유체 이송 시스템 시장 : 추진력·구성요소별, 시스템 유형별, 차종별, 지역별 - 예측(-2032년)

Fluid Transfer System Market by Propulsion & Component (Petrol/Gasoline, Diesel, CNG, Battery Electric, Plug-In Hybrid Electric), System Type, Vehicle Type (Passenger Cars, LCVs, Trucks, and Buses), and Region - Global Forecast to 2032

상품코드:1802927

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 434 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

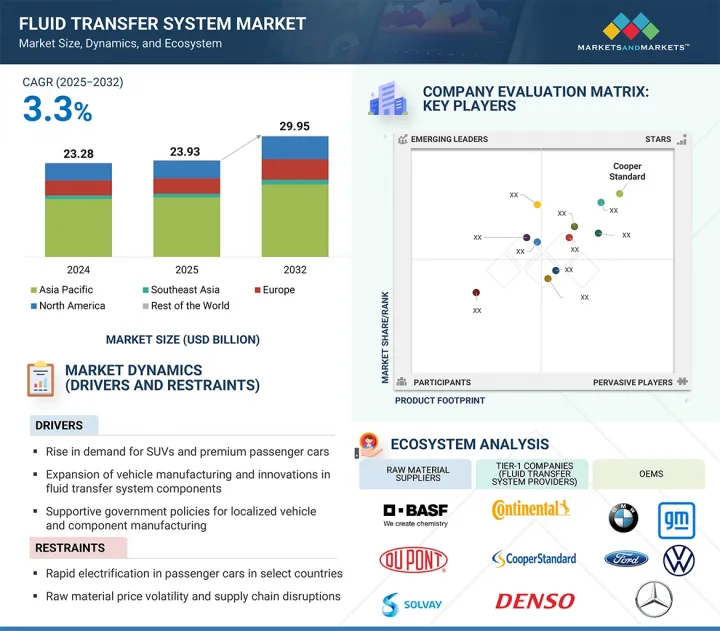

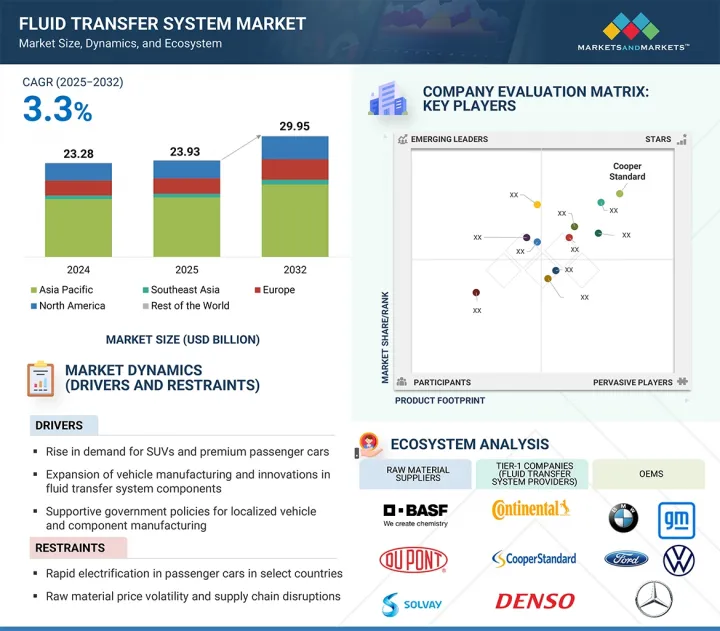

세계의 유체 이송 시스템 시장 규모는 2025년 239억 3,000만 달러에서 2032년까지 299억 5,000만 달러에 달할 것으로 예측되며, CAGR로 3.3%의 성장이 전망됩니다.

조사 범위

조사 대상 연도

2021-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

1,000대, 10억 달러

부문

추진력·구성요소, 차종, 시스템 유형, 지역

대상 지역

아시아태평양, 동남아시아, 유럽, 북미, 기타 지역

유체 이송 시스템 시장은 자동차 생산량 증가, 배기가스 규제 강화, 첨단 모빌리티 기술의 광범위한 채택에 힘입어 안정적인 성장세를 보일 것으로 예상됩니다. 유체 이송 시스템에 대한 수요는 연료, 공기, 오일, 냉각수, 기타 내연기관차 및 전기자동차의 성능, 효율성, 안전에 필수적인 유체를 관리하는 중요한 역할을 담당하고 있습니다.

고급 승용차로의 전환은 고급 에어컨, 서스펜션, 배기가스 제어 라인의 사용을 확대하고, BS-VI, Euro 6 등의 규제 강화는 SCR, DPF, EVAP 라인의 수요를 증가시키고 있습니다. 마찬가지로, EV의 보급은 배터리, 모터, 파워 일렉트로닉스의 냉각 라인을 포함한 열 관리 부품에 대한 새로운 기회를 촉진하고 있습니다.

