공구용 플라스틱 시장 : 유형별, 용도별, 기능성별, 최종 이용 산업별, 지역별 예측(-2030년)

Tools Plastic Market by Type, Application, End-use Industry, and Region - Global Forecast to 2030

상품코드:1811727

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 269 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

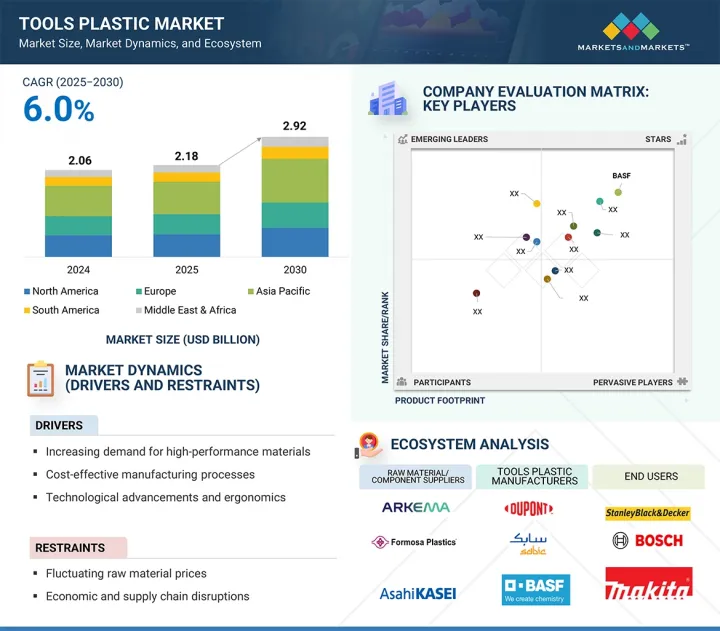

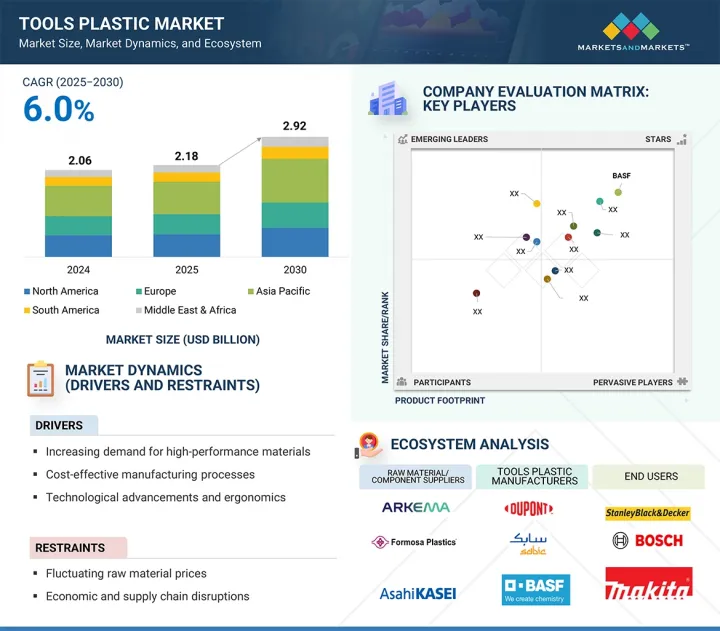

공구용 플라스틱 시장 규모는 예측 기간 동안 6.0%의 연평균 성장률(CAGR)로 확대되어 2025년 21억 8,000만 달러에서 2030년에 29억 2,000만 달러에 이를 전망입니다.

공구용 플라스틱 시장은 자동차, 포장, 건설 및 전자 산업에서 경량화, 내구성 및 비용 효율성을 갖춘 소재에 대한 수요 증가에 의해 촉진되고 있습니다. 폴리머 개질 분야의 최근 발전으로 인장 강도, 유연성, 내열성 등 플라스틱 특성이 향상되어 더 다양한 공구 용도의 요구를 충족시키고 있습니다.

