대형 자연 냉매 히트펌프 시장 : 기술별, 최종 용도별, 냉매별, 용량별, 지역별 예측(-2030년)

Large scale Natural Refrigerant Heat Pump Market by Refrigerant (Ammonia, Carbon Dioxide, Hydrocarbons), by Capacity, by End Use, and by Region - Global Forecast to 2030

상품코드:1804837

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 270 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

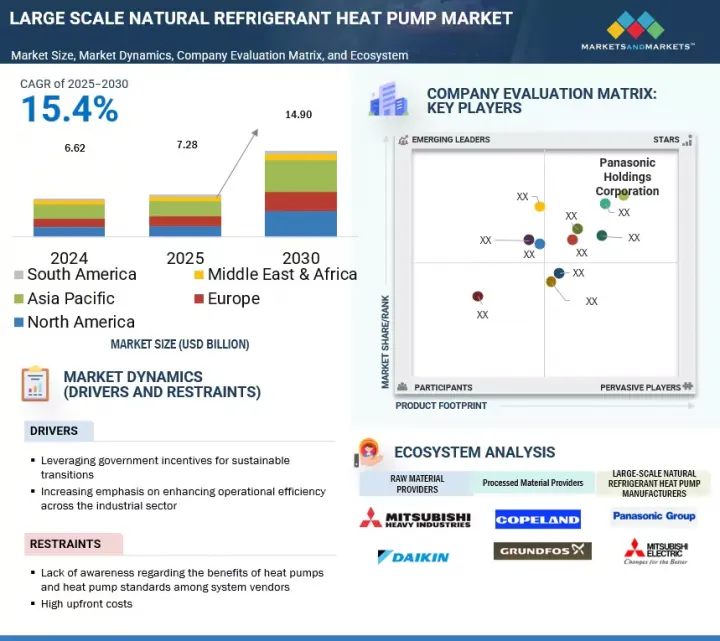

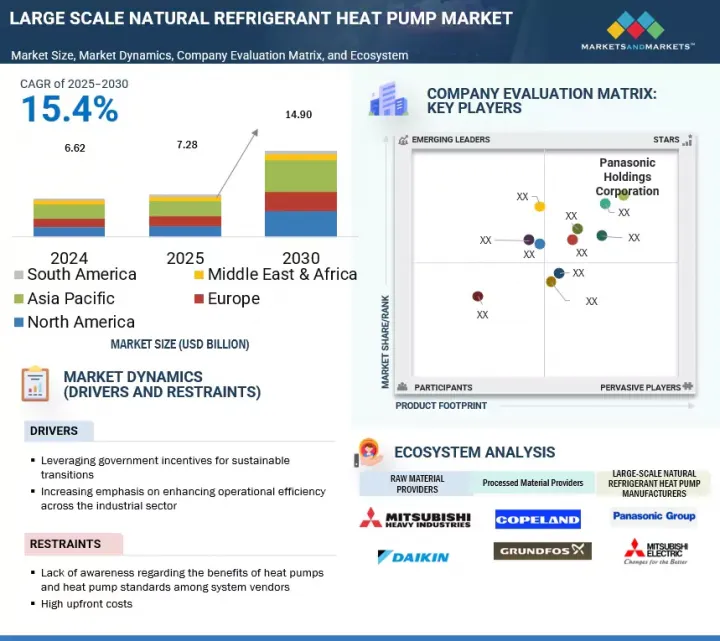

세계의 대형 자연 냉매 히트펌프 시장 규모는 2025년 72억 8,000만 달러에서 2030년에는 149억 달러에 이를 것으로 예측되어 CAGR은 15.4%를 나타낼 전망입니다.

조사 범위

조사 대상 연도

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러)

부문

기술별, 최종 용도별, 냉매별, 용량별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카

이해관계자 및 규제기관의 압력에 따라 대기업들은 환경, 사회, 지배구조(ESG) 전략의 일환으로 산업시설 및 상업시설에 자연냉매 히트펌프 도입을 늘리고 있습니다. 이러한 시스템은 온실가스 배출을 줄이고 ESG 보고의 투명성을 높여 지속가능성 및 기후 변화 대응 목표에 부합합니다. 저GWP 기술을 통합함으로써 기업은 기후 변화에 대한 적극적인 리더십을 발휘하고, 브랜드 인지도를 향상시키며, 진화하는 환경 규제와 투자자의 기대에 부응하는 미래지향적인 비즈니스를 운영할 수 있습니다.

