액추에이터 시장 : 액추에이션별, 유형별, 용도별, 업계별, 지역별 - 예측(-2030년)

Actuators Market by Actuation (Electric, Hydraulic, Pneumatic), Type (Linear, Rotary), Application (Industrial Automation, Robotics, Vehicle Equipment), Vertical (Power Generation, Automotive, Aerospace & Defense) and Region - Global Forecast to 2030

상품코드:1816002

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 264 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 액추에이터 시장 규모는 2025년에 712억 2,000만 달러, 2030년에는 1,004억 1,000만 달러에 달하고, 예측 기간에 CAGR 7.1%의 성장이 전망됩니다.

액추에이터는 산업 자동화, 자동차, 항공우주, 에너지, 로봇 등 다양한 분야에서 운동과 제어를 실현하는 중요한 요소입니다. 액추에이터 기술은 에너지를 정확한 기계적 운동으로 변환하여 자동화, 성능 최적화, 업무 효율성 향상을 가능하게 합니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

액추에이션, 유형, 용도, 업계, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

스마트 액추에이터는 센서, IoT 연결성, 예지보전 기능과의 통합을 통해 그 가치를 더욱 높여 인더스트리 4.0과 스마트 인프라의 핵심이 되고 있습니다. 전동 액추에이터로의 전환은 지속가능성 목표, 에너지 효율성, 유지보수 비용 절감에 의해 추진되고 있습니다. 이로 인해 특히 자동차 전동화 및 재생 에너지 시스템 응용 분야에서 액추에이터의 채택이 가속화되고 있습니다. 조직이 액추에이터 기술을 활용하여 지능적이고 효율적인 데이터 기반 경영을 실현하기 위해 액추에이터 기술을 활용함에 따라, 디지털 전환 및 산업 자동화 노력과 액추에이터의 연계는 경쟁력을 강화할 수 있습니다.

"유압 액추에이터 부문은 2024년 액추에이터 시장에서 두 번째 점유율을 차지했습니다. "

유압 액추에이터 부문은 2024년 액추에이터 시장에서 두 번째 점유율을 차지했습니다. 그 주된 이유는 매우 큰 힘과 토크를 생성하는 능력으로, 중장비 산업, 건설, 항공우주, 방위산업에 필수적인 요소로 자리 잡았습니다. 유압 시스템은 특히 가혹한 압력과 조건에서 견고한 성능이 요구되는 환경에서 높은 정밀도와 높은 신뢰성으로 큰 하중을 효율적으로 처리할 수 있습니다. 석유 및 가스, 광업, 해양, 중장비 부문에서 널리 사용되는 것도 안정적인 수요에 기여하고 있습니다. 그러나 전기 액추에이터에 비해 에너지 효율이 낮고 부피가 크며 유지보수가 번거로워 그 우위는 제한적입니다.

"산업별로는 전자 및 전기 부문이 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

자동화의 급속한 확대, 소형화, 소비자 가전, 반도체, 데이터 저장 장치에서 첨단 모션 제어 시스템의 통합이 증가함에 따라 전자 및 전기 부문은 액추에이터 시장에서 가장 빠르게 성장하는 최종 사용자로 부상하고 있습니다. 특히 PCB 조립용 로봇 암, 반도체 팹의 웨이퍼 핸들링, 광학기기 및 디스플레이의 미세 위치 결정 등의 분야에서 액추에이터는 독보적인 위치를 차지하고 있습니다. 또한, 스마트폰, IoT 기기, 전기차 배터리, 5G 인프라에 대한 수요 증가는 대규모 생산을 촉진하고, 액추에이터를 핵심 부품으로 하는 보다 효율적이고 자동화된 시스템을 채택하도록 제조업체를 자극하고 있습니다.

"중동은 2025-2030년 액추에이터 시장에서 가장 빠르게 성장하는 지역이 될 가능성이 높습니다. "

중동은 인프라 프로젝트 확대와 자동화 기술에 대한 투자 증가로 인해 예측 기간 동안 액추에이터 시장에서 가장 빠른 성장률을 보일 것으로 예측됩니다. 이 지역 정부들은 경제 다각화를 추진하고 있으며, 특히 중동의 석유 의존도가 높은 경제는 제조, 재생 에너지, 효율성과 제어를 위해 첨단 액추에이터에 의존하는 스마트 인프라에 많은 투자를 하고 있습니다.