"서스펜션 시스템은 예측 기간 동안 큰 성장률을 보일 것으로 예상됩니다."

유체 이송 시스템 시장의 서스펜션 시스템 부문은 차량의 안정성, 승차감, 핸들링 개선에 대한 수요 증가로 인해 예측 기간 동안 큰 성장을 보일 것으로 예상됩니다. 하이드로 서스펜션 라인, 에어 서스펜션 라인, 쇼크 업소버 호스, 안티 롤 호스 등 서스펜션 유체 이송 관련 부품은 차량의 안정성을 유지하고 차체 롤을 최소화하며 차고 조정 및 하중 관리를 가능하게 하는 데 필수적입니다. 승용차에서는 고급화 추세로 인해 에어 서스펜션과 첨단 감쇠 시스템의 채택이 가속화되고 있으며, 상용차에서는 하이드로 서스펜션 라인과 에어 서스펜션 라인이 내구성과 하중 제어를 위해 필수적입니다. 전기 버스로의 전환은 수요를 더욱 증가시킬 것입니다. 이러한 차량은 보다 부드러운 승차감을 보장하고 배터리 무게를 상쇄하기 위해 에어 서스펜션 시스템을 사용하는 경우가 많아졌기 때문입니다. 서스펜션 부문은 유체 이송 시스템 시장에서 가장 유망한 성장 분야 중 하나로, 제조업체들이 편안함, 성능, 안전에 대한 소비자의 기대에 부응하기 위해 첨단 서스펜션 기술에 투자하고 있기 때문입니다.

"승용차가 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예상됩니다."

승용차 부문은 차량 대수 증가와 첨단 차량 기술의 급속한 채택으로 인해 예측 기간 동안 유체 이송 시스템 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 고급차와 중급차의 수요 증가로 에어 서스펜션 시스템과 듀얼 존 또는 뒷좌석 에어컨의 사용이 확대되면서 특수 에어 서스펜션과 A/C 유체 이송 라인에 대한 요구가 증가하고 있습니다. 인도의 BS-VI, 유럽의 Euro 6 등 전 세계적으로 배기가스 규제가 강화되면서 선택적 촉매 환원(SCR), 디젤 미립자 필터(DPF) 라인 및 기타 배기가스 후처리 부품의 채택이 가속화되고 있습니다. 동시에 하이브리드 자동차 및 전기 승용차의 보급은 기존의 연료 및 윤활 라인 수요에 더해 배터리, 모터, DC-DC 컨버터 냉각수 호스에 대한 새로운 기회를 창출하고 있습니다. 이러한 규제 대응, 편의성 향상, 전기화의 복합적인 효과로 인해 승용차 부문은 유체 이송 시스템에서 가장 크고 역동적인 시장으로 남을 것으로 보입니다.

"유럽의 유체 이송 시스템 시장은 예측 기간 동안 큰 성장을 보일 것으로 예상됩니다."

유럽은 탄탄한 자동차 제조 기반, 기술 리더십, 엄격한 규제 프레임워크에 힘입어 예측 기간 동안 유체 이송 시스템 시장에서 큰 성장을 보일 것으로 예상됩니다. 이 지역에는 Volkswagen, BMW, Mercedes-Benz, Renault, Stellantis, Volvo, Scania 등의 상위 OEM과 TI Fluid Systems, Continental AG, Gates Corporation, Parker Hannifin 등의 Tier-1 공급업체 및 유체 이송 전문가들이 존재하여 지속적인 기술 혁신과 대규모 공급 능력을 보장합니다. Euro 6d 규제 및 향후 Euro 7 규제를 포함한 규제 변경으로 인해 승용차, 트럭, 버스 전반에 걸쳐 더욱 강화되는 CO2 및 NOx 저감 기준을 충족하기 위한 첨단 배기가스 규제 라인, 배기가스 재순환 파이프, 열 관리 호스에 대한 수요가 증가하고 있습니다.