산업 부문은 에너지 집약적인 열 공정에서 발생하는 이산화탄소 배출을 줄여야 한다는 규제와 사회적 압력에 직면해 있습니다. 보일러나 증기발생기와 같은 화석연료에 의존하는 기존 시스템은 산업계의 CO2 배출에 크게 기여하고 있습니다. 암모니아(R717)나 CO2(R744)와 같은 자연 냉매를 이용하는 대형 히트펌프는 고온의 열을 공급하기 위한 깨끗하고 에너지 효율적인 솔루션입니다. 이러한 시스템을 통해 산업계는 난방 작업을 전기화하여 이산화탄소 배출량을 크게 줄이고 국가와 기업의 탈탄소화 목표에 부합할 수 있습니다. 대규모 열 펌프 시스템은 화학, 식음료, 펄프 및 제지, 야금 등 다양한 산업 응용 분야에서 다양한 온도를 제공하는 많은 산업 공정에 대한 잠재적인 솔루션을 창출하고 뛰어난 효율로 고온 출력을 제공합니다. 대규모 자연 냉매 히트 펌프는 산업계가 연소 기반 시스템에서 전기화 된 열 에너지로 축을 옮길 수있는 실행 가능한 솔루션입니다. 열에너지의 전기화를 통해 산업계는 장기적인 온실가스 감축 전략을 수립하고, ESG 보고, 국가 기후 목표, 세계 탈탄소화 약속을 달성할 수 있습니다. 산업계는 지속가능성 전략뿐만 아니라 비즈니스 연속성을 우선시하는 경향이 있으며, 대규모 자연냉매 히트펌프가 성능, 컴플라이언스, 환경적 이점을 함께 제공할 가능성이 높습니다.

탄소 책임에 대한 전 세계적인 변화로 인해 화석연료 기반 난방 시스템에 의존하는 산업은 탄소세, 배출권 거래제, 규제 처벌로 인해 점점 더 많은 부담을 받고 있습니다. 이러한 경제적 압력은 더 깨끗하고 지속 가능한 기술에 대한 수요를 촉진하고 있습니다. CO2 기반 히트펌프는 직접적인 온실가스 배출을 크게 줄임으로써 설득력 있는 대안을 제공합니다. 이 히트펌프의 채택으로 산업계는 탄소 부채를 최소화하고, 배출 감소 인센티브를 활용하며, 장기적인 비용 예측 가능성을 향상시킬 수 있습니다. 저급 폐열을 회수하고 업그레이드할 수 있어 산업 탈탄화에 매우 효과적입니다. 또한, CO2 기반 시스템은 정부 보조금, 탄소배출권 제도, 세제 혜택의 대상이 되고 있으며, 개보수 및 그린필드 프로젝트 모두에서 재정적 타당성이 향상되고 있습니다. 생산 규모를 확대하고 R-744 시스템의 성능을 향상시키는 OEM이 증가함에 따라, 이 부문은 2025년까지 자연 냉매 시장을 선도하고 세계 순 제로 난방 기술로의 전환을 위한 초석이 될 것입니다.

탈탄소화를 위한 광범위한 노력의 일환으로 북미 산업계는 공정 난방의 전기화로 전환을 가속화하고 있습니다. 이러한 전환은 화석연료에 대한 의존도를 줄이고, 진화하는 기후 규제를 준수하며, 기업의 지속가능성 목표를 달성하기 위한 필요성에 의해 추진되고 있습니다. 암모니아, CO2 등 자연 냉매를 사용하는 대형 히트펌프는 기존 가스 연소 보일러를 대체할 수 있는 전략적 솔루션으로 떠오르고 있습니다. 이러한 시스템은 에너지 효율이 높고, 온실 가스 배출량이 적으며, 재생에너지와 원활하게 통합할 수 있기 때문에 산업 환경에서 전기화의 중요한 도구가 되고 있습니다.

