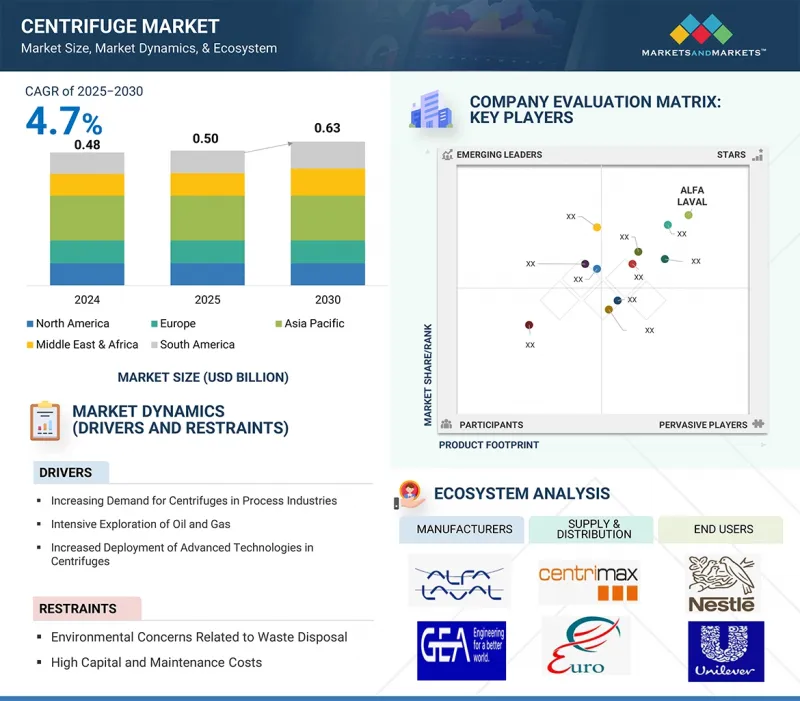

원심분리기 시장 규모는 4.7%의 CAGR로 확대하며, 2025년 5억 달러에서 2030년에는 6억 3,000만 달러로 성장할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 유닛 | 금액(100만 달러/10억 달러) 및 수량(대) |

| 부문 | 용도별, 용량별, 최종 용도 산업별, 로터 유형별, 스피드별, 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 & 아프리카, 남미 |

원심분리기 시장은 제약, 생명공학, 식품 및 음료, 화학, 광업, 폐수처리 등의 산업에서 수요가 증가함에 따라 꾸준히 성장하고 있습니다. 세계 인구 증가, 급속한 도시화, 환경 규제 강화로 인해 산업계는 효율성, 품질 및 규정 준수를 개선하기 위해 첨단 분리 기술을 도입하고 있습니다.

제약 및 생명공학 분야에서는 의약품 제조 및 진단에서 정확한 분리의 필요성이 원심분리기의 활용을 확대하고 있으며, 식품 가공 분야에서는 오염물질이 없는 고품질 제품의 필요성이 수요를 촉진하고 있습니다. 광업 분야에서는 광물 회수에 원심분리기를 사용하며, 폐수처리장에서는 슬러지 탈수 및 자원 회수에 원심분리기를 활용하고 있습니다. 자동화, 에너지 효율적 설계, 공정 제어 강화 등 기술 발전으로 인해 채택이 더욱 가속화되고 있습니다. 아시아태평양은 산업 확장, 도시 인프라 개발, 헬스케어 투자 증가로 시장 개발을 주도하고 있으며, 북미와 유럽은 기술 혁신과 규제 준수에 따른 안정적인 수요를 보이고 있습니다. 설비 비용의 상승과 유지보수 필요성 등의 문제에도 불구하고 세계 원심분리기 시장은 산업 현대화와 자원 효율성 추구에 힘입어 지속적인 성장이 예상됩니다. 이러한 성장은 재생에너지, 생명공학 연구, 정밀 제조 분야의 새로운 용도에 의해 더욱 강화될 것입니다.

