마이크로그리드 시장 : 발전기, 에너지 저장 시스템, 컨트롤러, 그리드 연결, 오프그리드, 태양광발전, 연료전지, 열병합발전(CHP), 천연가스, 원격지, 전력 기업, 군사시설 - 예측(-2030년)

Microgrid Market by Power Generator, Energy Storage System, Controller, Grid-connected, Off-grid, Solar PV, Fuel Cell, Combined Heat and Power (CHP), Natural Gas, Remote Area, Utility and Military Facility - Global Forecast to 2030

상품코드:1812634

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 338 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

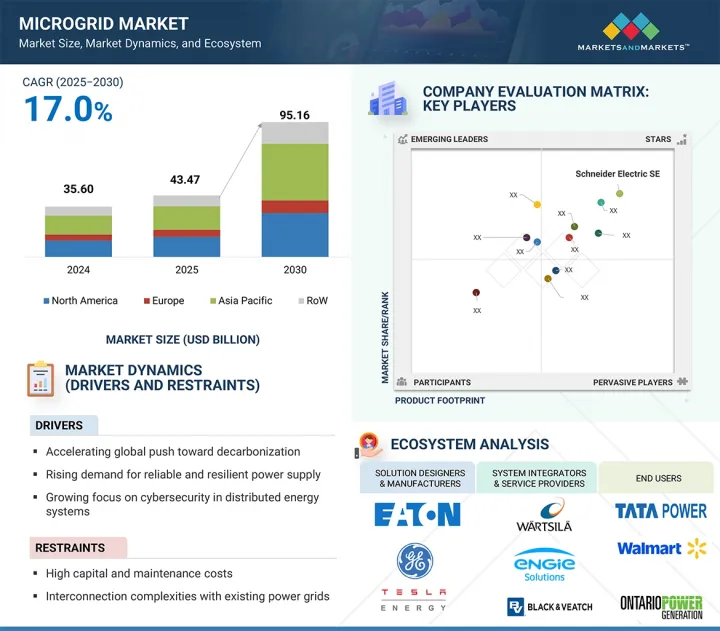

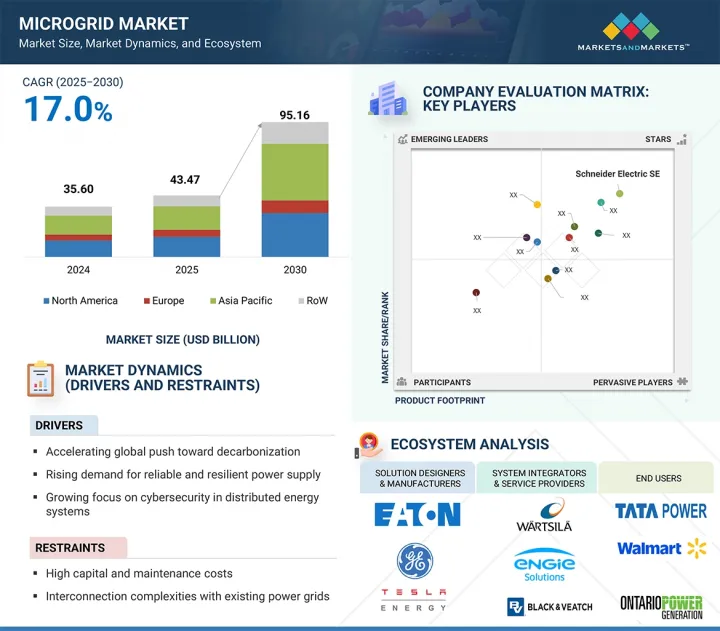

세계의 마이크로그리드 시장 규모는 2025년에 434억 7,000만 달러를 기록하고, 2030년까지 951억 6,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 17.0%의 성장이 전망됩니다.

여러 요인이 시장을 주도하고 있습니다. 탄력적이고 안정적인 전력 공급에 대한 수요 증가와 재생에너지원의 통합은 정부, 전력 회사 및 산업계가 분산형 에너지 솔루션을 채택하도록 유도하고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

난방 기기, 냉방 기기, 환기 기기, 기술, 도입 방식, 서비스 유형, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

지원적인 정책 프레임워크, 농촌의 전기화 노력, 정전되기 쉬운 지역의 전력망 안정성에 대한 요구가 보급을 더욱 가속화하고 있습니다. 에너지 저장, 첨단 컨트롤러, 분산형 에너지 자원(DER) 관리 시스템의 기술 발전은 마이크로그리드의 운영 효율성, 유연성, 확장성을 높이고 있습니다. 그러나 높은 설비투자 요건, 복잡한 규제 당국의 승인, 다양한 기술 간의 상호운용성 문제 등이 보급의 걸림돌로 작용하고 있습니다. 또한, 일부 신흥 시장에서는 최종사용자의 인지도가 낮고 장기적인 경제적 이익을 정량화하기 어렵다는 점이 여전히 큰 장벽으로 작용하고 있습니다. 혁신적인 자금 조달 모델과 표준화된 프레임워크를 통해 이러한 과제를 극복하는 것이 지속적인 시장 확대에 필수적입니다.