조사 범위

조사 대상 연도

2022-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러)/킬로톤

부문

유형별, 용도별, 기능성별, 최종 이용 산업별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카

또한 지속 가능성에 주력하는 변화하는 소비자 선호도와 정부 규제는 재활용 가능 및 바이오 기반 플라스틱 분야의 혁신을 촉진하여 제조업체에게 새로운 기회를 창출하고 있습니다. 개발도상국의 급속한 도시화와 같은 요인들은 플라스틱 기반 공구 및 포장 재료 사용을 지속적으로 촉진될 것입니다. 마찬가지로 전자상거래의 부상은 더 가볍고 효율적인 플라스틱 포장 솔루션에 대한 수요를 증가시킵니다. 자동차 산업에서는 제조사들이 연비 향상과 탄소 배출 감축을 위해 차량 경량화를 점점 더 목표로 삼고 있어 플라스틱 사용량이 증가하고 있습니다. 또한 기업들은 급속한 산업화와 낮은 생산 비용이 플라스틱 시장 성장의 강력한 촉진요인으로 작용하는 아시아태평양 지역에 플라스틱 제품에 대한 투자를 크게 확대하고 있습니다.

폴리카보네이트는 높은 강도, 낮은 무게, 내충격성을 독특하게 결합한 특성으로 인해 공구용 플라스틱 시장에서 가장 빠르게 성장하는 유형 중 하나입니다. 내구성 있는 수공구 및 전동 공구 하우징, 안전 고글, 보호용 실드 등을 제작하는 데 사용됩니다. 폴리카보네이트는 열과 응력 하에서도 높은 치수 안정성을 유지하므로 건설 및 제조업과 같이 극한 작업 부하가 가해지는 고강도 환경에서 작동하는 공구에도 탁월한 선택입니다. 투명성과 성형성은 최근 공구의 디자인 유연성과 미적 옵션을 확대합니다. 산업계가 기존 공구에서 벗어나 인체공학적으로 설계되고 안전하며 효율적인 공구를 요구함에 따라, 제조업체들은 성능 향상과 최종 사용자 요구 및 공구 기능성을 모두 충족하는 혁신 개발을 위해 폴리카보네이트를 선택하고 있습니다. 또한 자외선 차단 및 난연 등급과 같은 새롭게 개선된 배합은 성장 기회를 더욱 확대합니다.

전동 공구는 산업, 건설 및 가정 분야에서 널리 사용되기 때문에 공구 플라스틱 시장 내에서 가장 중요한 용도 중 하나입니다. 전동 공구는 ABS, 폴리카보네이트, 나일론과 같은 플라스틱이 효과적으로 제공하는 내충격성, 내열성, 내마모성을 갖춘 견고하고 가벼운 소재를 필요로 합니다. 플라스틱은 전동 공구의 무게를 크게 감축하여 취급과 운반을 용이하게 합니다. 전문 작업 및 DIY 프로젝트에서 배터리식 또는 무선 전동 공구의 사용 증가로 전자 부품을 안전하고 확실하게 보호할 수 있는 고성능 플라스틱에 대한 수요가 더욱 촉진되었습니다. 또한 전 세계적으로 건설 및 제조 활동이 증가함에 따라 전동 공구에 대한 수요는 꾸준히 유지되고 있습니다. 이러한 동향이 인체공학적으로 설계된, 열 절연 또는 충격 흡수 하우징을 선호하는 방향으로 지속됨에 따라 플라스틱은 금속에 대한 선호되는 대안이 되었습니다. 궁극적으로 공구 설계 및 소재 분야의 지속적인 발전은 공구 플라스틱 시장에서 전동 공구의 중요성을 계속해서 강화하고 있습니다.

