차량 전동화 시장(-2032년) : 제품 유형(start stop, EPS, EHPS, 액체 히터 PTC, 전동 에어컨 압축기, 전동 진공 펌프, 전동 오일펌프, 전동 워터 펌프, ISG), 추진 구분, DOH, 차량 유형, 지역별

Vehicle Electrification Market by Product Type (Start-Stop, EPS, EHPS, Liquid Heater PTC, Electric A/C Compressor, Electric Vacuum Pump, Electric Oil Pump, Electric Water Pump, ISG), Propulsion, DOH, Vehicle Type, and Region - Global Forecast to 2032

상품코드:1826560

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 303 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

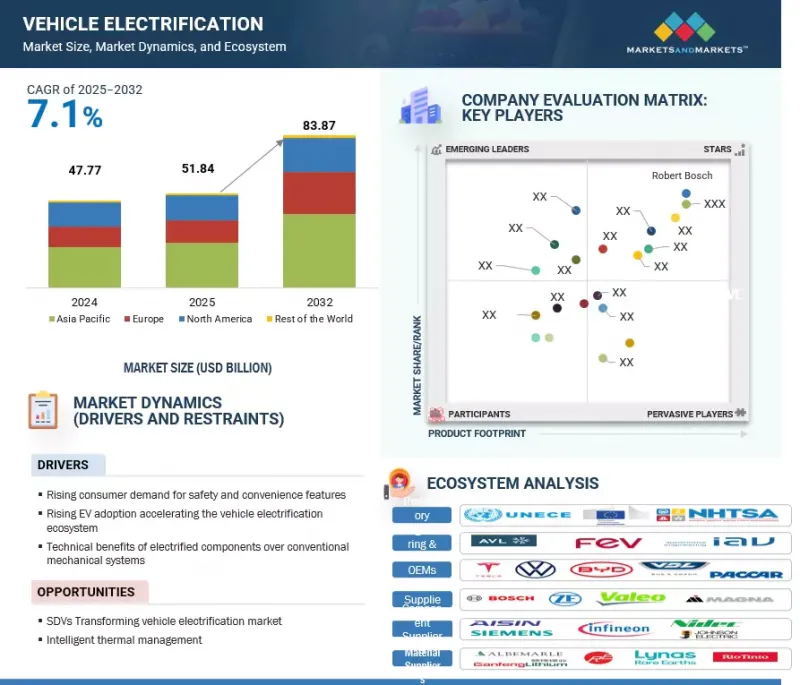

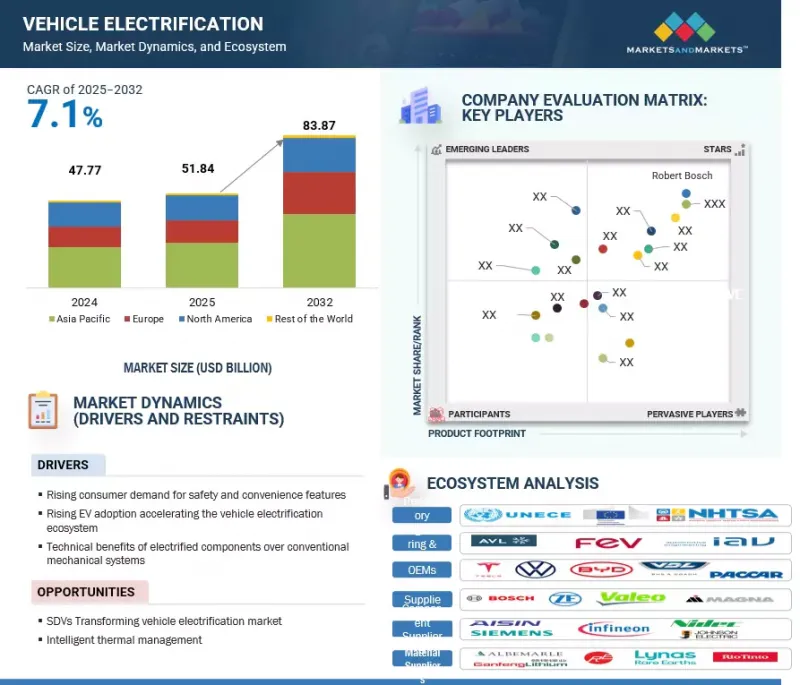

차량 전동화 시장 규모는 2025년 569억 4,000만 달러에서 CAGR 7.0%로 성장을 지속하여, 2032년에는 913억 달러로 성장할 것으로 예측됩니다.