"동력원별로는 연료전지 부문이 2025-2030년 가장 높은 CAGR을 기록할 것으로 예상됩니다."

마이크로그리드 시장의 연료전지 부문은 깨끗하고 효율적이며 신뢰할 수 있는 분산형 전력 솔루션에 대한 수요 증가로 인해 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. 연료전지는 지속적인 저배출 전력 생산능력으로 인해 마이크로그리드 애플리케이션에 대한 채택이 증가하고 있으며, 탈탄소화 및 지속가능성 목표를 달성하고자 하는 상업, 산업 및 시설에 이상적입니다. 또한, 높은 효율성, 모듈식 확장성, 단독 또는 재생에너지와 함께 운영할 수 있는 능력으로 인해 계통연계형 및 섬형 마이크로그리드의 주요 기술로 자리매김하고 있습니다. 수소 생산, 저장 및 유통 인프라의 발전으로 연료전지 기반 마이크로그리드의 경제성이 향상되고 있으며, 지원 정책과 인센티브는 특히 아시아태평양, 북미 및 유럽에서 마이크로그리드 보급을 가속화하고 있습니다. 주요 제조업체들은 내구성 향상, 비용 절감, 연료전지와 첨단 에너지 관리 시스템과의 통합을 통한 성능 극대화에 초점을 맞추고 있습니다. 에너지 전환에 대한 노력이 가속화되고 있는 가운데, 연료전지는 차세대 마이크로그리드 아키텍처를 형성하는 데 있어 매우 중요한 역할을 할 것으로 예상됩니다.

"정격 출력별로는 1-5MW 부문이 2025-2030년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

마이크로그리드 시장의 1-5MW 부문은 전력량, 확장성, 범용성의 최적 균형에 힘입어 2025-2030년 사이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이 출력 범위의 시스템은 상업 시설, 산업 시설, 의료 시설, 교육 캠퍼스, 소규모 커뮤니티에 적합하며, 비용 효율성을 유지하면서 다양한 에너지 수요를 충족시킬 수 있는 충분한 전력을 제공합니다. 태양광발전, 풍력발전, 열병합발전(CHP), 연료전지, 에너지 저장 등 여러 분산형 에너지 자원을 통합할 수 있는 능력으로 신뢰도 향상, 에너지 비용 절감, 계통 중단에 대한 복원력을 실현합니다. 또한, 1-5MW 범위는 대규모 시스템에 따른 높은 자본 비용을 부담하지 않고 부분적인 그리드 독립, 재생에너지 통합, 피크 부하 관리를 목표로 하는 시설의 증가하는 요구사항에 대응합니다. 아시아태평양, 북미, 유럽에서는 규제 지원, 재생에너지 목표, 마이크로그리드 성능을 최적화하는 제어 및 자동화 기술의 발전으로 인해 마이크로그리드 채택이 활발하게 이루어지고 있습니다.

"북미가 2025-2030년 시장 점유율 2위를 차지할 것으로 예상됩니다."

북미는 탄력적이고 신뢰할 수 있는 전력 시스템에 대한 수요 증가, 재생에너지 통합 증가, 지원적인 규제 프레임워크에 힘입어 2025-2030년 세계 마이크로그리드 시장에서 두 번째 점유율을 차지할 것으로 예상됩니다. 미국과 캐나다는 마이크로그리드 도입의 최전선에 있으며, 전력회사, 정부기관, 민간기업이 에너지 안보 강화와 탄소배출 감소를 위해 적극적으로 투자하고 있습니다. 이 지역은 허리케인, 산불 등 이상기후에 취약하기 때문에 병원, 군사기지, 데이터센터, 커뮤니티 에너지 시스템 등 중요 시설에 대한 구축이 가속화되고 있습니다. 제어 소프트웨어, 에너지 저장 및 하이브리드 전력 솔루션의 발전은 성능과 비용 효율성을 더욱 향상시킵니다.

