초저전력 마이크로컨트롤러 시장 : 주변 기기별, 패킹 유형별, 최종 용도별, 지역별 예측(-2030년)

Ultra-low-power Microcontroller Market by Peripheral Device, Packaging Type, End-use Application, Region - Global Forecast to 2030

상품코드:1810322

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 357 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

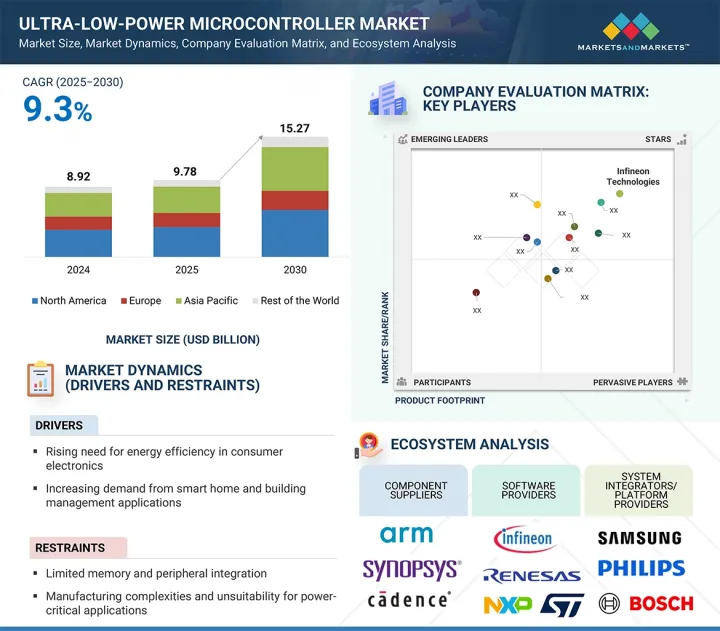

초저전력 마이크로컨트롤러 시장 규모는 9.3%의 연평균 복합 성장률(CAGR)로 확대될 전망이며, 2025년 97억 8,000만 달러에서 2030년에는 152억 7,000만 달러로 확대될 것으로 예측되고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

주변 기기별, 패킹 유형별, 최종 용도별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

초저전력 마이크로컨트롤러 시장의 성장은 배터리 구동 산업용 센서의 도입이 증가하고 있는 것 외에 스마트 홈이나 빌딩 관리 용도에서의 수요가 증가하고 있는 것이 배경에 있습니다. 이 MCU는 에너지 효율을 최적화하고 작동 수명을 연장하고 전력에 민감한 환경에서 자동화, 모니터링 및 제어 시스템에 이상적입니다. 신흥 경제국가의 녹색 산업화 노력은 정부의 지원 정책과 IoT 및 반도체 분야에 대한 투자와 함께 시장의 잠재력을 더욱 강화하고 있습니다.

의료용 초저전력 마이크로컨트롤러 시장은 휴대용 의료기기, 원격 환자 모니터링 시스템, 웨어러블 헬스 트래커의 채용 증가로 높은 성장이 전망되고 있습니다. ULP MCU는 포도당 모니터, ECG 패치, 산소포화도 측정기와 같은 장치에서 배터리 전력을 절약하면서 연속 동작, 안정적인 데이터 처리 및 안전한 무선 연결을 가능하게 합니다. 헬스케어가 예방의료, 원격의료, 재택진단으로 이동함에 따라 작고 전력 효율적인 MCU에 대한 수요가 급증하고 있습니다. 커넥티드 메디컬 기술에 대한 규제 당국의 지원은 이 부문의 성장성을 더욱 가속화하고 있습니다.

