Coil Coatings Market by Type (Polyester, Fluropolymer, and Others), Application (Steel & Aluminum), End-use Industry (Building & Construction, Automotive, and Other End-use Industries), and Region - Global Forecast to 2030

상품코드:1819096

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 231 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

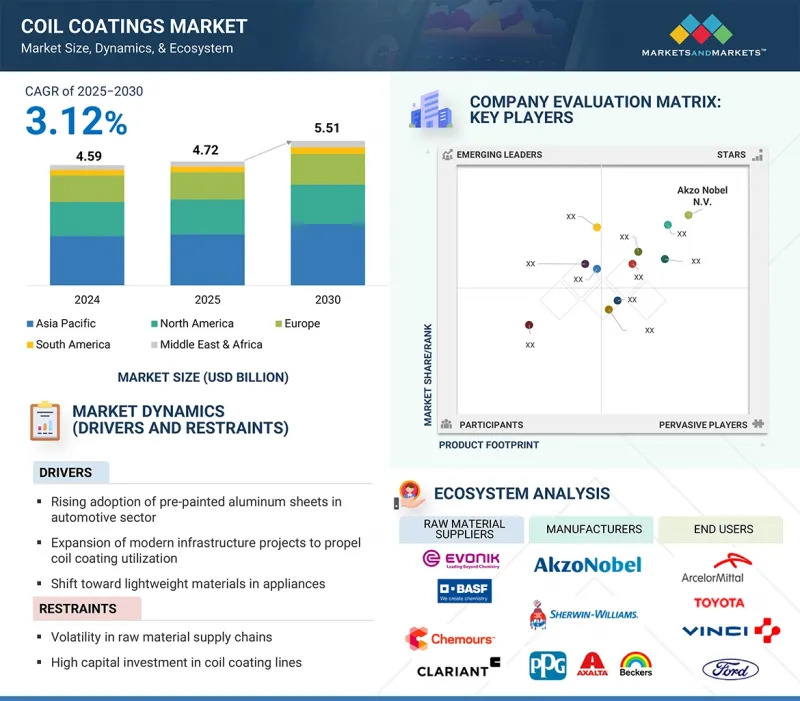

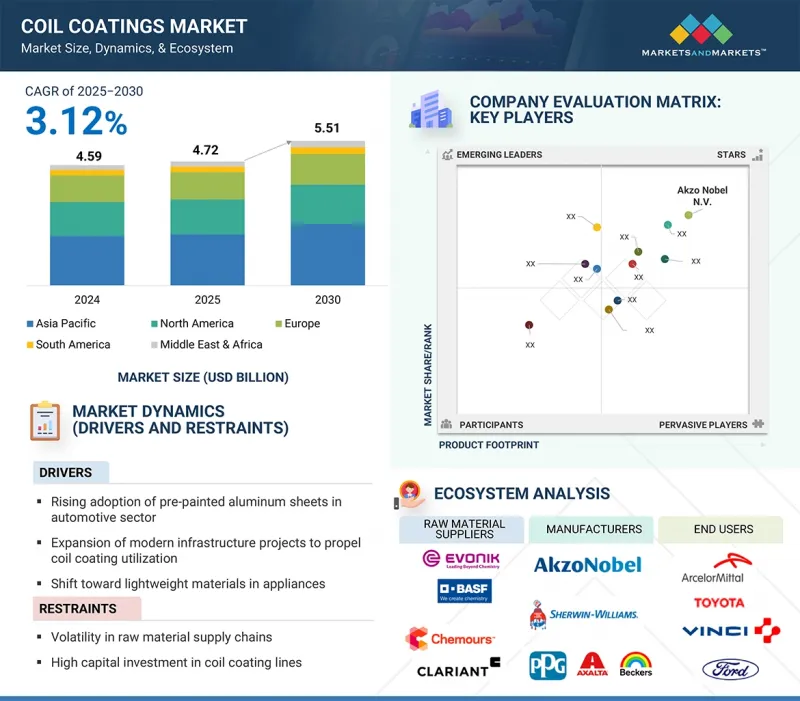

세계의 코일 코팅 시장 규모는 건축·건설, 자동차, 가전, 산업 기기 분야에서의 수요 확대에 의해 예측 기간 동안 CAGR 3.12%를 기록할 것으로 전망되며, 2025년 47억 2,000만 달러에서 2030년에는 55억 1,000만 달러에 달할 것으로 예측됩니다.