세계의 마이크로그리드 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 경쟁 상황, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

마이크로그리드 시장 기업에서 매력적인 기회

마이크로그리드 시장 : 전력 정격별

마이크로그리드 시장 : 동력원별

마이크로그리드 시장 : 연결성별

마이크로그리드 시장 : 제공별

마이크로그리드 시장 : 최종사용자별

마이크로그리드 시장 : 지역별

마이크로그리드 시장 : 지리별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

공급망 분석

생태계 분석

가격 책정 분석

마이크로그리드 평균판매가격 : 최종사용자별, 전력 정격별(2024년)

유틸리티 기반 마이크로그리드 프로젝트 평균판매가격 동향 : 지역별(2021-2024년)

투자와 자금 조달 시나리오

고객 비즈니스에 영향을 미치는 동향/혼란

기술 분석

주요 기술

보완 기술

인접 기술

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

SKAGERAK ENERGI, HITACHI ENERGY의 태양광 발전 기술을 활용해 노르웨이 ODD SOCCER CLUB의 SKAGERAK ARENA에 전력 공급

CUMMINS, GOLD FIELDS 시설에 호주 최대 규모의 하이브리드 재생 에너지 마이크로그리드 설치

ONTARIO INSTITUTE OF TECHNOLOGY, GE Vernova의 캠퍼스 기반 마이크로그리드 시스템으로 그리드 운영 최적화

필라델피아 해군 조선소 프로젝트, 전력 수요 충족을 위해 GE Vernova의 내구성 및 신뢰성 높은 전력 공급 시스템 채택

ACE NATURAL, HOMER GRID의 에너지 비용 모델 구축을 위해 SOLAR ONE ENERGY와 계약

HALF MOON VENTURES, 오하이오주 마이크로그리드 프로젝트의 EPC 서비스를 S&C ELECTRIC COMPANY에 위탁

ERGON ENERGY, 마이크로그리드 전력 품질 향상을 위해 S&C ELECTRIC COMPANY의 에너지 저장 시스템 채택

AEG POWER SOLUTIONS, MBOGO VALLEY TEA FACTORY에 무정전 전원 장치용 그리드 형성 인버터 제공

HITACHI ENERGY, 남아프리카공화국에서 발전기 백업 시스템을 혁신적인 마이크로그리드 솔루션으로 전환

무역 분석

수입 시나리오(HS 코드 8501)

수출 시나리오(HS 코드 8501)

특허 분석

주요 회의와 이벤트(2025-2026년)

규제 상황

규제기관, 정부기관, 기타 조직

표준

규제

마이크로그리드 시장에 대한 AI/생성형 AI의 영향

마이크로그리드 시장에 대한 2025년 미국 관세의 영향

소개

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종사용자에 대한 영향

제6장 마이크로그리드 유형

소개

AC 마이크로그리드

DC 마이크로그리드

하이브리드 마이크로그리드

제7장 마이크로그리드 전개 지역

소개

도시/대도시

준도시

농촌/섬

제8장 마이크로그리드 아키텍처 유형

소개

기존

근대식

첨단/차세대

제9장 마이크로그리드 시장 : 전력 정격별

소개

1MW 미만

1-5MW

5-10MW

10MW 이상

제10장 마이크로그리드 시장 : 동력원별

소개

천연가스

태양광발전

열병합발전(CHP)

디젤

연료전지

기타 동력원

제11장 마이크로그리드 시장 : 연결성별

소개

그리드 연결

오프그리드

제12장 마이크로그리드 시장 : 제공별

소개

하드웨어

소프트웨어

서비스

제13장 마이크로그리드 시장 : 최종사용자별

소개

상업·산업 빌딩

원격지

군사시설

정부 청사

전력 기업

기관·캠퍼스

의료 시설

제14장 마이크로그리드 시장 : 지역별

소개

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

영국

독일

프랑스

이탈리아

스페인

폴란드

북유럽

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

호주

중국

일본

한국

인도

인도네시아

태국

베트남

말레이시아

기타 아시아태평양

기타 지역

기타 지역의 거시경제 전망

중동

아프리카

남미

제15장 경쟁 구도

개요

주요 진출 기업의 전략/강점(2021-2025년)

시장 점유율 분석(2024년)

매출 분석(2020-2024년)

기업 평가와 재무 지표

브랜드/제품의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제16장 기업 개요

주요 기업

SCHNEIDER ELECTRIC

SIEMENS

GE VERNOVA

EATON

ABB

HITACHI ENERGY LTD

HONEYWELL INTERNATIONAL INC.

