건설용 플라스틱 시장 예측(-2030년) : 플라스틱 유형별, 용도별, 최종 용도 산업별, 지역별

Construction Plastics Market by Plastic Type (PVC, PE, PP, PS, PC, PU), Application (Pipes, Windows & Doors, Insulation Materials, Roofing, Flooring, Ducts, Walls), End-use Industry (Residential, Non-Residential), and Region - Global Forecast to 2030

상품코드:1823731

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 247 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

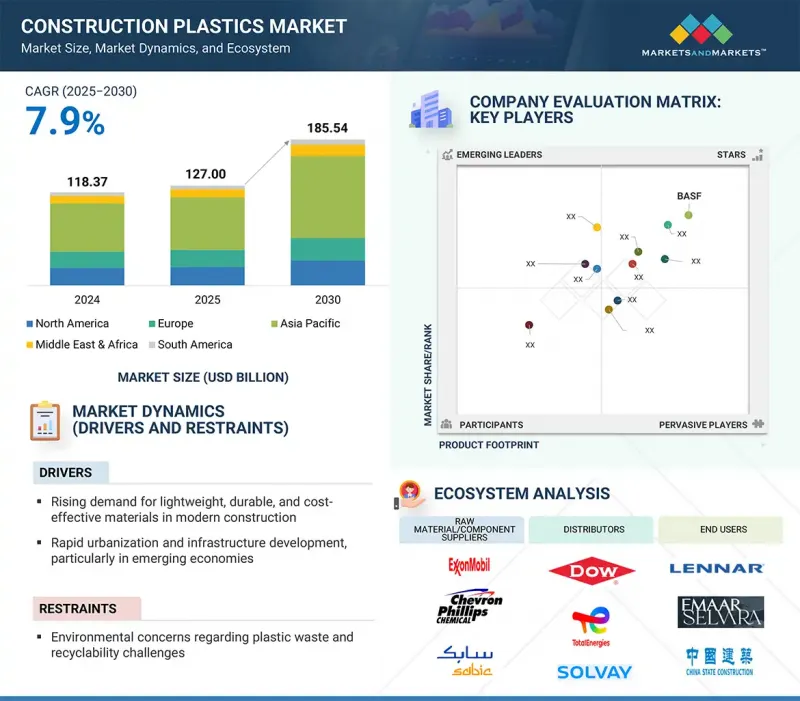

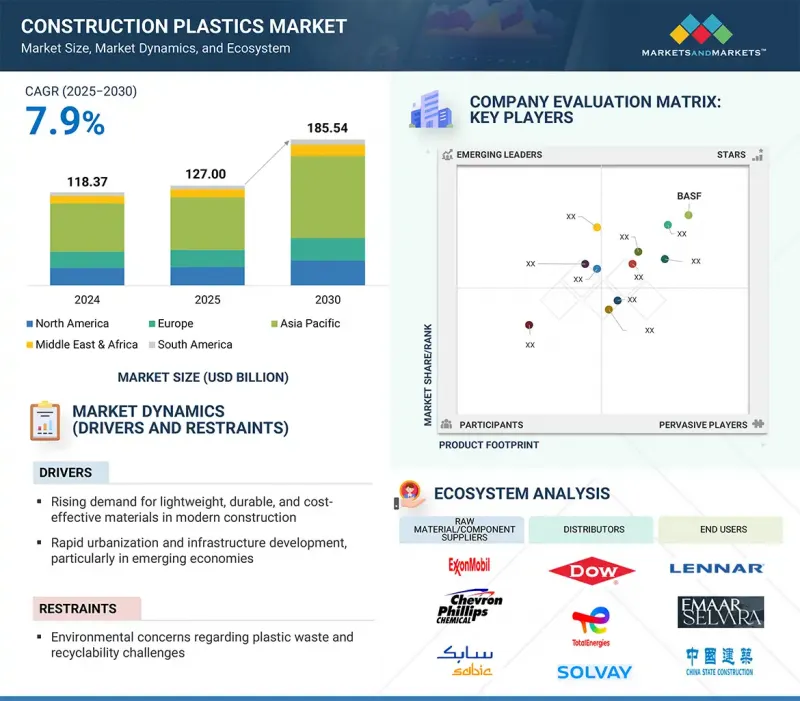

건설용 플라스틱 시장 규모는 2025년에 1,270억 달러로 추정되며, 2025-2030년의 CAGR은 7.9%로 전망되고 있으며, 2030년에는 1,855억 4,000만 달러에 달할 것으로 예측됩니다.

