헤드업 디스플레이(HUD) 시장 : 컴바이너 HUD, 윈드실드 HUD, 웨어러블 HUD, AR HUD, 기존 HUD, 디스플레이 유닛, 비디오 제너레이터/프로세싱 유닛, 프로젝터/프로젝션 유닛 - 예측(-2030년)

Head-up Display (HUD) Market by Combiner HUD, Windshield HUD, Wearable HUD, Augmented Reality (AR) HUD, Conventional HUD, Display Unit, Video Generator/Processing Unit, and Projector/ Projection Unit - Global Forecast to 2030

상품코드:1819095

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 240 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

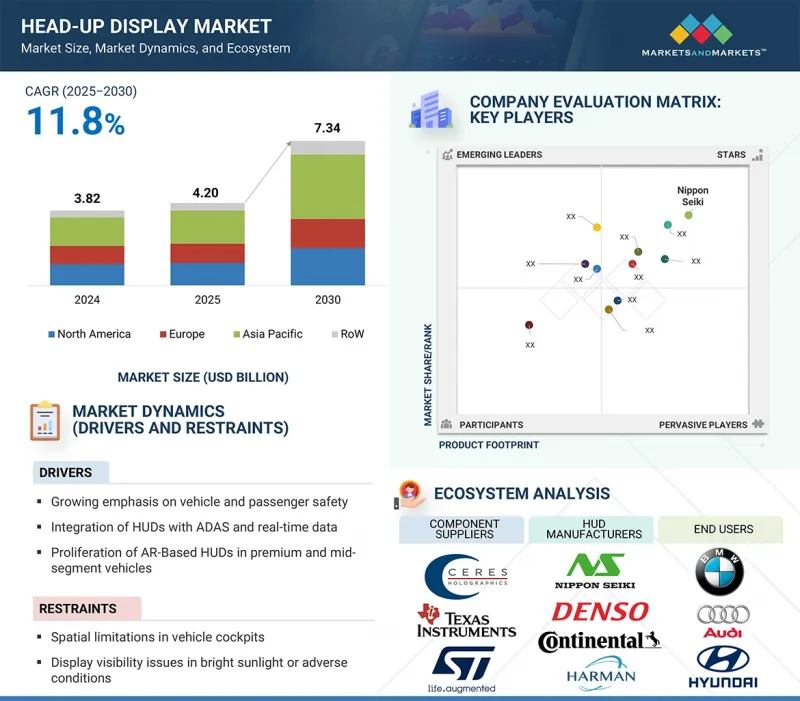

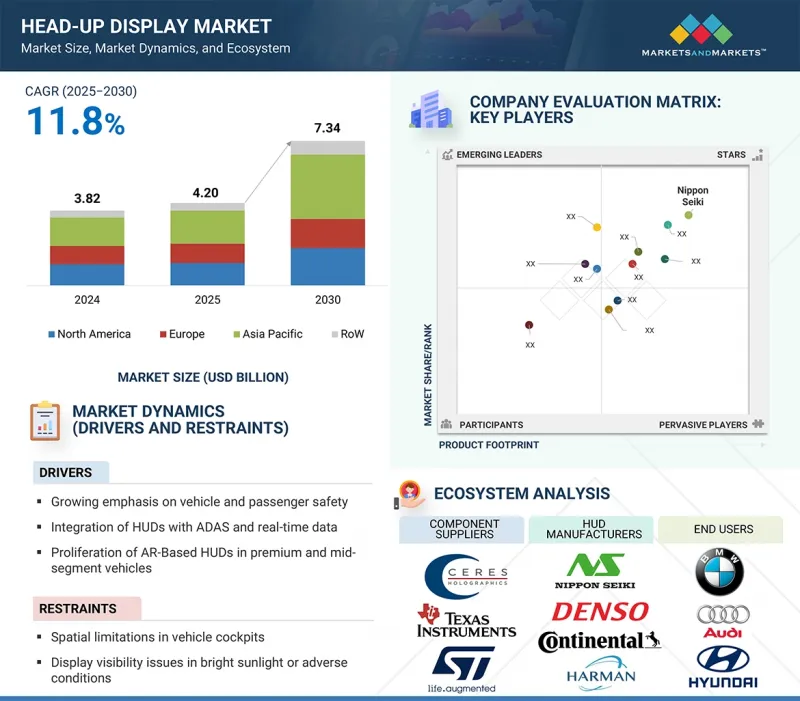

세계의 헤드업 디스플레이(HUD) 시장 규모는 2025년에 42억 달러, 2030년까지 73억 4,000만 달러에 달할 것으로 예측되며, 2025-2030년에 CAGR로 11.8%의 성장이 전망됩니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