CATERPILLAR

S&C ELECTRIC COMPANY

TESLA

기타 기업

HOMER ENERGY

EMERSON ELECTRIC CO.

PARETO ENERGY

SPIRAE LLC

KOHLER CO.

AMERESCO

SAFT

FERROAMP AB

CANOPY POWER PTE LTD.

POWERSECURE, INC.

POLARIS

ANBARIC DEVELOPMENT PARTNERS, LLC.

WARTSILA

AGGREKO

POWER ANALYTICS

BLOOM ENERGY

ENGIE

ROLLS-ROYCE PLC

ENEL X S.R.L.

XENDEE INC.

BOXPOWER, INC.

제17장 부록

KSM

영문 목차

영문목차

The microgrid market is projected to be valued at USD 43.47 billion in 2025 and USD 95.16 billion by 2030, recording a CAGR of 17.0% during the forecast period. Several factors are driving the global microgrid market. Rising demand for resilient and reliable power supply, coupled with the integration of renewable energy sources, is prompting governments, utilities, and industries to adopt decentralized energy solutions.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Heating Equipment, Cooling Equipment, Ventilation Equipment, Technology, Implementation Type, Service Type, End User, and Region

Regions covered

North America, Europe, APAC, RoW

Supportive policy frameworks, rural electrification initiatives, and the need for grid stability in regions prone to outages further accelerate deployment. Technological advancements in energy storage, advanced controllers, and distributed energy resource (DER) management systems are enhancing the operational efficiency, flexibility, and scalability of microgrids. However, high capital investment requirements, complex regulatory approvals, and interoperability challenges between diverse technologies can hinder adoption. In addition, limited awareness among end users in certain emerging markets and the difficulty quantifying long-term economic benefits remain key barriers. Overcoming these challenges through innovative financing models and standardized frameworks will be critical for sustained market expansion.

"By power source, the fuel cell segment is expected to register the highest CAGR between 2025 and 2030."

The fuel cell segment of the microgrid market is projected to register the highest CAGR during the forecast period, owing to the rising demand for clean, efficient, and reliable distributed power solutions. Fuel cells are increasingly adopted for microgrid applications due to their ability to provide continuous, low-emission power generation, making them ideal for commercial, industrial, and institutional facilities aiming to meet decarbonization and sustainability goals. Their high efficiency, modular scalability, and capability to operate independently or in conjunction with renewable energy sources position them as a key technology for grid-connected and islanded microgrids. Advancements in hydrogen production, storage, and distribution infrastructure are improving the economic feasibility of fuel cell-based microgrids, while supportive policies and incentives are accelerating deployments, particularly in Asia Pacific, North America, and Europe. Key manufacturers focus on enhancing durability, lowering costs, and integrating fuel cells with advanced energy management systems to maximize performance. As energy transition initiatives gain momentum, fuel cells are expected to be pivotal in shaping next-generation microgrid architectures.

"By power rating, the 1-5 MW segment is projected to account for the largest market share from 2025 to 2030."

The 1-5 MW segment of the microgrid market is expected to hold the largest market share from 2025 to 2030, supported by its optimal balance between capacity, scalability, and application versatility. Systems within this power range are ideally suited for commercial complexes, industrial facilities, healthcare institutions, educational campuses, and small communities, offering sufficient capacity to meet diverse energy demands while maintaining cost efficiency. Their ability to integrate multiple distributed energy resources, including solar PV, wind, combined heat and power (CHP), fuel cells, and energy storage, enables enhanced reliability, energy cost savings, and resilience against grid disruptions. The 1-5 MW range also meets the growing requirements of facilities aiming for partial grid independence, renewable integration, and peak load management without incurring the high capital costs associated with larger systems. Strong adoption is observed in Asia Pacific, North America, and Europe, driven by regulatory support, renewable energy targets, and advancements in control and automation technologies that optimize microgrid performance within this segment.

"North America is projected to account for the second-largest market share from 2025 to 2030."

North America is projected to hold the second-largest share of the global microgrid market from 2025 to 2030, driven by increasing demand for resilient and reliable power systems, rising renewable energy integration, and supportive regulatory frameworks. The US and Canada are at the forefront of microgrid adoption, with strong investments from utilities, government agencies, and private enterprises to enhance energy security and reduce carbon emissions. The region's vulnerability to extreme weather events, such as hurricanes and wildfires, has accelerated deployment in critical facilities, including hospitals, military bases, data centers, and community energy systems. Advancements in control software, energy storage, and hybrid power solutions further boost performance and cost efficiency.