Siemens Energy(독일),Johnson Controls(아일랜드),Copeland LP(미국),GEA Group Aktiengesellschaft(독일),Mitsubishi Electric Corporation(일본), Guangdong PHNIX Eco-energy Solution Ltd. Guangdong PHNIX Eco-energy Solution Ltd.(중국),ARANER(중국),Copeland LP(미국),GEA Group Aktiengellschaft(중국),ARANER(영국),Star Refrigeration(영국)),Clade Engineering Systems Ltd(영국),AGO GmbH Energie+Anlagen(독일),Lync(미국),SKADEC GmbH(독일),Akkawa Manufacturing(일본),Fenagy A/S(덴마크),Pure Thermal(미국) Enerblue srl(이탈리아), ALFA LAVAL(스웨덴), NH3 Solutions(덴마크), Thermax Limited(인도)가 대형 자연냉매 히트펌프 시장의 주요 기업입니다. 이 조사에는 대형 자연냉매 히트펌프 시장의 주요 업체들의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석이 포함되어 있습니다.

대형 자연냉매 히트펌프 시장을 냉매별(암모니아(R-717), 이산화탄소(R-744), 탄화수소, 기타 냉매), 용량별(20년-200kW, 200-500kW, 500-1000kW, 1000kW 이상), 최종 용도별(상업용, 산업용), 기술별(공랭식, 수열식, 공기열원식, 수열식, 하이브리드) 히트펌프,공기 대 물 히트펌프,수원 히트펌프,지열(지열) 히트펌프,하이브리드 히트펌프),지역별(북미,유럽,아시아태평양,중동 및 아프리카,남미)로 정의,설명,예측했습니다. 이 보고서의 조사 범위는 대형 자연냉매 히트펌프 시장의 성장에 영향을 미치는 시장 성장 촉진요인 및 과제 등 주요 요인에 대한 자세한 정보를 포함하고 있습니다. 주요 업계 진출업체에 대한 철저한 분석을 통해 사업 개요, 솔루션, 서비스, 계약, 파트너십, 합의, 합병 및 인수와 같은 주요 전략, 대형 자연냉매 히트펌프 시장과 관련된 최근 동향에 대한 통찰력을 제공합니다. 이 보고서는 대형 자연냉매 히트펌프 시장 생태계에서 향후 신흥기업들의 경쟁 분석을 다루고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 분석

합성 냉매와 천연 냉매

공급망 분석

생태계 분석

기술 분석

무역 분석

2025년-2026년 주요 컨퍼런스 및 이벤트

규제 상황

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

특허 분석

사례 연구 분석

투자 및 자금조달 시나리오

AI/생성형 AI가 대형 자연 냉매 히트펌프 시장에 미치는 영향

세계 거시경제 전망

2025년 미국 관세가 대형 자연 냉매 히트펌프 시장에 미치는 영향

제6장 대형 자연 냉매 히트펌프 시장(기술별)

서론

AIR-TO-AIR 히트펌프

AIR-TO-WATER 히트펌프

수원 히트펌프

지열 히트 펌프

하이브리드 히트펌프

제7장 대형 자연 냉매 히트펌프 시장(최종 용도별)

서론

상업

산업

제8장 대형 자연 냉매 히트펌프 시장(냉매별)

서론

암모니아(R-717)

이산화탄소(R-744)

탄화수소

기타

제9장 대형 자연 냉매 히트펌프 시장(용량별)

서론

20-200kW

201-500kW

501-1,000KW

1,000KW 이상

제10장 대형 자연 냉매 히트펌프 시장(지역별)

서론

북미

미국

캐나다

멕시코

아시아태평양

중국

일본

한국

기타

유럽

독일

영국

프랑스

기타

남미

아르헨티나

브라질

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

제11장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점, 2020년-2025년

시장 점유율 분석, 2024년

시장 평가 프레임워크

매출 분석, 2020년-2024년

제품 비교

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제12장 기업 개요

주요 시장 진출기업

SIEMENS ENERGY

MITSUBISHI ELECTRIC CORPORATION

JOHNSON CONTROLS

PANASONIC HOLDINGS CORPORATION

GEA GROUP AKTIENGESELLSCHAFT

ALFA LAVAL

THERMAX LIMITED

EVERLLENCE

AGO GMBH ENERGIE+ANLAGEN

COPELAND LP

GUANGDONG PHNIX ECO-ENERGY SOLUTION LTD.

