정형외과용 보조기 및 지지대 시장 : 제품별, 유형별, 용도별, 유통 채널별, 지역별 예측(-2030년)

Orthopedic Braces & Supports Market by Product (Knee, Ankle, Hip, Spine, Shoulder, Neck, Elbow, Hand, Wrist), Category (Soft, Rigid, Hinged), Application (Ligament (ACL, LCL), Preventive, OA), Distribution (Pharmacies) - Global Forecast to 2030

상품코드:1807082

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 322 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

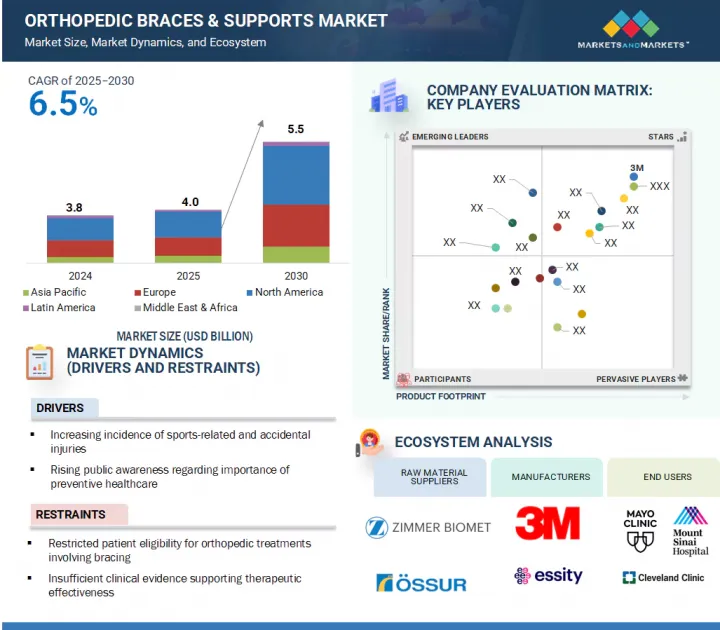

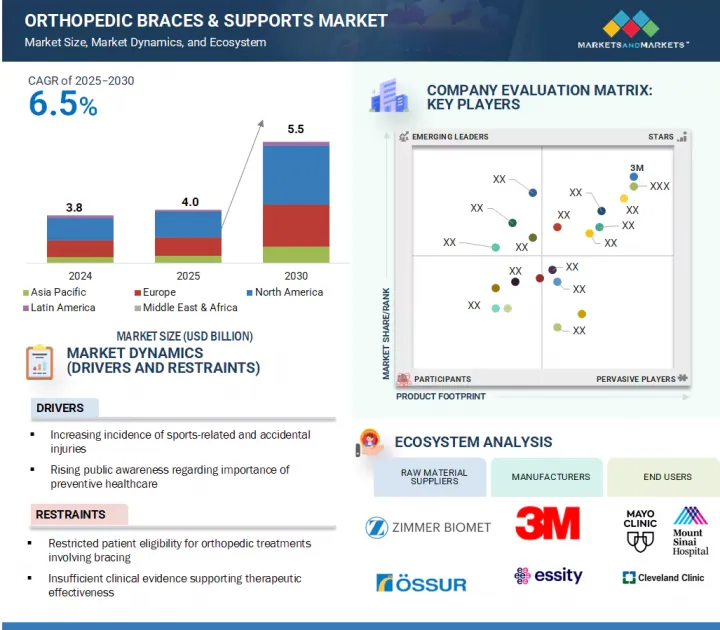

세계의 정형외과용 보조기 및 지지대 시장 규모는 2025년 40억 8,000만 달러에서 2030년에는 55억 9,510만 달러로 성장할 것으로 예측되며, 2025년에서 2030년까지 CAGR 6.5%가 될 것으로 보입니다.

정형외과용 보조기 및 지지대 시장은 인구 역학 변화, 건강 관리 요구, 기술 진보, 소비자 행동의 변화에 견인되어 강력한 성장을 이루고 있습니다. 주로 고령화와 좌석없는 라이프 스타일에 의한 근골격계 장애 증가로 인해 이러한 제품에 대한 수요가 크게 증가하고 있습니다.