세계의 액추에이터(Actuator) 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

액추에이터 시장 기업에 있어서 매력적인 기회

액추에이터 시장 : 액추에이션별

액추에이터 시장 : 유형별

액추에이터 시장 : 용도별

액추에이터 시장 : 업계별

액추에이터 시장 : 국가별

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

생태계 분석

저명 기업

민간기업과 중소기업

용도

밸류체인 분석

규제 상황

규제기관, 정부기관 및 기타 조직

기준과 규제

가격 결정 분석

주요 액추에이터 제품 판매 가격

액추에이터 참고 가격 : 유형별

액추에이터 평균 판매 가격대 : 지역별

무역 분석

수입 시나리오(HS코드 841229)

수출 시나리오(HS코드 841229)

고객의 비즈니스에 영향을 미치는 동향/혼란

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

사례 연구 분석

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

주요 컨퍼런스 및 이벤트(2025년-2026년)

투자 및 자금조달 시나리오

액추에이터 시장에 대한 AI/생성형 AI의 영향

액추에이터 시장에 대한 2025년 미국 관세의 영향

서론

주요 관세율

가격 영향 분석

국가/지역에 대한 영향

최종 이용 산업에 대한 영향

제6장 액추에이터 시장 : 액추에이션별

서론

전기

유압

공기압

기타

제7장 액추에이터 시장 : 용도별

서론

산업 자동화

로보틱스

차량 장비

제8장 액추에이터 시장 : 유형별

서론

선형 액추에이터

로터리 액추에이터

제9장 액추에이터 시장 : 업계별

서론

식품 및 음료

석유 및 가스

금속 및 광업/기계

발전

화학제품/종이 및 플라스틱

의약품 및 의료

자동차

항공우주 및 방위

해사

전자공학 및 전기공학

건설

유틸리티

가정용품 및 엔터테인먼트

농업

제10장 지역 분석

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

러시아

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

인도

일본

한국

호주

기타 아시아태평양

중동

중동의 거시경제 전망

GCC 국가

기타 중동

기타 지역

기타 지역의 거시경제 전망

라틴아메리카

아프리카

제11장 경쟁 구도

서론

주요 시장 진출기업의 전략/강점

매출 분석(2020년-2024년)

시장 점유율 분석(2024년)

기업 평가와 재무 지표

제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제12장 기업 개요

주요 기업

EMERSON ELECTRIC CO.

ROCKWELL AUTOMATION

PARKER HANNIFIN CORP

ABB

SMC CORPORATION

MOOG INC.

CURTISS-WRIGHT CORPORATION

REGAL REXNORD

ROTORK GROUP

SKF GROUP

MISUMI GROUP INC.

IMI

EATON

TOLOMATIC

VENTURE MFG. CO.

기타 기업

INTELLIGENT ACTUATOR, INC.

HARMONIC DRIVE LLC

NOOK INDUSTRIES, INC.

SHOGHI COMMUNICATION LTD.

DVG AUTOMATION SPA

MACRON DYNAMICS

ROTOMATION INC.

