Wound Dressings Market by Type (Advanced, Traditional), Wound Type, End User - Global Forecast to 2030

상품코드:1807076

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 353 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

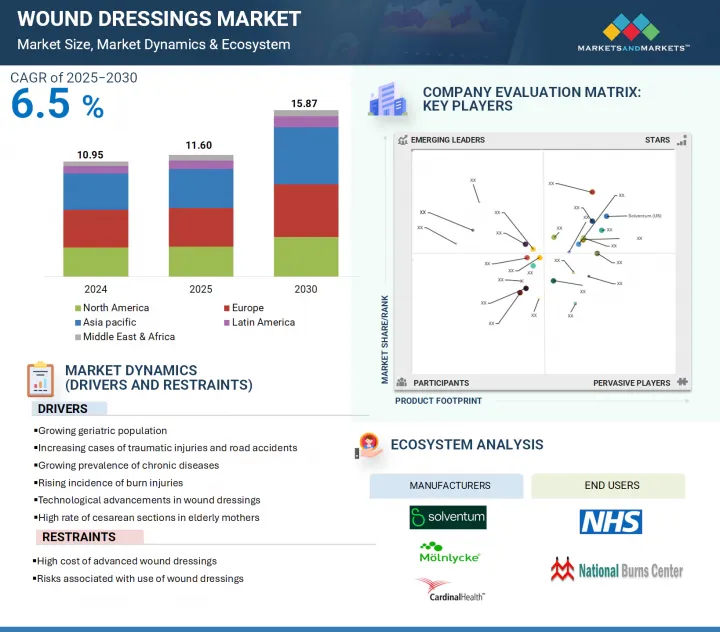

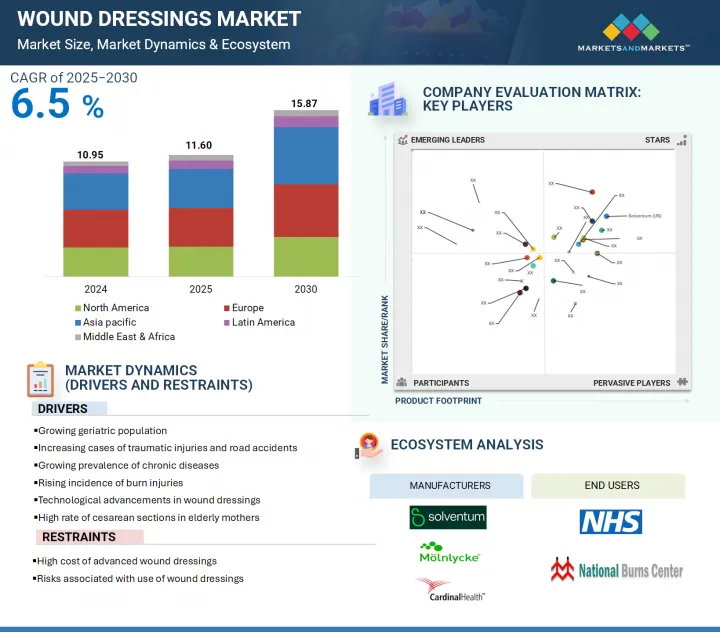

세계의 상처 드레싱 시장 규모는 2025년 116억 달러에서 2030년까지 158억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 6.5%가 될 것으로 보입니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

유형별, 상처 유형별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

시장은 주로 열상 발생률 증가, 만성 상처, 수술 상처, 외상성 상처 유병률 증가, 노인 여성의 제왕절개율 증가, 교통 사고 증가로 인한 것입니다. 그러나 첨단 상처 드레싱의 높은 가격과 한정적인 채용이 예측 기간 동안 시장 성장을 방해할 것으로 예측되고 있습니다.

