Phosphoric Acid Market by Process Type (Wet, Thermal), Application (Fertilizers, Feed & Food Additives, Detergents, Water Treatment Chemicals, Metal Treatment, Industrial Use), and Region - Global Forecast to 2030

상품코드:1816010

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 234 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

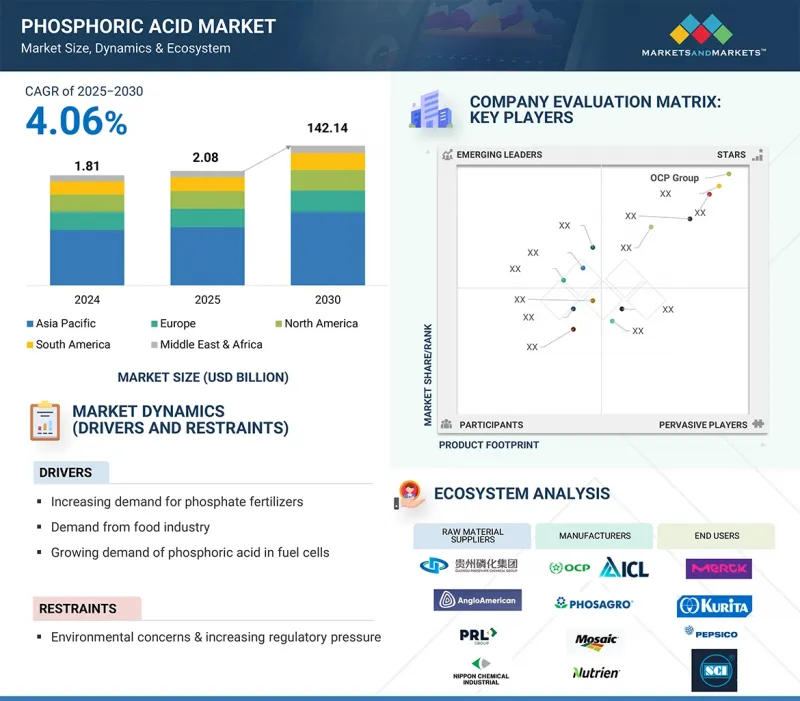

세계의 인산 시장 규모는 2024년 1,120억 3,000만 달러에서 2030년까지 1,421억 4,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 4.06%의 성장이 전망됩니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러, 킬로톤

부문

프로세스 유형, 용도, 지역

대상 지역

아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미

인산 시장은 세계 농업이 인산을 많이 함유한 비료를 필요로 하는 고생산성 농업으로 발전하고 식량 생산 수요 증가에 대응하면서 성장세를 보이고 있습니다. 급성장 시장의 산업화 진행과 세계 인구 증가, 도시에서의 식습관이 수요를 확대하고, 생산기술의 발전이 공급 효율성과 원가경쟁력을 높이고 있습니다.

"열처리 유형은 2024년 시장 점유율 2위를 차지했습니다. "

2024년, 열처리 유형은 인산 시장에서 두 번째 점유율을 차지했습니다. 이는 식품용 및 산업용에 적합한 순수 산을 생산할 수 있는 능력이 있기 때문입니다. 습식 공정과 달리 열 공정은 제약, 음료, 전자제품 제조 등 높은 공정 품질이 요구되는 분야에서 많이 선택되고 있습니다. 이는 제품의 순도와 성능에 프리미엄이 붙기 때문에 특히 규제 준수와 특수 용도가 가격보다 우선시되는 시장에서 안정적인 수요를 증명하고 있습니다.

"2024년, 세제 부문은 세계 인산 시장에서 금액 기준으로 세 번째 용도를 차지했습니다. "

2024년, 세제 부문은 금액 기준으로 세 번째 시장 점유율을 차지했습니다. 이러한 우위는 청소용품 및 위생용품 생산의 기본 구성 요소로서 필수 불가결한 위치에 있기 때문입니다. 인산은 세정력을 높이고 가정용, 산업용, 시설용 제품의 성능을 보장하기 위해 광물성 침전물을 제거하는 데 매우 효과적이기 때문에 세제 제품 제조 분야에서 널리 사용되고 있습니다. 이 부문 시장 수요는 위생 수준에 대한 소비자의 인식 증가, 도시 인구 증가, 개발도상국 시장의 성장에 의해 뒷받침되고 있습니다. 또한, 환경 친화적인 고성능 세제의 끊임없는 기술 혁신은 안정적인 소비를 촉진하여 전체 시장 포트폴리오에서 이 부문의 확고한 입지를 구축했습니다.