북미는 강력한 제조 기반, 기술적 발전, 최종 사용 산업의 높은 수요로 인해 두 번째로 큰 공구 플라스틱 시장입니다. 이 지역은 ABS, 폴리카보네이트, 나일론과 같은 엔지니어링 플라스틱의 강도, 내충격성, 경량성 덕분에 이를 크게 의존하는 전동 공구, 수공구, 의료 장비의 주요 생산지입니다. 미국과 캐나다의 건설 및 자동차 부문은 지속적으로 저렴하고 내구성 있는 플라스틱 공구를 필요로 하는 확립된 산업을 보유하고 있습니다. DIY 프로젝트, 주택 리모델링, 도시 개발 사업에 대한 관심이 증가하면서 시장 성장이 지속되고 있습니다. 해당 지역에서 운영되는 전 세계 플라스틱 제조사 및 공구 생산사는 고성능 친환경 플라스틱 개발을 가능케 하는 고급 연구 시설의 혜택을 누리고 있습니다. 경량화 및 재활용 가능한 공구 소재에 대해 규제가 주력하면서 특수 플라스틱 채택이 더욱 촉진됩니다. 이러한 요인들이 결합되어 북미는 공구용 플라스틱의 핵심 시장이자 플라스틱 혁신의 중심지로 자리매김하고 있습니다.

본 보고서에서는 세계의 공구용 플라스틱 시장에 대해 조사했으며, 유형별, 용도별, 기능성별, 최종 이용 산업별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

거시경제지표

밸류체인 분석

규제 상황

무역 분석

생태계 분석

고객사업에 영향을 주는 동향 및 혼란

사례 연구 분석

기술 분석

가격 분석

주된 회의 및 이벤트(2025-2026년)

특허 분석

AI/생성형 AI가 공구용 플라스틱 시장에 미치는 영향

투자 및 자금조달 시나리오

미국 관세가 공구용 플라스틱 시장에 미치는 영향(2025년)

제6장 공구용 플라스틱 시장(유형별)

소개

아크릴로니트릴부타디엔스티렌(ABS)

나일론(폴리아미드-PA)

폴리카보네이트(PC)

폴리프로필렌(PP)

폴리염화비닐(PVC)

고밀도 폴리에틸렌(HDPE)

기타

제7장 공구용 플라스틱 시장(용도별)

소개

산업용(전문용)

상업용

주거용(DIY)

제8장 공구용 플라스틱 시장(기능성별)

소개

전동 공구

기계 공구

제9장 공구용 플라스틱 시장(최종 이용 산업별)

소개

건설

의료

자동차

농업/원예/경작

제조

항공우주

조선

기타

제10장 공구용 플라스틱 시장(지역별)

소개

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

기타

아시아태평양

중국

일본

인도

한국

기타

중동 및 아프리카

GCC 국가

남아프리카

기타

남미

브라질

아르헨티나

기타

제11장 경쟁 구도

개요

주요 진입기업의 전략

수익 분석(2022-2024년)

시장 점유율 분석(2024년)

기업평가와 재무지표

브랜드, 제품 비교 분석

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타트업, 중소기업(2024년)

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

BASF

COVESTRO AG

DUPONT

LYONDELLBASELL INDUSTRIES HOLDINGS BV

LG CHEM

SABIC

ASAHI KASEI CORPORATION

ARKEMA

FORMOSA PLASTICS CORPORATION

MITSUBISHI CHEMICAL GROUP CORPORATION

기타 기업

ADVANSIX

TRINSEO

ENVALIOR

ROCHLING SE & CO. KG

POLYPLASTICS CO. LTD.

INEOS

ENSINGER

GRAND PACIFIC PETROCHEMICAL CORPORATION

TRIDENT PLASTICS INC.

CENTROPLAST

POLYPLASTY SRO

RTP COMPANY

ESTER

CELANESE CORPORATION

JOSLYN MANUFACTURING

제13장 부록

HBR

영문 목차

영문목차

The tools plastic market is projected to reach USD 2.92 billion by 2030 from USD 2.18 billion in 2025, at a CAGR of 6.0% during the forecast period. The tools plastic market is driven by the growing demand for lightweight, durable, and cost-effective materials in the automotive, packaging, construction, and electronics industries. Recent advancements in polymer modification have enhanced plastic properties like tensile strength, flexibility, and thermal resistance to meet the needs of a wider range of tool applications.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million)/ Volume (Kiloton)