조사 범위

조사 대상 연도

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

제품별, 유형별, 용도별, 유통채널별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

동시에 스포츠나 신체활동 참여가 늘어나고 염좌, 골절, 인대단열 등의 부상이 증가하여 시장이 더욱 확대되고 있습니다. 가볍고 통기성이 있는 소재, 3D 프린팅, 센서 부착 스마트 장비 등의 기술 혁신에 의해 쾌적성, 피트감, 치료 결과가 개선되어, 이러한 장비의 매력이 증가하고 있습니다. 게다가 예방의료 및 비침습적 치료에 대한 주목, 헬스케어 지출 증가, 전자상거래와 보험 적용에 의한 액세스의 향상이 세계적인 보급과 시장 확대를 뒷받침하고 있습니다.

제품별로는 정형외과용 보조기 및 지지대 시장은 무릎 보조기 및 지지대, 발목 보조기 및 지지대, 발 보행기 및 보조기, 등, 허리 척추 보조기 및 지지대(목 및 경추, 하부척추), 어깨보조기 및 지지대, 팔꿈치 보조기 및 지지대, 손 및 손목장구, 얼굴 보조기 및 지지대 등이 있습니다. 정형외과용 보조기 및 지지대 시장에서는 무릎 보조기 및 지지대 부문이 최대 매출을 차지하고 있습니다. 무릎 보조기 및 지지대 시장은 다양한 요인에 의해 강력한 성장을 이루고 있습니다. 인구의 고령화, 비만 증가, 보다 활동적인 라이프 스타일 등이 주된 원인으로 무릎과 관련된 부상이나 변형성 관절증 등 변성 질환의 발생률이 상승하여 수요가 꾸준히 증가하고 있습니다. 스포츠 및 피트니스 활동에 대한 참여가 늘어남에 따라 급성 및 반복성 긴장으로 인한 부상이 급증하고 운동 선수와 피트니스 애호가가 예방 및 재활용 장비를 요구하게 되었습니다. 가볍고 통기성이 있는 소재, 힌지식 디자인, 조절 가능한 압박 기능, 3D 프린팅에 의한 커스텀 장비 등의 기술 혁신으로 제품의 쾌적성, 기능성, 사용자의 컴플라이언스가 대폭 향상되고 있습니다. 또한 비침습적 치료 옵션에 대한 건강 관리 제공업체와 소비자의 의식이 높아짐에 따라 수락이 진행되고 있습니다. 이러한 추세는 온라인 플랫폼과 소매 채널을 통한 제품 입수의 용이성, 상환 범위의 개선에 의해 더욱 강화되고 시장 성장을 가속하고 있습니다.

유형별로, 정형외과용 보조기 및 지지대 시장은 소프트 탄성 보조기 및 지지대, 하드 보조기 및 지지대, 힌지 부착 보조기 및 지지대로 나눌 수 있습니다. 정형외과용 보조기 및 지지대 시장에서 소프트 탄성 장비 및 지지대의 성장은 특히 노인과 신체활동 그룹 사이에서 염좌, 긴장, 관절 불안정성과 같은 근골격계 질환의 유병률이 증가하는 등 몇 가지 중요한 요인에 의해 견인되고 있습니다. 이 제품은 편안함, 유연성, 경량 설계, 사용 편의성으로 인기가 있으며 일상적인 착용, 예방 관리, 조기 재활에 이상적입니다. 비침습적이고 합리적인 가격의 치료 옵션에 대한 수요 증가는 연성 장비의 채용을 더욱 강화하고 있습니다. 흡습 발산성, 통기성, 항균성 섬유 등의 천 소재의 진보에 의해 사용감과 컴플라이언스가 향상하고 있습니다. 게다가, 이러한 기구가 시판되고 온라인으로 이용가능하다는 점, 소비자의 의식이 높아지고, 경미한 정형외과적 문제의 보존적 관리에 대한 의료 전문가의 추천이 이 부문의 성장에 크게 기여하고 있습니다.