PEGASUS ACTUATORS GMBH

KINITICS AUTOMATION

FESTO

제13장 부록

LSH

영문 목차

영문목차

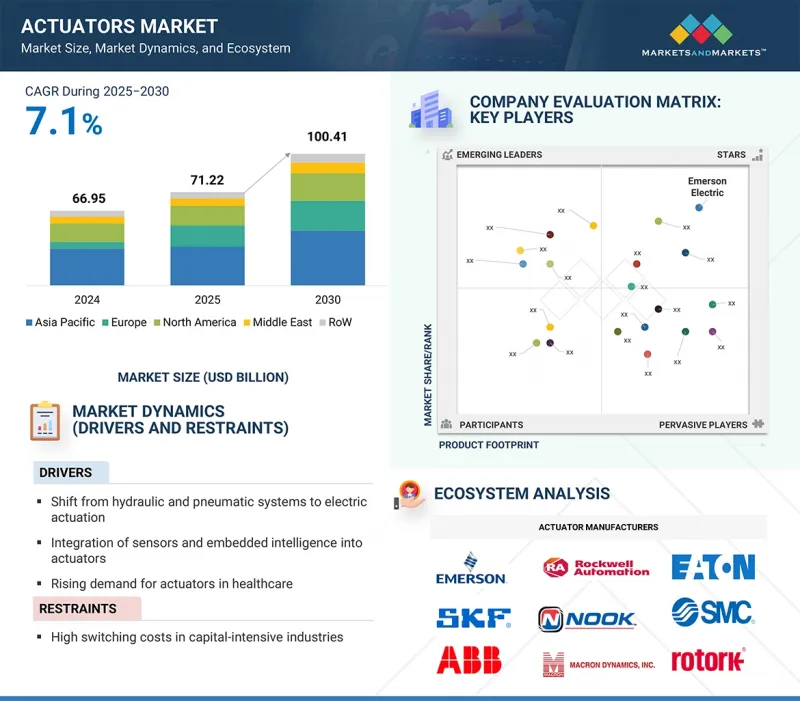

The global actuators market is expected to be valued at USD 71.22 billion in 2025 and USD 100.41 billion in 2030, registering a CAGR of 7.1% during the forecast period. Actuators are key enablers of motion and control across various sectors, such as industrial automation, automotive, aerospace, energy, and robotics. The actuator technology enables automation, performance optimization, and enhanced operational efficiency by converting energy into precise mechanical motion.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Actuation, Type, Application, Vertical and Region

Regions covered

North America, Europe, APAC, RoW

The integration of smart actuators with sensors, IoT connectivity, and predictive maintenance capabilities further amplifies their value, making them a cornerstone of Industry 4.0 and smart infrastructure. The shift toward electric actuators is driven by sustainability goals, energy efficiency, and reduced maintenance costs. This accelerates the adoption of actuators, particularly in automotive electrification and renewable energy system applications. Its alignment with digital transformation and industrial automation initiatives strengthens competitiveness, as organizations increasingly leverage actuator technologies for intelligent, efficient, and data-driven operations.

"Hydraulic actuation segment held the second-largest share of the actuators market in 2024"

The hydraulic actuation segment captured the second-largest share of the actuators market in 2024, primarily due to their ability to generate extremely high force and torque, making them indispensable in heavy-duty industrial, construction, aerospace, and defense applications. Hydraulic systems can efficiently handle large loads with high precision and reliability, especially in environments that demand rugged performance under extreme pressures and conditions. Their widespread use in oil & gas, mining, marine, and heavy machinery sectors contributes to steady demand. However, they are often considered less energy-efficient, bulkier, and require more maintenance than electric actuators, limiting their dominance.

"By vertical, the electronics & electrical segment is expected to witness highest CAGR during the forecast period"

The electronics and electrical vertical is emerging as the fastest-growing end user in the actuators market due to the rapid expansion of automation, miniaturization, and the increasing integration of advanced motion-control systems in consumer electronics, semiconductors, and data storage devices. Electronics manufacturing requires high precision, repeatability, and speed-qualities that actuators are uniquely positioned to deliver, particularly in applications such as robotic arms for PCB assembly, wafer handling in semiconductor fabs, and micro-positioning in optics and displays. Furthermore, the rising demand for smartphones, IoT devices, EV batteries, and 5G infrastructure drives large-scale production, pushing manufacturers to adopt more efficient, automated systems where actuators are core components.

"Middle East is likely to be the fastest-growing region in the actuators market from 2025 to 2030"

The Middle East is expected to witness the fastest growth rate in the actuators market during the forecast period due to expanding infrastructure projects and the increasing investment in automation technologies. Governments in these regions push for economic diversification, particularly in the Middle East, where oil-dependent economies invest heavily in manufacturing, renewable energy, and smart infrastructure that rely on advanced actuators for efficiency and control.