STAR REFRIGERATION

CLADE ENGINEERING SYSTEMS LTD

LYNC

SKADEC GMBH

기타 기업

NH3 SOLUTIONS

ARANER

EMICON AC S.P.A.

COMPACT KALTETECHNIK GMBH

ECOTECH SOLUTIONS

MAYEKAWA MFG. CO., LTD.

FENAGY A/S

PURE THERMAL

TEKO GMBH

ENERBLUE SRL

제13장 부록

LSH

영문 목차

영문목차

The global large scale natural refrigerant heat pump market is projected to reach USD 14.90 billion by 2030 from USD 7.28 billion in 2025, registering a CAGR of 15.4%.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion)

Segments

Refrigerant, Capacity, End Use, Technology

Regions covered

North America, Europe, Asia Pacific, South America, Middle East, and Africa

In response to growing pressure from stakeholders and regulatory bodies, large corporations are increasingly adopting natural refrigerant heat pumps across industrial and commercial facilities as part of their Environmental, Social, and Governance (ESG) strategies. These systems align with sustainability and climate action goals by reducing greenhouse gas emissions and enhancing transparency in ESG reporting. By integrating low-GWP technologies, companies demonstrate proactive climate leadership, improve brand reputation, and future-proof operations against evolving environmental regulations and investor expectations.

"By end use, the industrial segment is expected to be the fastest-growing market during the forecast period."

Industrial sectors are facing growing regulatory and societal pressure to reduce carbon emissions from energy-intensive thermal processes. Traditional systems reliant on fossil fuels, such as boilers and steam generators, contribute significantly to industrial CO2 emissions. Large scale heat pumps utilizing natural refrigerants like ammonia (R717) and CO2 (R744) present a clean, energy-efficient solution for delivering high-temperature heat. These systems enable industries to electrify their heating operations, significantly lower their carbon footprint, and align with national and corporate decarbonization goals-without compromising on performance or reliability. Large scale heat pump systems are providing high-temperature output with remarkable efficiency, creating a potential solution to the many industrial processes to deliver a range of temperatures encountered within industrial applications, in the chemical, food & beverage, pulp & paper, and metallurgy sectors. Large scale natural refrigerant heat pumps are viable solutions for industries to pivot from combustion-based systems to an electrified thermal energy. By electrifying thermal energy, industries can define long-term GHG emissions reduction strategies and meet ESG reporting, national climate targets, and global decarbonization commitments. As industries not only position for sustainability strategies, they are likely to prioritize operational continuity, and it is highly likely that large scale natural refrigerant heat pumps may deliver performance, compliance, and environmental benefits together.

"By refrigerant, the Carbon dioxide (R-744) segment is anticipated to dominate the market in 2025."

With the global shift toward carbon accountability, industries reliant on fossil-fuel-based heating systems are increasingly burdened by carbon taxes, emissions trading schemes, and regulatory penalties. These financial pressures are driving demand for cleaner, more sustainable technologies. CO2-based heat pumps offer a compelling alternative by significantly lowering direct greenhouse gas emissions. Their adoption enables industries to minimize carbon liabilities, access emissions reduction incentives, and improve long-term cost predictability-while aligning with climate commitments and sustainability targets. Its capability to recover and upgrade low-grade waste heat makes it highly effective for industrial decarbonization. Moreover, CO2-based systems are increasingly eligible for government subsidies, carbon credit schemes, and tax incentives, which improve their financial viability for both retrofits and greenfield projects. With a growing number of OEMs scaling up production and enhancing R-744 system performance, the segment is set to lead the natural refrigerant market by 2025-serving as a cornerstone in the global shift toward net-zero heating technologies.

"By region, North America is expected to account for the second-largest market share during the forecast period."