산업용 원심분리기는 제약, 식품 및 음료, 화학 제조, 석유 및 가스, 폐수 처리 등 대규모 처리 산업에서 광범위하게 채택되어 강력한 성장을 목격하고 있습니다. 이 원심분리기는 연속적인 고처리량 작업을 위해 설계되어 산업 규모에서 고체와 액체, 액체와 액체를 효율적으로 분리하고 입자를 정화할 수 있습니다. 수요 증가의 배경에는 산업 자동화의 발전, 품질 기준의 강화, 생산 시설의 효율적인 폐기물 관리의 필요성이 있습니다. 제약 부문에서는 산업용 원심분리기가 의약품 유효성분(API) 생산에 필수적이며, 식품 산업에서는 우유 정화, 주스 추출, 식용유 정제 등의 공정에 사용됩니다. 폐수처리장도 슬러지 탈수 및 폐수 관리를 위해 산업용 원심분리기에 크게 의존하고 있습니다. 에너지 효율이 높은 모터, 강화된 안전 시스템, IoT 지원 모니터링 등 설계의 발전이 채택을 촉진하고 있습니다. 신흥 국가의 제조 거점 확대와 청정 산업 공정에 대한 규제 강화는 시장 성장을 더욱 촉진하고 있습니다.

처리 용량이 10m3/시간 미만인 소용량 원심분리기 부문은 특수하고 정밀한 용도에 적합해 원심분리기 시장에서 가장 빠르게 성장하고 있습니다. 이 원심분리기는 고정밀, 제어된 시료 처리, 컴팩트한 디자인이 중요한 연구실, 임상 진단, 파일럿 규모 생산, 틈새 산업 공정에 널리 사용됩니다. 상대적으로 설치 면적이 작고 휴대성이 뛰어나며, 기존 설비에 쉽게 통합할 수 있으며, 공간과 예산에 제약이 있는 연구실이나 소규모 생산 장비에 적합합니다. 또한 특히 제약, 생명공학, 식품 가공, 환경 검사 분야에서 맞춤형 원심분리에 대한 수요가 증가함에 따라 원심분리에 대한 채택이 더욱 가속화되고 있습니다. 전 세계에서 맞춤형 의료의 급격한 증가, 연구개발 활동의 집중화, 신흥 국가의 소규모 제조 확대도 주요 성장 촉진요인으로 꼽힙니다. 또한 소용량 원심분리기는 설비 투자가 적고 유지보수 비용도 절감할 수 있으므로 비용에 민감한 최종사용자에게 매력적입니다. 개선된 로터 설계, 디지털 제어, 에너지 효율 등의 기술 발전으로 용량이 확대되어 더 복잡한 분리 작업에 적합합니다.

5,000-20,000RPM에서 작동하는 중속 원심분리기 부문은 다목적성과 폭넓은 적용 범위로 인해 원심분리기 시장에서 가장 빠르게 성장하고 있습니다. 이 원심분리기는 분리 효율과 시료의 무결성 사이에서 최적의 균형을 이루며, 산업 및 실험실 환경 모두에 적합합니다. 생명공학 및 제약 분야에서 중속 원심분리기는 세포 채취, 단백질 정제, 백신 제조에 사용되며, 섬세한 생물학적 물질을 손상 없이 정확하게 분리하는 것이 필수적입니다. 산업 공정에서 폐수 처리, 식품 및 음료 정화, 화학 처리에서 중요한 역할을 하는 중속 원심분리기는 부품의 마모를 줄이면서 효과적인 분리를 실현할 수 있습니다. 생물학적 샘플에서 산업용 슬러리까지 다양한 자재관리에 대응할 수 있는 적응성으로 인해 다양한 분야에서 수요가 확대되고 있습니다. 또한 중속 원심분리기는 일반적으로 초고속 모델보다 에너지 소비가 적어 비용 절감과 운영의 지속가능성을 제공합니다. 로터 밸런스 강화, 자동 제어, 안전 메커니즘 개선 등의 기술 혁신을 통해 효율성과 사용 편의성을 더욱 향상시켰습니다. 또한 바이오의약품 제조의 확대, 연구 투자 증가, 확장 가능하고 효율적인 분리 솔루션에 대한 니즈도 성장의 원동력이 되고 있습니다.