Segments

Type, Application, End-use Industry, and Region

Regions covered

North America, Europe, Asia Pacific, South America, and Middle East & Africa

Additionally, changing consumer preferences and government regulations focused on sustainability are encouraging innovation in recyclable and bio-based plastics, creating new opportunities for manufacturers. Factors such as rapid urbanization in developing economies will continue to boost the use of plastic-based tools and packaging materials. Similarly, the rise of e-commerce increases the demand for lighter, more efficient plastic packaging solutions. In the automotive industry, manufacturers are increasingly aiming to reduce vehicle weight to improve fuel efficiency and lower carbon emissions, leading to higher use of plastics. Moreover, companies are heavily investing in plastic products in the Asia Pacific region, where rapid industrialization and low production costs serve as strong motivators for growth in the plastic market.

"Polycarbonate to be fastest-growing type in tools plastic market during forecast period"

Polycarbonate is one of the fastest-growing types in the tool plastics market due to its unique combination of high strength, low weight, and impact resistance. It is used to create durable hand tools and housings for power tools, safety goggles, and protective shields, among others. With high-dimensional stability under heat and stress, polycarbonate is also a great choice for tools that operate in high-stress situations with extreme workloads, such as in construction and manufacturing. Its clarity and formability allow for greater design flexibility and aesthetic options for modern tools. As industries move away from traditional tools and demand more ergonomically designed, safe, and efficient tools, manufacturers are turning to polycarbonate to enhance performance and develop innovations that meet both end-user needs and tool functionality. Additionally, new and improved formulations, such as UV-resistant and flame-retardant grades, provide even more opportunities for growth.

"Power tools to be largest application in tools plastic market during forecast period"

Power tools are among the most important applications in the tools plastic industry because they are widely used in industrial, construction, and domestic sectors. Power tools require tough, lightweight materials, and resistant to impact, heat, and wear-qualities that plastics like ABS, polycarbonate, and nylon effectively provide. Plastics greatly reduce the weight of power tools, making them easier to handle and carry. The increasing use of battery-operated or cordless power tools in trades and DIY projects has further boosted the demand for high-performance plastics that can safely and securely enclose electronic components. Additionally, the demand for power tools remains steady with a rise in building and manufacturing activities worldwide. As these trends continue to favor ergonomically designed, heat-insulated, or shock-absorbing housings, plastics have become a preferred alternative to metals. Ultimately, ongoing advancements in tool design and materials continue to reinforce the importance of power tools in the tools plastic market.

"North America to be second-largest tools plastic market during forecast period"

North America is the second-largest tools plastic market due to its strong manufacturing base, technological advancements, and high demand in end-use industries. The region is home to leading producers of power tools, hand tools, and medical equipment that heavily rely on engineering plastics such as ABS, polycarbonate, and nylon because of their strength, impact resistance, and light weight. The construction and automotive sectors in the US and Canada have established industries that continuously require affordable, durable plastic tools. Growing interest in do-it-yourself projects, home remodeling, and city development initiatives fuels ongoing market growth. Global plastic manufacturers and tool producers operating in the region benefit from advanced research facilities that enable the development of high-performance, eco-friendly plastics. Increasing regulatory focus on lightweight, recyclable tool materials further drives the adoption of specialized plastics. Together, these factors position North America as a key market for tool plastics and a hub for plastic innovation.

Extensive primary interviews were conducted to determine and verify the market size for several segments and sub-segments, and the information was gathered through secondary research.

The breakdown of primary interviews is given below:

By Department: Tier 1: 40%, Tier 2: 25%, and Tier 3: 35%

By Designation: C Level: 35%, Director Level: 30%, and Executives: 35%

By Region: North America: 25%, Europe: 45%, Asia Pacific: 20%, South America: 5%, Middle East & Africa 5%

DuPont (US), BASF (Germany), Eastman Chemical Company (US), Covestro AG (Germany), Solvay (Belgium), LG Chem (South Korea), SABIC (Saudi Arabia), Dow (US), Exxon Mobil Corporation (US), and LyondellBasell Industries Holdings B.V. (US), among others are some of the key players in the tools plastic market.