Key players such as Schneider Electric SE (France), General Electric Company (US), and Eaton (Ireland) are actively partnering with regional utilities and municipalities to implement scalable, grid-connected, and islandable microgrid solutions. With robust technological capabilities and supportive policies, North America remains a pivotal market for global microgrid expansion.

The break-up of the profile of primary participants in the microgrid market-

By Company Type: Tier 1 - 50%, Tier 2 - 25%, Tier 3 - 25%

By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, RoW - 15%

Note: Other designations include sales, marketing, and product managers.

The three tiers of the companies are based on their total revenues as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: USD 500 million.

The major players in the microgrid market with a significant global presence include Schneider Electric (France), Siemens (Germany), General Electric Company (US), Eaton (Ireland), ABB (Switzerland), and others.

Research Coverage

The report segments the microgrid market and forecasts its size by offering, connectivity, power rating, power source, end user, and region. It also comprehensively reviews drivers, restraints, opportunities, and challenges influencing market growth. The report covers qualitative aspects in addition to quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants with information on the closest approximate revenues for the overall microgrid market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

Analysis of key drivers (increasing emphasis on decarbonization, growing need for reliable and uninterrupted power supply, surging deployment of microgrids for rural electrification, increasing cyberattacks on energy infrastructure, rising demand for electric vehicle (EV) charging infrastructure, increasing need for demand response and load management capabilities, economic and environmental advantages associated with use of microgrids), restraints ( high installation and maintenance costs, complexities in grid interconnections, low economies of scale), opportunities (increasing number of microgrid projects across different industries and sectors , growing energy demand and adoption of renewable energy in Asia Pacific, rising interest of investors in energy-as-a-service (EaaS) business model to minimize cost, rising government support for microgrid projects, digitalization and smart grid integration), and challenges (lack of standardization and regulatory frameworks related to microgrid operations, technical challenges related to microgrids operating in island mode, complexities associated with standardizing scalability of microgrids , difficulties in planning and designing large-sized microgrids)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches, agreements, partnerships, acquisitions, and contracts in the microgrid market

Market Development: Comprehensive information about lucrative markets - the report analyses the microgrid market across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the microgrid market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product/service offerings of leading players, including Schneider Electric SE (France), Siemens (Germany), General Electric Company (US), Eaton (Ireland), ABB (Switzerland), Hitachi Energy Ltd (Switzerland), Honeywell International Inc. (US), Caterpillar (US), S&C Electric Company (US), and Tesla (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 YEARS CONSIDERED

1.3.3 INCLUSIONS AND EXCLUSIONS

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants

2.1.2.2 Breakdown of primaries

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.1.2 Demand-side analysis

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.2.2.2 Supply-side analysis

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MICROGRID MARKET

4.2 MICROGRID MARKET, BY POWER RATING

4.3 MICROGRID MARKET, BY POWER SOURCE

4.4 MICROGRID MARKET, BY CONNECTIVITY

4.5 MICROGRID MARKET, BY OFFERING

4.6 MICROGRID MARKET, BY END USER

4.7 MICROGRID MARKET, BY REGION

4.8 MICROGRID MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Accelerating global push toward decarbonization and renewable integration

5.2.1.2 Growing focus on resilient power supply amid extreme weather events and grid failures

5.2.1.3 Expanding microgrid deployment for rural and remote electrification

5.2.1.4 Rising integration of EV charging infrastructure with microgrids

5.2.2 RESTRAINTS

5.2.2.1 High capital and lifecycle maintenance costs

5.2.2.2 Interconnection complexities and delays in grid synchronization

5.2.2.3 Uncertainty in long-term revenue models and business case viability

5.2.3 OPPORTUNITIES

5.2.3.1 Implementation of government incentives, policy support, and decentralization mandates

5.2.3.2 Advancements in digitalization, smart grid, and AI/Gen AI-powered optimization solutions

5.2.4 CHALLENGES

5.2.4.1 Absence of unified standards and regulatory frameworks

5.2.4.2 Technical challenges in islanded mode and grid resynchronization

5.2.4.3 Growing cybersecurity threats associated with distributed energy systems

5.3 SUPPLY CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF MICROGRIDS, BY END USER AND POWER RATING, 2024

5.5.2 AVERAGE SELLING PRICE TREND OF UTILITY-BASED MICROGRID PROJECTS, BY REGION, 2021-2024

5.6 INVESTMENT AND FUNDING SCENARIO

5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Blockchain

5.8.1.2 Microgrid smart controllers

5.8.1.3 AI/ML-driven control systems

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Next-gen battery storage systems