용도별로, 정형외과용 보조기 및 지지대 시장은 예방 케어, 인대 손상(전 십자 인대 손상, 외부 부인대 손상, 기타 인대 손상), 수술 후 재활, 골관절염, 압박 요법, 골절 관리로 나뉩니다. 정형외과용 보조기 및 지지대 시장에서는 예방 의료가 가장 높은 성장을 보이고 있습니다. 이 분야는 몇 가지 중요한 요인으로 기세를 늘리고 있습니다. 특히 운동선수와 피트니스 애호가들 사이에서 부상을 입기 전에 관절을 보호하고 근육을 지원하는 중요성에 대한 인식이 높아지고 있는 것, 의료 제공업체들 사이에서 초기 단계와 부하가 걸리기 쉬운 상태에서 보존적이고 비침습적인 치료를 선호하는 경향이 강해지고 있는 것, 경량으로 통기성이 있는 소재와 심리스한 디자인 쾌적성이나 장착성이 향상되고 있는 것, 직장의 웰니스 프로그램이나 인체 공학적 이니셔티브 증가에 의해 근골격계의 부담을 경감하기 위해서 장비의 사용이 촉진되고 있는 것, 시판 제품이나 온라인 판매 채널을 통해 예방 장비에의 액세스가 확대되어, 예방 장비가 보다 친숙해지고 조기 도입이 촉진되고 있는 것 등이 있습니다.

정형외과용 보조기 및 지지대 시장은 5개의 중요한 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동, 아프리카)을 포괄하고 있습니다. 북미의 정형외과용 보조기 및 지지대 시장은 몇 가지 중요한 요인에 의해 강력한 성장을 이루고 있습니다. 주로 고령화, 비만률 증가, 보다 활동적인 라이프 스타일에 의한 관절염, 골다공증, 스포츠 관련 상해 등 근골격계 질환의 이환율 상승이 수요를 크게 밀어 올리고 있습니다. 이 지역은 성숙한 의료 인프라,(FDA 허가 포함) 지원 규제 환경, 메디케어, 메디케이드, 민간 보험 회사의 유리한 상환 옵션 등의 혜택을 누리고 있으며, 이들 모두가 접근성과 저렴한 가격을 향상시키고 있습니다. 3D 프린팅, 스마트 소재, 통기성 소재, 센서 내장 장비 등의 기술 혁신으로 제품의 성능, 커스터마이즈성, 사용자의 쾌적성이 향상되었습니다. 또한 스포츠 및 피트니스 활동의 인기가 높아지고 직장 웰빙과 인체 공학적 노력이 예방 정형외과 솔루션 수요를 촉진하고 있습니다. 또한 전략적 합병, 인수, 의료 전문가와의 제휴는 기업이 제품 범위를 넓히고 지역 전체의 판매 네트워크를 강화하는 데 도움이 됩니다.

본 보고서에서는 세계의 정형외과용 보조기 및 지지대 시장에 대해 조사했으며, 제품별, 유형별, 용도별, 유통 채널별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

규제 상황

상환 시나리오 분석

밸류체인 분석

공급망 분석

에코시스템 시장 맵

무역 분석

특허 분석

가격 분석

기술 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

주요 회의 및 이벤트

사례 연구 분석

고객의 비즈니스에 영향을 미치는 동향/혼란

투자 및 자금조달 시나리오

미충족 요구

정형외과용 보조기 및 지지대 시장에서 AI의 영향

2025년 미국 관세의 영향 - 정형외과용 보조기 및 지지대 시장

제6장 정형외과용 보조기 및 지지대 시장(제품별)

소개

무릎 보조기 및 지지대

발목 보조기 및 지지대

보행기 및 교정기구

등, 허리, 척추 보조기 및 지지대

어깨 보조기 및 지지대

팔꿈치 보조기 및 지지대

손, 손목 보조기 및 지지대

얼굴용 보조기 및 지지대

제7장 정형외과용 보조기 및 지지대 시장(유형별)