The study includes an in-depth competitive analysis of these key players in the authentication and brand

protection market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The market study covers the tools plastic market across various segments. It aims to estimate the market size and growth potential in different segments based on type, application, end-use industry, and region. The study also includes an in-depth competitive analysis of key market players, their company profiles, key observations related to their products and offerings, recent developments they have undertaken, and the main growth strategies they have adopted to strengthen their position in the tools plastic market.

Key Benefits of Buying the Report

The report is designed to help market leaders and new entrants approximate the revenue figures of the overall tools plastic market, as well as its segments and sub-segments. It aims to assist stakeholders in understanding the competitive landscape, gaining insights to enhance their business position, and planning effective go-to-market strategies. Additionally, the report provides stakeholders with insights into the market's current trends and key factors such as drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (Increasing demand for high-performance materials, Cost-effective manufacturing processes, Technological advancements and ergonomics), restraints (Fluctuating raw material prices, Economic and supply chain disruptions), opportunities (Innovation in sustainable and bio-based plastics, Rising industrialization in emerging markets), and challenges (Environmental issues and regulatory restrictions, Competition from metal substitutes).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the tools plastic market

Market Development: Comprehensive information about lucrative markets - the report analyses the tools plastic market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the tools plastic market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like DuPont (US), BASF (Germany), Eastman Chemical Company (US), Covestro AG (Germany), Solvay (Belgium), LG Chem (South Korea), SABIC (Saudi Arabia), Dow (US), Exxon Mobil Corporation (US), and LyondellBasell Industries Holdings B.V. (US) among others are the top manufacturers covered in the tools plastic market report.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants-demand and supply side

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 FORECAST NUMBER CALCULATION