OEM은 엄격한 배출가스 규제를 충족하고 모든 차량 유형에서 연비를 개선하기 위해 기존 시스템에서 스타트-스톱 시스템, 전기 오일 펌프, 전기 진공 펌프와 같은 고급 전동화 구성품으로 전환하여 시장을 주도하고 있습니다.

조사 범위

조사 대상 연도

2025-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

금액(달러)

부문

제품 유형, 추진 구분, DOH, 차량 유형, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

예를 들어, Cummins는 최근 스톱 스타트, 중립 공회전, 자동 엔진 정지 등의 공회전 저감 기술을 도입하여 차량용 ICE 파워트레인에서 최대 17%의 연비 개선을 실현할 수 있다고 밝혔습니다. 부품 공급업체들도 기계식에 비해 기생 손실을 줄이는 에너지 절약형 전기 오일 펌프와 전기 진공 펌프를 홍보하고 있습니다. 그러나 전기자동차의 고비용은 여전히 제약요인으로 작용하고 있으며, 특히 인도나 남아시아 국가와 같이 가격에 민감한 시장에서는 이러한 첨단 시스템을 통합할 때 성능 향상과 경제성의 균형을 맞출 필요가 있습니다.

"하이브리드 수준별로는 ICE&마이크로하이브리드 차량이 예측 기간 동안 가장 큰 부문을 차지할 것으로 예측됩니다."

이는 주로 일반 승용차로의 폭넓은 도입과 기존 자동차 인프라와의 호환성 때문입니다. 마이크로 하이브리드는 일반적으로 스타트-스톱 시스템 및 전기 파워 스티어링(EPS)을 통합하는 것이 일반적이며, 특히 아시아태평양 및 북미와 같이 비용에 민감하고 시장 규모가 큰 지역에서는 표준 장비로 채택되고 있습니다. EPS는 ICE 및 마이크로 하이브리드 차량 플랫폼에서 채택이 확대되고 있으며, 엔진 부하를 줄이고 에너지 효율을 높이며, 첨단 운전 보조 시스템을 지원합니다. 또한, 전기 진공 펌프, 전기 A/C 컴프레서, 냉각수 펌프와 같은 전기 보조 기계가 48V 마일드 하이브리드 아키텍처 내에서 차량 효율을 더욱 향상시킵니다. 또한, 새로운 차량에 ISG 기술의 통합 확대로 인한 동적 에너지 관리는 2032년까지 ICE 및 마이크로하이브리드 차량의 전기화에서 유망한 성장 기회를 제공할 것으로 예측됩니다.

"지역별로는 유럽이 2025년 두 번째로 큰 시장이 될 전망"

유럽은 주요 경제권 정부의 대규모 인센티브와 산업계의 강력한 노력으로 2025년 차량 전동화 시장에서 2위를 차지할 것으로 예측됩니다. 이 지역의 전동화 상황은 ICE에서 HEV, PHEV, BEV에 이르기까지 모든 추진 차량을 포괄하는 다각화된 포트폴리오로 특징지어집니다. 유럽 최대 자동차 거점인 독일은 BEV 판매가 2025년 초에 15만 8,000대를 넘어서는 등 급격한 성장세를 보이고 있으며, Volkswagen과 BMW 등 OEM들이 전동화 플랫폼과 파워트레인 아키텍처를 적극적으로 추진하고 있습니다. 프랑스와 영국도 강력한 정책적 지원과 OEM의 전동화 로드맵을 통해 시장 성장을 가속하고 있으며, 영국의 Vehicle Emissions Trading Scheme은 2024년 전기차 판매 점유율 약 30%를 달성하는 데 기여했습니다.

또한, 유럽의 첨단 충전 인프라는 2025년 1분기 기준 100만 개 이상의 공공 충전소를 보유하고 있어 BEV와 PHEV의 보급을 뒷받침하고 있습니다. Continental, Bosch, Denso와 같은 주요 공급업체들은 유럽 시장의 규제 요건을 충족하는 전동화 부품을 개발하고 있습니다. 마일드 하이브리드는 여전히 중요한 전환 기술이며, ICE 플랫폼의 연비 효율과 배기가스 배출 성능을 향상시키고 있으며, 전기 워터 펌프와 전기 오일 펌프 시스템의 혁신으로 뒷받침되고 있습니다. 스페인, 이탈리아 등에서도 하이브리드 채택이 확대되고 있으며, 배터리 기술 향상과 인센티브가 PHEV 및 HEV 부문을 강화하고 있습니다. 인프라, OEM, 공급업체, 규제 프레임워크의 종합적인 지원으로 유럽은 예측 기간 동안 ICE/마일드 하이브리드에서 완전 전기차를 아우르는 지속적인 차량 전동화 성장에 유리한 위치에 있습니다.

