기계 제어 시스템 시장(-2030년) : 유형(토탈 스테이션, GNSS, 레이저 스캐너, 센서), 최종 용도 기기(굴삭기, 도저, 그레이더, 스크레이퍼, 로더, 포장 시스템)

Machine Control System Market by Type (Total Stations, Global Navigation Satellite Systems (GNSS), Laser Scanners, Sensors), By End-use Equipment (Excavators, Dozers, Graders, Scrapers, Loaders, Paving Systems) - Global Forecast to 2030

상품코드:1812633

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 280 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

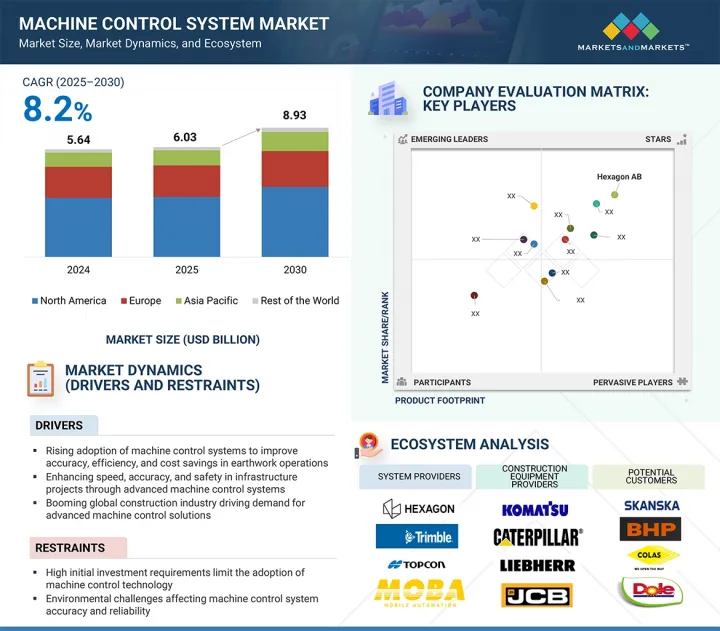

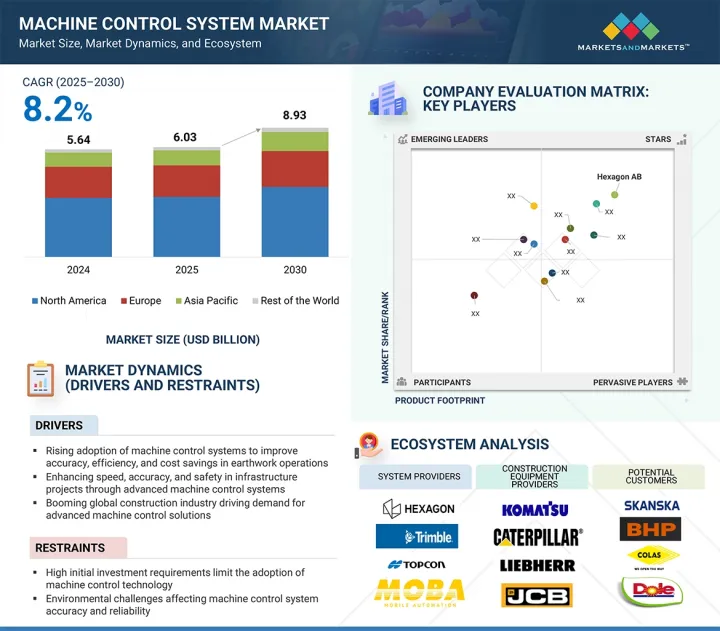

세계의 기계 제어 시스템 시장 규모는 2025년 60억 3,000만 달러에서 예측 기간 동안 CAGR 8.2%로 추이하고, 2030년에는 89억 3,000만 달러로 성장할 것으로 예측되고 있습니다.

건설, 광업, 농업에 있어서의 자동화, 정밀화, 효율화에 대한 수요 증가가 시장 성장의 원동력이 되고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

달러

부문

유형, 최종 사용 장비, 산업, 지역

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

장비 제조업체는 장비의 정확성을 높이고 손 반환을 줄이고 연료 소비를 최소화하기 위해 GNSS, 토탈 스테이션, 레이저 스캐너 및 센서와 같은 기계 제어 기술을 점차 채택하고 있습니다. 이러한 시스템은 프로젝트의 신속한 실행을 지원하고 작업 현장의 안전을 향상시킵니다. 3D 머신 가이던스, 텔레매틱스 및 OEM 통합 솔루션의 발전은 대규모 인프라 및 유틸리티 프로젝트에서 시스템 도입을 가속화하고 있습니다. 노동력 부족과 건설 비용 상승도 자동 기계로의 전환을 뒷받침하고 있습니다. 이러한 동향이 결합되어 주택, 상업, 인프라, 산업 등 각 분야에서 세계적으로 기계 제어 시스템에 대한 수요가 높아지고 있습니다.

