아세트산메틸 시장 : 등급별, 순도별, 판매 채널별, 최종 이용 산업별, 지역별 - 예측(-2030년)

Methyl Acetate Market by Grade (Industrial grade, Pharmaceutical grade, and Food grade), Purity (= 99% Purity, 90-99% Purity, and < 90% purity), Sales Channel (Direct and Indirect), End-use Industry, and Region - Global Forecast to 2030

상품코드:1819105

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 247 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

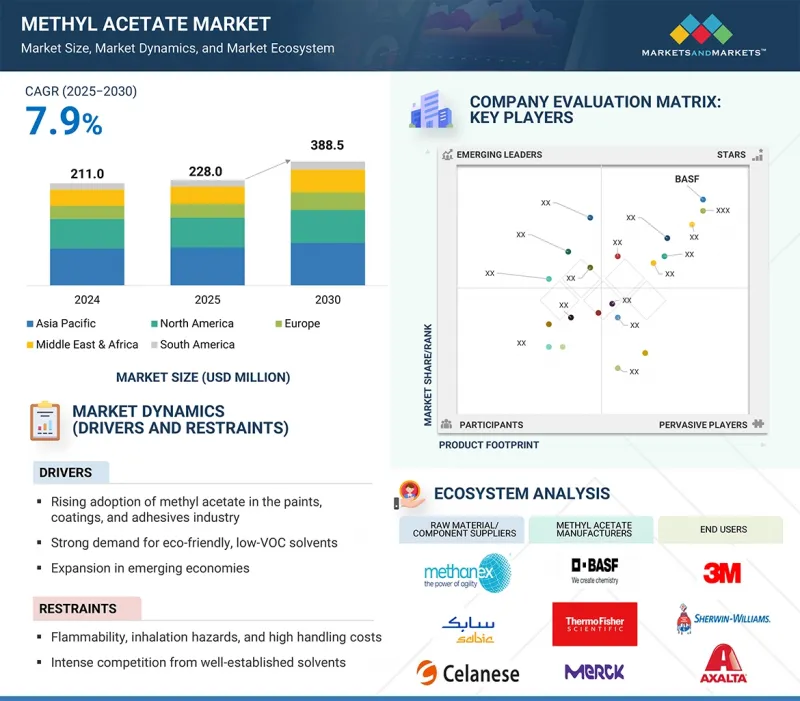

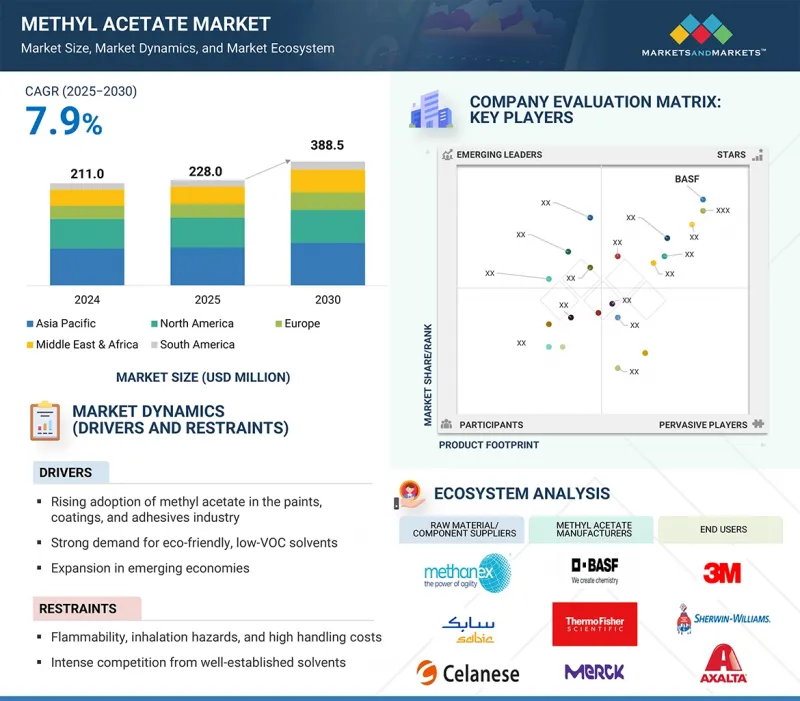

아세트산메틸 시장 규모는 2025년 2억 2,800만 달러에서 2030년에는 3억 8,850만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 7.9%로 전망됩니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러) 및 톤