세계의 차량 전동화(Vehicle Electrification) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

제6장 업계 동향

공급망 분석

생태계 분석

가격 분석

무역 분석

고객 사업에 영향을 미치는 동향/혼란

2025-2026년 주요 컨퍼런스 및 이벤트

사례 연구 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

차량 하이브리드화 단계 개요

플랫폼 모듈화와 표준화 동향

전기자동차 승용차 제조업체 주요 10개사의 전동 쿨란트 펌프 소비량

상용차 OEM 주요 10개사의 전동 쿨란트 펌프 소비량

주요 10개 공급업체의 가격 분석

주요 10 OEM의 가격 분석

전동 쿨란트 펌프 : 누가 누구에게 공급하는가?

전동 쿨란트 펌프 : 공급업체 계약

규제 상황

주요 이해관계자와 구입 기준

제7장 차량 전동화 시장 : 추진 구분, 제품별

start stop 시스템

전동 파워스티어링

전동 유압 파워스티어링

액체 히터 PTC

전동 에어컨 압축기

전동 진공 펌프

전동 오일 펌프

전동 워터 펌프

통합 스타터 제네레이터

주요 인사이트

제8장 차량 전동화 시장 : 차량 유형

승용차

소형 상용차

트럭

버스

주요 인사이트

제9장 차량 전동화 시장 : 하이브리드 레벨별

ICE&마이크로 하이브리드 자동차

하이브리드 자동차

PHEV

전기자동차

주요 인사이트

제10장 차량 전동화 시장 : 지역별

아시아태평양

거시경제 전망

중국

일본

인도

한국

기타

북미

거시경제 전망

미국

캐나다

멕시코

유럽

거시경제 전망

독일

네덜란드

프랑스

영국

스페인

이탈리아

기타

세계 기타 지역

거시경제 전망

브라질

남아프리카공화국

기타

제11장 경쟁 구도

주요 시장 진출기업의 전략/강점

전동 쿨란트 펌프 : 시장 점유율 분석

전동 압축기 : 시장 점유율 분석

E엑슬 : 시장 점유율 분석

매출 분석

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 신규 기업/중소기업

기업 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오

제12장 기업 개요

주요 기업

ROBERT BOSCH GMBH

CONTINENTAL AG

APTIV

DENSO CORPORATION

MITSUBISHI MOTORS CORPORATION

BORGWARNER INC.

JOHNSON ELECTRIC HOLDINGS LIMITED

MAGNA INTERNATIONAL INC.

AISIN CORPORATION

NIDEC CORPORATION

PANASONIC AUTOMOTIVE SYSTEMS CO., LTD.

기타 기업

JTEKT CORPORATION

ASTEMO, LTD.

ZF FRIEDRICHSHAFEN AG

VALEO

GKN AUTOMOTIVE LTD.

SCHAEFFLER AG

MAHLE GMBH

DANA LIMITED

BROSE FAHRZEUGTEILE SE & CO. KG

KEB AUTOMATION

TECO CORPORATION

YASA LIMITED

제13장 제안

아시아태평양이 차량 전동화 주요 시장이 된다

스티어링 시스템이 차량 전동화 주요 추진 요인으로서 부상

승용차가 세계에 보급

결론

제14장 부록

LSH

영문 목차

영문목차

The vehicle electrification market is projected to grow from USD 56.94 billion in 2025 to USD 91.30 billion by 2032 at a CAGR of 7.0%. OEMs continue transitioning from conventional systems to advanced electrified components such as start-stop systems, electric oil pumps, and electric vacuum pumps to meet strict emissions regulations and enhance fuel efficiency across all vehicle types, driving the market.

Scope of the Report

Years Considered for the Study

2025-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Million/Billion)

Segments

Product Type, Propulsion, DOH, Vehicle Type, and Region

Regions covered

North America, Europe, Asia Pacific, and RoW

For instance, Cummins recently highlighted idle reduction technologies, including stop-start, neutral idle, and automatic engine shutdown, capable of delivering up to 17% fuel-economy improvements in ICE powertrains for fleet applications. Component suppliers are also promoting energy-efficient electric oil and vacuum pumps that reduce parasitic loads compared to mechanical counterparts. Still, the higher cost of electric vehicles remains a constraint, especially for price-sensitive markets such as India and South Asia countries, where integration of these advanced systems must balance performance gains with affordability.