소개

소프트 탄력 보조기 및 지지대

하드 보조기 및 지지대

힌지 부착 보조기 및 지지대

제8장 정형외과용 장비 및 서포트 시장(용도별)

소개

예방 케어

인대 손상

수술 후 재활

골관절염

압박요법

골절 관리

기타

제9장 정형외과용 보조기 및 지지대 시장(유통 채널별)

소개

병원 및 외과 센터

정형외과 클리닉

약국 및 소매점

전자상거래 플랫폼

DME 딜러

기타

제10장 정형외과용 보조기 및 지지대 시장(지역별)

소개

북미

북미 : 거시경제 전망

미국

캐나다

유럽

유럽: 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양: 거시경제 전망

중국

일본

인도

호주

한국

기타

라틴아메리카

라틴아메리카: 거시경제 전망

브라질

멕시코

기타

중동 및 아프리카

중동 및 아프리카 : 거시경제 전망

GCC 국가

기타

제11장 경쟁 구도

소개

주요 진입기업의 전략 및 강점

수익 분석, 2022-2024년

시장 점유율 분석, 2024년

시장 랭킹 분석, 2024년

기업 평가 매트릭스: 주요 진입기업, 2024년

기업 평가 매트릭스: 스타트업 및 중소기업, 2024년

경쟁 시나리오

기업 평가와 재무지표

브랜드 및 제품 비교

제12장 기업 프로파일

주요 진출기업

3M COMPANY

ESSITY HEALTH & MEDICAL

OSSUR

THUASNE

ZIMMER BIOMET HOLDINGS, INC.

BIRD & CRONIN, LLC(DYNATRONICS CORPORATION)

ENOVIS CORPORATION

OTTOBOCK

BAUERFEIND

BREG, INC

DEROYAL INDUSTRIES, INC.

ALCARE CO., LTD

NIPPON SIGMAX CO., LTD.

MEDI GMBH & CO. KG

TRULIFE

기타 기업

FOUNDATION WELLNESS(FORMERLY KNOWN AS REMINGTON PRODUCTS COMPANY)

MCDAVID, INC.(A PART OF SHOCK DOCTOR)

MUELLER SPORTS MEDICINE, INC.

BECKER ORTHOPEDIC

ORLIMAN SLU(A PART OF MAGNUM INDUSTRIAL PARTNERS)

FRANK STUBBS COMPANY INC.

ASPEN MEDICAL PRODUCTS LLC

DARCO INTERNATIONAL, INC.

UNITED MEDICARE

VISSCO REHABILITATION AIDS PVT. LTD.

제13장 부록

JHS

영문 목차

영문목차

The global orthopedic braces & supports market is anticipated to grow from USD 4,080.0 million in 2025 to USD 5,595.1 million in 2030 at a CAGR of 6.5% from 2025 to 2030. The orthopedic braces & supports market is experiencing strong growth, driven by demographic changes, healthcare needs, technological advances, and shifts in consumer behavior. The rising occurrence of musculoskeletal disorders-mainly due to an aging population and sedentary lifestyles-has greatly increased demand for these products.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, Type, Application, Distribution Channel, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

At the same time, more participation in sports and physical activities has led to a rise in injuries such as sprains, fractures, and ligament tears, further expanding the market. Innovations like lightweight, breathable materials, 3D printing, and smart braces with sensors are improving comfort, fit, and treatment results, making these devices more attractive. Additionally, the focus on preventive care and non-invasive treatments, along with higher healthcare spending and better access through e-commerce and insurance coverage, is boosting adoption and market reach worldwide.

"The knee braces & supports segment accounted for the highest growth rate in the orthopedic braces & supports products market in 2024."