고정각 로터 원심분리기 부문은 효율성, 다목적성, 산업 및 실험실에서의 광범위한 채택으로 인해 원심분리기 시장의 로터 유형 카테고리에서 가장 빠른 성장세를 보이고 있습니다. 고정각 로터는 회전축에 대해 일정한 각도(보통 25-40도)로 시료를 고정하여 튜브 벽을 따라 입자를 빠르게 침전시킬 수 있습니다. 이 설계는 높은 분리 효율을 달성하면서 작동 시간을 최소화하여 세포 펠릿화, 세포내 성분 분리, 핵산 정제, 산업용 워크플로우의 대량 처리 등의 용도에 이상적입니다. 바이오의약품 제조에서 고정각 로터는 고 수율의 세포배양 채취 및 단백질 분리를 위해 선호되고 있습니다. 견고한 설계로 스윙 버킷 로터에 비해 더 빠른 속도와 더 큰 원심력을 지원하며, 다양한 점도와 밀도에 적합합니다. 식품 가공, 화학 제조, 폐수 처리와 같은 산업 분야에서는 내구성과 비용 효율성으로 인해 이 원심분리기를 점점 더 많이 채택하고 있습니다. 내식 합금, 경량 복합재 등 로터 소재의 발전으로 성능이 향상되고 수명이 연장되었습니다. 또한 자동 제어 및 강화된 안전 메커니즘을 특징으로 하는 최신 원심분리기 시스템과의 호환성이 수요를 주도하고 있습니다.

유체 정화 부문은 고순도 액체를 필요로 하는 산업 전반에서 중요한 역할을 하고 있으며, 원심분리기 시장에서 가장 빠른 성장을 보이고 있습니다. 유체 정화에는 액체에서 부유 물질, 불순물 및 기타 미립자를 효율적으로 제거하여 다운스트림 공정에서 일관된 품질과 성능을 보장하는 것이 포함됩니다. 이 용도는 주스, 와인, 맥주를 맑게 하는 식품 및 음료 산업, 유효 성분이나 주사제를 정제하는 제약 산업, 귀중한 생체 분자로부터 세포 잔해를 분리하는 생명공학 산업에서 특히 중요합니다. 또한 화학 및 석유화학 산업에서는 공정 효율과 제품 무결성을 유지하기 위해 유체 정화에 의존하고 있습니다. 규제 준수, 제품 안전성, 품질 기준에 대한 중요성이 강조되면서 채택이 증가하고 있습니다. 또한 고속, 자동화, CIP(Clean In Place) 시스템 등 원심분리기 기술의 발전으로 가동 중단 시간을 줄이면서 정화 효율이 향상되고 있습니다. 특히 도시 및 산업 환경에서의 수처리 구상의 확대는 유체 정화에 대한 원심분리기 수요를 더욱 증가시키고 있습니다. 산업 생산량이 증가하고 환경 규제가 강화되고 있는 신흥 국가들은 이러한 성장에 크게 기여하고 있습니다.

산업계가 효율성, 지속가능성, 정확성을 점점 더 중요시하는 가운데, 원심분리기를 이용한 유체 정화는 필수 불가결한 요소로 자리 잡으며 시장 가치 측면에서 가장 빠르게 성장하는 용도로 자리매김하고 있습니다.