부문

등급별, 순도별, 판매 채널별, 최종 이용 산업별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미

아세트산메틸의 수요는 빠른 기화 속도, 낮은 독성, 범용성이 높은 용매를 필요로 하는 다양한 산업에서 꾸준히 증가할 것으로 예상됩니다. 아세트산메틸은 페인트, 코팅제, 접착제, 실란트, 의약품, 전자제품, 퍼스널케어 등의 분야에서 까다로운 환경 및 성능 사양을 충족시키면서 높은 성능을 발휘합니다. 미국 환경보호청(EPA), 캘리포니아주 SCAQMD, 유럽화학제품청(ECHA) 등의 기관은 VOC 배출, 화학제품 안전, 환경 발자국에 대해 더욱 엄격한 규제를 부과하고 있습니다. 제조업체는 고순도, 저 VOC, 지속가능한 등급을 제공함으로써 지속가능한 처방 전략을 만족시켜 이 과제를 해결하고 있습니다.

최근 기술 혁신에는 용제 배합의 최적화, 습기에 민감한 배합 개발, 효율과 건조 시간 및 성능 향상을 가져오는 새로운 가공 기술 등이 포함됩니다. 아세트산메틸은 규제 적합성, 기술적 유연성, 지속가능성을 모두 갖추고 있어 많은 산업 분야에 적합한 제품입니다. 아세트산메틸은 고성능, 효율적이고 친환경적인 제조 공정을 보장하는 데 도움이 됩니다.

산업용 아세트산메틸은 높은 용해성, 빠른 증발 시간, 낮은 독성으로 알려져 있으며, 고성능의 친환경 용매를 요구하는 산업 제조 업계에서 널리 사용되고 있습니다. 산업용 아세트산메틸 분야는 규제적 지위도 고려되고 있으며, 지정된 VOC(휘발성 유기화합물) 규제가 중요한 용도나 성능과 지속가능/재생 가능한 솔루션의 균형을 찾는 것이 가장 중요한 산업 부문에 적합한 후보로 떠오르고 있습니다. 또한, 아세트산메틸이 유독성 용매를 안전하고 효과적으로 대체할 수 있는 전자, 건설, 자동차, 포장용도 등의 산업 분야에서도 수요가 증가하고 있습니다. 또한, 아세트산메틸은 성형 산업에서 사용되는 대부분의 수지 및 폴리머와 호환되므로 제품 배합에 아세트산메틸이 적합하여 범용성이 높아집니다. 이러한 위험한 용매를 지속적으로 대체할 수 있는 능력과 환경적으로 안전한 생산에 대한 요구가 높아지면서 2024년 산업용 아세트산메틸 부문이 세계 시장을 주도할 것으로 예상됩니다.

2024년 아세트산메틸 시장은 우수한 표면 마무리, 높은 용해도, 빠른 증발 속도, 낮은 독성으로 인해 페인트 및 코팅 분야가 지배적이었습니다. 자동차, 건축, 산업 분야에서 널리 사용되는 아세트산메틸은 원활한 도포, 빠른 건조, 도료의 내구성 향상을 용이하게 합니다. 아세트산메틸은 다양한 수지 및 안료와 함께 사용할 수 있어 배합에 유연성을 부여하고, VOC 규제를 엄격히 준수하여 기존 용매보다 친환경적입니다. 인프라 정비와 산업 성장에 따라 장식용 도료와 보호용 도료에 대한 수요가 증가함에 따라 이 분야의 우위가 높아지고 있습니다.