By product, the orthopedic braces & supports market is segmented into knee braces & supports, ankle braces & supports, foot walkers & orthoses, back, hip and spine braces & supports (neck and cervical, lower spine), shoulder braces & supports, elbow braces & supports, hand & wrist braces & supports, facial braces & supports. The knee braces & supports segment accounted for the greatest amount of revenue in the orthopedic braces & supports market . The knee braces & supports market is experiencing strong growth, driven by a combination of factors. The rising incidence of knee-related injuries and degenerative conditions like osteoarthritis-mainly due to aging populations, increasing obesity levels, and more active lifestyles-has resulted in a steady increase in demand. Greater participation in sports and fitness activities has led to a surge in both acute and repetitive strain injuries, prompting athletes and fitness enthusiasts to seek preventive and rehabilitative bracing solutions. Innovations in technology, such as lightweight, breathable materials, hinged designs, adjustable compression features, and 3D-printed custom braces, have greatly improved product comfort, functionality, and user compliance. Additionally, growing awareness among healthcare providers and consumers about non-invasive treatment options has increased acceptance. This trend is further supported by easier product access through online platforms, retail channels, and improved reimbursement coverage, collectively fueling market growth.

"The soft & elastic braces & supports segment held the largest market share, by type, in 2024."

Based on the type, the market for orthopedic braces & supports is divided into soft & elastic braces & supports, hard braces & supports, and hinged braces & supports. The growth of soft & elastic braces & supports in the orthopedic braces & supports market is driven by several key factors, including the increasing prevalence of musculoskeletal conditions like sprains, strains, and joint instability, especially among the elderly and physically active groups. These products are popular for their comfort, flexibility, lightweight design, and ease of use, making them ideal for daily wear, preventive care, and early-stage rehabilitation. The rising demand for non-invasive, affordable treatment options has further boosted the adoption of soft braces. Advances in fabric materials-such as moisture-wicking, breathable, and antimicrobial textiles-have enhanced user experience and compliance. Moreover, the availability of these braces over the counter and online, along with growing consumer awareness and recommendations from healthcare professionals for conservative management of mild orthopedic issues, significantly contributes to the growth of this segment.

"The preventive care application segment held the largest share of the market in 2024."

Based on the application, the market for orthopedic braces & supports is divided into preventive care, ligament injury (anterior cruciate ligament injury, lateral collateral ligament injury, other ligament injury), post-operative rehabilitation, osteoarthritis, compression therapy, and fracture management. Preventive care is seeing the highest growth in the orthopedic braces & supports market . This sector is gaining momentum due to several key factors: increased awareness among individuals-especially athletes and fitness enthusiasts-about the importance of joint protection and muscle support before injuries happen; a growing preference among healthcare providers for conservative, non-invasive treatments in early-stage or stress-prone conditions; improvements in brace comfort and wearability through advancements in lightweight, breathable materials and seamless designs; a rise in workplace wellness programs and ergonomics initiatives promoting brace use to reduce musculoskeletal strain; and expanded access via over-the-counter products and online sales channels, making preventive braces more accessible and encouraging early adoption.

"The North American market is expected to hold a significant market share for orthopedic braces & supports market in 2024."

The market for orthopedic braces & supports encompasses five significant geographies: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The North American orthopedic braces & supports market is experiencing robust growth, fueled by several key factors. The rising incidence of musculoskeletal conditions like arthritis, osteoporosis, and sports-related injuries-mainly due to an aging population, increasing obesity rates, and more active lifestyles-has significantly boosted demand. The region benefits from a mature healthcare infrastructure, a supportive regulatory environment (including FDA approvals), and favorable reimbursement options through Medicare, Medicaid, and private insurers, all of which improve access and affordability. Technological innovations such as 3D printing, smart materials, breathable fabrics, and sensor-embedded braces are enhancing product performance, customization, and user comfort. Additionally, the rising popularity of sports and fitness activities, along with workplace wellness and ergonomic initiatives, is fueling demand for preventive orthopedic solutions. Moreover, strategic mergers, acquisitions, and collaborations with healthcare professionals are helping companies broaden their product ranges and strengthen distribution networks throughout the region.