조사 범위

조사 대상 연도

2022-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러), 킬로톤

부문

플라스틱 유형별, 용도별, 최종 용도 산업별, 지역별

대상 지역

유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미

폴리스티렌은 저렴한 가격, 적응성, 지붕재, 단열재, 경량 건축 등 다양한 용도로 사용되어 현재 세계 건축용 플라스틱 시장에서 두 번째 점유율을 차지하고 있습니다. 압출 폴리스티렌(XPS)과 발포 폴리스티렌(EPS)은 우수한 단열성으로 인해 에너지 효율이 높은 건축 솔루션에 필수적이며, 가장 중요한 두 가지 용도로 사용됩니다. 주거 및 상업 분야 모두에서 폴리스티렌 기반 단열재에 대한 수요가 꾸준히 증가하고 있는 것은 친환경 건축에 대한 관심이 높아지고, 건물의 에너지 성능 향상에 대한 규제 요건이 강화되고 있기 때문입니다. 또한 폴리스티렌은 가볍고 시공이 간편하여 인건비가 저렴하므로 대규모 인프라 프로젝트에서 사용이 권장되고 있습니다.

폴리스티렌은 환경 문제, 특히 재활용의 어려움으로 인해 많은 비판을 받고 있지만, 재활용 기술의 발전과 바이오 대체품의 개발은 이러한 문제를 완화하는 데 도움이 될 것으로 보입니다. 유럽에서는 지속가능한 건축 솔루션에 대한 관심이 첨단 EPS/XPS 소재의 사용을 촉진하는 반면, 아시아태평양은 중국과 인도의 급속한 도시화에 힘입어 소비량에서 선두를 달리고 있습니다. 북미는 특히 주택 건설 및 개보수 프로젝트에서 중요한 역할을 하고 있습니다. 전반적으로 폴리스티렌은 경제성, 기능성 및 진화하는 지속가능성 기준의 균형을 유지하면서 건축용 플라스틱의 중요한 구성 요소로 남아있습니다.

현대 건축 설계에서 열적 쾌적성과 에너지 효율성 향상에 중요한 역할을 하는 단열재는 세계 건축용 플라스틱 시장에서 두 번째 점유율을 차지하고 있습니다. 세계 각국 정부와 규제기관이 에너지 효율 규제와 친환경 건축물 인증을 강화하면서 발포 폴리스티렌(EPS), 압출 폴리스티렌(XPS), 폴리우레탄 폼 등 단열 플라스틱에 대한 수요가 증가하고 있습니다. 뛰어난 내열성과 경량성으로 인해 바닥재, 벽, 지붕에 널리 사용되고 있습니다. 이를 통해 냉난방 부하를 줄여 운전 비용과 에너지 소비를 절감할 수 있습니다. 선진국의 노후화된 인프라 보수 및 개축, 신흥 국가의 급속한 도시화로 인해 효율적인 단열 솔루션에 대한 요구가 더욱 커지고 있습니다.

또한 전 세계에서 제로 에너지 빌딩과 지속가능한 건축 공법이 추진됨에 따라 첨단 단열 플라스틱도 널리 사용되고 있습니다. 재활용 가능한 단열 폼과 바이오 대체품의 혁신은 특히 재활용 가능성과 사용 후 제품 폐기와 관련하여 환경에 미치는 영향에 대한 비판에도 불구하고 새로운 시장 기회를 열어주고 있습니다. 단열재는 주거, 상업, 산업 분야에서 높은 수요를 보이고 있으며, 건축용 플라스틱 산업에서 없어서는 안 될 필수적인 요소로 자리 잡고 있습니다.

비주거 부문은 전 세계 상업, 산업 및 시설 건축 프로젝트의 강력한 성장에 힘입어 건축용 플라스틱 시장에서 가장 높은 시장 점유율을 차지할 것으로 예측됩니다. 플라스틱은 내구성, 비용 효율성, 디자인 유연성 등으로 인해 오피스 단지, 쇼핑몰, 공항, 병원, 학교, 공장 등에서 배관, 단열재, 지붕재, 바닥재, 창틀, 피복재 등의 용도로 널리 사용되고 있습니다. 특히 아시아태평양, 중동 및 아프리카의 신흥 경제권에서 현대식 인프라에 대한 수요가 증가함에 따라 비주거용 프로젝트에서 플라스틱 기반 재료의 대규모 채택이 촉진되고 있습니다. 사우디아라비아의 NEOM City와 중국의 상업 허브에 대한 지속적인 투자와 같은 대규모 인프라 계획은 효율적이고 지속가능한 솔루션을 위한 건설용 플라스틱 사용에 박차를 가하고 있습니다. 북미와 유럽과 같은 선진 지역에서는 그린 빌딩 인증과 더 엄격한 에너지 효율 규제를 충족하기 위한 비주거용 건물의 개축 및 현대화가 수요를 더욱 촉진하고 있습니다.