유형별로 보면, 상처 드레싱 시장은 기존 상처 드레싱와 첨단 상처 드레싱으로 구분됩니다. 2024년에는 첨단 상처 드레싱 부문이 상처 드레싱 시장의 유형별 점유율에서 최대를 차지했습니다. 이는 당뇨족궤양, 정맥성 허벅지 궤양, 욕창과 같은 만성 상처의 발생률이 증가하고 있으며, 전문적이고 효과적인 치료법이 필요하다는 것이 주요 요인입니다. 또한 당뇨병의 유병률 상승, 상처 관리에 대한 환자의 의식 증가, 상처 케어 기술의 진보, 원내 감염(HAI) 증가 등의 요인도 첨단 상처 드레싱의 왕성한 수요로 이어지고 있습니다. 이러한 제품은 치유를 가속화하고 감염 위험을 줄이고 환자의 결과를 개선하기 위해 더욱 채용되고 있습니다.

상처 유형별로 시장은 외과 상처 및 외상 상처, 당뇨족궤양, 욕창, 정맥 하퇴 궤양, 화상 및 기타 상처로 구분됩니다. 상처 유형별로 보면, 2024년 상처 드레싱 시장에서는 외과 상처 및 외상 상처 분야가 가장 큰 점유율을 차지하고 있습니다. 이 큰 점유율은 주로 세계 수술 수 증가, 사고 및 넘어짐으로 인한 외상 발생률 증가로 인한 것입니다. 또한, 만성 질환과 수술을 받기 쉬운 노인 인구 증가와 교통 사고의 세계적인 증가가 이 부문의 이점에 기여합니다. 또한 수술 절차의 지속적인 개선, 수술 후 관리, 병원 및 재택 관리의 현장에서 상처 드레싱의 사용 증가로 이 분야는 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다.

세계 상처 피복 시장은 5개의 주요 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)으로 분류됩니다. 그 중에서도 아시아태평양은 고령화 사회와 만성상처의 원인이 되는 생활습관병 유병률의 상승을 배경으로 급성장하고 있습니다. 고품질의 건강 관리 서비스에 대한 수요가 증가함에 따라 병원 인프라와 첨단 의료 기술에 대한 많은 투자가 고급 상처 치료용 드레싱 재료의 보급에 박차를 가하고 있습니다. 또한 인도, 태국, 싱가포르 등의 국가에서 의료 관광 산업이 성장하고 있기 때문에 수술이 증가하고 있으며 효과적인 수술 후 상처 케어의 필요성이 높아지고 있습니다. 환자의 치료 성적 향상과 회복 기간 단축에 의료 제공자가 강한 관심을 갖고 있기 때문에 아시아태평양 시장은 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다.

본 보고서에서는 세계의 상처 드레싱 시장에 대해 조사했으며, 유형별, 상처 유형별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 분석

밸류체인 분석

공급망 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

무역 분석

2025-2026년의 주된 회의와 이벤트

사례 연구 분석

규제 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

AI가 상처 드레싱 시장에 미치는 영향

2025년 미국 관세가 상처 드레싱 시장에 미치는 영향

제6장 상처 드레싱 시장(유형별)

소개

첨단 상처 드레싱

기존 상처 드레싱

제7장 상처 드레싱 시장(상처 유형별)

소개

외과 상처 및 외상 상처

당뇨족궤양

욕창

정맥성 다리 궤양

화상 및 기타 상처

제8장 상처 드레싱 시장(최종 사용자별)

