Kaolin Market by Type, Process, End-use Industry, and Region - Forecast to 2030

상품코드:1802918

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 301 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

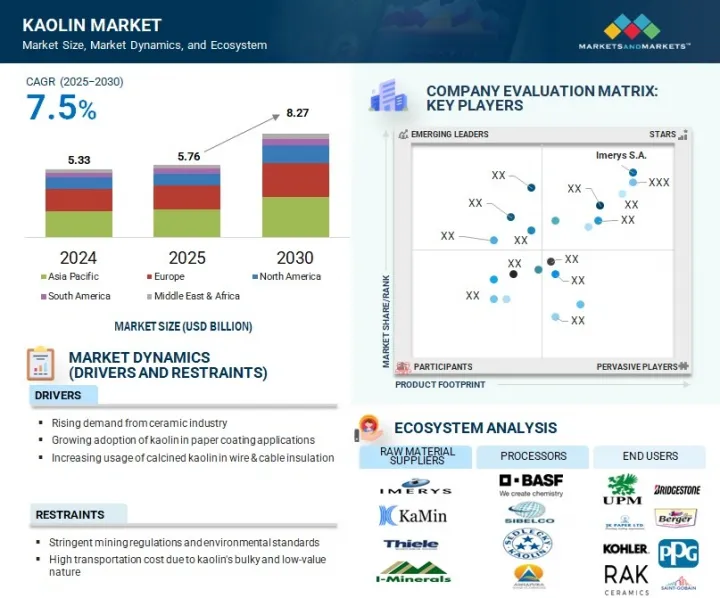

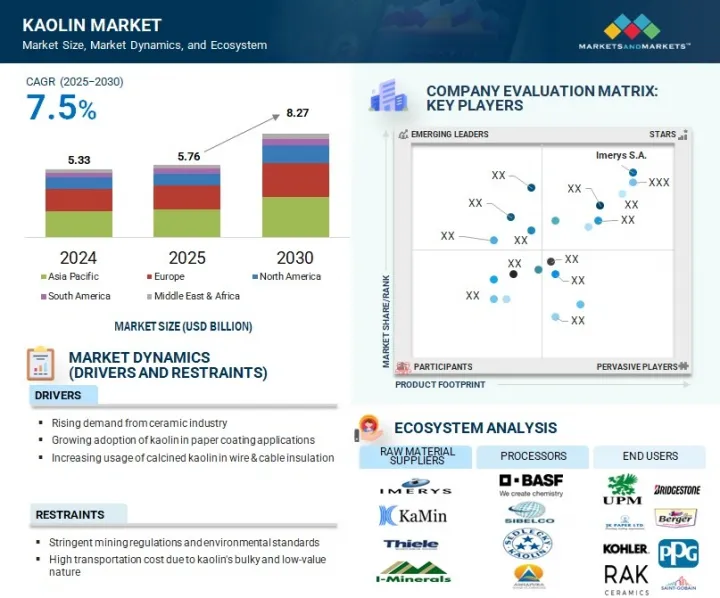

카올린 시장 규모는 2025년 57억 6,000만 달러에서 2030년에는 82억 7,000만 달러에 달하며, CAGR은 7.5%로 예측됩니다.

카올린은 제지, 세라믹, 위생도기, 유리섬유, 페인트 및 코팅, 고무 제조, 플라스틱 등 다양한 산업에서 널리 사용되고 있습니다.

조사 범위

조사 대상연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

대상 단위

킬로톤, 금액(100만 달러/10억 달러)

부문

유형별, 프로세스별, 최종 용도 산업별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 남미, 중동 및 아프리카

미국, 브라질, 영국 등 풍부한 고품질 카올린을 매장하고 있는 국가들은 세계 시장에 고급 카올린을 공급하는 데 중요한 역할을 하고 있습니다. 이러한 요인들이 종합적으로 카올린 시장의 성장을 주도하고 있습니다. 합성 카올린은 높은 비용과 작은 기반에도 불구하고 하이테크 용도에서 수요가 증가함에 따라 천연 카올린보다 빠르게 성장하고 있습니다.