제약 산업은 인구 증가, 고령화, 만성질환 및 전염병의 유행으로 인해 의약품, 백신, 생물제제에 대한 전 세계적인 수요가 증가함에 따라 원심분리기 시장에서 가장 빠르게 성장하는 최종 용도 분야입니다. 원심분리기는 의약품 제조, 특히 원료의약품, 혈액성분, 세포배양, 생물제제의 분리, 정제, 정련, 정화 과정에서 중요한 역할을 합니다. 바이오의약품과 맞춤 의료의 급속한 성장은 원심분리기, 특히 고속 원심분리기와 초원심분리기의 채택을 더욱 가속화하고 있습니다. 또한 COVID-19 팬데믹은 백신 생산 및 연구를 위한 첨단 원심분리 기술의 필요성을 부각시켰습니다. 의약품의 엄격한 규제 요건과 연속 생산으로의 전환은 정확성, 무균성 및 규정 준수를 보장하는 고성능 자동 원심분리기에 대한 투자를 촉진하고 있습니다.

아시아태평양은 급속한 산업화, 제조 능력 확대, 인프라 및 공정 산업에 대한 막대한 투자로 인해 원심분리기 시장에서 가장 빠르게 성장하는 지역입니다. 중국, 인도, 일본, 한국 등의 국가에서는 제약, 생명공학, 식품 및 음료, 화학 처리, 폐수 처리 등의 분야에서 강력한 성장을 보이고 있으며, 이 모든 분야는 원심분리기 기술에 크게 의존하고 있습니다. 인구 증가와 가처분 소득 증가로 인한 헬스케어 수요 증가로 인해 제약 및 바이오프로세스용 원심분리기에 대한 수요가 증가하고 있습니다. 깨끗한 물, 폐기물 관리, 환경 규제 준수에 대한 정부의 구상으로 지자체 및 산업 폐수 처리에 대한 채택이 가속화되고 있습니다. 또한 아시아태평양은 제조 및 연구개발의 거점이 되고 있으며, 세계 기업은 현지 가동률을 높이고 비용을 절감하기 위해 생산시설을 설치하여 현지 가동률을 높이고 있습니다. 경쟁력 있는 노동 시장, 유리한 무역정책, 수출 증가도 시장 확대에 기여하고 있습니다. 이 지역의 강력한 경제 성장, 도시 개발, 산업 다각화는 세계 원심분리기 산업의 주요 성장 동력으로 자리매김하고 있습니다.

세계의 원심분리기 시장에 대해 조사했으며, 용도별, 용량별, 최종 용도 산업별, 로터 유형별, 스피드별, 유형별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