"2024년 유럽은 인산 시장에서 금액 기준으로 2위를 차지했습니다. "

유럽은 2024년 인산 시장 규모 기준 2위를 차지할 것으로 예상되며, 이는 주로 사료 및 식품 첨가물, 수처리, 인산 비료 수요에 기인합니다. 시장은 통합된 공급망, 높은 규제 준수율, 생산 기술로 동일한 제품을 높은 확률로 지속할 수 있는 생산 기술을 가진 전통 있는 화학 공급업체들이 독점하고 있으며, 지속가능성을 기반으로 작동하고 있습니다. 또한, 특수 화학제품 및 산업용도의 이용 증가도 시장 지위를 강화하고 있습니다.

세계의 인산(Phosphoric Acid) 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

인산 시장 기업에 있어서 매력적인 기회

인산 시장 : 지역별

아시아태평양 인산 시장 : 프로세스 유형별, 국가별

지역 분석, 인산 시장 : 용도별

인산 시장의 매력

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 지표

제6장 산업 동향

공급망 분석

원재료 공급업체

제조업체

판매업체

최종사용자

가격 결정 분석

주요 응용 분야별 주요 기업의 평균 판매 가격(2024년)

인산 평균 판매 가격 추이 : 지역별

고객의 비즈니스에 영향을 미치는 동향/혼란

생태계 분석

기술 분석

주요 기술

보완 기술

사례 연구 분석

고순도 인산에 의한 비료 생산 최적화

인산 혼합물을 이용한 금속 처리 부식 저감

무역 분석

수입 시나리오(HS코드 280920)

수출 시나리오(HS코드 280920)

규제 상황

규제기관, 정부기관 및 기타 조직

규제 구조

주요 컨퍼런스 및 이벤트

투자 및 자금조달 시나리오

특허 분석

접근

문헌 유형

주요 출원자

관할 분석

인산 시장에 대한 2025년 미국 관세의 영향

서론

주요 관세율

가격 영향 분석

국가/지역에 대한 영향

용도에 대한 영향

인산 시장에 대한 AI/생성형 AI의 영향

제7장 인산 시장 : 용도별

서론

비료

사료 및 식품첨가물

세제

수처리 약품

금속 마감

산업 용도

기타 용도

제8장 인산 시장 : 프로세스 유형별

서론

습식 프로세스

열 프로세스

제9장 인산 시장 : 지역별

서론

아시아태평양

중국

인도

인도네시아

파키스탄

호주

북미

미국

멕시코

캐나다

유럽

러시아

튀르키예

폴란드

프랑스

스페인

남미

브라질

아르헨티나

중동 및 아프리카

사우디아라비아

모로코

이집트

제10장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

시장 점유율 분석(2024년)

주요 5개사의 매출 분석(2021년-2024년)

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

브랜드/제품 비교 분석

기업 평가와 재무 지표

경쟁 시나리오

제11장 기업 개요

주요 기업

OCP GROUP

THE MOSAIC COMPANY

PJSC PHOSAGRO

ICL GROUP LTD

NUTRIEN LTD.

EUROCHEM GROUP AG

INNOPHOS

SOLVAY SA

MA'ADEN

IFFCO

기타 기업

PRAYON

ADITYA BIRLA MANAGEMENT CORPORATION PVT. LTD.

J.R. SIMPLOT COMPANY

JORDAN PHOSPHATE MINES COMPANY, PLC.(JPMC)

AGROPOLYCHIM

PARADEEP PHOSPHATES LTD.

GUJARAT STATE FERTILIZERS & CHEMICALS LIMITED(GSFC)

WENGFU & ZIJIN CHEMICAL INDUSTRY CO., LTD.