디지털 기기 부문은 에너지 제약이 있는 용도에서의 처리, 로직 제어, 통신 기능에 적합하기 때문에 초저전력 마이크로컨트롤러 시장에서 큰 점유율을 차지하고 있습니다. 이러한 MCU는 효율적인 디지털 신호 처리, 안전한 데이터 처리, 무선 통신 프로토콜과의 통합이 필요한 장비에 필수적입니다. 소형화와 저소비 전력이 중요한 소비자용 전자기기, 스마트 미터, 휴대기기, 산업용 제어 시스템 등에 널리 도입되고 있습니다. IoT 에코시스템이 확대되고 고성능 저전력 컴퓨팅에 대한 수요가 높아짐에 따라 디지털 주변장치 탑재 ULP MCU는 안정적인 시장 성장을 유지할 것으로 예측됩니다.

유럽의 초저전력 마이크로컨트롤러(ULP MCU) 시장은 이 지역이 에너지 효율, 산업 자동화, 지속가능한 일렉트로닉스를 중시하고 있는 것을 배경으로 강력한 성장이 전망되고 있습니다. EU의 까다로운 환경 규제와 유럽 그린딜과 같은 이니셔티브는 자동차, 헬스케어, 스마트 인프라에서 저전력 솔루션의 채택을 가속화하고 있습니다. 독일, 프랑스, 이탈리아의 주요 자동차 제조업체에 의해 지원되는 전기자동차 수요 증가는 배터리 관리 시스템 및 센서 시스템에 대한 ULP MCU 통합을 뒷받침하고 있습니다. 게다가 IoT 대응의 산업기기나 의료기기의 진보가 혁신을 촉진하고 있으며, STMicroelectronics나 NXP 등의 주요 기업이 지역 시장의 견인역이 되고 있습니다.

본 보고서에서는 세계의 초저전력 마이크로컨트롤러 시장에 대해 조사했으며, 주변 기기별, 패킹 유형별, 최종 용도별, 지역별 동향, 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서문

시장 역학

고객의 비즈니스에 영향을 미치는 동향 및 혼란

밸류체인 분석

생태계 분석

Porter's Five Forces 분석

특허 분석

규제 분석

무역 분석

가격 분석

기술 분석

사례 연구 분석

주된 회의 및 이벤트(2025-2026년)

주요 이해관계자 및 구매 기준

초저전력 마이크로컨트롤러 시장에서의 AI의 영향

미국 관세가 초저전력 마이크로컨트롤러 시장에 미치는 영향(2025년)

제6장 초저전력 마이크로컨트롤러 시장 : 주변 기기별

서문

아날로그

디지털

제7장 초저전력 마이크로컨트롤러 시장 : 패키징 유형별

서문

8비트

16비트

32비트

제8장 초저전력 마이크로컨트롤러 시장 : 최종 용도별

서문

가전

제조

자동차

헬스케어

통신

항공우주 및 방위

미디어 및 엔터테인먼트

서버 데이터센터

기타

제9장 초저전력 마이크로컨트롤러 시장 : 지역별

서문

북미

북미의 거시 경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시 경제 전망

영국

독일

프랑스

이탈리아

기타

아시아태평양

아시아태평양의 거시 경제 전망

일본

중국

한국

인도

호주

기타

기타 지역

기타 지역의 거시 경제 전망

남미

중동

아프리카

제10장 경쟁 구도

개요

주요 참가 기업의 전략 및 강점(2021-2025년)

수익 분석(2021-2024년)

시장 점유율 분석(2024년)

기업 평가 및 재무지표

브랜드 및 제품 비교

기업 평가 매트릭스 : 주요 진입기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

경쟁 시나리오

제11장 기업 프로파일

주요 진출기업

INFINEON TECHNOLOGIES AG

NXP SEMICONDUCTORS

RENESAS ELECTRONICS CORPORATION

STMICROELECTRONICS

MICROCHIP TECHNOLOGY INC.

TEXAS INSTRUMENTS INCORPORATED

ANALOG DEVICES, INC.

SILICON LABORATORIES

ROHM CO., LTD.

NUVOTON TECHNOLOGY CORPORATION

기타 기업

CHINA MICRO SEMICON CO.,LIMITED

CEC HUADA ELECTRONIC DESIGN CO., LTD.

NORDIC SEMICONDUCTOR

AMBIQ MICRO, INC.