유형, 구성요소, 폼팩터, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

헤드업 디스플레이(HUD) 시장은 운전자의 주의 산만함을 줄이고 상황 인식을 향상시키는 ADAS(첨단 운전자 보조 시스템)에 대한 수요 증가에 의해 주도되고 있습니다. AR 기능과 커넥티드 기술의 통합이 진행됨에 따라 내비게이션과 실시간 위험 감지 기능이 강화됩니다. 또한, 프로젝션 및 디스플레이 기술의 발전에 힘입어 고급 및 중급 차량에 HUD가 채택되면서 세계 시장의 성장을 촉진하고 있습니다.

"프로젝터/영사기 부문이 2024년 가장 큰 시장 점유율을 차지했습니다."

프로젝터는 윈드쉴드나 컴바이너에 이미지나 정보를 투사하는 핵심 부품입니다. 디스플레이의 선명도, 밝기, 해상도를 결정하는 핵심적인 역할을 하기 때문에 기존 시스템부터 AR 시스템까지 모든 HUD 유형에서 필수적인 요소로 자리 잡고 있습니다. 첨단 운전 보조 기능 및 몰입형 내비게이션 오버레이에 대한 수요가 증가함에 따라, 프로젝션 장치는 다양한 차량 유형에 적합하도록 더 높은 밝기, 더 넓은 시야, 컴팩트한 폼팩터로 설계되었습니다. 레이저 기반 및 마이크로 LED 프로젝션과 같은 기술 발전은 효율성, 내구성 및 시각적 성능을 더욱 향상시켜 자동차 제조업체가 선호하는 촉진제가 되고 있습니다. 모든 HUD가 주요 기능 요소로 프로젝션 장치에 의존하고 있기 때문에 고급차, 중급차, 전기자동차에 널리 통합되어 2024년 시장의 주요 구성요소로 자리매김할 것입니다.

"자동차 부문은 예측 기간 동안 헤드업 디스플레이(HUD) 시장에서 가장 높은 CAGR을 보일 것으로 예상됩니다."

자동차 부문은 중급 및 전기자동차를 포함한 다양한 자동차에 HUD가 빠르게 통합됨에 따라 2025-2030년 가장 높은 CAGR을 보일 것으로 예상됩니다. 첨단 안전, 실시간 내비게이션, 몰입형 차량 내 경험에 대한 소비자 수요가 증가함에 따라 자동차 제조사들은 디지털 콕핏 전략의 일환으로 HUD를 우선적으로 채택하고 있습니다. AR HUD의 보급이 확대되고, 작고 비용 효율적인 프로젝션 기술이 발전함에 따라 이 시스템은 고급차 이외의 차량에서도 쉽게 이용할 수 있게 되었습니다. 또한, 커넥티드 드라이빙과 자율주행을 향한 전 세계적인 추진은 HUD를 더욱 중요한 휴먼-머신 인터페이스로 만들었고, 이 기간 동안 자동차 부문에서 HUD의 빠른 성장을 보장합니다.

"인도는 2025-2030년 세계 헤드업 디스플레이(HUD) 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다."

