualization systems, other endoscopy equipment, and accessories. The endoscopes segment is further bifurcated into flexible endoscopes, rigid endoscopes, robot-assisted endoscopes, and capsule endoscopes. Among these in 2024, the flexible endoscopes segment accounted for the largest market share, due to their broad applicability, superior maneuverability, and preference in minimally invasive diagnostic and therapeutic procedures. This dominance is projected to continue during the forecast period.

Flexible endoscopes are widely used across gastrointestinal, pulmonary, urological, and gynecological applications, offering enhanced patient comfort and access to complex anatomical structures compared to rigid alternatives. Their ability to provide high-resolution imaging with greater precision supports early disease detection and effective treatment, driving higher adoption among healthcare providers. The rising global burden of gastrointestinal disorders, cancer screening programs, and the growing preference for outpatient endoscopic procedures further strengthen demand. Additionally, ongoing innovations such as disposable and single-use flexible endoscopes address concerns around cross-contamination and reprocessing costs, making them highly attractive to hospitals and ambulatory surgery centers. These factors collectively position flexible endoscopes as the most dominant segment in the endoscopy equipment market.

"Laparoscopy segment is projected to hold the second-largest market during the forecast period"

The laparoscopy segment accounted for the second largest share of the market in 2024 and is expected to lead during the forecast period. This is due to its widespread adoption as the preferred surgical approach across multiple therapeutic areas. For instance, according to the National Library of Medicine (October 2023), laparoscopic procedures demonstrate statistically significant advantages over traditional open surgeries, including shorter operative times, reduced blood loss, quicker recovery, and shorter hospital stays, making them highly favorable for patients and healthcare providers.

The rapid rise in obesity prevalence has further accelerated demand for laparoscopic bariatric procedures, as they ensure long-term survival and deliver substantial metabolic benefits. The increasing patient preference for reduced scarring and faster recovery continues to fuel this segment's growth, securing its strong position as the second-largest contributor within the endoscopy equipment market.

"Asia Pacific region is expected to grow at the fastest rate, while North America is projected to hold the largest share during the forecast period"

The global endoscopy equipment market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Among these, the Asia Pacific region is expected to grow at the fastest rate due to the healthcare infrastructure development, increasing healthcare expenditure, and rising awareness of early disease detection across China and India. These countries are investing heavily to enhance diagnostic and surgical capabilities, particularly to manage rising cases of chronic diseases such as cancer and cardiovascular disorders. Japan's well-established healthcare system with universal insurance coverage ensures wide accessibility to advanced endoscopic procedures. Moreover, increasing medical tourism, favorable government initiatives, and the rising adoption of minimally invasive technologies are accelerating market penetration, making Asia Pacific a high-growth region in the global endoscopy equipment market.

The North American endoscopy equipment market is primarily dominated by the US, driven by favorable reimbursement policies, advanced healthcare infrastructure, and high disease prevalence. Robust coverage for endoscopic procedures under Medicare and private insurance significantly reduces patient out-of-pocket costs, leading to increased adoption of endoscopy equipment in hospitals and outpatient settings.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

By Designation: C-level - 50%, Director level - 30%, and Others - 20%

By Region: North America - 30%, Europe - 25%, Asia Pacific - 20%, Latin America - 15%, and Middle East & Africa - 10%.

The players operating in the endoscopy equipment market include Olympus Corporation (Japan), Karl Storz SE & CO. Kg (Germany), Boston Scietific Corporation (US), FUJIFILM Corporation (Japan), HOYA Corporation (Japan), Stryker (US), Medtronic (Ireland), Smith+Nephew (UK), Johnson & Johnson (US), Nipro (Japan), Steris (US), B Braun SE (Germany), Conmed Corporation (US), Ambu A/S (Denmark), Cook Medical (US), Hologic Inc. (US), EndoMed Systems GmbH (Germany), Richard Wolf GmbH. (Germany), CapsoVision, Inc. (US), Teleflex Incorporated (US), Laborie (US), Arthrex, Inc. (US), Dantschke Medizintechnik GMBH & Co. KG (Germany), The Cooper Companies, Inc. (US), and SonoScape Medical Corp (China).

Research Coverage

This report studies the endoscopy equipment market based on type, application, end user, and region. The report also studies factors (such as drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets concerning their individual growth trends and forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them gain a larger market share. Firms purchasing the report could use one or a combination of the strategies mentioned below to strengthen their market presence.

This report provides insights into the following pointers.

Analysis of key drivers (The increasing requirement for endoscopy to diagnose and treat target diseases, Surging incidence of inflammatory bowel diseases and colorectal cancer, Rising focus of medical specialists to shift from manual to automated endoscopy reprocessing), restraints (High overhead costs of endoscopy procedures with limited reimbursement in emerging economies, Increasing risk of getting infections during endoscopic procedures), opportunities (Rapidly developing healthcare sector in emerging economies, Increasing adoption of single-use endoscopes), challenges (Increasing number of product recalls, Lack of proper sterilization and reprocessing, Shortage of trained physicians and endoscopists)

Market Penetration: Complete knowledge of the spectrum of products presented by the major companies in the endoscopy equipment market

Product Development/Innovation: Comprehensive understanding of the forthcoming trends, research and development initiatives, and product launches within the endoscopy equipment market

Market Development: Complete knowledge about profitable developing regions

Market Diversification: Exhaustive knowledge of new goods, expanding geographies, and current changes in the endoscopy equipment industry help to diversify the market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Olympus Corporation (Japan), Karl Storz SE & CO. Kg (Germany), Boston (US), FUJIFILM Corporation (Japan), HOYA Corporation (Japan), Stryker (US), and Ambu A/S (Denmark)