코일 코팅은 금속 제품에 내식성, 장수명, 미관을 부여하는 데 필수적이며, 제품 수명 연장 및 유지보수 비용 절감에 필수적입니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 유닛

금액(100만 달러) 및 킬로톤

부문

유형별, 용도별, 최종 이용 산업별, 지역별

대상 지역

아시아태평양, 서유럽, 중유럽 및 동유럽, 북미, 중동 및 아프리카, 남미

환경 규제 변화에 대응하기 위해 산업계가 저 VOC, 에너지 효율, 재활용 가능한 페인트로 전환함에 따라 지속가능성에 대한 관심이 높아지고 있습니다. 또한, 건축 구조물 및 자동차의 경량 도장 금속의 적용 확대도 코일 도료의 채택을 촉진하고 있습니다. 이처럼 내구성, 지속가능성, 국제 규제 준수에 대한 중요성이 강조되면서 코일 페인트는 다양한 산업에서 효율성과 장기적인 가치를 실현하는 중요한 요소 중 하나가 되고 있습니다.

플루오로폴리머 코일 코팅은 2024년 세계 코일 코팅 시장에서 금액 기준으로 2위를 차지했습니다. 이는 내후성, 내 자외선성, 색상 유지력이 우수하기 때문입니다. 불소수지 페인트는 외관, 지붕, 커튼월과 같은 고품질 건축 용도에 사용되는 가장 일반적인 페인트 중 하나입니다. 폴리에스테르 도료에 비해 비용면에서는 비싸지만 가혹한 환경에서 타의 추종을 불허하는 성능을 발휘하는 것이 강력한 수요의 배경입니다.

2024년 세계 코일 코팅 시장의 금액 기준으로 가장 큰 용도는 건축 구조물, 전자제품, 산업 구체 및 기타 분야에서 널리 사용되기 때문에 철강으로 나타났습니다. 코일코팅강은 내구성, 내식성, 비용 효율성으로 인해 지붕재, 벽재, 건축 구조재에 일반적으로 사용됩니다. 기능성과 미적 감각을 효과적으로 결합할 수 있기 때문에 철강은 많은 산업 분야에서 코일 코팅 응용 분야에서 선호되는 기판이 되었습니다.

2024년 세계 코일 코팅 시장에서 자동차 산업은 금액 기준으로 두 번째로 큰 최종 이용 산업이었습니다. 이는 업계가 경량화, 긴 수명, 우수한 마감재에 중점을 두고 있기 때문입니다. 코일 코팅 금속은 패널, 인테리어 트림, 방열판과 같은 자동차 부품에 많이 사용되며, 제조업체에 비용 절감, 내식성, 설계 유연성을 제공합니다. 전기자동차의 보급과 내후성 및 외관을 개선한 고성능 도료에 대한 수요는 업계의 코일 도료 의존도를 더욱 강화하고 있으며, 자동차는 건설 산업에 이어 주요 촉진요인으로 작용하고 있습니다.

북미는 코일 코팅 시장에서 금액 기준으로 두 번째로 큰 지역입니다. 이러한 성장은 주거 및 상업 인프라에 대한 투자 증가와 에너지 효율적이고 내구성이 뛰어난 건축자재에 대한 수요 증가에 의해 주도되고 있습니다. 또한, PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd. 등의 대형 코일 도료 제조업체가 존재함으로써 기술 발전을 촉진하고 고성능 도료의 안정적인 공급을 보장하고 있습니다.

세계의 코일 코팅 시장에 대해 조사했으며, 유형별, 용도별, 최종 이용 산업별, 지역별 동향, 시장 진입 기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

소개

시장 역학

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 지표

제6장 업계 동향

공급망 분석

가격 분석

고객 비즈니스에 영향을 미치는 동향/혼란

생태계 분석

기술 분석

사례 연구 분석

무역 분석

규제 상황

2025-2026년의 주요 회의와 이벤트

투자와 자금 조달 시나리오

특허 분석

2025년 미국 관세의 영향

AI/생성형 AI가 코일 코팅 시장에 미치는 영향

제7장 코일 코팅 시장(유형별)

소개

폴리에스테르

불소수지

기타

제8장 코일 코팅 시장(용도별)

소개

강철

알루미늄

제9장 코일 코팅 시장(최종 이용 산업별)

소개

건축·건설

자동차

기타

제10장 코일 코팅 시장(지역별)

소개

아시아태평양

중국

일본

인도

한국

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

스페인

이탈리아

중동 및 아프리카

GCC 국가

남아프리카공화국

남미

브라질

아르헨티나

제11장 경쟁 구도

소개

주요 진출 기업의 전략/강점

시장 점유율 분석

매출 분석

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

브랜드/제품 비교 분석

기업 평가와 재무 지표

경쟁 시나리오

제12장 기업 개요

주요 진출 기업

AKZO NOBEL N.V.