The primary interviews conducted for this report can be categorized as follows:

By Company Type: Tier 1: 20%, Tier 2: 45%, and Tier 3: 35%

By Designation: C-level: 30%, Director-level: 20%, and Others: 50%

By Region: North America: 36%, Europe: 25%, Asia Pacific: 27%, and Rest of the World: 12%

List of key Companies Profiled in the Report:

The prominent players in the orthopedic braces & supports market are Alcare Co., Ltd. (Japan), Aspen Medical, LLC (Australia), Becker Orthopedic (US), Bauerfeind (Germany), Breg, Inc. (US), DARCO International, Inc. (US), DeRoyal Industries, Inc. (US), ESSITY HEALTH & MEDICAL (Sweden), FOUNDATION WELLNESS (US), Frank stubbs company inc (US), Mueller Sports Medicine, Inc (US ), MEDI GMBH & CO. KG (Germany), and MCDAVID (US ) among others.

Research Coverage:

This report examines the orthopedic braces & supports market based on product, type, application, distribution channel, and region. It also discusses the factors influencing market growth, analyzes the various opportunities and challenges, and provides details about the competitive landscape for market leaders. Additionally, the report assesses micro markets in terms of their individual growth trends and forecasts revenue for market segments across five main regions and their respective countries.

Key Benefits of Buying the Report:

The report will assist market leaders and new entrants by providing approximate revenue figures for the overall orthopedic braces & supports market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain insights to more effectively position their business and develop appropriate go-to-market strategies. This report will enable stakeholders to grasp the market's pulse and offer information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of key drivers (rising incidence of orthopedic conditions and musculoskeletal disorders), restraints (restricted eligibility of patients for orthopedic treatment involving bracing), opportunities (growth in sales of ready-to-use and e-commerce-based orthopedic products), and challenges (widespread reliance on pain medications as an alternative to bracing solutions).

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product approvals/launches in the orthopedic braces & supports market.

Market Development: Comprehensive information about lucrative markets-the report analyses the market across varied regions.

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the orthopedic braces & supports market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/ approvals, pipeline analysis, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the orthopedic braces & supports market."

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.2 RESEARCH DATA SOURCES

2.2.1 SECONDARY RESEARCH SOURCES

2.2.2 PRIMARY RESEARCH SOURCES

2.2.2.1 Primary sources

2.2.2.2 Key industry insights

2.2.2.3 Breakdown of primaries

2.3 MARKET SIZE ESTIMATION METHODOLOGY

2.3.1 APPROACH 1: COMPANY REVENUE ESTIMATION APPROACH

5.19 IMPACT OF AI ON ORTHOPEDIC BRACES & SUPPORTS MARKET

5.19.1 INTRODUCTION

5.19.2 MARKET POTENTIAL OF AI ON ORTHOPEDIC BRACES & SUPPORTS

5.19.3 AI USE CASES

5.19.4 KEY COMPANIES IMPLEMENTING AI

5.19.5 FUTURE OF AI ON ORTHOPEDIC BRACES & SUPPORTS MARKET

5.20 IMPACT OF 2025 US TARIFF - ORTHOPEDIC BRACES & SUPPORTS MARKET

5.20.1 INTRODUCTION

5.20.2 KEY TARIFF RATES

5.20.3 PRICE IMPACT ANALYSIS

5.20.4 IMPACT ON COUNTRY/REGION

5.20.4.1 US

5.20.4.2 Europe

5.20.4.3 Asia Pacific

5.20.5 IMPACT ON END-USE INDUSTRIES

6 ORTHOPEDIC BRACES & SUPPORTS MARKET, BY PRODUCT

6.1 INTRODUCTION

6.2 KNEE BRACES & SUPPORTS

6.2.1 GROWTH IN ELDERLY POPULATION COUPLED WITH SURGE IN SPORTS-RELATED INJURIES

6.3 ANKLE BRACES & SUPPORTS

6.3.1 INCREASE IN INCIDENCE OF ANKLE INJURIES AND ANKLE OSTEOARTHRITIS

6.4 FOOT WALKER & ORTHOSES

6.4.1 RISE IN INCIDENCE OF DIABETES AND AWARENESS ABOUT PREVENTIVE FOOT CARE

6.5 BACK, HIP, AND SPINE BRACES & SUPPORTS

6.5.1 INCREASE IN INCIDENCE OF LOWER BACK PAIN, SPINAL STENOSIS, SCOLIOSIS, HERNIATED DISCS, AND DEGENERATIVE DISC DISEASES