As part of broader efforts to decarbonize operations, North American industries are accelerating the shift toward electrified process heating. This transition is driven by the need to reduce dependence on fossil fuels, comply with evolving climate regulations, and meet corporate sustainability targets. Large scale heat pumps using natural refrigerants like ammonia and CO2 are emerging as strategic solutions for replacing conventional gas-fired boilers. These systems offer high energy efficiency, lower greenhouse gas emissions, and seamless integration with renewable electricity sources-making them vital tools in the industrial electrification landscape.

In-depth interviews were conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 60%, Tier 2 - 30%, and Tier 3 - 10%

By Designation: Managers - 45%, CEO's and Directors - 30%, and Executives - 25%

By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Middle East & Africa - 5% and South America - 10%

Note: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million. Others include sales managers, engineers, and regional managers.

Siemens Energy (Germany), Johnson Controls (Ireland), Copeland LP (US), GEA Group Aktiengesellschaft. (Germany), Mitsubishi Electric Corporation (Tokyo), Guangdong PHNIX Eco-energy Solution Ltd. (China), ARANER (United Kingdom), Star Refrigeration (United Kingdom), Clade Engineering Systems Ltd (United Kingdom), AGO GmbH Energie + Anlagen (Germany), Lync (US), SKADEC GmbH. (Germany), MAYEKAWA MFG. CO., LTD. (Japan), Fenagy A/S. (Denmark), Pure Thermal (US), Enerblue srl (Italy), ALFA LAVAL (Sweden), NH3 Solutions (Denmark), Thermax Limited (India) are the key players in the large scale natural refrigerant heat pump market. The study includes an in-depth competitive analysis of these key players in the large scale natural refrigerant heat pump market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report defines, describes, and forecasts the large scale natural refrigerant heat pump market by Refrigerant (Ammonia (R-717), Carbon dioxide (R-744), Hydrocarbons, Other Refrigerants), Capacity (20-200 kW, 200-500kW, 500-1000kW, Above 1000 kW), End Use (commercial, Industrial), Technology (Air-to-Air Heat Pumps, Air-to-Water Heat Pumps, Water Source Heat Pumps, Ground-Source (Geothermal) Heat Pumps, Hybrid Heat Pumps), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of large scale natural refrigerant heat pump market. A thorough analysis of the key industry players has provided insights into their business overview, solutions, and services; key strategies such as contracts, partnerships, agreements, mergers, and acquisitions; and recent developments associated with the large scale natural refrigerant heat pump market. This report covers the competitive analysis of upcoming startups in the large scale natural refrigerant heat pump market ecosystem.

Key Benefits of Buying the Report

The report includes the analysis of key drivers (Mounting demand for low-emission energy amid rapid industrialization, shifting preference from coal to cleaner alternative fuels, and increasing adoption of large scale natural refrigerant heat pumps.

in power generation, heating, and other industrial applications), restraints (requirement for substantial financial resources and long payback period, issues related to compliance with safety, environmental, and land use regulations), opportunities (increasing reliance on natural gas to curb carbon footprint, growing focus on diversifying energy sources and enhancing energy security, and rising emphasis on supporting regions with under-developed gas infrastructure) and challenges (climate risks and high operational costs of Floating storage regasification unit (FSRU), and geopolitical instability impacting supply security) influencing the growth of the large scale natural refrigerant heat pump market.

Product Development/Innovation: EPC companies are effectively using next-level project management, pre-fabrication, and combined design capabilities to increase efficiency and decrease complexity at the site. Innovations in the large scale natural refrigerant heat pump sector include AI for scheduling, remote construction monitoring, and 3D modeling digital twins to enhance precision and reduce delays. The industry increasingly adopts low-carbon designs with carbon capture, renewable energy, and waste heat recovery. These trends help EPC contractors provide flexible, scalable, and energy-compliant large scale natural refrigerant heat pump infrastructure while supporting global demand growth and decarbonization efforts.

Market Development: In October 2023, Siemens Energy received a contract from MVV GmbH to supply and integrate a 20 MWth river-source heat pump into Mannheim's district heating network. The system uses Rhine River water and renewable electricity to deliver heat up to 99 °C, serving around 3,500 households and reducing ~10,000 tons of CO2 annually.