HUBEI XINGFA CHEMICALS GROUP CO., LTD.

FOSKOR

CHONGQING CHUANDONG CHEMICAL(GROUP) CO., LTD.

VINIPUL CHEMICALS PVT. LTD.

CENTRAL & WESTERN INDIA CHEMICALS

FOSFA

JIANGSU CHENGXING PHOSPH- CHEMICALS CO., LTD.

제12장 인접 시장과 관련 시장

서론

제한 사항

인산염 시장

시장의 정의

시장 개요

인산염 시장 : 지역별

아시아태평양

유럽

북미

중동 및 아프리카

남미

제13장 부록

LSH

영문 목차

영문목차

The global phosphoric acid market size is projected to reach USD 142.14 billion in 2030 from USD 112.03 billion in 2024, at a CAGR of 4.06% during the forecast period.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Process Type, Application, and Region

Regions covered

Asia Pacific, Europe, North America, Middle East & Africa, and South America

The market for phosphoric acid is experiencing growth as world agriculture evolves toward more productive practices demanding phosphate-rich fertilizers to address increasing food production needs. Increased industrialization in fast-growing markets, combined with growing global population and urban eating habits, is building demand, while production technology advances are enhancing supply efficiency and cost competitiveness.

"Thermal process type accounted for the second-largest share of the phosphoric acid market in 2024."

In 2024, the thermal process segment had the second-biggest market share of phosphoric acid because it has the capacity to produce pure acid, which fits both food-grade and industrial uses. In contrast with the wet process, the thermal path is chosen more frequently in the sector where high process quality is demanded, like pharmaceuticals, beverages, or electronics production. This is evidenced by its stable demand because of the premium it sets on the purity and performance of the products, especially in markets where regulatory compliance and specialized applications prevail over pricing.

"Detergents segment was the third largest application of the global phosphoric acid market, in terms of value, in 2024."

In 2024, the detergents segment accounted for the third-largest share of the global phosphoric acid market in terms of value. This dominance is led by its indispensable status as a fundamental component in the production of cleaning and hygiene goods. Phosphoric acid is widely used in the area of formulating a detergent product since it is quite effective in the removal of mineral deposits to enhance cleaning power and guarantee the performance of the products in household, industrial, and institutional applications. Market demand for the segment was underpinned by consumers' increasing consciousness about hygiene levels, urban population growth, and the emergence of developing markets. Moreover, the constant innovation of green and high-performance detergents helped drive stable consumption, consolidating the segment's strong position in the overall market portfolio.

"Europe was the second-largest phosphoric acid market, in terms of value, in 2024."

Europe was the second-largest phosphoric acid market in value in 2024, led primarily by the demand from feed & food additives, water treatment, and phosphate-based fertilizers. The market is controlled by well-established chemical suppliers with incorporated supply chains, high regulatory adherence, and technology in the production can ensure the persistence of the same product at a high rate, and functions based on sustainability. Also, the market position is strengthened by the increasing utilization of specialty chemicals and industrial usage applications.

By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

By Designation: Directors - 50%, Managers - 30%, and Others - 20%

By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, Rest of World - 5%

The key players profiled in the report include OCP Group (Morocco), The Mosaic Company (US), PJSC PhosAgro (Russia), ICL Group Ltd (Israel), Nutrien Ltd. (Canada), EuroChem Group AG (Switzerland), Innophos (US), Solvay SA (Belgium), Ma'aden (Saudi Arabia), and IFFCO (India).

Research Coverage

This report segments the phosphoric acid market based on process type, application, and region and provides estimations of value (USD million) for the overall market size across various regions. It has also conducted a detailed analysis of key industry players to provide insights into their business overviews, services, and key strategies associated with the phosphoric acid market.