The study contains insights from various industry experts, including actuator providers, Tier 1 companies, and end users. The break-up of the primaries is as follows:

By Company Type - Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

By Designation- C-level Executives - 48%, Directors - 33%, and Others - 19%

By Region-North America - 35%, Europe - 18%, Asia Pacific - 40%, and RoW - 7%

The actuators market is dominated by a few globally established players, such as Emerson Electric Co. (US), PARKER HANNIFIN CORP (US), ABB (Switzerland), Rockwell Automation (US), and SMC Corporation (Japan). The study includes an in-depth competitive analysis of these key players in the actuators market and their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the actuators market and forecasts its size by actuation, application, type, vertical, and region. The report also discusses the drivers, restraints, opportunities, and challenges pertaining to the market. It gives a detailed view of the market across four main regions-North America, Europe, Asia Pacific, and RoW. A supply chain analysis has been included in the report, along with the key players and their competitive analysis of the actuators ecosystem.

Key Benefits of Buying the Report:

Analysis of key drivers (Shift from hydraulic and pneumatic systems to electric actuation, Integration of sensors and embedded intelligence into actuators, Rising demand for actuators in healthcare), restraints (High switching costs in capital-intensive industries), opportunities (Harnessing industrial automation and AI to unlock new value, Capitalizing on retrofit demand and servitization of legacy systems, Increased spending on renewable sources of energy for power generation), and challenges (Issues of leakage in pneumatic and hydraulic actuators, ensuring cybersecurity and functional safety in smart actuators)

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the actuators market

Market Development: Comprehensive information about lucrative markets - the report analyses the actuators market across varied regions

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the actuators market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Emerson Electric Co. (US), PARKER HANNIFIN CORP (US), ABB (Switzerland), Rockwell Automation (US), and SMC Corporation (Japan), in the actuators market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNITS CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants

2.1.2.2 Breakdown of primary interviews

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION METHODOLOGY

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ACTUATORS MARKET

4.2 ACTUATORS MARKET, BY ACTUATION

4.3 ACTUATORS MARKET, BY TYPE

4.4 ACTUATORS MARKET, BY APPLICATION

4.5 ACTUATORS MARKET, BY VERTICAL

4.6 ACTUATORS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Shift from hydraulic and pneumatic systems to electric actuation

5.2.1.2 Integration of sensors and embedded intelligence into actuators

5.2.1.3 Rising demand from healthcare

5.2.2 RESTRAINTS

5.2.2.1 High switching costs in capital-intensive industries

5.2.3 OPPORTUNITIES

5.2.3.1 Harnessing industrial automation and AI

5.2.3.2 Capitalizing on retrofit demand and servitization of legacy systems

5.2.3.3 Increased spending on renewable sources of energy for power generation

5.2.4 CHALLENGES

5.2.4.1 Issues of leakage in pneumatic and hydraulic actuators

5.2.4.2 Ensuring cybersecurity and functional safety in smart actuators

5.3 ECOSYSTEM ANALYSIS

5.3.1 PROMINENT COMPANIES

5.3.2 PRIVATE AND SMALL ENTERPRISES

5.3.3 APPLICATIONS

5.4 VALUE CHAIN ANALYSIS

5.5 REGULATORY LANDSCAPE

5.5.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.5.2 STANDARDS AND REGULATIONS

5.6 PRICING ANALYSIS

5.6.1 SELLING PRICE OF KEY ACTUATOR PRODUCTS

5.6.2 INDICATIVE PRICING OF ACTUATORS, BY TYPE

5.6.3 AVERAGE SELLING PRICE RANGE OF ACTUATOR, BY REGION

5.7 TRADE ANALYSIS

5.7.1 IMPORT SCENARIO (HS CODE 841229)

5.7.2 EXPORT SCENARIO (HS CODE 841229)

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Smart actuators for Industry 4.0