"2024년 로더 부문이 시장에서 상당한 점유율을 차지"

2024년 로더 부문은 건설, 광업, 인프라 프로젝트에서 광범위한 사용을 지원하여 시장에서 상당한 점유율을 차지했습니다. 로더는 자재관리, 토목 작업, 현장 정지 등의 효율성과 정밀도가 불가결한 작업에 빠뜨릴 수 없는 존재입니다. 기계 제어는 실시간 피드백과 자동화를 제공하여 로더 성능을 향상시키고 자재의 과도한 취급, 연료 소비 및 운영자의 피로를 줄입니다. 특히 혼잡하거나 환경에 배려가 필요한 현장에서는 정확도가 중요하며 이러한 시스템이 큰 효과를 발휘합니다. 생산성 향상, 수복 감소, 숙련 노동력의 보다 나은 활용에 대한 수요 증가가 머신 컨트롤 대응 로더의 채용을 뒷받침하고 있습니다. GNSS, 센서, 3D 가이던스 시스템을 로더에 통합함으로써 작업 사이클의 단축과 적재 위치의 정밀도 향상이 가능해 프로젝트 전체의 효율 향상에 기여합니다. 건설사가 디지털 현장 관리와 비용 최적화에 주력하는 가운데 첨단 제어 시스템을 탑재한 로더의 역할은 계속 확대되고 있으며 시장 확대의 주요 요인이 되고 있습니다.

"아시아태평양은 2030년 시장에서 가장 큰 점유율을 차지할 전망"

아시아태평양은 급속한 인프라 개발과 정밀 건설 기술의 채택 가속화로 2030년 최대 점유율을 차지할 것으로 예측됩니다. 이 지역에서는 특히 수송, 에너지, 도시계획 프로젝트에서 토목, 정지, 굴착 작업으로 자동화 수요가 강해지고 있습니다. 중국, 인도, 일본, 한국 등의 국가에서는 정밀도 향상, 운영 지연 감소, 품질 기준 달성을 목적으로 건설 기계에 기계 제어를 적극적으로 도입하고 있습니다. 대규모 인프라 자금과 근대화 이니셔티브와 같은 정부 지원 정책도 장비 수준의 기술 통합을 뒷받침하고 있습니다. 또한 국내외 OEM은 지역 사업을 확대하고 지역 프로젝트 요구사항에 맞는 첨단 머신 컨트롤 솔루션을 제공합니다. 연료소비 절감, 귀환 최소화, 숙련 노동자 부족 대응 등의 과제에 대한 관심 증가도 자동화 시스템의 채용을 촉진하고 있습니다. 스마트 건설 전망과 경제 성장 지속을 배경으로 아시아태평양은 예측기간 말까지 세계의 기계 제어 시장에서 최대 점유율을 유지하는 태세에 있습니다.

본 보고서에서는 세계의 기계 제어 시스템 시장을 조사했으며, 시장 개요, 각종 시장 성장 영향요인 분석, 기술 및 특허 동향, 법 규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