세계의 유체 이송 시스템 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 경쟁 상황, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

유체 이송 시스템 시장 기업에서 매력적인 기회

유체 이송 시스템 시장 : 차종별

유체 이송 시스템 시장 : 시스템 유형별

유체 이송 시스템 시장 : 추진력별

유체 이송 시스템 시장 : 지역별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향과 혼란

가격 책정 분석

주요 기업이 제공하는 유체 이송 부품 평균판매가격

평균판매가격 동향 : 차종별

평균판매가격 동향 : 지역별

생태계 분석

밸류체인 분석

사례 연구 분석

VCOLLAB 솔루션이 COOPER STANDARD의 시뮬레이션 효율을 향상

FLUID COOLING SYSTEMS의 공정 냉각 솔루션이 FORD의 알루미늄 용접 공정을 강화

LUCAS-MILHAUPT의 플럭스 프리 브레이징 공정이 FORD의 연료 센서 누출 방지를 보장

특허 분석

기술 분석

주요 기술

보완 기술

인접 기술

무역 분석

수입 시나리오(HS 코드 4009)

수출 시나리오(HS 코드 4009)

관세와 규제 상황

관세 데이터

규제기관, 정부기관, 기타 조직

유체 이송 시스템 시장 규제 분석

주요 회의와 이벤트(2025-2026년)

주요 이해관계자와 구입 기준

AI의 영향

OEM과 Tier-1조달/채용 전략

OEM 조달 전략

Tier-1채용/차별화 전략

디지털화와 스마트 매뉴팩처링의 대처

모듈형 자동화 추적 가능한 생산 시스템

예지보전과 실시간 프로세스 최적화를 가능하게 하는 스마트 매뉴팩처링 플랫폼

임베디드 센서 기술과 첨단 재료

전기화를 지지하는 확장가능한 디지털 제조

AI 기반 품질 체크, 적층 가공, 5G 연결성

전기화로의 전환

기존 ICE 유체 이송 시스템 쇠퇴

EV 구동 유체 이송 시스템 수요 증가

모듈형 통합 어셈블리 증가

애프터마켓의 ICE 유체 이송 시스템으로부터의 전환

재료 분석 : 유체 이송 구성요소별

공급업체 분석 : 유체 이송 시스템별

제6장 유체 이송 시스템 시장 : 추진력·구성요소별

소개

가솔린

디젤

CNG

배터리 전기

플러그인 하이브리드 전기

중요한 인사이트

제7장 유체 이송 시스템 시장 : 차종별

소개

승용차

소형 상용차

트럭

버스

중요한 인사이트

제8장 유체 이송 시스템 시장 : 시스템 유형별

소개

엔진

트랜스미션

파워 스티어링

연료 공급

열 관리

서스펜션

브레이크·클러치

배기

바디·외장

윤활

중요한 인사이트

제9장 유체 이송 시스템 시장 : 지역별

소개

아시아태평양

거시경제 전망

중국

인도

일본

한국

동남아시아

거시경제 전망

태국

인도네시아

베트남

필리핀

북미

거시경제 전망

미국

캐나다

멕시코

유럽

미시경제 전망

독일

프랑스

이탈리아

스페인

영국

기타 유럽

기타 지역

거시경제 전망

남아프리카공화국

케냐

이집트

제10장 경쟁 구도

소개

주요 진출 기업의 전략/강점(2022-2025년)

시장 점유율 분석(2024년)

매출 분석(2020-2024년)

기업 평가와 재무 지표

브랜드/제품의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제11장 기업 개요

주요 기업

COOPER STANDARD

TI FLUID SYSTEMS

SUMITOMO RIKO COMPANY LIMITED

PARKER HANNIFIN CORP

GATES CORPORATION

SANOH INDUSTRIAL CO., LTD.

CONTINENTAL AG

DENSO CORPORATION

HUTCHINSON

NICHIRIN

USUI CO. LTD.

KONGSBERG AUTOMOTIVE

AKWEL

IMPERIAL AUTO

ROBERT BOSCH GMBH

기타 기업

LANDER TUBULAR PRODUCTS

TRISTONE

FLEXITECH

DELFINGEN

TALBROS

MANULI RYCO GROUP

GRACO INC.

NEWAGE INDUSTRIES

ARAYMOND ET CIE

CALEX AUTO

ARTH RUBBERS

MARUYASU INDUSTRIES CO., LTD.

제12장 MARKETSANDMARKETS에 의한 제안

아시아태평양이 유체 이송 시스템의 주요 시장으로 부상

경량 재료를 중시하는 기업

전기화 동향

상용차에서 HVAC와 에어 서스펜션 유체 이송 시스템의 높은 수요

결론

제13장 부록

KSM

영문 목차

영문목차

The fluid transfer system market is projected to reach USD 29.95 billion in 2032, from USD 23.93 billion in 2025, with a CAGR of 3.3%.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Volume (Thousand Units) and Value (USD Billion)

Segments

Propulsion & Component, Vehicle Type, System Type, and Region

Regions covered

Asia Pacific, Southeast Asia, Europe, North America, and Rest of the World

The fluid transfer system market is poised for steady growth, supported by increased vehicle production, stricter emission standards, and broader adoption of advanced mobility technologies. The demand for fluid transfer systems is also driven by their critical role in managing fuel, air, oil, coolant, and other fluids essential for performance, efficiency, and safety across ICE and electric vehicles.