2024년 제지 산업은 카올린 시장에서 수량과 금액 모두에서 가장 큰 최종 용도 부문이 될 것입니다. 카올린은 계속해서 시장을 선도하고 있으며, 앞으로도 안정적인 성장이 예상됩니다. 종이는 인쇄 매체 및 포장에 널리 사용되며, 특히 신흥 국가에서는 E-Commerce의 급격한 성장으로 종이 기반 포장 솔루션에 대한 수요가 증가하고 있습니다. 인도나 중국과 같은 국가들은 신문, 서적, 잡지 등 인쇄 매체 소비량이 많고, E-Commerce 활동도 활발하게 이루어지고 있으며, 큰 성장 기회를 가져다주고 있습니다. 지속가능하고 생분해 가능한 포장 옵션에 대한 전 세계적인 관심은 제지 산업에서 카올린에 대한 수요를 더욱 증가시키고 있습니다.

예측 기간 중, 라미네이트 제거 부문이 가장 높은 성장률을 보일 것으로 예측됩니다. 이러한 성장의 원동력은 더 우수한 밝기와 부드러움을 제공하는 고품질의 저마모성 박리 카올린의 가용성이 증가하고 있기 때문입니다. 박리 공정에서는 쌓인 층에서 개별 카올리나이트 소판을 파단하지 않고 분리하기 위해 정확한 기계적 힘이 필요합니다. 그 결과, 박리 카올린은 주로 제지 산업에서 인쇄성 및 표면 특성을 개선하기 위해 주로 사용됩니다. 또한 고급 코팅지에 대한 수요 증가와 제지 기술의 발전이 이 부문의 성장을 가속하고 있습니다.

아시아태평양은 중국, 인도, 일본, 한국, 호주 등의 국가를 포괄하는 광범위한 분석을 통해 카올린의 주요 시장으로 남아있습니다. 급속한 도시화, 양호한 인구 통계학적 변화, 신흥 국가의 경제 상황의 개선은 이 지역을 카올린 소비에 매우 매력적인 지역으로 만들고 있습니다. Ashapura Group(인도), EICL Limited(인도), Minotaur Exploration Limited(호주) 등 주요 기업은 안정적인 공급을 보장하기 위해 제조 단위, 유통 채널, 영업소를 통해 현지에 강력한 발자취를 남기고 있습니다. 또한 인프라, 건설 및 포장 산업에 대한 투자 증가는 아시아태평양의 카올린 시장의 지속적인 성장에 기여하고 있습니다.

세계의 카올린 시장에 대해 조사했으며, 유형별, 프로세스별, 최종 용도 산업별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

서론

시장 역학

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

공급망 분석

에코시스템/시장 맵

가격 분석

무역 분석

기술 분석

거시경제 전망

특허 분석

규제 상황

사례 연구 분석

고객 비즈니스에 영향을 미치는 동향과 혼란

투자와 자금조달 시나리오

AI/생성형 AI가 카올린 시장에 미치는 영향

2025년 미국 관세가 카올린 시장에 미치는 영향

제6장 카올린 시장(유형별)

서론

천연

합성

제7장 카올린 시장(프로세스별)

서론

물 세정

에어플로트

소성

박리

표면 개질

제8장 카올린 시장(최종 용도 산업별)

서론

제지

도자기·위생도기

유리섬유

페인트와 코팅

고무

플라스틱

기타 최종 용도 산업

접착제

실란트

퍼스널케어·헬스케어

농업

기타 최종 용도 산업에서의 카올린 시장(지역별)

제9장 카올린 시장(지역별)

서론

카올린 시장(지역별)

북미

아시아태평양

유럽

중동 및 아프리카

남미

제10장 경쟁 구도

개요

주요 참여 기업의 전략/강점, 2020년 1월-2025년 7월

매출 분석

시장 점유율 분석

브랜드/제품 비교 분석

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

카올린 벤더의 평가와 재무 지표

경쟁 시나리오

제11장 기업 개요

주요 참여 기업

IMERYS S.A.

20 MICRONS

KAMIN LLC.

ASHAPURA GROUP

SIBELCO

THIELE KAOLIN COMPANY

LB MINERALS, LTD.

EICL LIMITED

QUARZWERKE GMBH

SEDLECKY KAOLIN, A.S.

기타 기업

SHREE RAM KAOLIN

KERAMOST, A.S.