Market Diversification: The report offers a comprehensive analysis of the strategies employed by EPC players to facilitate market diversification. It outlines innovative service and operating models, as well as new partnership frameworks across various regions, underpinned by technology-driven business lines. The findings emphasize opportunities for expansion beyond traditional operations, identifying geographical areas and customer segments that are currently served but remain underserved and are suitable for strategic entry.

Competitive Assessment: The report provides an in-depth assessment of market shares, growth strategies, and service offerings of leading players such as Siemens Energy (Germany), Johnson Controls (Ireland), Copeland LP (US), GEA Group Aktiengesellschaft. (Germany), Mitsubishi Electric Corporation (Tokyo), Guangdong PHNIX Eco-energy Solution Ltd. (China), ARANER (United Kingdom), Star Refrigeration (United Kingdom), Clade Engineering Systems Ltd (United Kingdom), AGO GmbH Energie + Anlagen (Germany), among others, in the large scale natural refrigerant heat pump market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.2 PRIMARY AND SECONDARY DATA

2.2.1 SECONDARY DATA

2.2.1.1 List of key secondary sources

2.2.1.2 Key data from secondary sources

2.2.2 PRIMARY DATA

2.2.2.1 List of primary interview participants

2.2.2.2 Key data from primary sources

2.2.2.3 Key industry insights

2.2.2.4 Breakdown of primaries

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 MARKET SIZE ESTIMATION

2.4.1 BOTTOM-UP APPROACH

2.4.2 TOP-DOWN APPROACH

2.4.3 DEMAND-SIDE ANALYSIS

2.4.3.1 Demand-side assumptions

2.4.3.2 Demand-side calculations

2.4.4 SUPPLY-SIDE ANALYSIS

2.4.4.1 Supply-side assumptions

2.4.4.2 Supply-side calculations

2.5 GROWTH PROJECTION

2.6 RESEARCH LIMITATIONS

2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET

4.2 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY REFRIGERANT

4.3 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY CAPACITY

4.4 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY END USE

4.5 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY TECHNOLOGY

4.6 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Government incentives for sustainable transition

5.2.1.2 Increasing emphasis on enhancing operational efficiency across industrial sector

5.2.2 RESTRAINTS

5.2.2.1 Lack of awareness about heat pump standards and benefits among system vendors

5.2.2.2 High upfront costs

5.2.3 OPPORTUNITIES

5.2.3.1 Cold climate optimization

5.2.3.2 Industrial decarbonization initiatives

5.2.4 CHALLENGES

5.2.4.1 Availability of low-cost fossil energy-based alternative technologies

5.2.4.2 Energy source dependency in heat pump efficiency

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 PRICING RANGE OF LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS, BY TECHNOLOGY, 2024

5.4.2 AVERAGE SELLING PRICE TREND OF LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS, BY REGION, 2022-2024

5.5 SYNTHETIC REFRIGERANT VS. NATURAL REFRIGERANT

5.6 SUPPLY CHAIN ANALYSIS

5.7 ECOSYSTEM ANALYSIS

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Air-to-air heat pumps

5.8.1.2 Air-to-water heat pumps

5.8.1.3 Water-source heat pumps

5.8.1.4 Hybrid heat pumps

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Smart-grid and energy management systems

5.8.2.2 Smart controls and automation technologies

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Heat recovery ventilation systems