밸류체인 분석

생태계 분석

투자 및 자금조달 시나리오

고객의 사업에 영향을 미치는 동향/혼란

기술 분석

Porter's Five Forces 분석

가격 분석

주요 이해관계자와 구매 기준

사례 연구 분석

무역 분석

특허 분석

2025-2026년 주요 회의 및 이벤트

규제 상황

AI/생성형 AI가 기계 제어 시스템 시장에 미치는 영향

2025년 미국 관세의 영향-개요

제6장 기계 제어 시스템 시장 : 유형별

토탈 스테이션

GNSS

레이저 스캐너

센서

제7장 기계 제어 시스템 시장 : 최종 용도 기기별

굴삭기

로더

그레이더

도저

스크레이퍼

포장 시스템

제8장 기계 제어 시스템 시장 : 산업별

인프라

상업

주택

공업

제9장 기계 제어 시스템 시장 : 지역별

북미

거시경제 전망

미국

캐나다

멕시코

유럽

거시경제 전망

독일

영국

프랑스

이탈리아

스페인

폴란드

북유럽

기타

아시아태평양

거시경제 전망

중국

일본

한국

호주

인도

말레이시아

인도네시아

태국

베트남

기타

기타 지역

거시경제 전망

중동

아프리카

남미

제10장 경쟁 구도

주요 진입기업의 전략/강점

수익 분석

시장 점유율 분석

기업평가와 재무지표

제품 비교

기업 평가 매트릭스 : 주요 기업

기업평가 매트릭스 : 스타트업/중소기업

경쟁 시나리오

제11장 기업 프로파일

주요 기업

MACHINE CONTROL SYSTEM PROVIDERS

CONSTRUCTION EQUIPMENT PROVIDERS

기타 기업

STONEX SRL

KATO WORKS CO. LTD.

SHANGHAI HUACE NAVIGATION TECHNOLOGY LTD.

CARLSON SOFTWARE

IDIG SYSTEM

UNICONTROL APS

제12장 부록

JHS

영문 목차

영문목차

The global machine control system market is projected to grow from USD 6.03 billion in 2025 to USD 8.93 billion by 2030, growing at a CAGR of 8.2%. The rising demand for automation, precision, and efficiency in construction, mining, and agriculture fuels market growth.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Type, End-use equipment, Vertical, and Region

Regions covered

North America, Europe, APAC, RoW

Equipment manufacturers increasingly adopt machine control technologies such as GNSS, total stations, laser scanners, and sensors to enhance equipment accuracy, reduce rework, and minimize fuel consumption. These systems support faster project execution and improve jobsite safety. Advancements in 3D machine guidance, telematics, and OEM-integrated solutions accelerate system adoption across major infrastructure and utility projects. Labor shortages and rising construction costs also prompt the shift toward automated machinery. These trends collectively boost demand for machine control systems globally across residential, commercial, infrastructure, and industrial verticals.

"Loaders segment accounted for considerable share of the machine control system market in 2024"

In 2024, the loaders segment accounted for a considerable share of the machine control system market, supported by their widespread use in construction, mining, and infrastructure projects. Loaders are essential for material handling, earthmoving, and site preparation tasks, where efficiency and precision are critical. Machine control systems enhance loader performance by providing real-time feedback and automation, helping reduce material overhandling, fuel consumption, and operator fatigue. These systems are especially useful in crowded or sensitive jobsite environments where accuracy is vital. The growing demand for improved productivity, reduced rework, and better utilization of skilled labor is driving the adoption of machine-controlled loaders. Integration of GNSS, sensors, and 3D guidance systems into loaders enables faster cycle times and improved load placement, contributing to overall project efficiency. As construction companies focus on digital site management and cost optimization, the role of loaders equipped with advanced control systems continues to grow, making them a key contributor to market expansion.

"Residential segment to hold significant share of machine control system market 2030"

By 2030, the residential segment is expected to hold a significant share of the machine control system market, driven by rapid urbanization, housing demand, and growing emphasis on efficient and sustainable construction practices. Governments and private developers across emerging and developed economies invest heavily in large-scale residential projects, smart city initiatives, and affordable housing programs. This growing activity increases the demand for advanced machinery equipped with machine control technologies that offer greater accuracy, reduced labor dependency, and faster project execution. Machine control systems integrated into end-use equipment such as excavators, loaders, and graders enable precise site leveling, foundation work, and grading tasks in residential construction, reducing rework and improving build quality. Adopting GNSS, 3D guidance, and real-time monitoring in compact and mid-sized machines makes these systems suitable for urban and space-constrained sites. As the residential sector continues to adopt digital construction methods, machine control technologies will be crucial in delivering cost-effective and timely housing solutions.

"Asia Pacific to hold largest share of machine control system market in 2030"

Asia Pacific is projected to hold the largest machine control system market share in 2030, driven by the rapid scale of infrastructure development and accelerated adoption of precision construction technologies. The region is witnessing strong demand for automation in earthmoving, grading, and excavation activities, particularly across transport, energy, and urban planning projects. China, India, Japan, and South Korea are a few countries in the region that are actively incorporating machine control systems into construction machinery to improve accuracy, reduce operational delays, and meet quality standards. Supportive government policies, including large-scale infrastructure funding and modernization initiatives, reinforce technology integration at the equipment level. Additionally, local and global OEMs are expanding their regional operations, offering advanced machine control solutions tailored to regional project requirements. Increasing emphasis on reducing fuel consumption, minimizing rework, and addressing skilled labor shortages further encourages contractors to adopt automated systems. With a strong outlook for smart construction and continued economic development, Asia Pacific is well-positioned to maintain the largest share of the global machine control system market by the end of the forecast period.