UMA GROUP OF COMPANIES

JIANGXI SINCERE MINERAL INDUSTRY CO., LTD.

ACTIVE MINERALS INTERNATIONAL, LLC

BURGESS PIGMENT COMPANY

KAOLIN(MALAYSIA) SDN BHD.

KERALA CERAMICS LTD.

MOTA CERAMIC SOLUTIONS

MANEK GROUP

ZILLION SAWA MINERALS PRIVATE LIMITED

HITECH MINERALS AND CHEMICALS GROUP

AMGEEN MINERALS

GUJARAT EARTH MINERALS PVT. LTD.

HD MICRONS LIMITED.

제12장 부록

KSA

영문 목차

영문목차

The kaolin market is projected to reach USD 8.27 billion by 2030, from USD 5.76 billion in 2025, with a CAGR of 7.5%. Kaolin is widely used in various industries, including paper manufacturing, ceramics, sanitaryware, fiberglass, paints and coatings, rubber production, and plastics.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Volume (Kiloton); Value (USD Million/Billion)

Segments

Type, Process, End-use Industry, and Region

Regions covered

North America, Asia Pacific, Europe, South America, and Middle East & Africa

Countries with abundant and high-quality kaolin reserves, such as the US, Brazil, and the UK, play a significant role in supplying premium-grade kaolin to global markets. These factors collectively drive the growth of the kaolin market. Synthetic kaolin is growing faster than natural kaolin due to increasing demand in high-tech applications, despite its higher cost and smaller base.

''Kaolin prompts paper revolution from print to sustainable packaging.''

In 2024, the paper industry became the largest end-use segment in the kaolin market by both volume and value. It continues to lead the market and is expected to experience steady growth in the coming years. Paper is widely used in print media and packaging, with the rapid growth of e-commerce, especially in emerging economies, driving strong demand for paper-based packaging solutions. Countries like India and China offer significant growth opportunities due to their high consumption of print media, including newspapers, books, and magazines, along with increasing e-commerce activity. The global focus on sustainable and biodegradable packaging options is further increasing the demand for kaolin in the paper industry.

''Delaminated emerges as the fastest-growing process.''

The delaminated segment is expected to see the highest growth rate during the forecast period. This increase is driven by the growing availability of high-quality, low-abrasive delaminated kaolin, which provides better brightness and smoothness. The delamination process involves separating individual kaolinite platelets from stacked layers without breaking them, requiring precise mechanical force. As a result, delaminated kaolin is mainly used in the paper industry to improve printability and surface properties. Additionally, rising demand for premium-grade coated paper and advancements in paper manufacturing technologies are boosting the segment growth.

"Asia Pacific remains at the forefront of kaolin demand and growth."

Asia Pacific remains the leading market for kaolin, with extensive analysis covering countries such as China, India, Japan, South Korea, and Australia, among others. Rapid urbanization, favorable demographic shifts, and improved economic conditions in emerging economies make this region highly attractive for kaolin consumption. Key players like Ashapura Group (India), EICL Limited (India), and Minotaur Exploration Limited (Australia) have established strong local footprints through manufacturing units, distribution channels, and sales offices to ensure consistent supply. Furthermore, rising investments in infrastructure, construction, and packaging industries are contributing to the sustained growth of the kaolin market across Asia Pacific.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type - Tier 1 - 40%, Tier 2 - 33%, and Tier 3 - 27%

By Designation - C-level - 50%, D-level - 30%, and Others - 20%

By Region - North America - 15%, Europe - 50%, Asia Pacific - 20%, Middle East & Africa - 5%, and South America - 10%

Prominent companies in the kaolin market include Imerys S.A. (France), 20 Microns (India), KaMin LLC (US), Ashapura Group (India), SCR-Sibelco (Belgium), Thiele Kaolin Company (US), LB MINERALS, LTD. (Hungary), EICL Limited (India), Quarzwerke GmbH (Germany), and Sedlecky Kaolin a.s. (Czech Republic).