6.5.2 NECK AND CERVICAL BRACES & SUPPORTS

6.5.2.1 Increase in incidence of neck injuries caused by road accidents, sports-related incidents, and occupational hazards

6.5.3 LOWER SPINE BRACES & SUPPORTS

6.5.3.1 Growth in aging population prone to lower spine degeneration

6.6 SHOULDER BRACES & SUPPORTS

6.6.1 RISE IN CASES OF SPORTS INJURIES, ROAD ACCIDENTS, AND AGE-RELATED MUSCULOSKELETAL DISORDERS

6.7 ELBOW BRACES & SUPPORTS

6.7.1 GROWTH IN PARTICIPATION IN PHYSICAL AND ATHLETIC ACTIVITIES, COUPLED WITH GREATER AWARENESS OF NON-INVASIVE ORTHOPEDIC TREATMENTS AND EARLY INTERVENTION

6.8 HAND & WRIST BRACES & SUPPORTS

6.8.1 AGING POPULATION AND REPETITIVE STRAIN INJURIES AMONG WORKERS

6.9 FACIAL BRACES & SUPPORTS

6.9.1 INCREASE IN DEMAND FOR FACIAL RECONSTRUCTION SURGERIES AND RISE IN INCIDENCE OF CONGENITAL CRANIAL DEFORMITIES

7 ORTHOPEDIC BRACES & SUPPORTS MARKET, BY TYPE

7.1 INTRODUCTION

7.2 SOFT AND ELASTIC BRACES & SUPPORTS

7.2.1 ADVANTAGES OF SOFT & ELASTIC BRACES AND SUPPORTS INCLUDE THEIR FLEXIBILITY AND EASE OF USE

7.3 HARD BRACES & SUPPORTS

7.3.1 SUPPORTIVE REIMBURSEMENT SCENARIO AND RISING PREVALENCE OF TARGET DISEASES

7.4 HINGED BRACES & SUPPORTS

7.4.1 GROWTH IN GERIATRIC POPULATION AND RISE IN INCIDENCE OF LIGAMENT INJURIES

8 ORTHOPEDIC BRACES & SUPPORTS MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 PREVENTIVE CARE

8.2.1 INCREASE IN PUBLIC PARTICIPATION IN SPORTS-RELATED ACTIVITIES

8.3 LIGAMENT INJURY

8.3.1 ANTERIOR CRUCIATE LIGAMENT (ACL) INJURY

8.3.1.1 ACL injury applications to register highest growth rate during forecast period

8.3.2 LATERAL COLLATERAL LIGAMENT (LCL) INJURY

8.3.2.1 Rise in reimbursements of LCL-related surgical procedures

8.3.3 OTHER LIGAMENT INJURY

8.4 POST-OPERATIVE REHABILITATION

8.4.1 INCREASE IN NUMBER OF ORTHOPEDIC RECONSTRUCTIVE SURGERIES

8.5 OSTEOARTHRITIS

8.5.1 RISE IN OSTEOARTHRITIS CASES AND PUBLIC AWARENESS ON SIDE-EFFECTS OF ORAL MEDICATION FOR PAIN MANAGEMENT

8.6 COMPRESSION THERAPY

8.6.1 INNOVATION OF TECHNOLOGICALLY ADVANCED COMPRESSION BRACES

8.7 FRACTURE MANAGEMENT

8.7.1 RISE IN FRACTURE INCIDENCE, AGING POPULATIONS WITH OSTEOPOROSIS, AND GROWING PREFERENCE FOR NON-SURGICAL, EARLY MOBILIZATION SOLUTIONS