인도는 아시아태평양 및 세계 헤드업 디스플레이(HUD) 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 중국의 자동차 부문은 승용차 및 상용차 생산 및 판매 증가, 전기 이동성으로의 점진적인 전환에 힘입어 강력한 확장을 경험하고 있습니다. 가처분 소득의 증가, 중산층 인구의 증가, 고급차에 대한 소비자의 강한 선호도가 HUD를 포함한 첨단 자동차 기술의 채택을 촉진하고 있습니다. 또한, 교통 안전을 개선하고 ADAS와 커넥티드 모빌리티 솔루션의 통합을 촉진하기 위한 정부 주도의 노력은 HUD 시스템을 전체 자동차 카테고리에 적용하는 것을 촉진하고 있습니다. 기술에 정통한 젊은 소비자들이 많고 운전 경험과 내비게이션의 편의성 향상에 대한 관심이 높아지는 것도 시장 성장을 더욱 가속화하고 있습니다. 이러한 수요 측면과 정책 주도적 요인이 결합되면서 HUD는 아시아태평양 및 세계 시장에서 HUD 채택의 중요한 성장 동력이 되고 있습니다.

세계의 헤드업 디스플레이(HUD) 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

헤드업 디스플레이(HUD) 시장의 매력적인 기회

헤드업 디스플레이(HUD) 시장 : 최종 용도별

헤드업 디스플레이(HUD) 시장 : 폼팩터별

헤드업 디스플레이(HUD) 시장 : 유형별

헤드업 디스플레이(HUD) 시장 : 지역별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

밸류체인 분석

고객 비즈니스에 영향을 미치는 동향/혼란

생태계 분석

투자와 자금 조달 시나리오

기술 분석

주요 기술

인접 기술

보완 기술

가격 책정 분석

자동차용 HUD 평균판매가격 : 주요 제조업체별(2024년)

자동차용 HUD 평균판매가격 : 지역별(2024년)

사례 연구 분석

무역 분석

수입 시나리오(HS 코드 8528)

수출 시나리오(HS 코드 8528)

특허 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

규제 상황

규제기관, 정부기관, 기타 조직

기준과 규제

주요 회의와 이벤트(2025-2026년)

헤드업 디스플레이(HUD) 시장에 대한 AI/생성형 AI의 영향

소개

헤드업 디스플레이(HUD) 시장의 AI/생성형 AI 이용 사례와 영향

헤드업 디스플레이(HUD) 시장에 대한 2025년 미국 관세의 영향

소개

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종 용도에 대한 영향

제6장 헤드업 디스플레이(HUD) 기술

소개

디지털 HUD(LCD/LED/OLED)

DLP 기반 HUD

웨이브 가이드 기반 HUD

레이저 기반 HUD

제7장 헤드업 디스플레이(HUD) 특징

소개

시야

해상도

휘도

정확도

컴바이너 투과율

제8장 헤드업 디스플레이(HUD) 시장 : 구성요소별

소개

비디오 제너레이터/처리 장비

프로젝터/투영 장비

표시장치

기타 구성요소

제9장 헤드업 디스플레이(HUD) 시장 : 유형별

소개

기존 HUD

AR HUD

제10장 헤드업 디스플레이(HUD) 시장 : 폼팩터별

소개

윈드실드 HUD

컴바이너 HUD

웨어러블 HUD

제11장 헤드업 디스플레이(HUD) 시장 : 최종 용도별

소개

항공

민간 항공

군용 항공

자동차

중급차

고급차

기타 용도

제12장 헤드업 디스플레이(HUD) 시장 : 지역별

소개

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

폴란드

북유럽

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

한국

인도

호주

인도네시아

말레이시아

태국

베트남

기타 아시아태평양

기타 지역

기타 지역의 거시경제 전망

중동

아프리카

남미

제13장 경쟁 구도

개요

주요 진출 기업의 전략/강점(2020-2025년)

시장 점유율 분석(2024년)

매출 분석(2020-2024년)

기업 평가와 재무 지표

제품의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제14장 기업 개요

소개

주요 기업

NIPPON SEIKI CO., LTD.

CONTINENTAL AG

DENSO CORPORATION

PANASONIC HOLDINGS CORPORATION

VALEO

HARMAN INTERNATIONAL

E-LEAD ELECTRONICS CO., LTD

BAE SYSTEMS

YAZAKI CORPORATION

GARMIN LTD.

기타 기업

THALES

HONEYWELL INTERNATIONAL INC.