Research Coverage

This research report categorizes the kaolin market by type (synthetic, natural), process (water-washed, airfloat, calcined, delaminated, and surface-modified & unprocessed), end-use industry (paper, ceramics & sanitaryware, fiberglass, paints & coatings, rubber, plastic, others), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors affecting the growth of the kaolin market, such as drivers, restraints, challenges, and opportunities. A comprehensive analysis of key industry players has been performed to provide insights into their business overviews, solutions, services, key strategies, contracts, partnerships, and agreements. The report also covers new product and service launches, mergers and acquisitions, and recent developments in the kaolin market. Additionally, it features a competitive analysis of emerging startups within the kaolin market ecosystem.

Reasons to purchase this report:

The report will assist market leaders and new entrants with information on the closest estimates of revenue figures for the overall kaolin market and its subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report helps stakeholders grasp the market dynamics and offers key information on market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Increasing demand from key end-use industries, Rising adoption of kaolin in sustainable and biodegradable packaging), restraints (Environmental concerns and stringent mining regulations), opportunities (Technological advancements in processing techniques, Growing demand for high-performance kaolin in specialized applications), and challenges (Fluctuating raw material prices, Availability of substitutes like calcium carbonate) influencing the growth of the kaolin market

Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product & service launches in the kaolin market

Market Development: Comprehensive information about lucrative markets; the report analyzes the kaolin market across various regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the kaolin market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Imerys S.A. (France), 20 Microns (India), KaMin LLC (US), Ashapura Group (India), SCR-Sibelco (Belgium), Thiele Kaolin Company (US), LB MINERALS, LTD. (Hungary), EICL Limited (India), Quarzwerke GmbH (Germany), and Sedlecky Kaolin a.s. (Czech Republic), among others

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNITS CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key primary interview participants

2.1.2.3 Breakdown of primary interviews

2.1.2.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 TOP-DOWN APPROACH

2.2.2 BOTTOM-UP APPROACH

2.3 BASE NUMBER CALCULATION

2.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

2.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

2.4 MARKET FORECAST APPROACH

2.4.1 SUPPLY SIDE

2.4.2 DEMAND SIDE

2.5 DATA TRIANGULATION

2.6 FACTOR ANALYSIS

2.7 RESEARCH ASSUMPTIONS

2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN KAOLIN MARKET

4.2 KAOLIN MARKET, BY TYPE

4.3 KAOLIN MARKET, BY PROCESS

4.4 KAOLIN MARKET, BY END-USE INDUSTRY

4.5 KAOLIN MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Robust demand from ceramics and refractory industries

5.2.1.2 Growth in metakaolin demand for green cement applications

5.2.2 RESTRAINTS

5.2.2.1 High energy intensity and carbon emissions from calcination

5.2.2.2 Declining availability of high-grade reserves

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing use of ultrafine and engineered kaolin in advanced composites