GIGADEVICE

EM MICROELECTRONIC

ABOV SEMICONDUCTOR CO. LTD.

SHANGHAI LINGDONG MICROELECTRONICS CO., LTD.

TELINK

MEGAWIN TECHNOLOGY CO., LTD.

DIEDEVICES

ALIF SEMICONDUCTOR

ASPINITY

INNOPHASE IOT, INC.

ATMOSIC, INC.

MORSE MICRO

SYNTIANT

제12장 부록

AJY

영문 목차

영문목차

The ultra-low-power microcontroller market is projected to expand from USD 9.78 billion in 2025 to USD 15.27 billion by 2030, at a CAGR of 9.3%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Peripheral Device, Packaging Type, End-use Application and Region

Regions covered

North America, Europe, APAC, RoW

The growth of the ultra-low-power microcontroller market is propelled by the increasing demand from smart home and building management applications alongside the rising deployment of battery-powered industrial sensors. These MCUs offer optimized energy efficiency and extended operational lifespans, making them ideal for automation, monitoring, and control systems in power-sensitive environments. Green industrialization initiatives in developing economies, coupled with supportive government policies and investments in IoT and semiconductor sectors, are further enhancing market potential.

"Healthcare is projected to record the highest CAGR during the forecast period."

The ultra-low-power microcontroller market for healthcare is expected to grow at a high rate, fueled by the increasing adoption of portable medical devices, remote patient monitoring systems, and wearable health trackers. ULP MCUs enable continuous operation, reliable data processing, and secure wireless connectivity in devices such as glucose monitors, ECG patches, and pulse oximeters, all while conserving battery power. As healthcare shifts toward preventive care, telemedicine, and home-based diagnostics, demand for compact, power-efficient MCUs is rising sharply. Regulatory support for connected medical technologies further accelerates this segment's growth potential.

"The digital devices segment is expected to hold a significant market share in 2025."

The digital devices segment accounts for a significant share of the ultra-low-power microcontroller market, owing to their suitability for processing, logic control, and communication functions in energy-constrained applications. These MCUs are integral to devices requiring efficient digital signal processing, secure data handling, and integration with wireless communication protocols. They are widely deployed in consumer electronics, smart meters, portable gadgets, and industrial control systems where compact size and low power consumption are critical. As IoT ecosystems expand and demand for high-performance, low-power computing increases, digital peripheral-equipped ULP MCUs are expected to maintain steady market growth.

"Europe is expected to hold a significant market share in 2025."

The ultra-low-power microcontroller (ULP MCU) market in Europe is set for strong growth, driven by the region's emphasis on energy efficiency, industrial automation, and sustainable electronics. The EU's stringent environmental regulations and initiatives like the European Green Deal are accelerating the adoption of low-power solutions in automotive, healthcare, and smart infrastructure. Growing demand for electric vehicles, supported by leading automakers in Germany, France, and Italy, is boosting ULP MCU integration in battery management and sensor systems. Additionally, advancements in IoT-enabled industrial equipment and medical devices are fostering innovation, with companies like STMicroelectronics and NXP leading the regional market push.

Extensive primary interviews were conducted with key industry experts in the ultra-low-power microcontroller market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

By Designation: C-level Executives (20%), Directors (30%), and Others (50%)

By Region: Asia Pacific (40%), Europe (20%), North America (30%), and RoW (10%)

The ultra-low-power microcontroller market is dominated by a few globally established players, such as Infineon Technologies AG (Germany), NXP Semiconductors (Netherlands), Renesas Electronics Corporation (Japan), STMicroelectronics (Switzerland), Microchip Technology Inc. (US), Texas Instruments Incorporated (US), Analog Devices, Inc. (US), Silicon Laboratories (US), ROHM Co., Ltd. (Japan), Nuvoton Technology Corporation (Taiwan), CHINA MICRO SEMICON CO., LIMITED (China), CEC Huada Electronic Design Co., Ltd. (China), Nordic Semiconductor (Norway), Ambiq Micro, Inc. (US), GigaDevice (China), EM Microelectronic (Switzerland), ABOV Semiconductor Co. Ltd. (South Korea), Shanghai Lingdong Microelectronics Co., Ltd. (China), Telink (China), megawin Technology Co., Ltd. (Taiwan), DieDevices (UK), Alif Semiconductor (US), Aspinity (US), InnoPhase IoT, Inc. (US), Atmosic, Inc. (US), Morse Micro (Australia), and Syntiant (US).