CMC ELECTRONICS

COLLINS AEROSPACE

RENESAS ELECTRONICS CORPORATION

STMICROELECTRONICS

EXCELITAS TECHNOLOGIES CORP.

ELBIT SYSTEMS LTD.

VUZIX CORPORATION

FORYOU CORPORATION

HUDWAY, LLC

WAYRAY AG

ENVISICS

TEXAS INSTRUMENTS INCORPORATED

SAMTEL AVIONICS

제15장 부록

KSM

영문 목차

영문목차

The global head-up display market is expected to reach USD 4.20 billion in 2025 and USD 7.34 billion by 2030, growing at a CAGR of 11.8% from 2025 to 2030.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Type, Component, Form Factor, End User, and Region

Regions covered

North America, Europe, APAC, RoW

The head-up display market is driven by the rising demand for advanced driver-assistance systems (ADAS) that reduce driver distraction and improve situational awareness. Increasing integration of augmented reality (AR) features and connected technologies enhances navigation and real-time hazard detection. Additionally, the mounting adoption of HUDs in premium and mid-range vehicles, supported by advancements in projection and display technologies, fuels the global market growth.

"Projectors/projection units segment accounted for the largest market share in 2024."

The projectors/projection units segment accounted for the largest share of the head-up display market in 2024. It serves as the core component responsible for creating and projecting images or information onto the windshield or combiner. Its central role in determining the clarity, brightness, and resolution of the display makes it indispensable across all HUD types, from conventional to augmented reality systems. With the rising demand for advanced driver-assistance features and immersive navigation overlays, projection units are designed with higher brightness, wider fields of view, and compact form factors to fit diverse vehicle models. Technological advancements, such as laser-based and microLED projection, further enhance efficiency, durability, and visual performance, driving their preference among automakers. Given that every HUD relies on the projection unit as its primary functional element, its widespread integration across premium, mid-range, and electric vehicles secures its position as the leading component in the market in 2024.

"Automotive segment is projected to witness the highest CAGR in the head-up display market during the forecast period."

The automotive segment is projected to exhibit the highest CAGR from 2025 to 2030, driven by the rapid integration of HUDs into a range of vehicles, including mid-range and electric models. Rising consumer demand for advanced safety, real-time navigation, and immersive in-vehicle experiences pushes automakers to prioritize HUD adoption as part of their digital cockpit strategies. The increasing deployment of augmented reality HUDs and the advancements in compact and cost-efficient projection technologies make the systems more accessible beyond luxury vehicles. Additionally, the global push toward connected and autonomous driving further positions HUDs as a critical human-machine interface, ensuring their accelerated growth in the automotive sector during this period.

"India is expected to exhibit the highest CAGR in the global head-up display market from 2025 to 2030."

India is anticipated to record the highest CAGR in Asia Pacific and global head-up display markets. The country's automotive sector is experiencing robust expansion, supported by increasing production and sales of passenger and commercial vehicles and a gradual shift toward electric mobility. Rising disposable income, the growing middle-class population, and strong consumer preference for premium vehicles encourage the adoption of advanced in-vehicle technologies, including HUDs. Additionally, government-led initiatives to improve road safety and promote the integration of ADAS and connected mobility solutions foster greater deployment of HUD systems across vehicle categories. The large base of young, tech-savvy consumers, coupled with growing interest in enhanced driving experiences and navigation convenience, further accelerates the market growth. This combination of demand-side and policy-driven factors positions it as a key growth engine for HUD adoption in the Asia Pacific and global markets.

Extensive primary interviews were conducted with key industry experts in the head-up display market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below:

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

By Designation: C-level Executives - 40%, Managers - 30%, and Others - 30%

By Region: North America - 40%, Europe - 30%, Asia Pacific - 20%, and RoW - 10%

Nippon Seiki Co., Ltd. (Japan), Continental AG (Germany), DENSO CORPORATION (Japan), E-LEAD ELECTRONIC CO. LTD (Taiwan), BAE Systems (UK), Yazaki Corporation (Japan), HARMAN International (US), Valeo (France), Panasonic Holdings Corporation (Japan), and Garmin Ltd. (US) are some key players in the head-up display market.