2024년 아시아태평양은 아세트산메틸 시장에서 우위를 확고히 하고, 첨단 산업 발전, 제조 공정의 증가, 페인트 및 코팅에서 접착제 및 의약품에 이르기까지 다양한 주요 최종 용도의 강력한 수요로 인해 그 역할을 강화했습니다. 중국, 인도, 일본, 한국은 아세트산메틸의 주요 생산 및 소비 거점으로서 선두를 달리고 있는 주요 국가 중 하나입니다. 이러한 역할은 대량의 원료를 쉽게 구할 수 있고, 비용 효율적인 제조 공정을 이용할 수 있으며, 산업 성장을 지원하기 위한 우호적인 정부 정책이 수립되어 있다는 점 등이 뒷받침되고 있습니다. 높은 도시화율과 광범위한 인프라 개발과 함께 접착제와 코팅제에 대한 수요가 증가하고 있습니다. 동시에 전자, 자동차, 포장 산업은 계속해서 용제 수요를 크게 견인하고 있습니다. 시장 확대는 고성능, 친환경 화학제품에 대한 투자 증가에 의해 뒷받침되고 있습니다. 아시아태평양은 생산의 지속적인 기계적 발전과 함께 최고 수준의 화학 제조업체의 존재로 인해 2024년 세계 아세트산메틸 시장에서 우위를 점할 것으로 예상됩니다.

대상 기업

BASF(독일), Thermo Fisher Scientific Inc.(미국), Merck KGaA(독일), Celanese Corporation(미국), Eastman Chemical Company(미국), Sekisui Chemical Industry(일본), Wacker Chemie AG(독일), Synthomer plc(영국), Anhui Wanwei Group(중국), Chang Chun Group(대만)을 망라하고 있습니다.

이 보고서는 아세트산메틸 시장을 등급별, 순도별, 순도별, 판매 채널별, 최종 이용 산업별, 지역별로 분류하고 있습니다. 이 보고서의 조사 범위는 아세트산메틸 시장의 성장에 영향을 미치는 촉진요인, 저해요인, 과제 및 기회에 대한 상세한 정보를 포함하고 있습니다. 주요 업계 참여업체를 상세히 분석하여 사업 개요, 제공 제품, 아세트산메틸 시장과 관련된 제휴, 협력, 합병, 인수, 인수, 사업 확장 등 주요 전략에 대한 인사이트를 제공합니다. 이 보고서는 아세트산메틸 시장 생태계에서 향후 신흥 기업의 경쟁 분석을 다루고 있습니다.

이 보고서는 시장 리더/신규 진입자에게 전체 아세트산메틸 시장 및 하위 부문의 수익 수에 대한 가장 가까운 근사치에 대한 정보를 제공합니다. 이해관계자들이 경쟁 상황을 이해하고, 사업을 더 잘 포지셔닝하기 위한 고민을 깊게 하고, 적절한 시장 진입 전략을 계획할 수 있도록 돕습니다. 이 보고서는 관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 저해요인, 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

소개

시장 역학

고객 비즈니스에 영향을 미치는 동향과 혼란

생태계 분석

밸류체인 분석

관세와 규제 상황

무역 분석

기술 분석

특허 분석

주요 회의와 이벤트

사례 연구 분석

투자와 자금 조달 시나리오

생성형 AI/AI가 아세트산메틸 시장에 미치는 영향

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 분석

2025년 미국 관세의 영향 : 아세트산메틸 시장

제6장 아세트산메틸 시장(등급별)

소개

산업 등급

의약품 등급

식품 등급

제7장 아세트산메틸 시장(순도별)

소개

순도 99% 이상

순도 90-99%

순도 90% 미만

제8장 아세트산메틸 시장(판매 채널별)

소개

직접

간접

제9장 아세트산메틸 시장(최종 이용 산업별)

소개

페인트 및 코팅

접착제 및 실란트

의약품

잉크

퍼스널케어·화장품

기타

제10장 아세트산메틸 시장(지역별)

소개

아시아태평양

중국

인도

일본

한국

기타

유럽

독일

프랑스

영국

스페인

기타

북미

미국

캐나다

멕시코

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

기타

제11장 경쟁 구도

개요

주요 진출 기업의 전략

시장 점유율 분석

매출 분석

기업 평가와 재무 지표

제품/브랜드 비교

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제12장 기업 개요

주요 진출 기업

BASF

THERMO FISHER SCIENTIFIC INC.

MERCK KGAA

CELANESE CORPORATION

EASTMAN CHEMICAL COMPANY

SEKISUI CHEMICAL CO., LTD.

WACKER CHEMIE AG

SYNTHOMER PLC

ANHUI WANWEI GROUP CO., LTD.

CHANG CHUN GROUP

기타 기업

DAICEL CORPORATION

SHANXI SANWEI GROUP CO, LTD.

KISHIDA CHEMICAL CO., LTD.