Reasons to Buy this Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the phosphoric acid market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights into the following points:

Market Penetration: Comprehensive information on phosphoric acid offered by top players in the global market

Analysis of key drivers (Increasing demand for phosphate fertilizers, demand from the food industry, and growing demand for phosphoric acid in fuel cells), restraints (Environmental concerns & increasing regulatory pressure), opportunities (Commercialization of chiral phosphoric acid as catalyst and recovery of rare earth elements for phosphoric acids), and challenges (Diminishing supply of phosphate) influencing the growth of phosphoric acid market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the phosphoric acid market

Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for phosphoric acid across regions

Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global phosphoric acid market

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the phosphoric acid market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 MARKET DEFINITION AND INCLUSIONS, BY PROCESS TYPE

1.3.4 MARKET DEFINITION AND INCLUSIONS, BY APPLICATION

1.3.5 YEARS CONSIDERED

1.3.6 CURRENCY CONSIDERED

1.3.7 UNITS CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key primary participants

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 GROWTH FORECAST

2.4.1 SUPPLY-SIDE ANALYSIS

2.4.2 DEMAND-SIDE ANALYSIS

2.5 ASSUMPTIONS

2.6 LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PHOSPHORIC ACID MARKET

4.2 PHOSPHORIC ACID MARKET, BY REGION

4.3 ASIA PACIFIC: PHOSPHORIC ACID MARKET, BY PROCESS TYPE AND COUNTRY

4.4 REGIONAL ANALYSIS: PHOSPHORIC ACID MARKET, BY APPLICATION

4.5 PHOSPHORIC ACID MARKET ATTRACTIVENESS

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising demand for increasing crop yield

5.2.1.2 Improved texture, quality, and shelf life of food

5.2.1.3 Fuel cell applications in buses and trucks

5.2.2 RESTRAINTS

5.2.2.1 Environmental concerns and increasing regulatory pressure

5.2.3 OPPORTUNITIES

5.2.3.1 Commercialization of chiral phosphoric acid as catalyst

5.2.3.2 Recovery of rare earth elements from phosphoric acid

5.2.4 CHALLENGES

5.2.4.1 Diminishing supply of phosphate

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 THREAT OF SUBSTITUTES

5.3.2 THREAT OF NEW ENTRANTS

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GDP TRENDS AND FORECAST

6 INDUSTRY TRENDS

6.1 SUPPLY CHAIN ANALYSIS

6.1.1 RAW MATERIAL SUPPLIERS

6.1.2 MANUFACTURERS

6.1.3 DISTRIBUTORS

6.1.4 END USERS

6.2 PRICING ANALYSIS

6.2.1 AVERAGE SELLING PRICE OF KEY PLAYERS FOR KEY APPLICATIONS, 2024

6.2.2 AVERAGE SELLING PRICE TREND OF PHOSPHORIC ACID, BY REGION

6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.6.1 OPTIMIZING FERTILIZER PRODUCTION WITH HIGH-PURITY PHOSPHORIC ACID

6.6.2 REDUCING CORROSION IN METAL TREATMENT USING PHOSPHORIC ACID BLENDS

6.7 TRADE ANALYSIS

6.7.1 IMPORT SCENARIO (HS CODE 280920)

6.7.2 EXPORT SCENARIO (HS CODE 280920)

6.8 REGULATORY LANDSCAPE

6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.8.2 REGULATORY FRAMEWORK

6.8.2.1 ISO 3706:1976 Phosphoric acid for industrial use (including foodstuffs) - Determination of total phosphorus (V) oxide content - Quinoline phosphomolybdate gravimetric method

6.8.2.2 ISO 2997:1974 Phosphoric acid for industrial use - Determination of sulphate content - Method by reduction and titrimetry