AXALTA COATING SYSTEMS LTD.

PPG INDUSTRIES, INC.

THE SHERWIN-WILLIAMS COMPANY

BECKERS GROUP

NIPPON PAINT HOLDINGS CO., LTD

KANSAI PAINT CO., LTD.

KCC CORPORATION

JSW PAINTS

YUNG CHI PAINT & VARNISH MFG. CO., LTD

기타 기업

CLOVERDALE PAINT INC.

SALCHI METALCOAT S.R.L.

CONTINENTAL COATINGS

REPLASA ADVANCED MATERIALS, S. A.

ALCEA S.P.A.

TITAN COATINGS, INC.

SPECTRUM INDUSTRIES LLC

DYO BOYA FABRIKALARI SANAYI VE TICARET A.S.

HUEHOCO

METALCOLOR SA

UNIVERSAL CHEMICALS & COATINGS INC.

BHIMRAJKA MADER COATINGS PVT. LTD.

NOROO COIL COATINGS CO., LTD.

BRILLUX INDUSTRIAL COATINGS

PERFECT INDUSTRIES GROUP HOLDINGS LTD.

제13장 인접 시장과 관련 시장

제14장 부록

KSM

영문 목차

영문목차

The global coil coatings market size is projected to reach USD 5.51 billion by 2030 from USD 4.72 billion in 2025, at a CAGR of 3.12% during the forecast period, due to the growing demand across building & construction, automotive, appliances, and industrial equipment sectors. Coil coatings are essential for providing corrosion resistance, longevity, and aesthetic appeal to metal products, making them crucial for extending product life and reducing maintenance costs.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Type, Application, End-use Industry, and Region

Regions covered

Asia Pacific, Western Europe, Central & Eastern Europe, North America, Middle East & Africa, and South America

The focus on sustainability is growing as industries shift to low-VOC, energy-efficient, and recyclable coatings to address the changing environmental regulations. In addition, increasing applications of lightweight, pre-painted metals in building structures and automobiles are also encouraging the adoption of coil coatings. This high emphasis on durability, sustainability, and adhering to international regulations is making coil coatings one of the key enablers of efficiencies and long-term value in various industries.

"Fluropolymer segment accounted for the second-largest share of the coil coatings market in 2024."

Fluorpolymer coil coatings hold the second-largest share of the global coil coatings market, in terms of value, in 2024. This is fueled by their high resistance to weather, UV, and long-lasting color retention. Fluoropolymer coatings are one of the most popular coatings used in high-quality architectural applications like facades, roofing, and curtain walls. Though expensive in terms of cost when compared with polyester coatings, their unrivaled performance in severe environments has been the reason behind the strong demand.

"Steel was the largest application of the global coil coatings market in terms of value in 2024."

The largest application of the global coil coatings market in 2024, in value terms, was steel due to its wide use in building structures, electronic appliances, industry spheres, and other sectors. Coil-coated steel is commonly used in roofing systems, wall cladding, and structural materials for buildings due to its durability, corrosion resistance, and cost-effectiveness. Its ability to effectively combine functionality with aesthetic appeal makes steel the preferred substrate for coil coating applications in many industries.

"Automotive accounted for the second-largest share of the coil coatings market, in terms of value, in 2024."

The automobile sector was the second-largest end-use industry in the global coil coatings market, in terms of value, in 2024. This is largely due to the industry's focus on weight saving, long life, and superior finishes. Coil-coated metals are being used more on vehicle parts like panels, interior trim, and heat shields, providing manufacturers with cost savings, corrosion resistance, and design flexibility. Increased use of electric vehicles and demand for high-performance coatings with enhanced weatherability and appearance further consolidated the industry's dependence on coil coatings, making automotive a major growth driver following the construction industry.

"North America was the second-largest region in the coil coatings market, in terms of value, in 2024."