Research Coverage:

This research report categorizes the head-up display market based on type (conventional HUDs, AR HUDs), component (video generators/processing units, display units, projectors/projection units, other components), end user (aviation, automotive, and other end users), form factor (windshield HUDs, combiner HUDs, wearable HUDs), and region (North America, Europe, Asia Pacific, and RoW). The report describes the major drivers, restraints, challenges, and opportunities pertaining to the head-up display market and forecasts the same till 2030. Apart from this, the report also consists of leadership mapping and analysis of all the companies included in the head-up display ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market by providing information on the closest approximations of the revenue numbers for the overall head-up display market and the subsegments. This report will help stakeholders to understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (growing emphasis on vehicle and passenger safety; integration of head-up displays (HUDs) with advanced driver assistance systems (ADAS) and real-time data; proliferation of AR-Based HUDs in premium and mid-segment vehicles; technological advancements in microdisplay and projection technologies; growing consumer preference for enhanced in-vehicle user experience; rising demand for connected vehicles worldwide), restraints (spatial limitations in vehicle cockpits; display visibility issues in bright sunlight or adverse conditions; complexity in retrofitting and standardization; complex installation and maintenance), opportunities (expansion into two-wheelers and commercial vehicles, increasing interest in HUDs for electric and software-defined vehicles), and challenges (regulatory challenges; limited field of view (FOV); high expenses linked to advanced head-up displays) influencing the growth of the head-up display market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the head-up display market

Market Development: Comprehensive information about lucrative markets - the report analyzes the head-up display market across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the head-up display market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including Nippon Seiki Co., Ltd. (Japan), Continental AG (Germany), DENSO CORPORATION (Japan), E-LEAD ELECTRONIC CO. LTD (Taiwan), BAE Systems (UK), Yazaki Corporation (Japan), HARMAN International (US), Valeo (France), Panasonic Holdings Corporation (Japan), Garmin Ltd. (US) in the head-up display market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.1.2 List of key secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants

2.1.2.3 Breakdown of primaries

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEAD-UP DISPLAY MARKET

4.2 HEAD-UP DISPLAY MARKET, BY END USE

4.3 HEAD-UP DISPLAY MARKET, BY FORM FACTOR

4.4 HEAD-UP DISPLAY MARKET, BY TYPE

4.5 HEAD-UP DISPLAY MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing emphasis on vehicle and passenger safety

5.2.1.2 Rising integration of HUDs with ADAS and real-time data

5.2.1.3 Proliferating adoption of AR-based HUDs in premium and mid-segment vehicles

5.2.1.4 Rapid advances in microdisplay and projection technologies

5.2.1.5 Growing focus on enhanced in-vehicle user experience

5.2.1.6 Mounting global demand for connected vehicles

5.2.2 RESTRAINTS

5.2.2.1 Spatial limitations in vehicle cockpits

5.2.2.2 Display visibility issues in bright sunlight or adverse conditions

5.2.2.3 Issues related to retrofitting and standardization

5.2.2.4 Complex installation and maintenance

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing interest in HUDs for electric and software-defined vehicles

5.2.3.2 Rising application in two-wheeler and commercial vehicles

5.2.4 CHALLENGES

5.2.4.1 Regulatory challenges

5.2.4.2 Limited field of view (FOV)

5.2.4.3 High expenses linked to advanced HUDs

5.3 VALUE CHAIN ANALYSIS

5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.5 ECOSYSTEM ANALYSIS

5.6 INVESTMENT AND FUNDING SCENARIO

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Waveguide optics

5.7.1.2 Micro-LED and OLED displays

5.7.1.3 Digital light processing (DLP)

5.7.2 ADJACENT TECHNOLOGIES

5.7.2.1 Advanced driver assistance systems (ADAS)

5.7.2.2 Augmented reality mapping engines

5.7.3 COMPLEMENTARY TECHNOLOGIES

5.7.3.1 Holographic optical elements (HOEs)

5.8 PRICING ANALYSIS

5.8.1 AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS, BY KEY PLAYER, 2024

5.8.2 AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS, BY REGION, 2024