The study includes an in-depth competitive analysis of these key players in the ultra-low-power microcontroller market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the ultra-low-power microcontroller market based on peripheral device (analog devices, digital devices), packaging type (8-bit packaging, 16-bit packaging, 32-bit packaging), and end-use application (consumer electronics, manufacturing, automotive, healthcare, telecommunications, aerospace and defense, media and entertainment, servers and data centers, others). It also discusses the market's drivers, restraints, opportunities, and challenges. It gives a detailed view of the market across four main regions (North America, Europe, Asia Pacific, and RoW). The report includes an ecosystem analysis of key players.

Key Benefits of Buying the Report:

Analysis of key drivers (rising need for energy efficiency in consumer electronics, increasing demand from smart home and building management applications, growing number of connected devices in IoT network, and rising deployment in battery-powered industrial sensors), restraints (limited memory and peripheral integration and manufacturing complexities and unsuitability for power-critical applications), opportunities (growing adoption of power electronics in EV industry, government policies and investments for IoT and semiconductors, and green industrialization in developing economies), challenges (lower penetration of ultra-low-power MCUs than high- and low-power MCUs and integration with diverse connectivity protocols)

Service Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the ultra-low-power microcontroller market

Market Development: Comprehensive information about lucrative markets through the analysis of the ultra-low-power microcontroller market across varied regions

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the ultra-low-power microcontroller market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Infineon Technologies AG (Germany), NXP Semiconductors (Netherlands), Renesas Electronics Corporation (Japan), STMicroelectronics (Switzerland), Microchip Technology Inc. (US), Texas Instruments Incorporated (US), Analog Devices, Inc. (US), Silicon Laboratories (US), ROHM Co., Ltd. (Japan), Nuvoton Technology Corporation (Taiwan), CHINA MICRO SEMICON CO., LIMITED (China), CEC Huada Electronic Design Co., Ltd. (China), Nordic Semiconductor (Norway), Ambiq Micro, Inc. (US), and GigaDevice (China), among others

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants

2.1.2.2 Breakdown of primaries

2.1.2.3 Key data from primary sources

2.1.2.4 Key industry insights

2.1.3 SECONDARY & PRIMARY RESEARCH

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN & DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RISK ASSESSMENT

2.6 LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 OPPORTUNITIES FOR PLAYERS IN ULTRA-LOW-POWER MICROCONTROLLER MARKET

4.2 ULTRA-LOW-POWER MICROCONTROLLER MARKET, BY PERIPHERAL DEVICE AND PACKAGING TYPE

4.3 ULTRA-LOW-POWER MICROCONTROLLER MARKET, BY END-USE APPLICATION

4.4 ULTRA-LOW-POWER MICROCONTROLLER MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising need for energy efficiency in consumer electronics

5.2.1.2 Increasing demand for smart home and building management applications

5.2.1.3 Growing number of connected devices in IoT networks

5.2.1.4 Rising deployment of battery-powered industrial sensors

5.2.2 RESTRAINTS

5.2.2.1 Limited memory and peripheral integration

5.2.2.2 Manufacturing complexities and unsuitability for power-critical applications

5.2.3 OPPORTUNITIES

5.2.3.1 Growing adoption of power electronics in EV industry

5.2.3.2 Government policies and investments for IoT and semiconductors

5.2.3.3 Green industrialization in developing economies

5.2.4 CHALLENGES

5.2.4.1 Lower penetration of ultra-low-power microcontrollers than high- and low-power microcontrollers

5.2.4.2 Integration with diverse connectivity protocols