5.8.3.2 Internet of Things devices

5.9 TRADE ANALYSIS

5.9.1 EXPORT SCENARIO (841861)

5.9.2 IMPORT SCENARIO (841861)

5.10 KEY CONFERENCES AND EVENTS, 2025-2026

5.11 REGULATORY LANDSCAPE

5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.2 REGULATIONS

5.12 PORTER'S FIVE FORCES ANALYSIS

5.12.1 THREAT OF NEW ENTRANTS

5.12.2 THREAT OF SUBSTITUTES

5.12.3 BARGAINING POWER OF SUPPLIERS

5.12.4 BARGAINING POWER OF BUYERS

5.12.5 THREAT OF NEW ENTRANTS

5.12.6 INTENSITY OF COMPETITIVE RIVALRY

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 PATENT ANALYSIS

5.15 CASE STUDY ANALYSIS

5.15.1 ELIMINATION OF FOSSIL-FUEL BOILERS WITH HIGH-EFFICIENCY HEAT PUMP INTEGRATION

5.15.2 CARRIER'S AQUAEDGE 19DV CHILLER WITH HEAT RECOVERY INSTALLED TO DRIVE PROCESS INNOVATION AT INDUSTRIAL SITE

5.15.3 CUTTING EMISSIONS IN BEER PRODUCTION WITH HIGH-TEMPERATURE HEAT PUMPS

5.16 INVESTMENT AND FUNDING SCENARIO

5.17 IMPACT OF AI/GEN AI ON LARGE-SCALE NATURAL REFRIGERANT HEAT PUMP MARKET

5.17.1 ADOPTION OF AI/GEN AI IN LARGE-SCALE NATURAL REFRIGERANT HEAT PUMP APPLICATIONS

5.17.2 IMPACT OF AI/GEN AI ON LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS SUPPLY CHAIN, BY REGION

5.18 GLOBAL MACROECONOMIC OUTLOOK

5.18.1 INTRODUCTION

5.18.2 FOCUS ON LONG-TERM ENERGY SECURITY

5.18.3 TECHNOLOGICAL ADVANCEMENTS

5.18.4 FINANCING AND GOVERNMENT POLICY SUPPORT

5.18.5 HIGH CAPEX AMID INFLATION

5.19 IMPACT OF 2025 US TARIFF ON LARGE-SCALE NATURAL REFRIGERANT HEAT PUMP MARKET

5.19.1 INTRODUCTION

5.19.2 KEY TARIFF RATES

5.19.3 PRICE IMPACT ANALYSIS

5.19.4 IMPACT ON COUNTRIES/REGIONS

5.19.4.1 US

5.19.4.2 Europe

5.19.4.3 Asia Pacific

5.19.5 IMPACT ON END USE

6 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY TECHNOLOGY

6.1 INTRODUCTION

6.2 AIR-TO-AIR HEAT PUMPS

6.2.1 LOWER GWP IMPACT AND ENVIRONMENT-FRIENDLY HEATING AND COOLING SOLUTIONS TO DRIVE DEMAND

6.3 AIR-TO-WATER HEAT PUMPS

6.3.1 GROWING ADOPTION OF AIR-BASED HEATING SOLUTIONS TO DRIVE DEMAND

6.4 WATER-SOURCE HEAT PUMPS

6.4.1 HIGH OPERATIONAL EFFICIENCY TO BOOST ADOPTION

6.5 GROUND-SOURCE (GEOTHERMAL) HEAT PUMPS

6.5.1 POLICY MEASURES FOR DEPLOYMENT OF GEOTHERMAL HEAT PUMPS TO DRIVE MARKET

6.6 HYBRID HEAT PUMPS

6.6.1 SEAMLESS INTEGRATION WITH EXISTING INFRASTRUCTURE TO DRIVE DEMAND

7 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY END USE

7.1 INTRODUCTION

7.2 COMMERCIAL

7.2.1 INVESTMENT IN ENERGY-EFFICIENT HEAT PUMPS FOR LONG-TERM SAVINGS TO DRIVE SEGMENT GROWTH

7.2.2 EDUCATIONAL INSTITUTES

7.2.2.1 Sustainable learning environments empowered by heat pumps to fuel market growth

7.2.3 HOSPITALITY SPACES

7.2.3.1 Modern infrastructure in hospitality spaces to drive market growth

7.2.4 OTHER COMMERCIAL BUILDINGS

7.3 INDUSTRIAL

7.3.1 BOOST IN INDUSTRIAL PROCESS EFFICIENCY TO SPUR DEMAND

7.3.2 FOOD & BEVERAGES

7.3.2.1 Reduction in greenhouse gas emission to fuel market growth

7.3.3 PULP & PAPER

7.3.3.1 Sustainable heating for growing packaging industry to boost market growth

7.3.4 CHEMICALS & PETROCHEMICALS

7.3.4.1 Revolutionized high-heat industrial applications to drive market growth

7.3.5 OTHER INDUSTRIES

8 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMP MARKET, BY REFRIGERANT