The shift toward premium passenger cars is expanding the use of advanced air conditioning, suspension, and emission control lines, while stricter regulations such as BS-VI and Euro 6 are boosting demand for SCR, DPF, and EVAP lines. Similarly, the growing penetration of EVs is driving new opportunities for thermal management components, including battery, motor, and power electronics cooling lines.

"Suspension systems are expected to show a significant growth rate during the forecast period."

The suspension systems segment in the fluid transfer system market is expected to experience significant growth during the forecast period, driven by rising demand for improved vehicle stability, comfort, and handling. Components related to suspension fluid transfer, such as hydraulic suspension lines, air suspension lines, shock absorber hoses, and anti-roll hoses, are vital for maintaining vehicle stability, minimizing body roll, and allowing adjustable ride height and load management. In passenger cars, trends toward premiumization are accelerating the adoption of air suspension and advanced damping systems, while in commercial vehicles, hydraulic and air suspension lines are essential for durability and load control. The shift to electric buses further boosts demand, as these vehicles increasingly utilize air suspension systems to ensure smoother rides and offset battery weight. As manufacturers invest in advanced suspension technologies to meet consumer expectations for comfort, performance, and safety, the suspension segment is becoming one of the most promising growth areas in the fluid transfer system market.

"Passenger cars are expected to hold the largest share during the forecast period."

The passenger cars segment is expected to account for the largest share of the fluid transfer system market during the forecast period, driven by both volume growth and rapid adoption of advanced vehicle technologies. Increasing demand for premium and mid-range vehicles is expanding the use of air suspension systems and dual-zone or rear-seat air conditioning, boosting requirements for specialized air suspension and A/C fluid transfer lines. Stricter emission standards worldwide, such as BS-VI in India and Euro 6 in Europe, are accelerating the adoption of selective catalytic reduction (SCR) and diesel particulate filter (DPF) lines, as well as other exhaust after-treatment components. At the same time, growing penetration of hybrid and electric passenger cars is creating new opportunities for battery, motor, and DC-DC converter coolant hoses, adding to the traditional demand for fuel and lubrication lines. This combined effect of regulatory compliance, rising comfort features, and electrification ensures that the passenger car segment will remain the largest and most dynamic market for fluid transfer systems.

"Europe's fluid transfer system market is expected to witness notable growth during the forecast period."

Europe is expected to experience significant growth in the fluid transfer system market during the forecast period, supported by its well-established automotive manufacturing base, leadership in technology, and strict regulatory frameworks. The region is home to top OEMs such as Volkswagen, BMW, Mercedes-Benz, Renault, Stellantis, Volvo, and Scania, along with Tier-1 suppliers and fluid transfer specialists like TI Fluid Systems, Continental AG, Gates Corporation, and Parker Hannifin, which ensure continuous innovation and large-scale supply capability. Regulatory changes, including the Euro 6d standard and the upcoming Euro 7 regulations, are increasing demand for advanced emission control lines, exhaust gas recirculation pipes, and thermal management hoses to meet tightening CO2 and NOx reduction standards across passenger cars, trucks, and buses. Electrification is rapidly expanding in both passenger vehicles and heavy commercial trucks, creating opportunities for new product categories such as battery coolant hoses, thermal lines for inverters and motors, and specialized EV climate control tubing. Plug-in hybrid vehicles also support dual demands, maintaining requirements for conventional fuel and oil lines while opening up opportunities in EV cooling and heating systems. Europe's strong truck and bus manufacturing sector, led by Daimler Truck, MAN, Iveco, and Volvo, is further increasing demand for durable high-pressure fuel lines, SCR and EGR assemblies, and thermal hoses, as fleets work to meet stricter emission standards and electrification goals.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various organizations operating in this market.

By Company Type: Tier 1 - 32%, Tier 2 - 45%, and Tier 3 - 23%

By Designation: Directors - 36%, Managers - 43%, and Others - 21%

By Region: Asia Pacific - 36%, Southeast Asia - 13%, Europe - 24%, North America - 21%, and Rest of the World - 6%

The fluid transfer system market is led by major companies, including Cooper Standard (US), TI Fluid Systems (UK), Sumitomo Riko Company Limited (Japan), Parker Hannifin Corp (US), and Gates Corporation (US). These firms are expanding their product ranges to reinforce their market position.