5.8.2.2 Advanced solar photovoltaics (PV)

5.8.2.3 5G/IoT communication networks

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Virtual power plants (VPPs)

5.8.3.2 Advanced materials for microgrid components

5.8.3.3 Digital twin

5.9 PORTER'S FIVE FORCES ANALYSIS

5.9.1 THREAT OF NEW ENTRANTS

5.9.2 THREAT OF SUBSTITUTES

5.9.3 BARGAINING POWER OF SUPPLIERS

5.9.4 BARGAINING POWER OF BUYERS

5.9.5 INTENSITY OF COMPETITIVE RIVALRY

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDY ANALYSIS

5.11.1 SKAGERAK ENERGI LEVERAGES HITACHI ENERGY'S PV TECHNOLOGY TO POWER ODD SOCCER CLUB'S SKAGERAK ARENA IN NORWAY

5.11.2 CUMMINS IMPLEMENTS AUSTRALIA'S LARGEST HYBRID RENEWABLE ENERGY MICROGRID AT GOLD FIELDS' SITE

5.11.3 UNIVERSITY OF ONTARIO INSTITUTE OF TECHNOLOGY USES GE VERNOVA'S CAMPUS-BASED MICROGRID SYSTEM TO OPTIMIZE GRID OPERATIONS

5.11.4 NAVY SHIPYARD PROJECT IN PHILADELPHIA ADOPTS GE VERNOVA'S RESILIENT AND RELIABLE POWER SUPPLY SYSTEMS TO MEET ELECTRICITY NEEDS

5.11.5 ACE NATURAL CONTRACTS SOLAR ONE ENERGY FOR HOMER GRID TO MODEL ENERGY COSTS

5.11.6 HALF MOON VENTURES TURNS TO S&C ELECTRIC COMPANY FOR EPC SERVICES FOR MICROGRID PROJECT IN OHIO

5.11.7 ERGON ENERGY USES S&C ELECTRIC COMPANY'S ENERGY STORAGE SYSTEMS FOR MICROGRIDS TO IMPROVE POWER QUALITY

5.11.8 AEG POWER SOLUTIONS PROVIDES GRID-FORMING INVERTER TO MBOGO VALLEY TEA FACTORY FOR UNINTERRUPTED POWER SUPPLY

5.11.9 HITACHI ENERGY TRANSFORMS GENERATOR BACKUP SYSTEM INTO INNOVATIVE MICROGRID SOLUTION IN SOUTH AFRICA

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 8501)