5.9.2 COMPLIMENTARY TECHNOLOGIES

5.9.2.1 Artificial muscles

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 Power electronics

5.10 PATENT ANALYSIS

5.11 CASE STUDY ANALYSIS

5.12 PORTER'S FIVE FORCES ANALYSIS

5.12.1 INTENSITY OF COMPETITIVE RIVALRY

5.12.2 BARGAINING POWER OF SUPPLIERS

5.12.3 BARGAINING POWER OF BUYERS

5.12.4 THREAT OF SUBSTITUTES

5.12.5 THREAT OF NEW ENTRANTS

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 INVESTMENT AND FUNDING SCENARIO

5.16 IMPACT OF AI/GEN AI ON ACTUATORS MARKET

5.17 IMPACT OF 2025 US TARIFF ON ACTUATORS MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE INDUSTRIES

6 ACTUATORS MARKET, BY ACTUATION

6.1 INTRODUCTION

6.2 ELECTRIC

6.2.1 HIGHER EFFICIENCY AND LEVEL OF CONTROL TO INCREASE ADOPTION

6.3 HYDRAULIC

6.3.1 DEMAND IN HIGH-FORCE APPLICATIONS TO DRIVE MARKET GROWTH

6.4 PNEUMATIC

6.4.1 ADOPTION IN FOOD & BEVERAGES AND OIL & GAS INDUSTRIES TO DRIVE DEMAND

6.5 OTHERS

6.5.1 RECENT DEVELOPMENTS IN THERMAL, PIEZOELECTRIC, AND HYBRID ACTUATORS TO SUPPORT MARKET GROWTH

7 ACTUATORS MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 INDUSTRIAL AUTOMATION

7.2.1 NEED FOR ENHANCING QUALITY AND INCREASING FLEXIBILITY OF MANUFACTURING PROCESS TO DRIVE MARKET

7.3 ROBOTICS

7.3.1 INCREASING ADOPTION OF ROBOTICS ACROSS AUTOMOTIVE AND ELECTRONICS & ELECTRICAL INDUSTRIES TO DRIVE GROWTH

7.3.2 INDUSTRIAL ROBOTS

7.3.3 SERVICE ROBOTS

7.4 VEHICLE EQUIPMENT

7.4.1 INCREASING AUTONOMY LEVELS AND REQUIREMENTS FOR AUTOMATED VALVE CONTROLS AND SUSPENSION MECHANISMS TO DRIVE MARKET

8 ACTUATORS MARKET, BY TYPE

8.1 INTRODUCTION

8.2 LINEAR ACTUATORS

8.2.1 ROD TYPE

8.2.2 SCREW TYPE

8.2.3 BELT TYPE

8.3 ROTARY ACTUATORS

8.3.1 MOTORS

8.3.2 BLADDER & VANE

8.3.3 PISTON TYPE

9 ACTUATORS MARKET, BY VERTICAL

9.1 INTRODUCTION

9.2 FOOD & BEVERAGES

9.2.1 AUTOMATION IN FOOD & BEVERAGE SECTOR DRIVING DEMAND FOR SMART AND HYGIENIC ACTUATORS

9.3 OIL & GAS

9.3.1 NEED FOR PRECISE FLOW CONTROL AND EMISSIONS REDUCTION TO DRIVE MARKET GROWTH

9.4 METALS, MINING & MACHINERY

9.4.1 DEMAND FOR RELIABLE MOTION AND CONTROL SYSTEMS IN DEMANDING OPERATIONS TO FUEL ADOPTION

9.5 POWER GENERATION

9.5.1 ELECTRIC ACTUATORS INCREASINGLY USED IN AUXILIARY SYSTEMS AND BALANCE-OF-PLANT OPERATIONS

9.6 CHEMICALS, PAPER & PLASTICS

9.6.1 ADOPTION OF ADVANCED ACTUATORS INCREASING TO ENSURE RELIABLE QUALITY AND CONSISTENT PERFORMANCE

9.7 PHARMACEUTICALS & HEALTHCARE

9.7.1 STRINGENT REGULATIONS FOR HYGIENE AND INCREASED DEMAND FOR SURGICAL ROBOTS TO DRIVE GROWTH

9.8 AUTOMOTIVE

9.8.1 ADVANCEMENTS IN AUTOMOTIVE SECTOR TO INCREASE ADOPTION OF SMART ACTUATORS

9.9 AEROSPACE & DEFENSE

9.9.1 ADOPTION OF ELECTRIC AND ELECTROMECHANICAL ACTUATORS INCREASING IN SECONDARY SYSTEMS

9.10 MARINE

9.10.1 INCREASED USE IN COMMERCIAL SHIPBUILDING TO DRIVE SEGMENTAL GROWTH

9.11 ELECTRONICS & ELECTRICAL