Research Coverage:

The report covers the fluid transfer system market by propulsion & component {petrol/gasoline [intake hose, vacuum hose, fuel feed line, feed return line, fuel leak-off assembly, turbocharger oil feed line, turbocharger oil drain line, turbocharger coolant line, turbocharger coolant return line, positive crankcase ventilation (PCV) hose, vacuum modulator hose, dipstick tube, fluid return hose, pressure control solenoid hose, transmission oil cooler lines, hydraulic power steering hose, fuel delivery line, high-pressure fuel injection line/direct injection line, fuel rail, CNG tube, CNG hose, fuel vapor vent line, fuel injector line, fuel filler neck, fuel filler line, thermal line, expansion valve tube, A/C cabin climate control, radiator hose, reservoir, overflow hose, bypass hose, DC-DC converter cooling hose, motor cooling hose, battery coolant hose, A/C drain line, hydraulic suspension line, air suspension line, shock absorber hose, anti-roll hose, brake and clutch hose & line assembly, vacuum booster hose, brake bundle assembly, EGR tube & assembly, SCR tube & assembly, EVAP line, differential pressure hose, tailpipe, sunroof drain hose, windshield washer hose, power door lock hose, oil line], diesel, CNG, battery electric, and plug-in hybrid electric}, system type (engine, transmission, power steering, fuel delivery, thermal management, suspension, brake & clutch, exhaust, body & exterior, and lubrication), vehicle type (passenger cars, light commercial vehicles, trucks, and buses), and region. It also provides an in-depth competitive analysis of key market players, their company profiles, critical observations related to product and business offerings, recent developments, and growth strategies.

Key Benefits of Buying this Report:

The report serves as a valuable resource for market leaders and new entrants by providing insights into the closest approximations of revenue numbers for the fluid transfer system market and its subsegments. It aids stakeholders in comprehending the competitive landscape, allowing them to position their businesses effectively and devise suitable go-to-market strategies. Additionally, the report sheds light on the market pulse, outlining key drivers, restraints, challenges, and opportunities within the industry. It also offers an understanding of the current and future pricing trends related to the fluid transfer system market, equipping stakeholders with essential information for their decision-making processes.

The report provides insight into the following:

Analysis of drivers (rise in demand for SUVs and premium passenger cars, expansion of vehicle manufacturing and innovation in fluid transfer system components, supportive government policies for localized vehicle and component manufacturing), restraints (growing electrification in passenger cars in select countries), opportunities (rapid adoption of PHEVs, sustained demand in trucks amid slower rate of electrification, innovations in thermal management systems for electrified powertrains), and challenges (electrification in public transport, tariff-driven procurement volatility and system-level disruptions)

Product Development/Innovation: Detailed insights into upcoming technologies, R&D activities, and product launches in the fluid transfer system market

Market Development: Comprehensive information about lucrative markets; this report analyzes the fluid transfer system market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the fluid transfer system market

Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players in the fluid transfer system market, such as Cooper Standard (US), TI Fluid Systems (UK), Sumitomo Riko Company Limited (Japan), Parker Hannifin Corp (US), and Gates Corporation (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary participants

2.1.2.2 Primary interviews from demand and supply sides

2.1.2.3 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.3 DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLUID TRANSFER SYSTEM MARKET

4.2 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE

4.3 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE

4.4 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION

4.5 FLUID TRANSFER SYSTEM MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rise in demand for SUVs and premium passenger cars

5.2.1.2 Expansion of vehicle manufacturing and innovations in fluid transfer systems

5.2.1.3 Supportive government policies for localized manufacturing

5.2.2 RESTRAINTS

5.2.2.1 Electrification of passenger cars in select countries

5.2.3 OPPORTUNITIES

5.2.3.1 Rapid adoption of PHEVs

5.2.3.2 Sustained demand in trucks due to slower rate of electrification

5.2.3.3 Advances in thermal management systems for electrified powertrains

5.2.4 CHALLENGES

5.2.4.1 Shift toward electric buses and municipal EV fleets

5.2.4.2 Tariff-driven procurement volatility and system-level disruptions

5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE OF FLUID TRANSFER COMPONENTS OFFERED BY KEY PLAYERS

5.4.2 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE

5.4.3 AVERAGE SELLING PRICE TREND, BY REGION

5.5 ECOSYSTEM ANALYSIS

5.6 VALUE CHAIN ANALYSIS

5.7 CASE STUDY ANALYSIS

5.7.1 VCOLLAB'S SOLUTION IMPROVES SIMULATION EFFICIENCY FOR COOPER STANDARD

5.7.2 FLUID COOLING SYSTEMS' PROCESS COOLING SOLUTION ENHANCES ALUMINUM WELDING PROCESS FOR FORD

5.7.3 LUCAS-MILHAUPT'S FLUX-FREE BRAZING PROCESS ENSURES LEAK-FREE FUEL SENDERS FOR FORD

5.8 PATENT ANALYSIS

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Multi-layer hose and tube technology