"By degree of hybridization, the ICE & micro hybrid vehicle is projected to be the largest segment during the forecast period."

The ICE & micro hybrid vehicle segment accounts for the largest share within the global vehicle electrification market by degree of hybridization, primarily due to their wide deployment in mainstream passenger cars and their compatibility with existing automotive infrastructure. Micro hybrids, which commonly integrate start-stop systems and electric power steering (EPS), have become standard equipment, especially in cost-sensitive and high-volume markets across the Asia Pacific and North America. Electric power steering is being increasingly adopted in ICE and micro-hybrid platforms. It helps reduce engine loads, enhance energy efficiency, and support advanced driver assistance systems. Additionally, electrified auxiliaries such as electric vacuum pumps, electric A/C compressors, and coolant pumps, among others, within the 48 V mild-hybrid architecture would further enhance vehicle efficiency. Alternatively, rising integration of ISG technology in newer models for dynamic energy management would present a lucrative growth opportunity in the ICE & micro-hybrid vehicle electrification by 2032.

"The electric coolant pump segment is projected to be among the fastest-growing propulsion segments throughout the forecast period."

The electric coolant pump segment is emerging with a significant growth component across 48 V mild-hybrid, HEV, PHEV, and BEV architectures, addressing thermal precision needs in these vehicles. Unlike mechanically driven variants, electric coolant pumps offer precise, variable control over coolant flow, enabling efficient and targeted heat dissipation for power electronics, batteries, and turbocharged engines. Their integration is especially pronounced in 48V architectures, where it supports the efficient operation of auxiliary systems without relying on the engine. The shift to 48V electrical systems is enabling more advanced auxiliary electrification, such as electric coolant pumps that provide precise, on-demand cooling. This improves vehicle efficiency, helps control emissions, and allows for smaller, more efficient cooling systems, which are especially important as car makers move toward fully electric vehicles. 12V electric coolant pump leads the global installation rate owing to its higher installation base in electric & hybrid light-duty vehicles, as these vehicles have lower voltage and power requirements and are usually fitted with a 12V electrical system for main and auxiliary applications such as batteries, inverters, power electronics, lighting, and others. Further, these pumps with a wattage range of <150 W are typically used in smaller vehicles or auxiliary cooling systems where lower power consumption and flow rates are sufficient. Recent OEM and supplier developments have accelerated this trend. For instance, in 2024, Rheinmetall secured a substantial order of electric coolant pumps for several million units, rated between 50 watts and 2000 watts, for hybrid vehicle production through 2030, with service support extending to 2045, demonstrating supplier confidence in long-term demand. Additionally, in India, Concentric AB won a ~USD 6.6 million (70 MSEK) contract to supply its electric coolant pump for a new battery electric bus platform, with production scheduled to begin in late 2025. With stricter emissions rules, the growing popularity of fast-charging electric cars, and more requirements for mild hybrids, electric coolant pumps are becoming a key part of automakers' plans for vehicle electrification during the forecasted period.

"Europe is projected to be the second-largest market for vehicle electrification in 2025."

Europe is projected to be the second-largest market for vehicle electrification, driven by significant government incentives and robust industry engagement across its leading economies. The region's electrification landscape is characterized by a diversified portfolio encompassing all propulsion vehicles from ICE to HEVs to PHEVs and BEVs. Germany, as Europe's largest automotive hub, leads with rapid growth in BEV sales, surpassing ~158 thousand units in early 2025, supported strongly by OEMs like Volkswagen and BMW advancing electrified platforms and powertrain architectures. France and the UK similarly support the market's growth with strong policy support and OEM electrification roadmaps, with the UK's Vehicle Emissions Trading Scheme facilitating a near 30% EV sales share in 2024. Moreover, Europe's advanced charging infrastructure, with over 1 million public points by Q1 2025, supports BEV and PHEV adoption. Key suppliers, including Continental, Bosch, and Denso, are developing electrified components such as electric oil pumps, integrated inverters, and battery thermal management systems tailored for Europe's regulatory and market needs. Mild hybrids remain significant transitional technologies that enhance fuel efficiency and emissions performance on ICE platforms, supported by innovations in electric water pumps and electric oil pump systems. Growth in hybrid adoption is seen in countries like Spain and Italy, while improved battery technologies and incentives strengthen PHEV and HEV segments. Combined support from infrastructure, OEMs, suppliers, and regulatory frameworks positions Europe for sustained vehicle electrification growth, covering both electrified ICE/mild hybrids and full electric vehicles over the forecasted period.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in this market.