소개

병원, ASCS, 클리닉

재택 케어

기타

제9장 상처 드레싱 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시 경제 전망

독일

프랑스

영국

이탈리아

스페인

러시아

기타

아시아태평양

아시아태평양의 거시 경제 전망

중국

일본

인도

호주

기타

라틴아메리카

라틴아메리카의 거시 경제 전망

브라질

멕시코

기타

중동 및 아프리카

의료시설 수요 증가가 시장을 견인

제10장 경쟁 구도

개요

주요 진입기업의 전략 및 강점, 2024년

수익 분석, 2022-2024년

시장 점유율 분석, 2024년

기업 평가 매트릭스: 주요 진입기업, 2024년

기업 평가 매트릭스: 스타트업 및 중소기업, 2024년

기업 평가 및 재무지표

브랜드 및 제품 비교

경쟁 시나리오

제11장 기업 프로파일

주요 진출기업

SOLVENTUM

MOLNLYCKE AB

CARDINAL HEALTH

SMITH NEPHEW

CONVATEC GROUP PLC

PAUL HARTMANN AG

COLOPLAST GROUP

OWENS & MINOR

INTEGRA LIFESCIENCES CORPORATION

ESSITY AKTIEBOLAG

B. BRAUN SE

ADVANCED MEDICAL SOLUTIONS GROUP PLC

MATIV HOLDINGS, INC.

기타 기업

URGO GROUP

DEROYAL INDUSTRIES, INC.

LOHMANN & RAUSCHER GMBH & CO. KG

MEDLINE INDUSTRIES, LP

WINNER MEDICAL CO., LTD.

ADVANCIS(UK)

HOLLISTER INCORPORATED

DERMARITE INDUSTRIES, LLC

MIL LABORATORIES PVT. LTD.

GENTELL

SHIELDLINE

FOCUS HEALTH GROUP

제12장 부록

JHS

영문 목차

영문목차

The global wound dressings market is projected to reach USD 15.87 billion by 2030 from USD 11.60 billion in 2025, at a CAGR of 6.5% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Type, Wound Type, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The market is primarily driven by the rising incidence of burn injuries, increasing prevalence of chronic, surgical, and traumatic wounds, a high rate of cesarean sections among elderly women, and a growing number of road accidents. However, the high cost and limited adoption of advanced wound dressings are anticipated to hinder market growth during the forecast period.

The advanced wound dressings segment accounted for the largest share of the wound dressings market, by type.

Based on type, the wound dressings market is segmented into traditional wound dressings and advanced wound dressings. In 2024, the advanced wound dressings segment captured the largest share of the wound dressings market by type. This can be largely attributed to the growing incidence of chronic wounds such as diabetic foot ulcers, venous leg ulcers, and pressure ulcers, which require specialized and more effective treatment approaches. Additionally, factors such as the rising prevalence of diabetes, increased awareness among patients regarding wound management, advancements in wound care technologies, and the growing burden of hospital-acquired infections (HAIs) are contributing to the strong demand for advanced wound dressings. These products offer faster healing, reduced infection risk, and improved patient outcomes, further driving their adoption.

The surgical and traumatic wounds accounted for the largest market share in the wound dressings market.

Based on wound type, the market has been segmented into surgical and traumatic wounds, diabetic foot ulcers, pressure ulcers, venous leg ulcers, and burns & other wounds. Based on wound type, the surgical and traumatic wounds segment held the largest share of the wound dressings market in 2024. The significant share is primarily due to the rising number of surgical interventions worldwide and the increasing incidence of traumatic injuries resulting from accidents and falls. Furthermore, the growing elderly population, who are more prone to chronic conditions and surgeries, as well as the global rise in road traffic accidents, contribute to the segment's dominance. This segment is also projected to witness the highest CAGR during the forecast period, owing to continuous improvements in surgical techniques, post-operative care, and the increasing use of wound dressings in hospital and home care settings.

Asia Pacific is the fastest-growing region of the wound dressings market, by region.