ATOM SCIENTIFIC LTD

HAIHANG INDUSTRY

CENTRAL DRUG HOUSE

LOBACHEMIE PVT. LTD.

DUBICHEM

NACALAI TESQUE, INC.

ARDIN CHEMICAL COMPANY

MOLEKULA GROUP

RECOCHEM CORPORATION

SCHARLAB S.L.

SIMSON PHARMA LIMITED

CHEMICAL IRAN

제14장 부록

KSM

영문 목차

영문목차

The methyl acetate market is estimated to reach USD 388.5 million by 2030 from USD 228.0 million in 2025, at a CAGR of 7.9% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (tons)

Segments

Grade, Purity, Sales Channel, End-use Industry, and Region

Regions covered

North America, Asia Pacific, Europe, the Middle East & Africa, and South America

The demand for methyl acetate is anticipated to continue to grow steadily due to a variety of industries requiring fast-evaporating, low-toxicity, and versatile solvents. Methyl acetate delivers high performance while conforming to rigid environmental and performance specifications for use in paints, coatings, adhesives, sealants, pharmaceuticals, electronics, and personal care. Organizations such as the US Environmental Protection Agency (EPA), California's SCAQMD, and the European Chemicals Agency (ECHA) are imposing more stringent regulations on VOC emissions, chemical safety, and environmental footprint. Manufacturers are stepping up to the challenge by providing high-purity, low-VOC, and sustainability grades that enable sustainable formulation strategies to satisfaction.

Recent innovations involve optimizing solvent blends, developing moisture-sensitive formulations, and new processing technologies that provide improved efficiency, drying times, and performance. Methyl acetate remains a viable product to many industrial sectors because of its combination of regulatory compliance, technical flexibility, and sustainability. Methyl acetate helps ensure high-performance, efficient, and environmentally friendly manufacturing processes.

"Industrial-grade accounted for the largest share in the methyl acetate market in 2024."

In 2024, the methyl acetate market's industrial grade segment led the market due to its significant usage in paints and coatings, adhesives, inks, and cleaning products. Industrial-grade methyl acetate is known to have high solubility, fast evaporation time, and low toxicity, and is widely used in industrial manufacturing, looking for high-performing and eco-friendly solvents. The industrial methyl acetate segment was also gaining consideration for its regulatory status, which has made it a suitable candidate for applications where specified VOC (volatile organic compound) restrictions are important, and for the industrial sector, where finding a balance between performance and sustainable/renewable solutions is paramount. Demand has also been increasing in industries such as electronics, construction, automotive, and packaging applications, where methyl acetate is a safe and effective substitution for toxic solvents. Additionally, the compatibility of methyl acetate with the product formulations adds to the versatility of the product because methyl acetate is compatible with most resins and polymers used in the molding industry. This ability to continuously replace hazardous solvents, coupled with a growing desire for environmentally safe production, was advantageous to the industrial-grade methyl acetate segment and its lead in the global market in 2024.

"The paints & coatings segment accounted for the largest share of the methyl acetate market in 2024."

The market for methyl acetate in 2024 was dominated by the paints & coatings sector because of its superior surface finishes, high solvency, rapid evaporation rate, and low toxicity. Methyl acetate, extensively utilized in automotive, construction, and industrial sectors, facilitates seamless application, rapid drying, and enhanced durability of coatings. It can work with a large variety of resins and pigments, adding flexibility to formulations and rigorous adherence to VOC regulations, making it more environmentally friendly than conventional solvents. The growing demand for decorative and protective coatings, as a result of infrastructure development and industrial growth, has reinforced this segment's dominance. Continuous innovation in coating formulations will continue to allow for the use of methyl acetate in several global end-use segments.

"Asia Pacific dominated the regional market for methyl acetate in 2024."