유럽은 지속가능한 건설, 리노베이션 활동, 엄격한 건축법규 준수에 중점을 두고 있으며, 건설용 플라스틱 시장에서 세 번째 시장 점유율을 차지할 것으로 예측됩니다. 이 지역은 건설 산업이 성숙하고 주택, 비주거, 인프라 프로젝트에서 고급 플라스틱 용도에 대한 수요가 높은 지역입니다. PVC, 폴리에틸렌, 폴리프로필렌 등의 플라스틱은 내구성, 비용 효율성, 에너지 절약성으로 인해 단열 파이프, 창틀, 지붕재, 바닥재 등에 널리 사용되고 있습니다. BREEAM 및 LEED 인증과 같은 친환경 건축 표준에 대한 유럽의 리더십은 탄소 감축 목표를 지원하는 재활용 가능하고 에너지 효율적인 플라스틱 솔루션의 채택을 가속화하고 있습니다. 유럽연합(EU)의 유럽 그린딜과 순환 경제 원칙에 대한 강조는 재활용 플라스틱과 바이오 플라스틱의 기술 혁신을 촉진하고 시장에서의 역할을 더욱 강화시키고 있습니다. 특히 독일, 프랑스, 영국 등에서는 오래된 주택이 새로운 에너지 효율 요구 사항을 충족시키기 위해 현대화되고 있습니다.

세계의 건설용 플라스틱 시장에 대해 조사했으며, 플라스틱 유형별, 용도별, 최종 용도 산업별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

서론

시장 역학

Porter's Five Forces 분석

고객 비즈니스에 영향을 미치는 동향/혼란

에코시스템 분석

밸류체인 분석

규제 상황

무역 분석

가격 분석

기술 분석

특허 분석

사례 연구 분석

2025-2026년의 주요 컨퍼런스와 이벤트

투자와 자금조달 시나리오

생성형 AI/AI가 건설용 플라스틱 시장에 미치는 영향

주요 이해관계자와 구입 기준

거시경제 분석

2025년 미국 관세가 건설용 플라스틱 시장에 미치는 영향

제6장 건설용 플라스틱 시장(플라스틱 유형별)

서론

폴리염화비닐(PVC)

폴리에틸렌(PE)

폴리프로필렌(PP)

폴리스티렌(PS)

폴리우레탄(PU)

폴리카보네이트(PC)

기타

제7장 건설용 플라스틱 시장(용도별)

서론

파이프

창문과 도어

단열재

바닥재

루핑

덕트

벽

기타

제8장 건설용 플라스틱 시장(최종 용도 산업별)

서론

비주택

주택

제9장 건설용 플라스틱 시장(지역별)

서론

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

기타

남미

브라질

아르헨티나

기타

아시아태평양

중국

일본

인도

한국

기타

중동 및 아프리카

GCC 국가

기타

제10장 경쟁 구도

개요

주요 참여 기업의 전략

시장 점유율 분석, 2024년

매출 분석, 2020-2024년

기업 평가와 재무 지표

제품/브랜드 비교

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제11장 기업 개요

주요 참여 기업

BASF

SABIC

DOW

LYONDELLBASELL INDUSTRIES HOLDINGS B.V.

BOREALIS GMBH

FORMOSA PLASTICS CORPORATION

INEOS

SOLVAY

ASAHI KASEI CORPORATION

TOTALENERGIES

기타 기업

PALRAM INDUSTRIES LTD.

PLASKOLITE

EXCELITE PLASTIC CO. LTD.

CHEVRON PHILLIPS CHEMICAL COMPANY LLC.

SIBUR HOLDING PJSC

CHINA PETROCHEMICAL CORPORATION

SUMITOMO CHEMICAL CO., LTD.