5.2.3.2 Technological advancements in sustainable mining and process water recovery

5.2.4 CHALLENGES

5.2.4.1 Intensifying competition from alternative minerals

5.2.4.2 Logistical constraints and transportation inefficiencies

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 BARGAINING POWER OF BUYERS

5.3.2 BARGAINING POWER OF SUPPLIERS

5.3.3 THREAT OF NEW ENTRANTS

5.3.4 THREAT OF SUBSTITUTES

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 SUPPLY CHAIN ANALYSIS

5.5.1 RAW MATERIAL

5.5.2 PROCESSING/MODIFICATION

5.5.3 END-USE APPLICATIONS

5.6 ECOSYSTEM/MARKET MAP

5.7 PRICING ANALYSIS

5.7.1 AVERAGE SELLING PRICE, BY KEY PLAYERS

5.7.2 AVERAGE SELLING PRICE TREND

5.8 TRADE ANALYSIS

5.8.1 EXPORT SCENARIO (HS CODE 2507)

5.8.2 IMPORT SCENARIO (HS CODE 2507)

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.3 ADJACENT TECHNOLOGIES

5.10 MACROECONOMIC OUTLOOK

5.10.1 INTRODUCTION

5.10.2 GDP TRENDS AND FORECAST

5.10.3 TRENDS IN GLOBAL KAOLIN INDUSTRY

5.11 PATENT ANALYSIS

5.11.1 INTRODUCTION

5.11.2 METHODOLOGY

5.11.3 DOCUMENT TYPE

5.11.4 INSIGHTS

5.11.5 LEGAL STATUS OF PATENTS

5.11.6 JURISDICTION ANALYSIS

5.11.7 ANALYSIS OF TOP APPLICANTS

5.11.8 PATENTS BY CHINA PETROLEUM & CHEMICAL CORPORATION

5.11.9 PATENTS BY BASF CORPORATION

5.11.10 PATENTS BY JINGDEZHEN CERAMIC INSTITUTE

5.11.11 TOP PATENT OWNERS (US) IN LAST 10 YEARS

5.12 REGULATORY LANDSCAPE

5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13 CASE STUDY ANALYSIS

5.13.1 CASE STUDY 1: IMERYS INVESTED IN SUSTAINABLE KAOLIN PROCESSING TECHNOLOGIES

5.13.2 CASE STUDY 2: THIELE KAOLIN EXPANDED OPERATIONS THROUGH STRATEGIC ACQUISITION

5.13.3 CASE STUDY 3: SIBELCO DEVELOPED ULTRA-FINE KAOLIN FOR PHARMACEUTICALS AND COSMETICS INDUSTRIES

5.14 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.15 INVESTMENT AND FUNDING SCENARIO