During the year 2024, the Asia Pacific region solidified its dominance in the market for methyl acetate, a role spurred by high levels of industrial development, the rise in manufacturing processes, and a strong demand from major end-use applications whose range spans from paints and coatings to adhesives and pharmaceuticals. China, India, Japan, and South Korea are among the major countries that have risen to a frontline position as major manufacturing and consumption centers for methyl acetate. This role has been supported intensely by the ready availability of huge quantities of raw materials, the availability of cost-effective manufacturing processes, and the formulation of friendly government policies aimed at helping the growth of industry. The high levels of urbanization rates, coupled with wide infrastructure development, have also boosted the demand for adhesives and coatings. At the same time, the electronics, automotive, and packaging industries continue to drive their demand for solvents significantly. The market expansion has also been supported by increasing investments in high-performance, more environmentally friendly chemicals. Asia Pacific solidified their dominance of the global methyl acetate market in 2024 with the presence of top chemical producers, along with continued mechanical advances in production.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa: 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: > USD 1 Billion; Tier 2: USD 500 million to USD 1 Billion; and Tier 3: < USD 500 million

Companies Covered: BASF (Germany), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Celanese Corporation (US), Eastman Chemical Company (US), Sekisui Chemical Co., Ltd. (Japan), Wacker Chemie AG (Germany), Synthomer plc (UK), Anhui Wanwei Group Co., Ltd. (China), and Chang Chun Group (Taiwan) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the methyl acetate market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the methyl acetate market based on grade (Industrial Grade, Pharmaceutical Grade, and Food Grade), purity (>= 99% purity, 90-99% purity, < 90% purity), sales channel (Direct and Indirect), end-use industry (Paints and Coatings, Adhesives and Sealants, Pharmaceuticals, Inks, Personal Care and Cosmetics, and Other endues industries) and Region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the methyl acetate market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, mergers, acquisitions, and expansions, associated with the methyl acetate market. This report covers a competitive analysis of upcoming startups in the methyl acetate market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall methyl acetate market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (rising adoption of methyl acetate in the paints, coatings, and adhesives industry, strong demand for eco-friendly, low-VOC solvents, and expansion in emerging economies), restraints (flammability, inhalation hazards & high handling costs, and Intense competition from well-established solvents), opportunities (expanding applications across high-growth industries and growth through bio-based and circular economy integration), and challenges (stringent regulatory compliance across regions and escalating production costs driven by feedstock volatility and energy intensity).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the methyl acetate market.

Market Development: Comprehensive information about profitable markets-the report analyzes the methyl acetate market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the methyl acetate market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as BASF (Germany), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Celanese Corporation (US), Eastman Chemical Company (US), Sekisui Chemical Co., Ltd. (Japan), Wacker Chemie AG (Germany), Synthomer plc (UK), Anhui Wanwei Group Co., Ltd. (China), and Chang Chun Group (Taiwan), among others.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.3 BASE NUMBER CALCULATION

2.3.1 DEMAND-SIDE APPROACH

2.3.2 SUPPLY-SIDE APPROACH

2.4 MARKET FORECAST APPROACH

2.4.1 SUPPLY SIDE

2.4.2 DEMAND SIDE

2.5 DATA TRIANGULATION

2.6 FACTOR ANALYSIS

2.7 RESEARCH ASSUMPTIONS

2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METHYL ACETATE MARKET

4.2 ASIA PACIFIC: METHYL ACETATE MARKET, BY GRADE AND COUNTRY

4.3 METHYL ACETATE MARKET, BY GRADE

4.4 METHYL ACETATE MARKET, BY END-USE INDUSTRY

4.5 METHYL ACETATE MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rise in adoption of methyl acetate in paints, coatings, and adhesives

5.2.1.2 Strong demand for eco-friendly, low-VOC solvents

5.2.1.3 Expansion in emerging economies

5.2.2 RESTRAINTS

5.2.2.1 Flammability, inhalation hazards, and high handling costs

5.2.2.2 Intense competition from well-established solvents

5.2.3 OPPORTUNITIES

5.2.3.1 Expanding applications across high-growth industries

5.2.3.2 Growth through bio-based and circular economy integration

5.2.4 CHALLENGES

5.2.4.1 Stringent regulatory compliance across regions

5.2.4.2 Escalating production costs driven by feedstock volatility and energy intensity

5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 ECOSYSTEM ANALYSIS

5.5 VALUE CHAIN ANALYSIS

5.6 TARIFF AND REGULATORY LANDSCAPE

5.6.1 TARIFF ANALYSIS (HS CODE: 291539)

5.6.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.6.3 KEY REGULATIONS

5.6.3.1 REACH Regulation (EC 1907/2006)

5.6.3.2 OSHA - Hazard Communication Standard (29 CFR 1910.1200)

5.6.3.3 GHS - Globally Harmonized System of Classification and Labelling of Chemicals

5.6.3.4 Clean Air Act (CAA) - US EPA (40 CFR Part 60 & 63

5.6.4 PRICING ANALYSIS

5.6.4.1 Pricing analysis based on grade

5.6.4.2 Pricing analysis based on region

5.7 TRADE ANALYSIS

5.7.1 EXPORT SCENARIO (HS CODE 291539)

5.7.2 IMPORT SCENARIO (HS CODE 291539)

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Reactive distillation (RD)