8.1 INTRODUCTION

8.2 AMMONIA (R-717)

8.2.1 HIGH EFFICIENCY OF LOW-CHARGE AMMONIA HEAT PUMPS TO DRIVE MARKET

8.3 CARBON DIOXIDE (R-744)

8.3.1 REVOLUTIONIZED LOW-TEMPERATURE APPLICATIONS WITH CO2 REFRIGERATION TO SPUR DEMAND

8.4 HYDROCARBONS

8.4.1 ADVANCED COOLING SYSTEMS WITH HIGH LATENT HEAT HYDROCARBONS TO CONTRIBUTE TO SEGMENTAL GROWTH

8.5 OTHER REFRIGERANTS

9 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY CAPACITY

9.1 INTRODUCTION

9.2 20-200 KW

9.2.1 SMALL-SCALE COMMERCIAL AND LIGHT INDUSTRIAL DECARBONIZATION TO DRIVE SEGMENT

9.3 201-500 KW

9.3.1 MID-SCALE COMMERCIAL INTEGRATION TO DRIVE USE

9.4 501-1,000 KW

9.4.1 WIDELY USED IN LARGE-SCALE COMMERCIAL & INDUSTRIAL PROCESS APPLICATIONS

9.5 ABOVE 1,000 KW

9.5.1 FOCUS ON UTILITY-SCALE & DISTRICT ENERGY DECARBONIZATION TO DRIVE DEMAND

10 LARGE-SCALE NATURAL REFRIGERANT HEAT PUMPS MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 US

10.2.1.1 Government focus on cold-climate heat pumps to bolster market growth

10.2.2 CANADA

10.2.2.1 Focus on reduction of greenhouse gas (GHG) emissions to fuel demand

10.2.3 MEXICO

10.2.3.1 Increasing focus on regulatory standards and energy-saving initiatives to drive market

10.3 ASIA PACIFIC

10.3.1 CHINA

10.3.1.1 Action plan to advance heat pump industry to fuel demand

10.3.2 JAPAN

10.3.2.1 EcoCute program under Kyoto protocol framework to augment market growth

10.3.3 SOUTH KOREA

10.3.3.1 Increasing demand for energy-efficient heating technology to propel market growth

10.3.4 REST OF ASIA PACIFIC

10.4 EUROPE

10.4.1 GERMANY

10.4.1.1 Federal incentive and subsidies on use of natural refrigerant products to drive market

10.4.2 UK

10.4.2.1 Climate-friendly natural refrigerant systems and renewable energy transition to propel demand

10.4.3 FRANCE

10.4.3.1 Domestic manufacturing and rising utilization of energy-efficient heating systems to boost market growth

10.4.4 REST OF EUROPE

10.5 SOUTH AMERICA

10.5.1 ARGENTINA

10.5.1.1 Significant focus on sustainability to drive market growth

10.5.2 BRAZIL

10.5.2.1 Adoption of renewable energy to fuel market growth

10.5.3 REST OF SOUTH AMERICA

10.6 MIDDLE EAST & AFRICA

10.6.1 GCC COUNTRIES

10.6.1.1 Saudi Arabia

10.6.1.1.1 Energy efficiency program in industrial & commercial sector to boost market growth

10.6.1.2 Other GCC countries

10.6.1.2.1 Kigali Amendment and green building frameworks encouraging low-GWP systems lead to market growth

10.6.2 SOUTH AFRICA

10.6.2.1 Emissions reduction goals to boost market growth

10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2025

11.3 MARKET SHARE ANALYSIS, 2024

11.4 MARKET EVALUATION FRAMEWORK

11.5 REVENUE ANALYSIS, 2020-2024

11.6 PRODUCT COMPARISON

11.7 COMPANY VALUATION AND FINANCIAL METRICS

11.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.8.1 STARS

11.8.2 EMERGING LEADERS

11.8.3 PERVASIVE PLAYERS

11.8.4 PARTICIPANTS

11.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.8.5.1 Company footprint

11.8.5.2 Region footprint

11.8.5.3 Refrigerant footprint

11.8.5.4 Capacity footprint

11.8.5.5 End-use footprint

11.8.5.6 Technology footprint

11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024