5.12.2 EXPORT SCENARIO (HS CODE 8501)

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 REGULATORY LANDSCAPE

5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15.2 STANDARDS

5.15.3 REGULATIONS

5.16 IMPACT OF AI/GEN AI ON MICROGRID MARKET

5.17 IMPACT OF 2025 US TARIFF ON MICROGRID MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END USERS

6 MICROGRID TYPES

6.1 INTRODUCTION

6.2 AC MICROGRIDS

6.3 DC MICROGRIDS

6.4 HYBRID MICROGRIDS

7 AREAS OF MICROGRID DEPLOYMENT

7.1 INTRODUCTION

7.2 URBAN/METROPOLITAN

7.3 SEMI-URBAN

7.4 RURAL/ISLAND

8 MICROGRIDS ARCHITECTURE TYPES

8.1 INTRODUCTION

8.2 TRADITIONAL

8.3 MODERN

8.4 ADVANCED/NEXT-GENERATION

9 MICROGRID MARKET, BY POWER RATING

9.1 INTRODUCTION

9.2 LESS THAN 1 MW

9.2.1 ABILITY TO PROVIDE ELECTRICITY IN REMOTE AREAS AND TEMPORARY CONSTRUCTION SITES TO BOOST SEGMENTAL GROWTH

9.3 1-5 MW

9.3.1 INTEGRATION WITH RENEWABLE ENERGY TO DELIVER RELIABLE AND SUSTAINABLE ELECTRICITY TO FUEL SEGMENTAL GROWTH

9.4 >5-10 MW

9.4.1 HIGH ADOPTION IN HOSPITALS, MILITARY BASES, AND DATA CENTERS TO ACCELERATE SEGMENTAL GROWTH

9.5 ABOVE 10 MW

9.5.1 ABILITY TO SUPPORT SMART CITY INITIATIVES AND POWER INDUSTRIAL COMPLEXES TO AUGMENT SEGMENTAL GROWTH

10 MICROGRID MARKET, BY POWER SOURCE

10.1 INTRODUCTION

10.2 NATURAL GAS

10.2.1 HIGH EMPHASIS ON EFFICIENT POWER GENERATION AND ENHANCING GRID RESILIENCE TO EXPEDITE SEGMENTAL GROWTH

10.3 SOLAR PV

10.3.1 EMERGENCE AS RELIABLE AND ABUNDANT ENERGY SOURCE TO CONTRIBUTE TO SEGMENTAL GROWTH

10.4 COMBINED HEAT AND POWER (CHP)

10.4.1 STRONG FOCUS ON ENERGY EFFICIENCY, SUSTAINABILITY, AND RESILIENCE TO BOOST SEGMENTAL GROWTH

10.5 DIESEL

10.5.1 COMPACT, PORTABLE, AND IDEAL FOR REMOTE/OFF-GRID LOCATIONS TO ACCELERATE SEGMENTAL GROWTH

10.6 FUEL CELL

10.6.1 COST-EFFECTIVENESS, RELIABILITY, MODULARITY, AND SCALABILITY FEATURES TO DRIVE MARKET

10.7 OTHER POWER SOURCES

11 MICROGRID MARKET, BY CONNECTIVITY

11.1 INTRODUCTION

11.2 GRID-CONNECTED

11.2.1 COST SAVINGS, IMPROVED POWER QUALITY, AND LOW ENVIRONMENTAL IMPACT TO FOSTER SEGMENTAL GROWTH

11.3 OFF-GRID

11.3.1 ENERGY INDEPENDENCE AND RELIABLE POWER SUPPLY TO BOOST ADOPTION

12 MICROGRID MARKET, BY OFFERING

12.1 INTRODUCTION

12.2 HARDWARE

12.2.1 POWER GENERATORS

12.2.1.1 Ability to balance supply-demand fluctuations and maintain grid stability to fuel segmental growth

12.2.2 ENERGY STORAGE SYSTEMS

12.2.2.1 Use to ensure continuous power supply and reduce reliance on grid-supplied electricity to foster segmental growth

12.2.2.2 Lithium-ion batteries

12.2.2.3 Lead-acid batteries

12.2.2.4 Flow batteries

12.2.2.5 Flywheels

12.2.2.6 Other energy storage systems

12.2.3 CONTROLLERS

12.2.3.1 Focus on delivering optimized, cost-effective, and reliable power to contribute to segmental growth

12.3 SOFTWARE

12.3.1 EMPHASIS ON DELIVERING AI-DRIVEN ENERGY OPTIMIZATION AND PREDICTIVE ANALYTICS ACROSS DISTRIBUTED ENERGY RESOURCES TO DRIVE MARKET

12.4 SERVICES

12.4.1 USE TO ENSURE OPERATIONAL RELIABILITY AND SUSTAINABILITY OF MICROGRID DEPLOYMENTS TO ACCELERATE SEGMENTAL GROWTH

12.4.2 CONSULTING & ADVISORY SERVICES

12.4.3 ENGINEERING, PROCUREMENT & CONSTRUCTION (EPC) SERVICES

12.4.4 MICROGRID OPERATION & ASSET MANAGEMENT

13 MICROGRID MARKET, BY END USER

13.1 INTRODUCTION

13.2 COMMERCIAL & INDUSTRIAL BUILDINGS

13.2.1 REQUIREMENT FOR UNINTERRUPTED ELECTRICITY TO LOWER DOWNTIME AND IMPROVE EFFICIENCY TO BOLSTER SEGMENTAL GROWTH

13.3 REMOTE AREAS

13.3.1 NEED TO ESTABLISH POWER PROJECTS IN REMOTE AREAS TO ACCELERATE SEGMENTAL GROWTH

13.4 MILITARY FACILITIES

13.4.1 FOCUS ON MAINTAINING ENERGY RESILIENCE AND ENABLING UNINTERRUPTED CRITICAL OPERATIONS TO DRIVE MARKET

13.5 GOVERNMENT BUILDINGS

13.5.1 NEED FOR UNINTERRUPTED POWER SUPPLY IN EMERGENCY RESPONSE CENTERS AND MUNICIPAL BUILDINGS TO BOOST SEGMENTAL GROWTH