LG CHEM

RELIANCE INDUSTRIES LIMITED(RIL)

QATAR PETROCHEMICAL COMPANY(QAPCO) Q.P.J.S.C

SIMONA AG

BRASKEM

OCCIDENTAL PETROLEUM CORPORATION

WESTLAKE CORPORATION

VERSALIS S.P.A.

제12장 부록

KSA

영문 목차

영문목차

The construction plastics market is estimated at USD 127.00 billion in 2025 and is projected to reach USD 185.54 billion by 2030, at a CAGR of 7.9% from 2025 to 2030.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion), Volume (Kiloton)

Segments

Plastic Type, Application, End-use Industry, and Region

Regions covered

Europe, North America, Asia Pacific, the Middle East & Africa, and South America

Due to its affordability, adaptability, and extensive use in roofing, insulation, and lightweight construction, polystyrene currently holds the second-largest share in the global construction plastics market. Extruded polystyrene (XPS) and expanded polystyrene (EPS), which are highly prized for their superior thermal insulation qualities and essential to energy-efficient building solutions, are two of its most important applications. Both the residential and commercial sectors have seen a steady increase in demand for polystyrene-based insulation materials due to the growing emphasis on green construction and regulatory requirements for improved energy performance in buildings. Furthermore, polystyrene's low weight and simplicity of installation lower labor costs, which encourages its use in major infrastructure projects.

Although polystyrene is often criticized for its environmental issues, particularly its difficulty in recycling, advancements in recycling technology and the development of bio-based alternatives may help mitigate these challenges. In Europe, the focus on sustainable building solutions continues to promote the use of advanced EPS/XPS materials, while the Asia Pacific region leads in consumption, driven by rapid urbanization in China and India. North America also plays a significant role, particularly in residential construction and retrofitting projects. Overall, polystyrene remains a crucial component of construction plastics, balancing affordability, functionality, and evolving sustainability standards.

''In terms of value, the insulation materials segment accounted for the second-largest share of the construction plastics market.''

Due to their critical role in improving thermal comfort and energy efficiency in contemporary building designs, insulation materials account for the second-largest share of the global construction plastics market. As governments and regulatory agencies around the world impose more stringent energy-efficiency regulations and green building certifications, the demand for insulation plastics like expanded polystyrene (EPS), extruded polystyrene (XPS), and polyurethane foams has increased. Because of their exceptional thermal resistance and lightweight nature, these materials are widely used in flooring, walls, and roofs. This lowers operating costs and energy consumption by reducing heating and cooling loads. The need for efficient insulation solutions is further supported by the renovation and retrofitting of aging infrastructure in developed regions, as well as the rapid urbanization in emerging economies.

Advanced insulation plastics are also becoming more widely used due to the global push for net-zero energy buildings and sustainable construction methods. Innovations in recyclable insulation foams and bio-based substitutes are opening up new market opportunities despite criticism about their effects on the environment, particularly with regard to recyclability and end-of-life disposal. Insulation materials continue to be a vital component of the construction plastics industry, with high demand in the residential, commercial, and industrial sectors.

"The non-residential sector is projected to account for the largest market share in the construction plastics market during the forecast period."

The non-residential sector is expected to hold the highest market share in the construction plastics market, supported by strong growth in commercial, industrial, and institutional building projects worldwide. Plastics are extensively used in office complexes, shopping malls, airports, hospitals, schools, and factories for applications such as piping, insulation, roofing, flooring, window frames, and cladding due to their durability, cost efficiency, and design flexibility. The rising demand for modern infrastructure, particularly in emerging economies across the Asia Pacific, the Middle East, and Africa, is driving large-scale adoption of plastic-based materials in non-residential projects. Mega infrastructure initiatives like Saudi Arabia's NEOM City and China's continued investments in commercial hubs are fueling the use of construction plastics for efficient and sustainable solutions. In developed regions like North America and Europe, demand is further boosted by the renovation and modernization of non-residential buildings to meet green building certifications and stricter energy efficiency regulations.

"Europe is projected to account for the third-largest market share in the construction plastics market during the forecast period."