8.8 OTHER APPLICATIONS

9 ORTHOPEDIC BRACES & SUPPORTS MARKET, BY DISTRIBUTION CHANNEL

9.1 INTRODUCTION

9.2 HOSPITALS & SURGICAL CENTERS

9.2.1 INCREASE IN INVESTMENTS IN HOSPITAL INFRASTRUCTURE

9.3 ORTHOPEDIC CLINICS

9.3.1 SHORTER HOSPITAL STAYS, REDUCED TREATMENT COSTS, AND IMPROVED POST-OPERATIVE CARE

9.4 PHARMACIES & RETAILERS

9.4.1 WIDESPREAD AVAILABILITY OF PRODUCTS THROUGH RETAIL STORES AND PHARMACIES

9.5 E-COMMERCE PLATFORMS

9.5.1 GROWTH IN POPULARITY OF ECOMMERCE AND ITS CONVENIENCE

9.6 DME DEALERS

9.6.1 GROWTH IN ELDERLY POPULATION AND RISE IN INCIDENCE OF CHRONIC HEALTH CONDITIONS

9.7 OTHER DISTRIBUTION CHANNELS

10 ORTHOPEDIC BRACES & SUPPORTS MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

10.2.2 US

10.2.2.1 Rise in cases of osteoarthritis and rheumatoid arthritis and growth in preference for minimally invasive procedures

10.2.3 CANADA

10.2.3.1 Increase in prevalence of degenerative bone disorders and uptick in road accident-related injuries

10.3 EUROPE

10.3.1 EUROPE: MACROECONOMIC OUTLOOK

10.3.2 GERMANY

10.3.2.1 Rise in engagement in sports activities and growing awareness of healthy living

10.3.3 UK

10.3.3.1 Rise in awareness of orthopedic health issues challenged by rising costs of procedures

10.3.4 FRANCE

10.3.4.1 Increase in incidence of musculoskeletal disorders

10.3.5 ITALY

10.3.5.1 High incidence of sports-related injuries often managed non-invasively

10.3.6 SPAIN

10.3.6.1 Increase in presence of leading manufacturers and surge in osteoarthritis and osteoporosis cases

10.3.7 REST OF EUROPE

10.4 ASIA PACIFIC

10.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

10.4.2 CHINA

10.4.2.1 Need for effective rehabilitation solutions and related products with expanding target patient population

10.4.3 JAPAN

10.4.3.1 Rapidly aging population and supportive government initiatives

10.4.4 INDIA

10.4.4.1 Shift from traditional analog systems to modern digital systems utilizing flat panel detectors (FPDs)

10.4.5 AUSTRALIA

10.4.5.1 Expanding patient base, advancements in product design, and ongoing efforts to improve musculoskeletal care

10.4.6 SOUTH KOREA

10.4.6.1 Hub for technological innovation in medical devices, with domestic companies investing in smart, wearable technologies

10.4.7 REST OF ASIA PACIFIC

10.5 LATIN AMERICA

10.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

10.5.2 BRAZIL

10.5.2.1 Strong global player presence supported by extensive distribution networks

10.5.3 MEXICO

10.5.3.1 Improved access to healthcare services and increasing availability of ecommerce platforms

10.5.4 REST OF LATIN AMERICA

10.6 MIDDLE EAST & AFRICA

10.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

10.6.2 GCC COUNTRIES

10.6.2.1 Focus on infrastructure development and improved healthcare accessibility

10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3 REVENUE ANALYSIS, 2022-2024

11.4 MARKET SHARE ANALYSIS, 2024

11.5 MARKET RANKING ANALYSIS, 2024

11.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.6.1 STARS

11.6.2 EMERGING LEADERS

11.6.3 PERVASIVE PLAYERS

11.6.4 PARTICIPANTS

11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.6.5.1 Company footprint

11.6.5.2 Product footprint

11.6.5.3 Regional footprint

11.6.5.4 Type footprint

11.6.5.5 Application footprint

11.6.5.6 Distribution channel footprint

11.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

11.7.1 PROGRESSIVE COMPANIES

11.7.2 RESPONSIVE COMPANIES

11.7.3 DYNAMIC COMPANIES

11.7.4 STARTING BLOCKS

11.7.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2024

11.7.5.1 Detailed list of key startups/SMEs

11.7.5.2 Competitive benchmarking of key startups/SMEs