North America is the second-largest region in the coil coatings market in terms of value. This growth is propelled by increasing investments in residential and commercial infrastructure and the rising demand for energy-efficient and durable building materials. Additionally, the presence of major coil coating manufacturers such as PPG Industries, Inc., The Sherwin-Williams Company, and Axalta Coating Systems Ltd. fosters technological advancements and ensures a steady supply of high-performance coatings.

By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

By Designation: Directors - 50%, Managers - 30%, and Others - 20%

By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, and Rest of the World - 5%

The key players profiled in the report include Akzo Nobel N.V. (Netherlands), Axalta Coating Systems Ltd. (US), PPG Industries, Inc. (US), The Sherwin-Williams Company (US), Beckers Group (Germany), Nippon Paint Holdings Co., Ltd (Japan), Kansai Paint Co., Ltd. (Japan), KCC Corporation (South Korea), JSW Paints (India), and Yung Chi Paint & Varnish Manufacturing Co., Ltd. (Taiwan).

Research Coverage

This report segments the market for coil coatings based on type, application, end-use industry, and region, and provides estimations of value (USD million) for the overall market size across various regions. It has also conducted a detailed analysis of key industry players to provide insights into their business overviews, services, and key strategies associated with the market for coil coatings.

Reasons to Buy This Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the coil coatings market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights into the following points:

Market Penetration: Comprehensive information on coil coatings offered by top players in the global market.

Analysis of Market Dynamics: Drivers (rising adoption of pre-painted aluminum sheets in automotive, expansion of modern infrastructure projects to propel coil coating utilization, and shift toward lightweight materials in appliances), restraints (volatility in raw material supply chains and high capital investment in coil coating lines), opportunities (rising adoption in solar panels and growing preference for green buildings), and challenges (adapting coil coatings to extreme climate conditions) influencing the growth of the coil coatings market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the coil coatings market.

Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for coil coating across regions.

Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global coil coatings market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the coil coatings market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key primary participants

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 GROWTH FORECAST

2.4.1 SUPPLY-SIDE ANALYSIS

2.4.2 DEMAND-SIDE ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN COIL COATINGS MARKET

4.2 COIL COATINGS MARKET, BY REGION

4.3 ASIA PACIFIC COIL COATINGS MARKET, BY END-USE INDUSTRY AND COUNTRY

4.4 COIL COATINGS MARKET, TYPE VS. REGION

4.5 COIL COATINGS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising adoption of pre-painted aluminum sheets in automotive sector