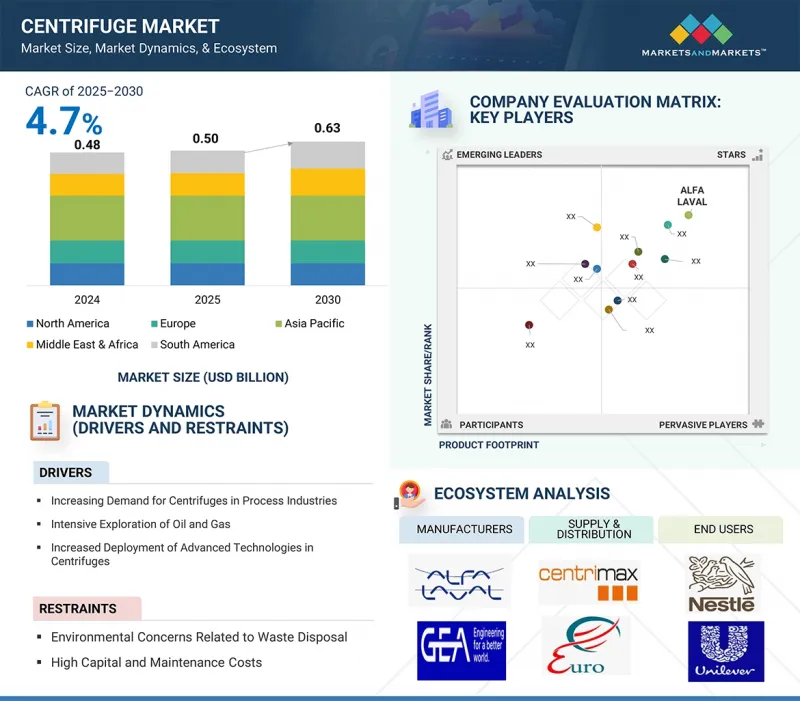

The centrifuge market is projected to grow from USD 0.50 billion in 2025 to USD 0.63 billion by 2030, at a CAGR of 4.7%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) and Volume (Units) |

| Segments | Type, Speed, Rotor Type, Capacity, Application, End-use Industry, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and South America |

The centrifuge market is experiencing steady growth driven by rising demand across industries such as pharmaceuticals, biotechnology, food and beverage, chemicals, mining, and wastewater treatment. Increasing global population, rapid urbanization, and stricter environmental regulations are prompting industries to adopt advanced separation technologies for improved efficiency, quality, and compliance.

In pharmaceuticals and biotechnology, the need for precise separation in drug manufacturing and diagnostics is expanding centrifuge usage, while in food processing, the demand is fueled by the need for high-quality, contaminant-free products. The mining sector uses centrifuges for mineral recovery, and wastewater treatment plants rely on them for sludge dewatering and resource recovery. Technological advancements, including automation, energy-efficient designs, and enhanced process control, are further boosting adoption. Asia Pacific leads market growth due to industrial expansion, urban infrastructure development, and rising healthcare investments, while North America and Europe see steady demand driven by innovation and regulatory compliance. Despite challenges such as high equipment costs and maintenance requirements, the global centrifuge market is poised for sustained expansion, supported by industrial modernization and the push for resource efficiency. This growth is further reinforced by emerging applications in renewable energy, biotechnology research, and precision manufacturing.

" Industrial centrifuge is projected to register the fastest growth in the centrifuge market in terms of value during the forecast period."

Industrial centrifuges are witnessing strong growth due to their widespread adoption in large-scale processing industries, including pharmaceuticals, food & beverage, chemical manufacturing, oil & gas, and wastewater treatment. These machines are designed for continuous, high-throughput operations, enabling efficient separation of solids from liquids, liquids from liquids, and particle clarification at an industrial scale. Their rising demand is driven by increasing industrial automation, stricter quality standards, and the need for efficient waste management in production facilities. In the pharmaceutical sector, industrial centrifuges are critical for producing active pharmaceutical ingredients (APIs), while in the food industry, they are used for processes such as milk clarification, juice extraction, and edible oil purification. Wastewater treatment plants also rely heavily on industrial centrifuges for sludge dewatering and effluent management. Advancements in design, such as energy-efficient motors, enhanced safety systems, and IoT-enabled monitoring, are boosting their adoption. The expansion of manufacturing bases in emerging economies, combined with regulatory pushes for cleaner industrial processes, further fuels market growth. As industries increasingly focus on operational efficiency and sustainable practices, industrial centrifuges are becoming indispensable, leading to their position as the fastest-growing type segment in the global centrifuge market.

"Small capacity (< 10 m3/hour) segment to register the fastest growth in the centrifuge market in terms of value during the forecast period."