Here is the breakdown of the interviews conducted:

By Company Type: Supplier - 60%, OEMs - 20%, Tier I - 20%

By Designation: D Level - 30%, C Level - 60%, and Others - 10%

By Region: North America - 15%, Europe - 45%, Asia Pacific - 30%, RoW - 10%

The key players in the vehicle electrification market are Robert Bosch GmbH (Germany), Continental AG (Germany), Denso Corporation (Japan), BorgWarner Inc. (US), and Aptiv (Ireland). Major companies' key strategies to maintain their position in the global vehicle electrification market are strong global networking, mergers and acquisitions, partnerships, and technological advancements.

Key Benefits of Buying the Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the vehicle electrification market and the sub-segments. The report also discusses ups and downs in vehicle electrification, allowing component suppliers to plan their strategies. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report further provides insights into the following points:

Market Dynamics: Analysis of key drivers (rising consumer demand for safety and convenience features, rising EV adoption accelerating the vehicle electrification ecosystem and technical benefits of electrified components over conventional mechanical systems), restraints (high cost of electric components), opportunities (SDVs transforming the vehicle electrification market, intelligent thermal management), and challenges (integration with ICE platforms) influencing the growth of the vehicle electrification market

Product Development/Innovation: Detailed insights into upcoming technologies and product & service launches in the vehicle electrification market

Market Development: Comprehensive market information (the report analyzes the authentication and brand protection market across varied regions)

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the vehicle electrification market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Robert Bosch GmbH (Germany), Continental AG (Germany), Denso Corporation (Japan), BorgWarner Inc. (US), and Aptiv (Ireland) in the vehicle electrification market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Secondary sources for vehicle production

2.1.1.2 Secondary sources for market sizing

2.1.1.3 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary interview participants

2.1.2.2 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.3 DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN VEHICLE ELECTRIFICATION MARKET

4.2 VEHICLE ELECTRIFICATION MARKET, BY VEHICLE TYPE

4.3 VEHICLE ELECTRIFICATION MARKET, BY DEGREE OF HYBRIDIZATION

4.4 VEHICLE ELECTRIFICATION MARKET, BY PROPULSION AND PRODUCT

4.5 VEHICLE ELECTRIFICATION MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Elevated consumer demand for safety and convenience features

5.2.1.2 Rise in global adoption of EVs

5.2.1.3 Technical benefits of electrified components over mechanical systems

5.2.2 RESTRAINTS

5.2.2.1 High cost of electric components

5.2.3 OPPORTUNITIES

5.2.3.1 Shift toward software-defined vehicles

5.2.3.2 Need for intelligent thermal management

5.2.4 CHALLENGES

5.2.4.1 Complex integration with ICE platforms

6 INDUSTRY TRENDS

6.1 SUPPLY CHAIN ANALYSIS

6.2 ECOSYSTEM ANALYSIS

6.3 PRICING ANALYSIS

6.3.1 AVERAGE SELLING PRICE, BY PRODUCT

6.3.2 AVERAGE SELLING PRICE, BY REGION

6.4 TRADE ANALYSIS

6.4.1 IMPORT SCENARIO (841330)

6.4.2 EXPORT SCENARIO (841330)

6.5 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.6 KEY CONFERENCES AND EVENTS, 2025-2026