The global wound dressings market is categorized into five key regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Among these, the Asia Pacific region is experiencing rapid growth, driven by an aging population and a rising prevalence of lifestyle-related conditions that contribute to chronic wounds. The increasing demand for high-quality healthcare services, along with substantial investments in hospital infrastructure and advanced medical technologies, is fueling the uptake of advanced wound care dressings. Additionally, the growing medical tourism industry in countries such as India, Thailand, and Singapore has led to a rise in surgical procedures, thereby increasing the need for effective post-operative wound care. With a strong focus among healthcare providers on enhancing patient outcomes and shortening recovery periods, the Asia Pacific market is expected to register the highest compound annual growth rate (CAGR) during the forecast period.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: C Level: 27%, Director Level: 18%, and Others: 55%

By Region: North America: 51%, Europe: 21%, Asia Pacific: 18%, Latin America: 6%, and Middle East & Africa: 4%

Note 1: Companies are classified into tiers based on their total revenue. As of 2023, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the wound dressings market are Solventum (US), Smith+ Nephew (UK), Convatec Group PLC (UK), Coloplast Group (Denmark), Cardinal Health (US), Molnlycke AB (Sweden), Integra LifeSciences Corporation (US), PAUL HARTMANN AG (Germany), B.Braun SE (Germany), Essity Aktiebolag (Sweden), Advanced Medical Solutions Group plc (UK), Mativ Holdings, Inc. (US), Owens & Minor (US), Lohmann & Rausher GmbH & Co. KG (Germany), Medline Industries, LP (US), DeRoyal Industries, Ine. (US), Winner Medical Co., LTD. (China), Advancis (UK), Hollister Incorporated (US), DermaRite Industries, LLC. (US), Mil Laboratories Pvt. Ltd. (India), Urgo Group (France), Gentell (US), Shield Line (US), and Focus Health Group (US)

Research Coverage

This report studies the wound dressings market based on type, wound type, end user, and country. The report also studies factors (such as drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends. It forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the strategies mentioned below to strengthen their market presence.

This report provides insights on the following pointers:

Analysis of key drivers (growing geriatric population, increasing cases of traumatic injuries, growing prevalence of chronic diseases

rising incidence of burn injuries, rising use of regenerative medicine for wound management,

and government initiatives and reimbursement policies), restraints (high cost of advanced wound care products, risks associated with use of advanced wound care products

and antimicrobial resistance challenges), opportunities (Growth opportunities in emerging economies, technological advancement in wound care, and home-care optimized solutions), challenges (lack of trained healthcare professionals, Limited awareness in underdeveloped regions, and data security and privacy concerns)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the wound dressings market

Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the wound dressings market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the wound dressings market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary sources

2.1.2.2 Key industry insights

2.1.2.3 Key data from primary sources

2.1.2.4 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach 1: Company revenue estimation approach

2.2.1.2 Approach 2: Presentations of companies and primary interviews

2.2.1.3 Approach 3: Primary interviews

2.2.1.4 Growth forecast

2.2.1.5 CAGR projections

2.2.2 TOP-DOWN APPROACH

2.3 MARKET BREAKDOWN & DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.4.1 STUDY-RELATED ASSUMPTIONS

2.4.2 PARAMETRIC ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 WOUND DRESSINGS MARKET OVERVIEW

4.2 ASIA PACIFIC: WOUND DRESSINGS MARKET SHARE, BY END USER AND COUNTRY

4.3 WOUND DRESSINGS MARKET: GEOGRAPHIC SNAPSHOT

4.4 WOUND DRESSINGS MARKET, REGIONAL MIX, 2025 VS. 2030

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing burden of chronic illnesses and conditions that impair natural wound healing

5.2.1.2 Rising cases of burn-related injuries globally

5.2.1.3 Increasing number of road accidents and trauma injuries

5.2.1.4 Elevated rate of cesarean deliveries in elderly mothers

5.2.1.5 Technological advancements in wound dressings

5.2.2 RESTRAINTS

5.2.2.1 High cost of advanced wound dressings

5.2.2.2 Potential risks and complications linked to wound dressings

5.2.2.3 Antimicrobial resistance challenges

5.2.3 OPPORTUNITIES

5.2.3.1 Growth opportunities in emerging economies

5.2.3.2 Supportive government initiatives and favorable reimbursement frameworks

5.2.4 CHALLENGES

5.2.4.1 Lack of trained healthcare professionals

5.2.4.2 Gaps in awareness and accessibility across emerging markets