Extensive primary interviews were conducted with key industry experts in the machine control system market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type - Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

By Designation - Managers - 25%, C- level Executives - 35%, and Others - 40%

By Region - Asia Pacific - 30%, Europe - 20%, North America - 45%, and RoW - 5%

The machine control system market is dominated by a few globally established players, such as Hexagon AB (Sweden), Trimble Inc. (US), Topcon Corporation (Japan), MOBA Mobile Automation AG (Germany), and Hemisphere GNSS (US).

The study includes an in-depth competitive analysis of these key players in the machine control system market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the machine control system market. It forecasts its size by type (total stations, global satellite systems (GNSS), laser scanners and sensors), by end-use equipment (excavators, loaders, graders, dozers, scrapers and paving systems), and by vertical (infrastructure, commercial, residential and industrial). It also discusses the market's drivers, restraints, opportunities, and challenges. It provides a detailed market analysis across four key regions (North America, Europe, Asia Pacific, and RoW). The report includes a review of the supply chain and the competitive landscape of key players operating in the machine control system ecosystem.

Key Benefits of Buying the Report:

Analysis of key drivers (rising adoption of machine control systems to improve accuracy, efficiency, and cost savings in earthwork operations, enhancing speed, accuracy, and safety in infrastructure projects through advanced machine control systems, booming global construction industry driving demand for advanced machine control solutions), restraints (high initial investment requirements limit adoption of machine control technology, environmental challenges affecting machine control system accuracy and reliability), opportunities (rising demand for 3D modeling and scanning driving technological advancements in machine control systems, infrastructure investments in developing regions fueling demand for machine control systems), challenges (lack of skilled workforce and training needs hamper adoption of machine control systems)

Service Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product launches in the machine control system market

Market Development: Comprehensive information about lucrative markets by analyzing the machine control system market across varied regions

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the machine control system market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Hexagon AB (Sweden), Trimble Inc. (US), Topcon Corporation (Japan), MOBA Mobile Automation AG (Germany), and Hemisphere GNSS (US).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of major secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of primary interview participants

2.1.3.2 Key industry insights

2.1.3.3 Key data from primary sources

2.1.3.4 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up approach (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down approach (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MACHINE CONTROL SYSTEM MARKET

4.2 MACHINE CONTROL SYSTEM MARKET, BY TYPE

4.3 MACHINE CONTROL SYSTEM MARKET, BY END-USE EQUIPMENT

4.4 MACHINE CONTROL SYSTEM MARKET, BY VERTICAL

4.5 MACHINE CONTROL SYSTEM MARKET IN NORTH AMERICA, BY VERTICAL AND COUNTRY

4.6 MACHINE CONTROL SYSTEM MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Optimized earthwork operations with advanced technologies

5.2.1.2 Need to monitor and control construction equipment to ensure optimal performance

5.2.1.3 Expanding global construction industry

5.2.2 RESTRAINTS

5.2.2.1 High installation and integration costs

5.2.2.2 Performance-related issues in harsh weather conditions

5.2.3 OPPORTUNITIES

5.2.3.1 Rising demand for 3D data in construction industry

5.2.3.2 Infrastructure development in emerging economies

5.2.4 CHALLENGES

5.2.4.1 Lack of technical knowledge

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 INVESTMENT AND FUNDING SCENARIO