6.9 KEY CONFERENCES AND EVENTS

6.10 INVESTMENT AND FUNDING SCENARIO

6.11 PATENT ANALYSIS

6.11.1 APPROACH

6.11.2 DOCUMENT TYPES

6.11.3 TOP APPLICANTS

6.11.4 JURISDICTION ANALYSIS

6.12 IMPACT OF 2025 US TARIFF ON PHOSPHORIC ACID MARKET

6.12.1 INTRODUCTION

6.12.2 KEY TARIFF RATES

6.12.3 PRICE IMPACT ANALYSIS

6.12.4 IMPACT ON COUNTRY/REGION

6.12.4.1 US

6.12.4.2 Europe

6.12.4.3 Asia Pacific

6.12.5 IMPACT ON APPLICATIONS

6.13 IMPACT OF AI/GEN AI ON PHOSPHORIC ACID MARKET

7 PHOSPHORIC ACID MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 FERTILIZERS

7.2.1 RISING DEMAND FOR INCREASING AGRICULTURAL YIELD TO BOOST MARKET

7.3 FEED & FOOD ADDITIVES

7.3.1 GROWING DEMAND FOR DAIRY AND FOOD PRODUCTS IN EMERGING ECONOMIES TO DRIVE MARKET

7.4 DETERGENTS

7.4.1 EFFECTIVE CLEANING WITH LESS WATER AT LOW TEMPERATURES TO POSITIVELY INFLUENCE MARKET GROWTH

7.5 WATER TREATMENT CHEMICALS

7.5.1 RISING USE FOR MUNICIPAL, INSTITUTIONAL, AND INDUSTRIAL APPLICATIONS TO PROPEL MARKET

7.6 METAL FINISHING

7.6.1 HIGH DEMAND FOR SURFACE ENHANCEMENT AND CORROSION PROTECTION TO DRIVE GROWTH

7.7 INDUSTRIAL USE

7.7.1 APPLICATIONS IN RUBBER, LEATHER, GLASS, PLASTICS, OIL REFINERIES, PAINTS, PIGMENTS, AND RESINS TO DRIVE MARKET

7.8 OTHER APPLICATIONS

8 PHOSPHORIC ACID MARKET, BY PROCESS TYPE

8.1 INTRODUCTION

8.2 WET PROCESS

8.2.1 EXTENSIVE USE IN FERTILIZERS TO BOOST MARKET GROWTH

8.3 THERMAL PROCESS

8.3.1 GROWING DEMAND FOR PROCESSED FOOD TO DRIVE MARKET

9 PHOSPHORIC ACID MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 CHINA

9.2.1.1 Various strengthening domestic sectors to drive demand

9.2.2 INDIA

9.2.2.1 Expansion of food & beverage and water treatment industries to boost growth

9.2.3 INDONESIA

9.2.3.1 Increasing food & beverage exports to propel market

9.2.4 PAKISTAN

9.2.4.1 Government initiatives to drive demand

9.2.5 AUSTRALIA

9.2.5.1 Increasing demand for meat and meat products to fuel market

9.3 NORTH AMERICA

9.3.1 US

9.3.1.1 Population growth and improving living standards to boost demand

9.3.2 MEXICO

9.3.2.1 Growing food industry to drive demand

9.3.3 CANADA

9.3.3.1 Well-established agriculture industry, depleting soil fertility, and loss of arable land to boost market

9.4 EUROPE

9.4.1 RUSSIA

9.4.1.1 Increasing purchasing power of farmers and government initiatives to drive demand

9.4.2 TURKEY

9.4.2.1 Strong government incentives for agriculture sector to fuel market growth

9.4.3 POLAND

9.4.3.1 Depletion of arable land to increase demand for fertilizers

9.4.4 FRANCE

9.4.4.1 Extensive fertile soil, moderate climate, and rainfall for agriculture to propel market

9.4.5 SPAIN

9.4.5.1 Growing consumption of processed food to drive market

9.5 SOUTH AMERICA

9.5.1 BRAZIL

9.5.1.1 Economic growth to drive demand

9.5.2 ARGENTINA

9.5.2.1 Increased demand in food and beverages to fuel market

9.6 MIDDLE EAST & AFRICA

9.6.1 SAUDI ARABIA

9.6.1.1 Government initiatives for reduction of dependence on oil to support increasing fertilizer production

9.6.2 MOROCCO

9.6.2.1 Rising trade with key countries to boost market

9.6.3 EGYPT

9.6.3.1 Nationwide focus on land retrieval for agricultural development to drive market

10 COMPETITIVE LANDSCAPE

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3 MARKET SHARE ANALYSIS, 2024

10.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2021-2024

10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.5.1 STARS

10.5.2 EMERGING LEADERS

10.5.3 PERVASIVE PLAYERS

10.5.4 PARTICIPANTS

10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.5.5.1 Company footprint

10.5.5.2 Region footprint

10.5.5.3 Process type footprint

10.5.5.4 Application footprint

10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024