6.7 CASE STUDY ANALYSIS

6.7.1 IMPLEMENTATION OF START-STOP SYSTEMS IN DIESEL VEHICLES

6.7.2 SHIFT TOWARD ELECTRIC POWER STEERING

6.7.3 DEVELOPMENT OF ADVANCED HIGH-VOLTAGE COMPONENTS

6.8 INVESTMENT AND FUNDING SCENARIO

6.9 TECHNOLOGY ANALYSIS

6.9.1 KEY TECHNOLOGIES

6.9.1.1 High-voltage integrated e-axle systems

6.9.1.2 Advanced ECUs and software-defined components

6.9.2 COMPLEMENTARY TECHNOLOGIES

6.9.2.1 Electric coolant pumps by non-sealed materials

6.9.2.1.1 Shaft materials

6.9.2.1.2 Bearing materials

6.9.3 ADJACENT TECHNOLOGIES

6.9.3.1 Connectivity & IoT-enabled components

6.10 PATENT ANALYSIS

6.11 OVERVIEW OF VEHICLE HYBRIDIZATION STAGES

6.11.1 MICRO HYBRID

6.11.2 MILD HYBRID

6.11.3 FULL HYBRID

6.11.4 PHEV/RANGE-EXTENDED EV (REEV)

6.11.5 BEV/EXTENDED-RANGE EV (EREV)

6.12 PLATFORM MODULARIZATION AND STANDARDIZATION TRENDS

6.13 ELECTRIC COOLANT PUMP CONSUMPTION BY TOP 10 ELECTRIC PASSENGER CAR OEMS

6.14 ELECTRIC COOLANT PUMP CONSUMPTION BY TOP 10 COMMERCIAL VEHICLE OEMS

6.15 TOP 10 SUPPLIER PRICING ANALYSIS

6.16 TOP 10 OEM PRICING ANALYSIS

6.17 ELECTRIC COOLANT PUMP: WHO SUPPLIES TO WHOM

6.18 ELECTRIC COOLANT PUMP: SUPPLIER CONTRACTS

6.19 REGULATORY LANDSCAPE

6.19.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.19.2 EV INCENTIVES, BY COUNTRY

6.19.2.1 Netherlands

6.19.2.2 Germany

6.19.2.3 France

6.19.2.4 UK

6.19.2.5 China

6.19.2.6 US

6.19.3 COMPONENT-LEVEL CARBON FOOTPRINT ANALYSIS

6.20 KEY STAKEHOLDERS AND BUYING CRITERIA

6.20.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.20.2 KEY BUYING CRITERIA