5.9.1.2 Advanced materials and composites

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Additive manufacturing

5.9.2.2 Automation and control systems

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 EV thermal management

5.10 TRADE ANALYSIS

5.10.1 IMPORT SCENARIO (HS CODE 4009)

5.10.2 EXPORT SCENARIO (HS CODE 4009)

5.11 TARIFF AND REGULATORY LANDSCAPE

5.11.1 TARIFF DATA

5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.3 REGULATORY ANALYSIS FOR FLUID TRANSFER SYSTEM MARKET

5.11.3.1 US

5.11.3.2 China

5.11.3.3 Japan

5.11.3.4 India

5.11.3.5 South Korea

5.11.3.6 Europe

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2 BUYING CRITERIA

5.14 IMPACT OF AI

5.15 OEM AND TIER-1 SOURCING/ADOPTION STRATEGIES

5.15.1 OEM SOURCING STRATEGIES

5.15.2 TIER-1 ADOPTION AND DIFFERENTIATION STRATEGIES

5.16 DIGITALIZATION AND SMART MANUFACTURING INITIATIVES

5.16.1 MODULAR, AUTOMATED, AND TRACEABLE PRODUCTION SYSTEMS

5.16.2 SMART MANUFACTURING PLATFORMS ENABLING PREDICTIVE MAINTENANCE AND REAL-TIME PROCESS OPTIMIZATION

5.16.3 EMBEDDED SENSOR TECHNOLOGIES AND ADVANCED MATERIALS

5.16.4 SCALABLE DIGITAL MANUFACTURING SUPPORTING ELECTRIFICATION

5.16.5 AI-DRIVEN QUALITY CHECKS, ADDITIVE MANUFACTURING, AND 5G CONNECTIVITY

5.17 SHIFT TOWARD ELECTRIFICATION

5.17.1 DECLINE IN CONVENTIONAL ICE FLUID TRANSFER SYSTEMS

5.17.2 ELEVATED DEMAND FOR EV-DRIVEN FLUID TRANSFER SYSTEMS

5.17.3 RISE IN MODULAR AND INTEGRATED ASSEMBLIES

5.17.4 AFTERMARKET'S SHIFT AWAY FROM ICE FLUID TRANSFER SYSTEMS

5.18 MATERIAL ANALYSIS, BY FLUID TRANSFER COMPONENT

5.19 SUPPLIER ANALYSIS, BY FLUID TRANSFER SYSTEM

6 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION AND COMPONENT

6.1 INTRODUCTION

6.2 PETROL/GASOLINE

6.2.1 RISING ADOPTION OF TURBOCHARGED ENGINES TO DRIVE MARKET

6.3 DIESEL

6.3.1 INCREASING STRINGENCY OF NOX EMISSION REGULATIONS TO DRIVE MARKET

6.4 CNG

6.4.1 GROWING INCLINATION TOWARD CLEANER FUEL ALTERNATIVES TO DRIVE MARKET

6.5 BATTERY ELECTRIC

6.5.1 EMERGING ELECTRIFICATION TRENDS TO DRIVE MARKET

6.6 PLUG-IN HYBRID ELECTRIC

6.6.1 CONSUMER DEMAND FOR FUEL EFFICIENCY AND DYNAMIC PERFORMANCE TO DRIVE MARKET

6.7 PRIMARY INSIGHTS

7 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE

7.1 INTRODUCTION

7.2 PASSENGER CARS

7.2.1 STRICTER EMISSION NORMS AND SURGE IN ELECTRIFICATION TO DRIVE MARKET

7.3 LIGHT COMMERCIAL VEHICLES

7.3.1 HEIGHTENED ADOPTION OF AUTOMATIC TRANSMISSIONS TO DRIVE MARKET

7.4 TRUCKS

7.4.1 RAPID INDUSTRIALIZATION AND INCREASED LOGISTICS ACTIVITIES TO DRIVE MARKET

7.5 BUSES

7.5.1 INTEGRATION OF AIR SUSPENSION IN NEW ELECTRIC BUSES TO DRIVE MARKET

7.6 PRIMARY INSIGHTS

8 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE

8.1 INTRODUCTION

8.2 ENGINE

8.2.1 NEED FOR HEAT RESISTANCE AND PRESSURE TOLERANCE TO DRIVE MARKET

8.3 TRANSMISSION

8.3.1 RISE OF AUTOMATIC TRANSMISSION DESIGNS TO DRIVE MARKET

8.4 POWER STEERING