The small capacity centrifuge segment, defined as units with a throughput of less than 10 m3/hour, is experiencing the fastest growth in the centrifuge market due to its suitability for specialized, precision-driven applications. These centrifuges are widely used in research laboratories, clinical diagnostics, pilot-scale production, and niche industrial processes where high accuracy, controlled sample handling, and compact design are critical. Their relatively low operational footprint, portability, and ease of integration into existing facilities make them ideal for laboratories and small-scale production units with space and budget constraints. Moreover, the rising demand for customized, application-specific centrifugation, especially in pharmaceuticals, biotechnology, food processing, and environmental testing, has further accelerated adoption. The global surge in personalized medicine, increased focus on R&D activities, and expansion of small-scale manufacturing in emerging economies are also key growth drivers. Additionally, small capacity centrifuges often require lower capital investment and offer reduced maintenance costs, appealing to cost-sensitive end users. Technological advancements, such as improved rotor designs, digital controls, and energy efficiency, have expanded their capabilities, making them suitable for more complex separation tasks. As industries increasingly value flexibility, precision, and operational efficiency, small capacity centrifuges are set to maintain their strong growth trajectory during the forecast period.

"Medium speed (5,000-20,000 RPM) segment to register the highest growth in the centrifuge market, in terms of value, during the forecast period."

The medium-speed centrifuge segment, operating between 5,000 and 20,000 RPM, is witnessing the fastest growth in the centrifuge market due to its versatility and broad application range. These centrifuges strike an optimal balance between separation efficiency and sample integrity, making them suitable for both industrial and laboratory settings. In biotechnology and pharmaceuticals, medium-speed centrifuges are used for cell harvesting, protein purification, and vaccine production, where precise separation without damaging sensitive biological materials is essential. In industrial processes, they play a critical role in wastewater treatment, food and beverage clarification, and chemical processing, where moderate speeds ensure effective separation with reduced wear on components. Their adaptability to handle a wide variety of materials, from biological samples to industrial slurries, has expanded their demand across diverse sectors. Furthermore, medium-speed centrifuges typically consume less energy than ultra-high-speed models, offering cost savings and operational sustainability. Technological innovations, such as enhanced rotor balancing, automated controls, and improved safety mechanisms, have further increased their efficiency and user-friendliness. The growth is also driven by expanding biopharmaceutical manufacturing, increased investment in research, and the need for scalable yet efficient separation solutions. As industries seek cost-effective, versatile centrifugation options, the medium-speed category is positioned for sustained high growth.

"Fixed-angle rotor centrifuge segment to register the highest growth in the centrifuge market in terms of value during the forecast period."

The fixed-angle rotor centrifuge segment is experiencing the fastest growth in the rotor type category of the centrifuge market due to its efficiency, versatility, and widespread industrial and laboratory adoption. Fixed-angle rotors hold samples at a constant angle (typically 25°-40°) relative to the axis of rotation, enabling rapid sedimentation of particles along the tube wall. This design minimizes run time while delivering high separation efficiency, making it ideal for applications such as pelleting cells, separating subcellular components, purifying nucleic acids, and processing large volumes in industrial workflows. In biopharmaceutical manufacturing, fixed-angle rotors are favored for high-yield cell culture harvesting and protein isolation. Their robust design supports higher speeds and greater centrifugal forces compared to swinging-bucket rotors, making them suitable for a wide range of viscosities and densities. Industrial sectors, including food processing, chemical manufacturing, and wastewater treatment, are increasingly adopting these centrifuges for their durability and cost-effectiveness. Advances in rotor materials, such as corrosion-resistant alloys and lightweight composites, have enhanced performance and extended service life. Additionally, their compatibility with modern centrifuge systems featuring automated controls and enhanced safety mechanisms is driving demand. As industries prioritize speed, efficiency, and reliability, fixed-angle rotor centrifuges are becoming a preferred choice, fueling their rapid market growth.

"Fluid clarification segment to register the highest growth in the centrifuge market during the forecast period."