7 VEHICLE ELECTRIFICATION MARKET, BY PROPULSION AND PRODUCT

7.1 INTRODUCTION

7.2 START-STOP SYSTEM

7.2.1 RAPID ADOPTION OF MILD-HYBRID VEHICLES AND FOCUS ON BATTERY LONGEVITY

7.2.1.1 ICE Start-Stop System

7.2.1.2 EV Start-Stop System

7.3 ELECTRIC POWER STEERING

7.3.1 ADAS INTEGRATION, REDUCTION OF MECHANICAL LOSSES, AND INCREASING REGULATORY PRESSURE FOR EFFICIENCY

7.3.1.1 ICE Electric Power Steering

7.3.1.2 EV Electric Power Steering

7.4 ELECTRO-HYDRAULIC POWER STEERING

7.4.1 NEED FOR HIGH TORQUE ASSIST WITHOUT CONSTANT ENGINE LOAD

7.4.1.1 ICE Electro-hydraulic Power Steering

7.4.1.2 EV Electro-hydraulic Power Steering

7.5 LIQUID HEATER PTC

7.5.1 NEED FOR EFFICIENT CABIN HEATING

7.5.1.1 ICE Liquid Heater PTC

7.5.1.2 EV Liquid Heater PTC

7.6 ELECTRIC A/C COMPRESSOR

7.6.1 EV ADOPTION REQUIRING ENGINE-INDEPENDENT HVAC

7.6.1.1 ICE Electric A/C Compressor

7.6.1.2 EV Electric A/C Compressor

7.7 ELECTRIC VACUUM PUMP

7.7.1 INCREASING HYBRID/ELECTRIC VEHICLE PENETRATION AND INTEGRATION WITH AUTONOMOUS BRAKING SYSTEMS

7.7.1.1 ICE Electric Vacuum Pump

7.7.1.2 EV Electric Vacuum Pump

7.8 ELECTRIC OIL PUMP

7.8.1 NEED FOR INDEPENDENT THERMAL MANAGEMENT

7.8.1.1 ICE Electric Oil Pump

7.8.1.2 EV Electric Oil Pump

7.9 ELECTRIC WATER PUMP

7.9.1 NEED FOR PRECISE COOLANT FLOW CONTROL FOR BATTERY PACKS

7.9.1.1 ICE Electric Water Pump

7.9.1.2 EV Electric Water Pump

7.10 INTEGRATED STARTER GENERATOR

7.10.1 GROWING ADOPTION OF 48V MILD HYBRID VEHICLES

7.10.1.1 ICE Integrated Starter Generator

7.10.1.2 EV Integrated Starter Generator

7.11 PRIMARY INSIGHTS

8 VEHICLE ELECTRIFICATION MARKET, BY VEHICLE TYPE

8.1 INTRODUCTION

8.2 PASSENGER CAR

8.2.1 EXPANSION OF MODULAR, ELECTRIFIED COMPONENTS ACROSS HYBRID AND BEV PLATFORMS

8.3 LIGHT COMMERCIAL VEHICLE

8.3.1 RISING ADOPTION OF HIGH-DUTY ELECTRIC COMPONENTS FOR PAYLOAD OPERATION

8.4 TRUCK

8.4.1 ELEVATED DEMAND FOR HIGH-POWER ELECTRIC PUMPS AND HVAC COMPRESSORS IN CLASS-8 AND MEDIUM-DUTY MODELS

8.5 BUS

8.5.1 INTEGRATION OF ELECTRIFIED AUXILIARIES FOR EFFICIENCY AND RELIABILITY

8.6 PRIMARY INSIGHTS

9 VEHICLE ELECTRIFICATION MARKET, BY DEGREE OF HYBRIDIZATION

9.1 INTRODUCTION

9.2 ICE & MICRO HYBRID VEHICLE

9.2.1 LOW-VOLTAGE HYBRIDIZATION IN PASSENGER AND COMMERCIAL VEHICLES

9.3 HEV

9.3.1 RISE IN STRATEGIC SUPPLIER-OEM PARTNERSHIPS

9.4 PHEV

9.4.1 ADVANCEMENTS IN POWER ELECTRONICS, THERMAL MANAGEMENT, AND BATTERY SUPPLY

9.5 BEV

9.5.1 INCREASED CONSUMER DEMAND FOR ZERO-EMISSION MOBILITY

9.6 PRIMARY INSIGHTS

10 VEHICLE ELECTRIFICATION MARKET, BY REGION

10.1 INTRODUCTION

10.2 ASIA PACIFIC

10.2.1 MACROECONOMIC OUTLOOK

10.2.2 CHINA

10.2.2.1 Strong NEV policies, OEM leadership, and supplier expansion to drive market

10.2.3 JAPAN

10.2.3.1 Leadership in hybrid and plug-in hybrid technologies to drive market

10.2.4 INDIA

10.2.4.1 OEM momentum and supplier localization to drive market

10.2.5 SOUTH KOREA

10.2.5.1 Strong OEM and supplier ecosystem to drive market

10.2.6 REST OF ASIA PACIFIC

10.3 NORTH AMERICA

10.3.1 MACROECONOMIC OUTLOOK

10.3.2 US

10.3.2.1 Stringent regulatory push to drive market

10.3.3 CANADA

10.3.3.1 ZEV mandates and supplier investments to drive market

10.3.4 MEXICO

10.3.4.1 Strict CO2 standards and localized production to drive market

10.4 EUROPE

10.4.1 MACROECONOMIC OUTLOOK

10.4.2 GERMANY

10.4.2.1 High EV production and elevated domestic demand to drive market

10.4.3 NETHERLANDS

10.4.3.1 Substantial EV adoption and V2G innovation to drive market

10.4.4 FRANCE

10.4.4.1 OEM programs, battery projects, and supplier scale-up to drive market

10.4.5 UK

10.4.5.1 Awareness of clean transport to drive market

10.4.6 SPAIN

10.4.6.1 Increasing demand for e-drives and power electronics to drive market

10.4.7 ITALY

10.4.7.1 Concentrated OEM investment and active supplier deals to drive market

10.4.8 REST OF EUROPE

10.5 REST OF THE WORLD

10.5.1 MACROECONOMIC OUTLOOK

10.5.2 BRAZIL