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 ASSUMPTIONS

2.7 LIMITATIONS AND RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TOOL PLASTICS MARKET

4.2 TOOL PLASTICS MARKET, BY TYPE

4.3 TOOL PLASTICS MARKET, BY FUNCTIONALITY

4.4 TOOL PLASTICS MARKET, BY APPLICATION

4.5 TOOL PLASTICS MARKET, BY END-USE INDUSTRY

4.6 TOOL PLASTICS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Expansion of key end-use industries

5.2.1.2 Technological advancements and cordless revolution

5.2.1.3 Growing do-it-yourself (DIY) culture

5.2.2 RESTRAINTS

5.2.2.1 Volatility in raw material prices

5.2.2.2 High cost of engineering plastics and tooling

5.2.3 OPPORTUNITIES

5.2.3.1 Growth in sustainable and recycled plastics

5.2.3.2 Innovation in high-performance applications

5.2.4 CHALLENGES

5.2.4.1 Stringent environmental regulations and public scrutiny

5.2.4.2 Competition from substitute materials

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 THREAT OF NEW ENTRANTS

5.3.2 THREAT OF SUBSTITUTES

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GLOBAL GDP TRENDS

5.6 VALUE CHAIN ANALYSIS

5.7 REGULATORY LANDSCAPE

5.7.1 NORTH AMERICA

5.7.1.1 US

5.7.2 ASIA PACIFIC

5.7.3 EUROPE

5.7.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.8 TRADE ANALYSIS

5.8.1 IMPORT SCENARIO (HS CODE 3926)

5.8.2 EXPORT SCENARIO (HS CODE 3926)

5.9 ECOSYSTEM ANALYSIS

5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.11 CASE STUDY ANALYSIS

5.11.1 BASF COLLABORATED WITH BOSCH TO ENGINEER HOUSING FOR A CORDLESS HAMMER DRILL

5.11.2 COVESTRO AG PROVIDES BAYBLEND BLENDS IN PORTABLE POWER STATION HOUSINGS

5.12 TECHNOLOGY ANALYSIS

5.12.1 KEY TECHNOLOGIES

5.12.1.1 Injection molding

5.12.1.2 3D printing

5.12.2 COMPLEMENTARY TECHNOLOGIES

5.12.2.1 Artificial Intelligence (AI)

5.12.2.2 Nanotechnology

5.13 PRICING ANALYSIS

5.13.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

5.13.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY, 2024

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 PATENT ANALYSIS

5.15.1 METHODOLOGY

5.15.2 DOCUMENT TYPES

5.15.3 PUBLICATION TRENDS

5.15.4 INSIGHTS

5.15.5 LEGAL STATUS OF PATENTS

5.15.6 JURISDICTION ANALYSIS

5.15.7 TOP APPLICANTS

5.16 IMPACT OF AI/GEN AI ON TOOL PLASTICS MARKET

5.17 INVESTMENT AND FUNDING SCENARIO

5.18 IMPACT OF 2025 US TARIFF ON TOOL PLASTICS MARKET

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 PRICE IMPACT ANALYSIS

5.18.4 IMPACT ON KEY COUNTRIES/REGIONS

5.18.4.1 North America

5.18.4.2 Europe

5.18.4.3 Asia Pacific

5.18.5 IMPACT ON END-USE INDUSTRIES

6 TOOL PLASTICS MARKET, BY TYPE

6.1 INTRODUCTION

6.2 ACRYLONITRILE BUTADIENE STYRENE (ABS)

6.2.1 EXCEPTIONAL IMPACT RESISTANCE, STRUCTURAL STRENGTH, AND RIGIDITY TO DRIVE MARKET

6.3 NYLON (POLYAMIDE - PA)

6.3.1 EXCEPTIONAL STRENGTH, DURABILITY, AND OUTSTANDING RESISTANCE TO HEAT, WEAR, AND CHEMICALS TO FUEL GROWTH

6.4 POLYCARBONATE (PC)

6.4.1 EXCEPTIONAL TOUGHNESS TO BOOST MARKET FOR SAFETY-CRITICAL AND PRECISION COMPONENTS

6.5 POLYPROPYLENE (PP)

6.5.1 HIGH DURABILITY AND RESISTANCE TO CHEMICALS, STRESS, AND CRACKING TO PROPEL GROWTH

6.6 POLYVINYL CHLORIDE (PVC)

6.6.1 SIGNIFICANT APPLICATIONS IN MEDICAL SECTOR TO SUPPORT MARKET GROWTH

6.7 HIGH DENSITY POLYETHYLENE (HDPE)

6.7.1 DEMAND FROM GARDENING AND LANDSCAPING SECTOR TO FUEL MARKET

6.8 OTHER TYPES

7 TOOL PLASTICS MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 INDUSTRIAL (PROFESSIONAL)

7.2.1 DEMAND FROM PROFESSIONALS ACROSS WIDE RANGE OF INDUSTRIES TO DRIVE MARKET

7.3 COMMERCIAL

7.3.1 HIGH MECHANICAL STRENGTH, HEAT RESISTANCE, AND ELECTRICAL INSULATION TO BOOST MARKET

7.4 RESIDENTIAL (DIY)

7.4.1 STRENGTH, CHEMICAL RESISTANCE, AND COMPETITIVE PRICING TO PROPEL MARKET GROWTH

8 TOOL PLASTICS MARKET, BY FUNCTIONALITY

8.1 INTRODUCTION

8.2 POWER TOOLS

8.2.1 DEMAND FOR PROTECTION WITHIN DURABLE, IMPACT-RESISTANT, AND LIGHTWEIGHT HOUSING TO DRIVE MARKET

8.3 MECHANICAL TOOLS

8.3.1 CRUCIAL ROLE IN IMPROVING USABILITY, SAFETY, AND DURABILITY TO BOOST MARKET

9 TOOL PLASTICS MARKET, BY END-USE INDUSTRY

9.1 INTRODUCTION

9.2 CONSTRUCTION

9.2.1 ROBUST AND DURABLE TOOLS WITHSTANDING HARSH JOB SITE CONDITIONS TO BOOST MARKET

9.3 MEDICAL

9.3.1 DEMAND FOR HYGIENE, STERILITY, AND PREVENTION OF CROSS-CONTAMINATION TO PROPEL MARKET

9.4 AUTOMOTIVE

9.4.1 INCREASING DEMAND FOR HAND TOOLS WITH ERGONOMIC PLASTIC GRIPS FOR BETTER MANOEUVRABILITY IN TIGHT SPACES TO FUEL MARKET GROWTH