8.4.1 CONTINUED RELIANCE ON HYDRAULIC STEERING IN COMMERCIAL VEHICLES TO DRIVE MARKET

8.5 FUEL DELIVERY

8.5.1 RIGOROUS EMISSION NORMS AND ELEVATED CNG ADOPTION TO DRIVE MARKET

8.6 THERMAL MANAGEMENT

8.6.1 SHIFT TOWARD HIGHER CAPACITY COOLING SYSTEMS TO DRIVE MARKET

8.7 SUSPENSION

8.7.1 HIGH DEMAND FOR IMPROVED RIDE COMFORT AND DURABILITY TO DRIVE MARKET

8.8 BRAKE & CLUTCH

8.8.1 IMPLEMENTATION OF STRICT VEHICLE SAFETY STANDARDS TO DRIVE MARKET

8.9 EXHAUST

8.9.1 WIDE ADOPTION OF AFTERTREATMENT TECHNOLOGIES IN COMMERCIAL VEHICLES TO DRIVE MARKET

8.10 BODY & EXTERIOR

8.10.1 INTEGRATION OF PREMIUM COMFORT AND SAFETY FEATURES IN MASS-MARKET MODELS TO DRIVE MARKET

8.11 LUBRICATION

8.11.1 EXPANSION OF DOWNSIZED ENGINES TO DRIVE MARKET

8.12 PRIMARY INSIGHTS

9 FLUID TRANSFER SYSTEM MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 MACROECONOMIC OUTLOOK

9.2.2 CHINA

9.2.2.1 Domestic OEM dominance and high NEV growth to drive market

9.2.3 INDIA

9.2.3.1 Emission compliance and local manufacturing to drive market

9.2.4 JAPAN

9.2.4.1 Dual-propulsion vehicle trends to drive market

9.2.5 SOUTH KOREA

9.2.5.1 Rising EV output to drive market

9.3 SOUTHEAST ASIA

9.3.1 MACROECONOMIC OUTLOOK

9.3.2 THAILAND

9.3.2.1 Expansion of domestic automotive manufacturing to drive market

9.3.3 INDONESIA

9.3.3.1 OEM investment in modern gasoline engine platforms to drive market

9.3.4 VIETNAM

9.3.4.1 Surge in vehicle electrification to drive market

9.3.5 PHILIPPINES

9.3.5.1 Urbanization and financing trends to drive market

9.4 NORTH AMERICA

9.4.1 MACROECONOMIC OUTLOOK

9.4.2 US

9.4.2.1 Plans for increasing domestic manufacturing to drive market

9.4.3 CANADA

9.4.3.1 High penetration of light commercial vehicles and trucks to drive market

9.4.4 MEXICO

9.4.4.1 Expansion of advanced powertrain production to drive market

9.5 EUROPE

9.5.1 MICROECONOMIC OUTLOOK

9.5.2 GERMANY

9.5.2.1 Collaborations between OEMs and Tier-1 suppliers to drive market

9.5.3 FRANCE

9.5.3.1 Focus on emission reduction and transition toward electrification to drive market

9.5.4 ITALY

9.5.4.1 High demand for fluid transfer systems in commercial vehicle applications to drive market

9.5.5 SPAIN

9.5.5.1 Diverse vehicle production mix to drive market

9.5.6 UK

9.5.6.1 Fleet electrification momentum to drive market

9.5.7 REST OF EUROPE

9.6 REST OF THE WORLD

9.6.1 MACROECONOMIC OUTLOOK

9.6.2 SOUTH AFRICA

9.6.2.1 Growing automotive manufacturing to drive market

9.6.3 KENYA

9.6.3.1 Increasing vehicle assembly activities to drive market

9.6.4 EGYPT

9.6.4.1 Established automotive manufacturing base to drive market

10 COMPETITIVE LANDSCAPE

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

10.3 MARKET SHARE ANALYSIS, 2024

10.4 REVENUE ANALYSIS, 2020-2024

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 BRAND/PRODUCT COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 EMERGING LEADERS