5.8.1.2 Carbonylation of dimethyl ether (DME)

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Microwave-assisted esterification

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Enzyme-based formulations

5.9 PATENT ANALYSIS

5.9.1 INTRODUCTION

5.9.2 METHODOLOGY

5.10 KEY CONFERENCES AND EVENTS

5.11 CASE STUDY ANALYSIS

5.11.1 SCCNFP SAFETY EVALUATION OF METHYL ACETATE IN NAIL POLISH REMOVERS

5.11.2 USING DYNAMIC FLOWSHEET DIVA(R) SIMULATOR FOR MODELING METHYL ACETATE REACTIVE DISTILLATION PROCESS

5.11.3 ACUTE METHYL ACETATE POISONING IN FABRIC PROCESSING WORKSHOP (CHINA)

5.12 INVESTMENT AND FUNDING SCENARIO

5.13 IMPACT OF GEN AI/AI ON METHYL ACETATE MARKET

5.13.1 INTRODUCTION

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 THREAT OF NEW ENTRANTS

5.14.2 THREAT OF SUBSTITUTES

5.14.3 BARGAINING POWER OF SUPPLIERS

5.14.4 BARGAINING POWER OF BUYERS

5.14.5 INTENSITY OF COMPETITIVE RIVALRY

5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 BUYING CRITERIA

5.16 MACROECONOMIC ANALYSIS

5.16.1 INTRODUCTION

5.16.2 GDP TRENDS AND FORECASTS

5.17 IMPACT OF 2025 US TARIFF: METHYL ACETATE MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRY/REGION

5.17.4.1 US

5.17.4.2 China

5.17.4.3 India

5.17.5 END-USE INDUSTRY IMPACT

6 METHYL ACETATE MARKET, BY GRADE

6.1 INTRODUCTION

6.2 INDUSTRIAL GRADE

6.2.1 VERSATILE SOLVENT FOR COATINGS, ADHESIVES, AND CHEMICAL SYNTHESIS

6.3 PHARMACEUTICAL GRADE

6.3.1 HIGH-PURITY SOLVENT FOR DRUG FORMULATION AND SYNTHESIS

6.4 FOOD GRADE

6.4.1 SAFE, REGULATED SOLVENT FOR FLAVORING AND FOOD PROCESSING

7 METHYL ACETATE MARKET, BY PURITY

7.1 INTRODUCTION

7.2 >= 99% PURITY

7.2.1 HIGH-PURITY METHYL ACETATE MEETS STRINGENT STANDARDS FOR SPECIALTY AND HIGH-VALUE APPLICATIONS

7.3 90-99% PURITY

7.3.1 INDUSTRIAL-GRADE METHYL ACETATE SUPPORTS MASS-MARKET PRODUCTION NEEDS

7.4 < 90% PURITY

7.4.1 TECHNICAL-GRADE METHYL ACETATE OFFERS COST-EFFICIENT SOLUTION FOR BLENDED APPLICATIONS

8 METHYL ACETATE MARKET, BY SALES CHANNEL

8.1 INTRODUCTION

8.2 DIRECT

8.2.1 LARGE-SCALE INDUSTRIAL CONSUMPTION TO DRIVE DEMAND FOR DIRECT SUPPLY AGREEMENTS

8.3 INDIRECT

8.3.1 DISTRIBUTION NETWORKS EXPAND MARKET REACH AND FLEXIBILITY FOR SMALLER BUYERS

9 METHYL ACETATE MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 PAINTS & COATINGS

9.2.1 RISE IN ENVIRONMENTAL REGULATIONS AND DEMAND FOR LOW-VOC SOLVENTS TO PROPEL METHYL ACETATE USE

9.3 ADHESIVES & SEALANTS

9.3.1 STRINGENT VOC REGULATIONS AND DEMAND FOR FAST-CURING ADHESIVES TO DRIVE METHYL ACETATE ADOPTION

9.4 PHARMACEUTICALS

9.4.1 REGULATORY COMPLIANCE AND SAFETY TO DRIVE METHYL ACETATE USE IN PHARMACEUTICAL MANUFACTURING

9.5 INKS

9.5.1 ABILITY TO ADVANCE SUSTAINABLE AND SAFE INK PRODUCTION WITH METHYL ACETATE SOLVENT TO FUEL SEGMENT GROWTH

9.6 PERSONAL CARE & COSMETICS