9.5 AGRICULTURE/GARDENING/FARMING

9.5.1 RESISTANCE TO MOISTURE AND CHEMICALS FROM FERTILIZERS AND PESTICIDES TO SUPPORT DEMAND

9.6 MANUFACTURING

9.6.1 REQUIREMENT FOR EFFICIENCY, PRECISION, AND INTEGRATION OF AUTOMATION TO DRIVE MARKET

9.7 AEROSPACE

9.7.1 EXCEPTIONAL PRECISION, RELIABILITY, AND SAFETY TO SUPPORT MARKET GROWTH

9.8 SHIPBUILDING

9.8.1 HIGH DURABILITY AND RESISTANCE TO ENVIRONMENTAL DEGRADATION TO PROPEL MARKET

9.9 OTHER END-USE INDUSTRIES

10 TOOL PLASTICS MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 US

10.2.1.1 Rising DIY culture to boost demand

10.2.2 CANADA

10.2.2.1 Strong construction sector to drive market

10.2.3 MEXICO

10.2.3.1 Manufacturing hub for automotive and electronics to fuel demand

10.3 EUROPE

10.3.1 GERMANY

10.3.1.1 Automotive and machine tool sectors to drive demand

10.3.2 FRANCE

10.3.2.1 Government support for automotive and medical and digital health sectors to drive market

10.3.3 UK

10.3.3.1 Growing infrastructure and medical sector investments to boost market

10.3.4 ITALY

10.3.4.1 Demand from EV and infrastructure sectors to fuel market

10.3.5 SPAIN

10.3.5.1 Demand from automotive, construction, and agriculture sectors to drive market growth

10.3.6 REST OF EUROPE

10.4 ASIA PACIFIC

10.4.1 CHINA

10.4.1.1 Developments in EV, infrastructure, electronics, and medical device sectors to drive market

10.4.2 JAPAN

10.4.2.1 Production of high-quality automotive components, consumer electronics, and industrial machinery to boost market

10.4.3 INDIA

10.4.3.1 Significant requirement for agricultural machinery and tools to support market growth

10.4.4 SOUTH KOREA

10.4.4.1 Shipbuilding industry to boost market

10.4.5 REST OF ASIA PACIFIC

10.5 MIDDLE EAST & AFRICA

10.5.1 GCC COUNTRIES

10.5.1.1 Saudi Arabia

10.5.1.1.1 Vision 2030 and NEOM mega project to support market growth

10.5.1.2 Rest of GCC countries

10.5.2 SOUTH AFRICA

10.5.2.1 Automotive and agriculture sectors to propel market

10.5.3 REST OF MIDDLE EAST & AFRICA

10.6 SOUTH AMERICA

10.6.1 BRAZIL

10.6.1.1 Government support in agriculture sector to drive market growth

10.6.2 ARGENTINA

10.6.2.1 Demand for automotive repair and maintenance tools to fuel market

10.6.3 REST OF SOUTH AMERICA

11 COMPETITIVE LANDSCAPE

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES

11.3 REVENUE ANALYSIS, 2022-2024

11.4 MARKET SHARE ANALYSIS, 2024

11.5 COMPANY VALUATION AND FINANCIAL METRICS

11.6 BRAND/PRODUCT COMPARISON ANALYSIS

11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.7.1 STARS

11.7.2 EMERGING LEADERS

11.7.3 PERVASIVE PLAYERS

11.7.4 PARTICIPANTS

11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.7.5.1 Company footprint

11.7.5.2 Region footprint

11.7.5.3 Type footprint

11.7.5.4 End-use industry footprint

11.7.5.5 Functionality footprint

11.7.5.6 Application footprint

11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024