10.7.3 PERVASIVE PLAYERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 System type footprint

10.7.5.4 Propulsion footprint

10.7.5.5 Vehicle type footprint

10.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

10.8.1 PROGRESSIVE COMPANIES

10.8.2 RESPONSIVE COMPANIES

10.8.3 DYNAMIC COMPANIES

10.8.4 STARTING BLOCKS

10.8.5 COMPETITIVE BENCHMARKING

10.8.5.1 List of start-ups/SMEs

10.8.5.2 Competitive benchmarking of start-ups/SMEs

10.9 COMPETITIVE SCENARIO

10.9.1 PRODUCT LAUNCHES

10.9.2 DEALS

10.9.3 EXPANSIONS

10.9.4 OTHER DEVELOPMENTS

11 COMPANY PROFILES

11.1 KEY PLAYERS

11.1.1 COOPER STANDARD

11.1.1.1 Business overview

11.1.1.2 Products/Solutions offered

11.1.1.3 Recent developments

11.1.1.3.1 Product launches/developments

11.1.1.3.2 Deals

11.1.1.3.3 Other developments

11.1.1.4 MnM view

11.1.1.4.1 Key strengths

11.1.1.4.2 Strategic choices

11.1.1.4.3 Weaknesses and competitive threats

11.1.2 TI FLUID SYSTEMS

11.1.2.1 Business overview

11.1.2.2 Products/Solutions offered

11.1.2.3 Recent developments

11.1.2.3.1 Product launches/developments

11.1.2.3.2 Deals

11.1.2.3.3 Expansions

11.1.2.4 MnM view

11.1.2.4.1 Key strengths

11.1.2.4.2 Strategic choices

11.1.2.4.3 Weaknesses and competitive threats

11.1.3 SUMITOMO RIKO COMPANY LIMITED

11.1.3.1 Business overview

11.1.3.2 Products/Solutions offered

11.1.3.3 Recent developments

11.1.3.3.1 Expansions

11.1.3.3.2 Other developments

11.1.3.4 MnM view

11.1.3.4.1 Key strengths

11.1.3.4.2 Strategic choices

11.1.3.4.3 Weaknesses and competitive threats

11.1.4 PARKER HANNIFIN CORP

11.1.4.1 Business overview

11.1.4.2 Products/Solutions offered

11.1.4.3 Recent developments

11.1.4.3.1 Product launches/developments

11.1.4.3.2 Deals

11.1.4.3.3 Expansions

11.1.4.3.4 Other developments

11.1.4.4 MnM view

11.1.4.4.1 Key strengths

11.1.4.4.2 Strategic choices

11.1.4.4.3 Weaknesses and competitive threats

11.1.5 GATES CORPORATION

11.1.5.1 Business overview

11.1.5.2 Products/Solutions offered

11.1.5.3 Recent developments

11.1.5.3.1 Product launches/developments

11.1.5.4 MnM view

11.1.5.4.1 Key strengths

11.1.5.4.2 Strategic choices

11.1.5.4.3 Weaknesses and competitive threats

11.1.6 SANOH INDUSTRIAL CO., LTD.

11.1.6.1 Business overview

11.1.6.2 Products/Solutions offered

11.1.6.3 Recent developments

11.1.6.3.1 Other developments

11.1.7 CONTINENTAL AG

11.1.7.1 Business overview

11.1.7.2 Products/Solutions offered

11.1.7.3 Recent development

11.1.7.3.1 Expansions

11.1.8 DENSO CORPORATION

11.1.8.1 Business overview

11.1.8.2 Products/Solutions offered

11.1.9 HUTCHINSON

11.1.9.1 Business overview

11.1.9.2 Products/Solutions offered

11.1.9.3 Recent developments

11.1.9.3.1 Product launches/developments

11.1.9.3.2 Expansions

11.1.10 NICHIRIN

11.1.10.1 Business overview

11.1.10.2 Products/Solutions offered

11.1.10.3 Recent developments

11.1.10.3.1 Deals

11.1.11 USUI CO. LTD.

11.1.11.1 Business overview

11.1.11.2 Products/Solutions offered

11.1.11.3 Recent developments

11.1.11.3.1 Other developments

11.1.12 KONGSBERG AUTOMOTIVE

11.1.12.1 Business overview

11.1.12.2 Products/Solutions offered

11.1.12.3 Recent developments

11.1.12.3.1 Other developments

11.1.13 AKWEL

11.1.13.1 Business overview

11.1.13.2 Products/Solutions offered

11.1.13.3 Recent developments

11.1.13.3.1 Expansions

11.1.13.3.2 Other developments

11.1.14 IMPERIAL AUTO

11.1.14.1 Business overview

11.1.14.2 Products/Solutions offered

11.1.14.3 Recent developments

11.1.14.3.1 Deals

11.1.14.3.2 Expansions

11.1.15 ROBERT BOSCH GMBH

11.1.15.1 Business overview

11.1.15.2 Products/Solutions offered

11.1.15.3 Recent developments

11.1.15.3.1 Product launches/developments

11.2 OTHER PLAYERS

11.2.1 LANDER TUBULAR PRODUCTS

11.2.2 TRISTONE

11.2.3 FLEXITECH

11.2.4 DELFINGEN

11.2.5 TALBROS

11.2.6 MANULI RYCO GROUP

11.2.7 GRACO INC.

11.2.8 NEWAGE INDUSTRIES

11.2.9 ARAYMOND ET CIE

11.2.10 CALEX AUTO

11.2.11 ARTH RUBBERS

11.2.12 MARUYASU INDUSTRIES CO., LTD.

12 RECOMMENDATIONS BY MARKETSANDMARKETS

12.1 ASIA PACIFIC TO BE LEADING MARKET FOR FLUID TRANSFER SYSTEMS

12.2 COMPANIES' EMPHASIS ON LIGHTWEIGHT MATERIALS

12.3 TREND OF ELECTRIFICATION

12.4 HIGH DEMAND FOR HVAC AND AIR SUSPENSION FLUID TRANSFER SYSTEMS IN COMMERCIAL VEHICLES