Europe is expected to account for the third-largest market share in the construction plastics market, driven by its strong focus on sustainable construction, renovation activities, and adherence to stringent building regulations. The region has a mature construction industry with high demand for advanced plastic applications in residential, non-residential, and infrastructure projects. Plastics such as PVC, polyethylene, and polypropylene are widely used in insulation pipes, window frames, roofing, and flooring due to their durability, cost efficiency, and energy-saving properties. Europe's leadership in green building standards, including BREEAM and LEED certifications, is accelerating the adoption of recyclable and energy-efficient plastic solutions that support carbon reduction goals. The European Union's commitment to the European Green Deal and its focus on circular economy principles are encouraging innovations in recycled and bio-based plastics, further enhancing their market role. The region also sees significant demand from renovation and retrofitting projects, particularly in countries like Germany, France, and the UK, where older housing stock is being modernized to meet new energy efficiency requirements.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

By Designation: C Level - 33%, Director Level - 33%, and Managers - 34%

By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa - 15%, and Latin America - 15%

The report offers a detailed analysis of various company profiles, highlighting prominent companies such as BASF (Germany), SABIC (Saudi Arabia), Dow (USA), LyondellBasell Industries Holdings B.V. (USA), Borealis GmbH (Austria), Formosa Plastics Corporation (Taiwan), INEOS (UK), Solvay (Belgium), Asahi Kasei Corporation (Japan), and TotalEnergies (France).

Reasons to Buy This Report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall construction plastics market and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (rising demand for lightweight, durable, and cost-effective materials in modern construction, increasing adoption of plastics for insulation, piping, and structural applications due to superior performance over conventional materials, and growth in energy-efficient and green building construction, which boost demand for plastic-based insulation and roofing materials), restraints (environmental concerns regarding plastic waste and recyclability challenges and stringent government regulations limiting plastic usage in certain regions), opportunities (growing smart city projects and infrastructure investments worldwide and increasing integration of recycled and bio-based plastics to meet sustainability targets), and challenges (limited awareness and acceptance of advanced plastic composites in developing markets, supply chain disruptions, and high dependency on petrochemical feedstocks).

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the construction plastics market.

Market Development: Comprehensive information about lucrative markets - the report analyses the construction plastics market across varied regions.

Market Diversification: Exhaustive information about products, untapped geographies, recent developments, and investments in the construction plastics market

Competitive Assessment: In-depth assessment of market shares, growth strategies and product offerings of leading players like BASF (Germany), SABIC (Saudi Arabia), Dow (US), LyondellBasell Industries Holdings B.V. (US), Borealis GmbH (Austria), Formosa Plastics Corporation (Taiwan), INEOS (UK), Solvay (Belgium), Asahi Kasei Corporation (Japan), and TotalEnergies (France).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.3 BASE NUMBER CALCULATION

2.3.1 DEMAND-SIDE APPROACH

2.3.2 SUPPLY-SIDE APPROACH

2.4 MARKET FORECAST APPROACH

2.4.1 SUPPLY SIDE

2.4.2 DEMAND SIDE

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONSTRUCTION PLASTICS MARKET

4.2 CONSTRUCTION PLASTICS MARKET, BY PLASTIC TYPE

4.3 CONSTRUCTION PLASTICS MARKET, BY APPLICATION

4.4 CONSTRUCTION PLASTICS MARKET, BY END-USE INDUSTRY

4.5 CONSTRUCTION PLASTICS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Urbanization and infrastructure growth

5.2.1.2 Innovation in sustainability-driven material solutions

5.2.2 RESTRAINTS

5.2.2.1 Regulatory restrictions

5.2.2.2 Alternatives gaining traction

5.2.3 OPPORTUNITIES

5.2.3.1 Integration of circular economy principles

5.2.3.2 Infrastructure investments in emerging countries

5.2.4 CHALLENGES

5.2.4.1 Volatility in crude oil prices

5.2.4.2 Underdeveloped recycling infrastructure

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 BARGAINING POWER OF SUPPLIERS

5.3.2 THREAT OF NEW ENTRANTS

5.3.3 THREAT OF SUBSTITUTES

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.5 ECOSYSTEM ANALYSIS

5.6 VALUE CHAIN ANALYSIS

5.7 REGULATORY LANDSCAPE

5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.7.2 REGULATIONS

5.7.2.1 California Proposition 65 - Safe Drinking Water and Toxic Enforcement Act of 1986

5.7.2.2 TSCA (Toxic Substances Control Act) - 15 U.S.C. 2601 et seq.

5.7.2.3 REACH Regulation (EC) No 1907/2006 - Registration, Evaluation, Authorisation and Restriction of Chemicals

5.7.2.4 Construction Products Regulation (CPR) (EU) No 305/2011

5.7.2.5 U.S. International Building Code (IBC) & ASTM Standards