10.5.2.1 Rising demand for fuel-efficient vehicles to drive market

10.5.3 SOUTH AFRICA

10.5.3.1 Growing demand for cleaner and more fuel-efficient vehicles to drive market

10.5.4 OTHERS

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

11.3 ELECTRIC COOLANT PUMP MARKET SHARE ANALYSIS, 2024

11.4 ELECTRIC COMPRESSOR MARKET SHARE ANALYSIS, 2024

11.5 E-AXLE MARKET SHARE ANALYSIS, 2024

11.5.1 CHINESE E-AXLE MARKET SHARE ANALYSIS, 2024

11.6 REVENUE ANALYSIS, 2021-2024

11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.7.1 STARS

11.7.2 EMERGING LEADERS

11.7.3 PERVASIVE PLAYERS

11.7.4 PARTICIPANTS

11.7.5 COMPANY FOOTPRINT

11.7.5.1 Company footprint

11.7.5.2 Region footprint

11.7.5.3 Vehicle type footprint

11.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

11.8.1 PROGRESSIVE COMPANIES

11.8.2 RESPONSIVE COMPANIES

11.8.3 DYNAMIC COMPANIES

11.8.4 STARTING BLOCKS

11.8.5 COMPETITIVE BENCHMARKING

11.8.5.1 List of start-ups/SMEs

11.8.5.2 Competitive benchmarking of start-ups/SMEs

11.9 COMPANY VALUATION AND FINANCIAL METRICS

11.10 BRAND/PRODUCT COMPARISON

11.11 COMPETITIVE SCENARIO

11.11.1 PRODUCT LAUNCHES/DEVELOPMENTS

11.11.2 DEALS

11.11.3 EXPANSIONS

12 COMPANY PROFILES

12.1 KEY PLAYERS

12.1.1 ROBERT BOSCH GMBH

12.1.1.1 Business overview

12.1.1.2 Products offered

12.1.1.3 Recent developments

12.1.1.3.1 Deals

12.1.1.3.2 Expansions

12.1.1.3.3 Others

12.1.1.4 MnM view

12.1.1.4.1 Key strengths

12.1.1.4.2 Strategic choices

12.1.1.4.3 Weaknesses and competitive threats

12.1.2 CONTINENTAL AG

12.1.2.1 Business overview

12.1.2.2 Products offered

12.1.2.3 Recent developments

12.1.2.3.1 Expansions

12.1.2.4 MnM view

12.1.2.4.1 Key strengths

12.1.2.4.2 Strategic choices

12.1.2.4.3 Weaknesses and competitive threats

12.1.3 APTIV

12.1.3.1 Business overview

12.1.3.2 Products offered

12.1.3.3 Recent developments

12.1.3.3.1 Deals

12.1.3.3.2 Expansions

12.1.3.3.3 Others

12.1.3.4 MnM view

12.1.3.4.1 Key strengths

12.1.3.4.2 Strategic choices

12.1.3.4.3 Weaknesses and competitive threats

12.1.4 DENSO CORPORATION

12.1.4.1 Business overview

12.1.4.2 Products offered

12.1.4.3 Recent developments

12.1.4.3.1 Product launches/developments

12.1.4.3.2 Deals

12.1.4.4 MnM view

12.1.4.4.1 Key strengths

12.1.4.4.2 Strategic choices

12.1.4.4.3 Weaknesses and competitive threats

12.1.5 MITSUBISHI MOTORS CORPORATION

12.1.5.1 Business overview

12.1.5.2 Products offered

12.1.5.3 Recent developments

12.1.5.3.1 Deals

12.1.5.4 MnM view

12.1.5.4.1 Key strengths

12.1.5.4.2 Strategic choices

12.1.5.4.3 Weaknesses and competitive threats

12.1.6 BORGWARNER INC.

12.1.6.1 Business overview

12.1.6.2 Products offered

12.1.6.3 Recent developments

12.1.6.3.1 Expansions

12.1.6.3.2 Others

12.1.7 JOHNSON ELECTRIC HOLDINGS LIMITED

12.1.7.1 Business overview

12.1.7.2 Products offered

12.1.7.3 Recent developments

12.1.7.3.1 Product launches/developments

12.1.8 MAGNA INTERNATIONAL INC.

12.1.8.1 Business overview

12.1.8.2 Products offered

12.1.8.3 Recent developments

12.1.8.3.1 Deals

12.1.8.3.2 Expansions

12.1.9 AISIN CORPORATION

12.1.9.1 Business overview

12.1.9.2 Products offered

12.1.9.3 Recent development

12.1.9.3.1 Deals

12.1.9.3.2 Others

12.1.10 NIDEC CORPORATION

12.1.10.1 Business overview

12.1.10.2 Products offered

12.1.10.3 Recent developments

12.1.10.3.1 Product launches/developments

12.1.10.3.2 Expansions

12.1.10.3.3 Others

12.1.11 PANASONIC AUTOMOTIVE SYSTEMS CO., LTD.

12.1.11.1 Business overview

12.1.11.2 Products offered

12.2 OTHER PLAYERS

12.2.1 JTEKT CORPORATION

12.2.2 ASTEMO, LTD.

12.2.3 ZF FRIEDRICHSHAFEN AG

12.2.4 VALEO

12.2.5 GKN AUTOMOTIVE LTD.

12.2.6 SCHAEFFLER AG

12.2.7 MAHLE GMBH

12.2.8 DANA LIMITED

12.2.9 BROSE FAHRZEUGTEILE SE & CO. KG

12.2.10 KEB AUTOMATION

12.2.11 TECO CORPORATION

12.2.12 YASA LIMITED

13 RECOMMENDATIONS

13.1 ASIA PACIFIC TO BE LEADING MARKET FOR VEHICLE ELECTRIFICATION

13.2 STEERING SYSTEMS EMERGE AS KEY ENABLER OF VEHICLE ELECTRIFICATION