The fluid clarification segment is witnessing the fastest growth in the centrifuge market due to its critical role across industries requiring high-purity liquids. Fluid clarification involves the efficient removal of suspended solids, impurities, and other particulates from liquids, ensuring consistent quality and performance in downstream processes. This application is particularly vital in the food & beverage industry for juice, wine, and beer clarification; in pharmaceuticals for purifying active ingredients and injectable solutions; and in biotechnology for separating cell debris from valuable biomolecules. The chemical and petrochemical industries also rely on fluid clarification to maintain process efficiency and product integrity. The growing emphasis on regulatory compliance, product safety, and quality standards is driving adoption. Additionally, advances in centrifuge technology, such as high-speed, automated, and clean-in-place (CIP) systems, have enhanced clarification efficiency while reducing operational downtime. Expanding water treatment initiatives, especially in urban and industrial settings, are further boosting demand for centrifuges in fluid purification. Emerging economies, with their rising industrial output and stricter environmental regulations, are contributing significantly to this growth. As industries increasingly prioritize efficiency, sustainability, and precision, fluid clarification using centrifuges is becoming indispensable, securing its position as the fastest-growing application segment in terms of market value.

"Pharmaceutical industry to witness the fastest growth in the centrifuge market in terms of value during the forecast period."

The pharmaceutical industry is the fastest-growing end-use segment for the centrifuge market due to increasing global demand for medicines, vaccines, and biologics, driven by rising population, aging demographics, and the prevalence of chronic and infectious diseases. Centrifuges play a critical role in drug manufacturing, particularly in separation, purification, and clarification processes for active pharmaceutical ingredients (APIs), blood components, cell cultures, and biologics. The rapid growth of biopharmaceuticals and personalized medicine has further accelerated centrifuge adoption, especially high-speed and ultracentrifuges. Additionally, the COVID-19 pandemic highlighted the need for advanced centrifugation technologies for vaccine production and research. Stringent regulatory requirements and the shift toward continuous manufacturing in pharma have also driven investments in high-performance, automated centrifuges that ensure precision, sterility, and compliance. Emerging markets, such as India and China, are boosting pharmaceutical production capacity, creating significant opportunities for centrifuge manufacturers to cater to both large-scale and specialty drug manufacturing needs.

"Asia Pacific is projected to be the fastest-growing region in the centrifuge market, in terms of value, during the forecast period."

Asia Pacific is the fastest-growing region in the centrifuge market due to rapid industrialization, expanding manufacturing capacity, and significant investments in infrastructure and process industries. Countries like China, India, Japan, and South Korea are witnessing strong growth in pharmaceuticals, biotechnology, food and beverage, chemical processing, and wastewater treatment, all of which rely heavily on centrifuge technology. Rising healthcare needs, fueled by large populations and increasing disposable incomes, are boosting demand for pharmaceutical and bioprocessing centrifuges. Government initiatives for clean water, waste management, and environmental compliance are accelerating adoption in municipal and industrial wastewater treatment. Additionally, the Asia Pacific is becoming a hub for manufacturing and R&D, attracting global players to set up production facilities, thereby improving local availability and reducing costs. Competitive labor markets, favorable trade policies, and growing exports also contribute to market expansion. The region's robust economic growth, urban development, and industrial diversification establish it as the leading growth engine for the global centrifuge industry.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the centrifuge market, and information was gathered from secondary research to determine and verify the market size of several segments.

The centrifuge market comprises major players such as ALFA LAVAL (Sweden), GEA Group Aktiengesellschaft (Germany), ANDRITZ (Austria), FLSmidth A/S (Denmark), KUBOTA Corporation (Japan), Flottweg SE (Germany), SPX FLOW, Inc. (US), Mitsubishi Kakoki Kaisha, Ltd. (Japan), Ferrum AG (Switzerland), and SIEBTECHNIK GmbH (Germany). The study includes an in-depth competitive analysis of these key players in the centrifuge market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the centrifuge market by type, speed, rotor type, capacity, application, end-use industry, and region, and estimates the overall market value across various regions. It has also conducted a detailed analysis of key industry players to provide insights into their business overviews, products and services, key strategies, and expansions associated with the centrifuge market.

Key Benefits of Buying This Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the centrifuge market, high-growth regions, and market drivers, restraints, opportunities, and challenges.