9.6.1 RISE IN CONSUMER DEMAND FOR SAFE AND SUSTAINABLE COSMETICS TO DRIVE METHYL ACETATE ADOPTION

9.7 OTHER END-USE INDUSTRIES

10 METHYL ACETATE MARKET, BY REGION

10.1 INTRODUCTION

10.2 ASIA PACIFIC

10.2.1 CHINA

10.2.1.1 Industrial renaissance and pharmaceutical expansion to drive methyl acetate demand

10.2.2 INDIA

10.2.2.1 Expanding pharmaceutical, cosmetics, and automotive industries to propel methyl acetate demand

10.2.3 JAPAN

10.2.3.1 Industrial innovation and environmental standards to boost demand

10.2.4 SOUTH KOREA

10.2.4.1 Emerging electronics and automotive growth to underpin methyl acetate market expansion

10.2.5 REST OF ASIA PACIFIC

10.3 EUROPE

10.3.1 GERMANY

10.3.1.1 Industrial innovation and automotive strength to fuel sustainable solvent demand

10.3.2 FRANCE

10.3.2.1 Sustainability and innovation in France's pharmaceuticals and cosmetics sector to boost methyl acetate demand

10.3.3 UK

10.3.3.1 Sustainable manufacturing and innovation to elevate methyl acetate adoption

10.3.4 SPAIN

10.3.4.1 Rise in pharmaceutical innovation and strong cosmetics market to fuel demand for sustainable solvents

10.3.5 REST OF EUROPE

10.4 NORTH AMERICA

10.4.1 US

10.4.1.1 Regulatory exemption and expanding industrial demand to drive market

10.4.2 CANADA

10.4.2.1 Eco-friendly manufacturing and regulatory alignment to fuel demand

10.4.3 MEXICO

10.4.3.1 Growth anchored in construction, manufacturing, and sustainable industrial practices to drive adoption of methyl acetate

10.5 MIDDLE EAST & AFRICA

10.5.1 GCC COUNTRIES

10.5.1.1 Saudi Arabia

10.5.1.1.1 Industrial diversification to support methyl acetate applications

10.5.1.2 UAE

10.5.1.2.1 Expanding industrial base and pharmaceutical sector to drive demand

10.5.1.3 Rest of GCC Countries

10.5.2 SOUTH AFRICA

10.5.2.1 Industrial growth and regulatory shifts to fuel safer, high-performance solvent adoption

10.5.3 REST OF MIDDLE EAST & AFRICA

10.6 SOUTH AMERICA

10.6.1 BRAZIL

10.6.1.1 Industrial diversification and manufacturing growth to propel methyl acetate demand

10.6.2 ARGENTINA

10.6.2.1 Industrial resilience and automotive activity to sustain methyl acetate demand

10.6.3 REST OF SOUTH AMERICA

11 COMPETITIVE LANDSCAPE

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES

11.3 MARKET SHARE ANALYSIS

11.4 REVENUE ANALYSIS

11.5 COMPANY VALUATION AND FINANCIAL METRICS

11.5.1 COMPANY VALUATION

11.5.2 FINANCIAL METRICS

11.6 PRODUCT/BRAND COMPARISON

11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.7.1 STARS

11.7.2 EMERGING LEADERS

11.7.3 PERVASIVE PLAYERS

11.7.4 PARTICIPANTS

11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.7.5.1 Company footprint

11.7.5.2 Regional footprint

11.7.5.3 Grade footprint

11.7.5.4 Purity footprint

11.7.5.5 Sales channel footprint

11.7.5.6 End-use industry footprint

11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024