5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 GNSS

5.7.1.2 IMUs

5.7.1.3 Real-time kinematic (RTK) positioning

5.7.2 ADJACENT TECHNOLOGIES

5.7.2.1 Digital twin

5.7.2.2 Edge AI processing

5.7.2.3 Fleet telematics integration

5.7.3 COMPLEMENTARY TECHNOLOGIES

5.7.3.1 5G

5.7.3.2 Building information modeling

5.8 PORTER'S FIVE FORCES ANALYSIS

5.8.1 INTENSITY OF COMPETITIVE RIVALRY

5.8.2 BARGAINING POWER OF SUPPLIERS

5.8.3 BARGAINING POWER OF BUYERS

5.8.4 THREAT OF SUBSTITUTES

5.8.5 THREAT OF NEW ENTRANTS

5.9 PRICING ANALYSIS

5.9.1 PRICING RANGE OF MACHINE CONTROL SYSTEMS, BY KEY PLAYER, 2024

5.9.2 AVERAGE SELLING PRICE TREND OF MACHINE CONTROL SYSTEMS, BY TYPE, 2021-2024

5.9.3 AVERAGE SELLING PRICE TREND OF TOTAL STATIONS, BY REGION, 2021-2024

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDY ANALYSIS

5.11.1 FAM CONSTRUCTION UTILIZES LEICA 3D SCANNING TO ENHANCE SITE DATA ACCURACY AND PROJECT MONITORING

5.11.2 WILMINGTON GIS TECHNICIAN USES GNSS RECEIVER TO IMPROVE WATER MAIN DOCUMENTATION AND PROJECT DELIVERY

5.11.3 SCCS SURVEY AND BUCKINGHAM GROUP MAXIMIZE CONSTRUCTION EFFICIENCY WITH LEICA GEOSYSTEMS HARDWARE AND 3D CONTROL

5.11.4 ZIAJKA ZBIGNIEW COMPANY DEPLOYS TRIMBLE 3D MACHINE CONTROL TO ENHANCE FLOOD PROTECTION AND REDUCE PROJECT COSTS IN POLAND

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 842952)