5.2.1.2 Expansion of modern infrastructure projects

5.2.1.3 Shift toward lightweight materials in appliance industry

5.2.2 RESTRAINTS

5.2.2.1 Volatility in raw material supply chains

5.2.2.2 High capital investment in coil coating lines

5.2.3 OPPORTUNITIES

5.2.3.1 Rising adoption in solar industry

5.2.3.2 Growing preference for green buildings

5.2.4 CHALLENGES

5.2.4.1 Failure in adapting to extreme climatic conditions

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 THREAT OF SUBSTITUTES

5.3.2 THREAT OF NEW ENTRANTS

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GDP TRENDS AND FORECAST

6 INDUSTRY TRENDS

6.1 SUPPLY CHAIN ANALYSIS

6.2 PRICING ANALYSIS

6.2.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION, 2024

6.2.2 AVERAGE SELLING PRICE TREND, BY REGION

6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.4 ECOSYSTEM ANALYSIS

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGIES

6.5.1.1 Polyester coil coatings

6.5.1.2 Fluoropolymer coil coatings

6.5.2 COMPLIMENTARY TECHNOLOGIES

6.5.2.1 Functional additives and pigment technologies

6.5.2.2 AI-driven process controls

6.6 CASE STUDY ANALYSIS

6.6.1 SUSTAINABLE FACADE WITH BECKERS COIL COATINGS

6.6.2 FLUROPON FINISH DELIVERS PERFORMANCE AND HERITAGE DESIGN

6.6.3 CUSTOM COIL-APPLIED EPOXY COATINGS FOR DECORATIVE METAL COMPONENTS

6.7 TRADE ANALYSIS

6.7.1 IMPORT SCENARIO (HS CODE 721240)

6.7.2 EXPORT SCENARIO (HS CODE 721240)

6.8 REGULATORY LANDSCAPE

6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.8.2 REGULATORY FRAMEWORK

6.8.2.1 ISO 14001: Environmental management systems

6.8.2.2 ISO 9001: Quality management systems

6.9 KEY CONFERENCES AND EVENTS, 2025-2026

6.10 INVESTMENT AND FUNDING SCENARIO

6.11 PATENT ANALYSIS

6.11.1 APPROACH

6.11.2 DOCUMENT TYPES

6.11.3 TOP APPLICANTS

6.11.4 JURISDICTION ANALYSIS

6.12 IMPACT OF 2025 US TARIFF

6.12.1 INTRODUCTION

6.12.2 KEY TARIFF RATES

6.12.3 PRICE IMPACT ANALYSIS

6.12.4 IMPACT ON KEY COUNTRIES/REGIONS

6.12.4.1 US

6.12.4.2 Europe

6.12.4.3 Asia Pacific

6.12.5 IMPACT ON END-USE INDUSTRIES

6.13 IMPACT OF AI/GEN AI ON COIL COATINGS MARKET

7 COIL COATINGS MARKET, BY TYPE

7.1 INTRODUCTION

7.2 POLYESTER

7.2.1 ENHANCED DURABILITY AND COST EFFICIENCY TO BOOST DEMAND

7.3 FLUOROPOLYMER

7.3.1 EXCELLENT CHEMICAL RESISTANCE TO DRIVE MARKET

7.4 OTHER TYPES

8 COIL COATINGS MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 STEEL

8.2.1 GROWING INDUSTRIAL USE OF STEEL TO BOOST DEMAND

8.3 ALUMINUM

8.3.1 RISING USE OF LIGHTWEIGHT ALUMINUM TO DRIVE MARKET

9 COIL COATINGS MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 BUILDING & CONSTRUCTION

9.2.1 INFRASTRUCTURE EXPANSION TO BOOST DEMAND

9.3 AUTOMOTIVE

9.3.1 INNOVATION IN VEHICLE DESIGN TO PROPEL DEMAND

9.4 OTHER END-USE INDUSTRIES

10 COIL COATINGS MARKET, BY REGION

10.1 INTRODUCTION

10.2 ASIA PACIFIC

10.2.1 CHINA

10.2.1.1 Strong domestic automobile manufacturing and rising electric vehicle production to fuel demand

10.2.2 JAPAN

10.2.2.1 Rising consumer demand for modern appliances and electronics to drive market

10.2.3 INDIA

10.2.3.1 Rapid industrialization to drive demand

10.2.4 SOUTH KOREA

10.2.4.1 Government-led initiatives for supporting sustainable construction and modernization of infrastructure to drive market

10.3 NORTH AMERICA

10.3.1 US

10.3.1.1 Strong industrial landscape to fuel market growth

10.3.2 CANADA

10.3.2.1 Focus on advanced research and development to drive demand

10.3.3 MEXICO

10.3.3.1 Rising demand for household appliances with durable and aesthetic finishes to drive market

10.4 EUROPE

10.4.1 GERMANY

10.4.1.1 Automotive industry leadership to boost market

10.4.2 FRANCE

10.4.2.1 Rising consumer preference for premium home appliances to drive market

10.4.3 UK

10.4.3.1 Stringent regulatory framework emphasizing safety, sustainability, and environmental responsibility to propel market

10.4.4 SPAIN

10.4.4.1 Growth in residential and commercial renovation activities to propel demand

10.4.5 ITALY

10.4.5.1 Growing adoption of energy-efficient building materials to drive market

10.5 MIDDLE EAST & AFRICA

10.5.1 GCC COUNTRIES

10.5.1.1 Saudi Arabia

10.5.1.1.1 Growth in large-scale building and construction projects to fuel demand

10.5.2 SOUTH AFRICA

10.5.2.1 Rising automobile manufacturing and component production to drive market

10.6 SOUTH AMERICA

10.6.1 BRAZIL

10.6.1.1 Economic growth to drive adoption

10.6.2 ARGENTINA

10.6.2.1 Increasing furniture manufacturing supported by design-driven demand to propel market

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3 MARKET SHARE ANALYSIS

11.4 REVENUE ANALYSIS

11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.5.1 STARS

11.5.2 EMERGING LEADERS

11.5.3 PERVASIVE PLAYERS

11.5.4 PARTICIPANTS

11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.5.5.1 Company footprint

11.5.5.2 Region footprint

11.5.5.3 Type footprint

11.5.5.4 Application footprint

11.5.5.5 End-use industry footprint

11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024