13.6 UTILITIES

13.6.1 HIGH EMPHASIS ON MANAGING ENERGY USAGE AND ENHANCING POWER SUPPLY QUALITY TO AUGMENT SEGMENTAL GROWTH

13.7 INSTITUTES & CAMPUSES

13.7.1 ADOPTION OF MICROGRIDS TO REDUCE CARBON EMISSIONS AND PROMOTE ENVIRONMENTAL INITIATIVES TO SUPPORT MARKET GROWTH

13.8 HEALTHCARE FACILITIES

13.8.1 NEED FOR RELIABLE POWER SOURCE TO OPERATE LIFE-SAVING EQUIPMENT AND PROVIDE TREATMENT TO EXPEDITE SEGMENTAL GROWTH

14 MICROGRID MARKET, BY REGION

14.1 INTRODUCTION

14.2 NORTH AMERICA

14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

14.2.2 US

14.2.2.1 Increasing investment in clean energy sources for power generation to drive market

14.2.3 CANADA

14.2.3.1 Rising microgrid installations in remote areas to foster market growth

14.2.4 MEXICO

14.2.4.1 Growing support for renewable energy to ensure grid resilience to augment market growth

14.3 EUROPE

14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

14.3.2 UK

14.3.2.1 Growing emphasis on preventing waste heat generation to boost market growth

14.3.3 GERMANY

14.3.3.1 Increasing deployment of solar PV technologies to fuel market growth

14.3.4 FRANCE

14.3.4.1 Rising focus on clean energy generation to augment demand

14.3.5 ITALY

14.3.5.1 Increasing need to enhance renewable energy integration to contribute to market growth

14.3.6 SPAIN

14.3.6.1 Growing emphasis on meeting climate and renewable targets to support market growth

14.3.7 POLAND

14.3.7.1 Increasing adoption of distributed energy to contribute to market growth

14.3.8 NORDICS

14.3.8.1 High renewable penetration and strong policy support for decarbonization to drive market

14.3.9 REST OF EUROPE

14.4 ASIA PACIFIC

14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

14.4.2 AUSTRALIA

14.4.2.1 Growing emphasis on grid reliability and providing electricity to unserved areas to accelerate market growth

14.4.3 CHINA

14.4.3.1 Increasing implementation of supportive regulatory frameworks to foster market growth

14.4.4 JAPAN

14.4.4.1 Growing focus on enhancing energy resilience to contribute to market growth

14.4.5 SOUTH KOREA

14.4.5.1 Increasing effort to diversify energy mix to bolster market growth

14.4.6 INDIA

14.4.6.1 Rising renewable integration and rural electrification strategies to expedite market growth

14.4.7 INDONESIA

14.4.7.1 Growing focus on electrification using renewable sources to augment market growth

14.4.8 THAILAND

14.4.8.1 Increasing renewable penetration and smart city initiatives to fuel market growth

14.4.9 VIETNAM

14.4.9.1 Rapid expansion of economy and manufacturing sector to accelerate market growth

14.4.10 MALAYSIA

14.4.10.1 Mounting demand for resilient and clean energy systems in industries to drive market

14.4.11 REST OF ASIA PACIFIC

14.5 ROW

14.5.1 MACROECONOMIC OUTLOOK FOR ROW

14.5.2 MIDDLE EAST

14.5.2.1 Growing healthcare sector and demand for reliable power supply to contribute to market growth

14.5.2.2 GCC countries

14.5.2.3 Rest of Middle East

14.5.3 AFRICA

14.5.3.1 Rising need to improve energy access in remote areas to drive market

14.5.4 SOUTH AMERICA

14.5.4.1 Brazil

14.5.4.1.1 Requirement for decentralized electrification to support market growth

14.5.4.2 Argentina

14.5.4.2.1 Strong focus on strengthening grid resilience in underserved regions to boost market growth

14.5.4.3 Rest of South America

15 COMPETITIVE LANDSCAPE

15.1 OVERVIEW

15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

15.3 MARKET SHARE ANALYSIS, 2024

15.4 REVENUE ANALYSIS, 2020-2024

15.5 COMPANY VALUATION AND FINANCIAL METRICS

15.6 BRAND/PRODUCT COMPARISON

15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

15.7.1 STARS

15.7.2 EMERGING LEADERS

15.7.3 PERVASIVE PLAYERS

15.7.4 PARTICIPANTS

15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

15.7.5.1 Company footprint

15.7.5.2 Region footprint

15.7.5.3 End user footprint

15.7.5.4 Offering footprint

15.7.5.5 Connectivity footprint

15.7.5.6 Power rating footprint

15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024