5.12.2 EXPORT SCENARIO (HS CODE 842952)

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 REGULATORY LANDSCAPE

5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15.2 STANDARDS

5.16 IMPACT OF AI/GEN AI ON MACHINE CONTROL SYSTEM MARKET

5.16.1 INTRODUCTION

5.16.2 IMPACT OF AI/GEN AI ON VERTICALS

5.16.2.1 Infrastructure

5.16.2.2 Commercial

5.16.2.3 Residential

5.16.2.4 Industrial

5.16.3 AI USE CASES

5.16.4 FUTURE OF AI/GEN AI IN MACHINE CONTROL ECOSYSTEM

5.17 IMPACT OF 2025 US TARIFF - OVERVIEW

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRY/REGION

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON VERTICALS

6 MACHINE CONTROL SYSTEM MARKET, BY TYPE

6.1 INTRODUCTION

6.2 TOTAL STATIONS

6.2.1 PREVENTION OF COSTLY REWORKS AND ENHANCED PRECISION TO FUEL MARKET GROWTH

6.3 GNSS

6.3.1 NEED TO ENHANCE SITUATIONAL AWARENESS FOR FIELD OPERATORS TO SUPPORT MARKET GROWTH

6.4 LASER SCANNERS

6.4.1 GROWING NEED FOR DETAILED VISUALIZATIONS OF STRUCTURAL ELEMENTS TO DRIVE MARKET

6.5 SENSORS

6.5.1 NEED TO IMPROVE OVERALL MACHINE AUTOMATION IN CONSTRUCTION SECTOR TO BOOST DEMAND

7 MACHINE CONTROL SYSTEM MARKET, BY END-USE EQUIPMENT

7.1 INTRODUCTION

7.2 EXCAVATORS

7.2.1 INCREASING APPLICATIONS IN DIGGING, MATERIAL HANDLING, AND DEMOLITION TO BOOST DEMAND

7.3 LOADERS

7.3.1 ONGOING ADVANCEMENTS IN LOADER SOLUTION TECHNOLOGIES TO DRIVE MARKET

7.4 GRADERS

7.4.1 ENHANCED ACCURACY AND REDUCED REWORK COSTS TO FOSTER MARKET GROWTH

7.5 DOZERS

7.5.1 ABILITY TO FUNCTION IN CHALLENGING CONDITIONS TO SUPPORT MARKET GROWTH

7.6 SCRAPERS

7.6.1 APPLICATION IN LARGE-SCALE EARTHMOVING PROJECTS TO DRIVE MARKET

7.7 PAVING SYSTEMS

7.7.1 ADVANCEMENT OF PAVING SYSTEMS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

8 MACHINE CONTROL SYSTEM MARKET, BY VERTICAL

8.1 INTRODUCTION

8.2 INFRASTRUCTURE

8.2.1 GROWING NUMBER OF AIRPORTS, DAMS, HYDROELECTRIC PROJECTS, ROADS, AND BRIDGES TO SPUR DEMAND

8.3 COMMERCIAL

8.3.1 INCORPORATION OF 3D MODELING AND VISUALIZATION CAPABILITIES TO DRIVE MARKET

8.4 RESIDENTIAL

8.4.1 EXPANSION OF MEGACITIES AND RAPID URBANIZATION TO FOSTER MARKET GROWTH

8.5 INDUSTRIAL

8.5.1 GROWING NEED TO ENHANCE SAFETY DURING OFFSHORE CONSTRUCTION AND UNDERWATER OPERATIONS TO DRIVE MARKET

9 MACHINE CONTROL SYSTEM MARKET, BY REGION

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

9.2.2 US

9.2.2.1 Emphasis on infrastructure projects to foster market growth

9.2.3 CANADA

9.2.3.1 Government-led investments in construction of public transit infrastructure to fuel market growth

9.2.4 MEXICO

9.2.4.1 Rapid urbanization and industrialization to support market growth

9.3 EUROPE

9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

9.3.2 GERMANY

9.3.2.1 Replacement of old buildings with energy-efficient green buildings to drive market

9.3.3 UK

9.3.3.1 Rising focus on expanding transportation infrastructure to boost demand

9.3.4 FRANCE

9.3.4.1 Growing emphasis on developing and modernizing rail infrastructure to foster market growth

9.3.5 ITALY

9.3.5.1 Adoption of digital tools to meet project timelines to fuel market growth

9.3.6 SPAIN

9.3.6.1 Development of coastal infrastructure to support market growth

9.3.7 POLAND

9.3.7.1 Rising focus on expanding roads, railways, and energy infrastructure to boost demand

9.3.8 NORDICS

9.3.8.1 Adoption of favorable regulations and digital construction mandates to benefit market

9.3.9 REST OF EUROPE

9.4 ASIA PACIFIC

9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

9.4.2 CHINA

9.4.2.1 High investments in road infrastructure development to fuel market growth

9.4.3 JAPAN

9.4.3.1 Emphasis on developing sustainable construction to boost demand

9.4.4 SOUTH KOREA

9.4.4.1 Focus on smart construction and infrastructure digitalization to foster market growth

9.4.5 AUSTRALIA

9.4.5.1 Expansion of urban infrastructure and transportation projects to support market growth

9.4.6 INDIA

9.4.6.1 Emphasis on redeveloping roads and highways to boost demand

9.4.7 MALAYSIA

9.4.7.1 Focus on digitalizing construction sector to support market growth

9.4.8 INDONESIA

9.4.8.1 Significant government-led investments in infrastructure to fuel market growth

9.4.9 THAILAND

9.4.9.1 Increasing expenditure on transport infrastructure to support market growth

9.4.10 VIETNAM

9.4.10.1 Strong urbanization trends to drive market

9.4.11 REST OF ASIA PACIFIC

9.5 ROW

9.5.1 MACROECONOMIC OUTLOOK FOR ROW

9.5.2 MIDDLE EAST

9.5.2.1 Saudi Arabia

9.5.2.1.1 Significant investments in housing and infrastructure development to drive market

9.5.2.2 UAE

9.5.2.2.1 Expansion of urban areas to support market growth

9.5.2.3 Bahrain

9.5.2.3.1 Investment in large-scale infrastructure to boost demand

9.5.2.4 Kuwait

9.5.2.4.1 Focus on digitalization in infrastructure to drive market

9.5.2.5 Qatar

9.5.2.5.1 Ongoing digital transformation in construction sector to fuel market growth

9.5.2.6 Oman

9.5.2.6.1 Development of major highway and logistics corridor projects to foster market growth

9.5.2.7 Rest of Middle East

9.5.3 AFRICA

9.5.3.1 South Africa

9.5.3.1.1 Rising infrastructure investments to drive market

9.5.3.2 Rest of Africa

9.5.4 SOUTH AMERICA

9.5.4.1 Brazil

9.5.4.1.1 Investment in highway modernization, sanitation, and energy infrastructure to boost demand

9.5.4.2 Argentina

9.5.4.2.1 Integration of advanced technologies to improve delivery speed to drive market

9.5.4.3 Rest of South America

10 COMPETITIVE LANDSCAPE

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3 REVENUE ANALYSIS, 2020-2024

10.4 MARKET SHARE ANALYSIS, 2024

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 PRODUCT COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 PERVASIVE PLAYERS

10.7.3 EMERGING LEADERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 Type footprint

10.7.5.4 Vertical footprint

10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024