9.11.1 NEED FOR ENHANCED CONTROL EFFICIENCY AND PRODUCTIVITY IN HIGH-TECH MANUFACTURING TO DRIVE DEMAND

9.12 CONSTRUCTION

9.12.1 INCREASING ADOPTION FOR HEAVY EQUIPMENT PRECISION AND OPERATIONAL EXCELLENCE TO DRIVE MARKET

9.13 UTILITIES

9.13.1 INCREASED DEMAND FOR LOGISTICS, AGRICULTURE, AND FIELD ROBOTS TO DRIVE SEGMENTAL GROWTH

9.14 HOUSEHOLD & ENTERTAINMENT

9.14.1 INCREASED DEMAND FOR SERVICE ROBOTS IN DOMESTIC APPLICATIONS TO BOOST DEMAND

9.15 AGRICULTURE

9.15.1 INCREASING MECHANIZATION TO DRIVE ADOPTION

10 REGIONAL ANALYSIS

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

10.2.2 US

10.2.2.1 Increase adoption of Industry 4.0 to drive market

10.2.3 CANADA

10.2.3.1 Rising demand for linear actuators to drive market

10.3 EUROPE

10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

10.3.2 GERMANY

10.3.2.1 Thriving automotive and manufacturing industries to drive market

10.3.3 UK

10.3.3.1 Increasing demand from oil & gas industry to drive market

10.3.4 FRANCE

10.3.4.1 Presence of major aerospace & defense manufacturers to drive market

10.3.5 ITALY

10.3.5.1 Presence of major automobile and food & beverages manufacturers to drive market

10.3.6 RUSSIA

10.3.6.1 Diverse industrial landscape to support market growth

10.3.7 REST OF EUROPE

10.4 ASIA PACIFIC

10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

10.4.2 CHINA

10.4.2.1 Presence of major industries to drive market growth

10.4.3 INDIA

10.4.3.1 Presence of flourishing steel and textile industries to drive market

10.4.4 JAPAN

10.4.4.1 Increasing production in industries to drive demand

10.4.5 SOUTH KOREA

10.4.5.1 Presence of major automotive and electronics manufacturers to drive market

10.4.6 AUSTRALIA

10.4.6.1 Advancements in automation technologies across industries to boost demand

10.4.7 REST OF ASIA PACIFIC

10.5 MIDDLE EAST

10.5.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST

10.5.2 GCC COUNTRIES

10.5.2.1 Industrialization and infrastructure development to drive growth

10.5.2.2 Saudi Arabia

10.5.2.2.1 Economic diversification efforts to drive market

10.5.2.3 UAE

10.5.2.3.1 Technological advancement and infrastructure development to support market growth

10.5.3 REST OF MIDDLE EAST

10.6 REST OF THE WORLD (ROW)

10.6.1 MACROECONOMIC OUTLOOK FOR ROW

10.6.2 LATIN AMERICA

10.6.3 AFRICA

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3 REVENUE ANALYSIS, 2020-2024

11.4 MARKET SHARE ANALYSIS, 2024

11.5 COMPANY VALUATION AND FINANCIAL METRICS

11.6 PRODUCT COMPARISON

11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.7.1 STARS

11.7.2 EMERGING LEADERS

11.7.3 PERVASIVE PLAYERS

11.7.4 PARTICIPANTS

11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.7.5.1 Company footprint

11.7.5.2 Region footprint

11.7.5.3 Actuation footprint

11.7.5.4 Type footprint

11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024