5.16 IMPACT OF AI/GEN AI ON KAOLIN MARKET

5.16.1 TOP USE CASES AND MARKET POTENTIAL

5.16.2 CASE STUDIES OF AI IMPLEMENTATION IN KAOLIN MARKET

5.17 IMPACT OF 2025 US TARIFFS ON KAOLIN MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE INDUSTRIES

6 KAOLIN MARKET, BY TYPE

6.1 INTRODUCTION

6.2 NATURAL

6.2.1 WIDELY USED FOR FINE PARTICLE SIZE, HIGH BRIGHTNESS, AND CHEMICAL INERTNESS

6.2.2 NATURAL KAOLIN MARKET, BY REGION

6.3 SYNTHETIC

6.3.1 INCREASING DEMAND IN HIGH-PRECISION APPLICATIONS

6.3.2 SYNTHETIC KAOLIN MARKET, BY REGION

7 KAOLIN MARKET, BY PROCESS

7.1 INTRODUCTION

7.2 WATER-WASHED

7.2.1 WIDELY USED IN PRODUCTION OF HYDROUS KAOLIN

7.2.2 WATER-WASHED KAOLIN MARKET, BY REGION

7.3 AIRFLOAT

7.3.1 REMOVES MAJOR CONTAMINANTS FOUND IN CLAY

7.3.2 AIRFLOAT KAOLIN MARKET, BY REGION

7.4 CALCINED

7.4.1 REMOVES STRUCTURAL HYDROXYLS BY ENHANCING HARDNESS, BRIGHTNESS, AND POROSITY OF KAOLIN

7.4.2 CALCINED KAOLIN MARKET, BY REGION

7.5 DELAMINATED

7.5.1 INCREASED USE IN PAINTS & COATINGS INDUSTRY

7.5.2 DELAMINATED KAOLIN MARKET, BY REGION

7.6 SURFACE-MODIFIED

7.6.1 INCREASES CHEMICAL BOND STRENGTH OF KAOLIN

7.6.2 SURFACE-MODIFIED KAOLIN MARKET, BY REGION

8 KAOLIN MARKET, BY END-USE INDUSTRY

8.1 INTRODUCTION

8.2 PAPER

8.2.1 HIGH DEMAND FOR PAPER PACKAGING TO DRIVE GROWTH

8.2.2 STANDARD COATED FINE PAPER

8.2.3 LOW-COAT WEIGHT PAPER

8.2.4 ART PAPER

8.2.5 COATED FINE PAPER

8.2.6 COATED GROUNDWOOD PAPER

8.2.7 OTHER COATED PAPERS

8.2.8 KAOLIN MARKET IN PAPER INDUSTRY, BY REGION

8.3 CERAMICS & SANITARYWARE

8.3.1 INCREASE IN DEMAND FOR CERAMIC PRODUCTS IN CONSTRUCTION SECTOR TO DRIVE MARKET

8.3.2 WHITEWARE

8.3.3 PORCELAIN

8.3.4 REFRACTORIES

8.3.5 KAOLIN MARKET IN CERAMICS & SANITARYWARE INDUSTRY, BY REGION

8.4 FIBERGLASS

8.4.1 HIGH DEMAND FOR FIBERGLASS ACROSS VARIOUS INDUSTRIES TO DRIVE MARKET

8.4.2 KAOLIN MARKET IN FIBERGLASS INDUSTRY, BY REGION

8.5 PAINTS & COATINGS

8.5.1 RISE IN DEMAND FOR SPECIALTY PAINTS & COATINGS IN CONSTRUCTION AND INDUSTRIAL SECTORS TO DRIVE MARKET

8.5.2 AUTOMOTIVE

8.5.3 INDUSTRIAL

8.5.4 INKS

8.5.5 ARCHITECTURAL

8.5.6 SPECIALTY COATINGS

8.5.7 KAOLIN MARKET IN PAINTS & COATINGS INDUSTRY, BY REGION

8.6 RUBBER

8.6.1 INCREASE IN DEMAND FOR RUBBER IN FOOTWEAR AND TIRES TO DRIVE MARKET

8.6.2 TIRES

8.6.3 FOOTWEAR

8.6.4 CONVEYOR BELTS

8.6.5 KAOLIN MARKET IN RUBBER INDUSTRY, BY REGION

8.7 PLASTICS

8.7.1 HIGH DEMAND FOR PVC CABLES TO DRIVE MARKET

8.7.2 FILMS & SHEETS

8.7.3 WIRES & CABLES

8.7.4 KAOLIN MARKET IN PLASTICS INDUSTRY, BY REGION

8.8 OTHER END-USE INDUSTRIES

8.8.1 ADHESIVES

8.8.2 SEALANTS

8.8.3 PERSONAL CARE & HEALTHCARE

8.8.4 AGRICULTURE

8.8.5 KAOLIN MARKET IN OTHER END-USE INDUSTRIES, BY REGION

9 KAOLIN MARKET, BY REGION

9.1 INTRODUCTION

9.1.1 KAOLIN MARKET, BY REGION

9.2 NORTH AMERICA

9.2.1 NORTH AMERICA: KAOLIN MARKET, BY PROCESS

9.2.2 NORTH AMERICA: KAOLIN MARKET, BY END-USE INDUSTRY

9.2.3 NORTH AMERICA: KAOLIN MARKET, BY COUNTRY

9.2.3.1 US

9.2.3.1.1 Increasing demand from paper, ceramics, paints & coatings, and fiberglass industries to drive market

9.2.3.1.2 US: Kaolin market, by process

9.2.3.1.3 US: Kaolin market, by end-use industry

9.2.3.2 Canada

9.2.3.2.1 Growing construction sector to drive market

9.2.3.2.2 Canada: Kaolin market, by process

9.2.3.2.3 Canada: Kaolin market, by end-use industry

9.2.3.3 Mexico

9.2.3.3.1 Increasing production of plastic products to drive market

9.2.3.3.2 Mexico: Kaolin market, by process

9.2.3.3.3 Mexico: Kaolin market, by end-use industry

9.3 ASIA PACIFIC

9.3.1 ASIA PACIFIC: KAOLIN MARKET, BY PROCESS

9.3.2 ASIA PACIFIC: KAOLIN MARKET, BY END-USE INDUSTRY

9.3.3 ASIA PACIFIC: KAOLIN MARKET, BY COUNTRY

9.3.3.1 China

9.3.3.1.1 Rise in consumption of packaged food items to drive market

9.3.3.1.2 China: Kaolin market, by process

9.3.3.1.3 China: Kaolin market, by end-use industry

9.3.3.2 Japan

9.3.3.2.1 Increased demand for coated and uncoated papers in packaging applications to drive market

9.3.3.2.2 Japan: Kaolin market, by process

9.3.3.2.3 Japan: Kaolin market, by end-use industry

9.3.3.3 India

9.3.3.3.1 Presence of strong paper industry to drive market

9.3.3.3.2 India: Kaolin market, by process

9.3.3.3.3 India: Kaolin market, by end-use industry

9.3.3.4 South Korea

9.3.3.4.1 Growth in residential construction to drive market

9.3.3.4.2 South Korea: Kaolin market, by process

9.3.3.4.3 South Korea: Kaolin market, by end-use industry

9.3.3.5 Australia

9.3.3.5.1 Paper, ceramics, and paints & coatings industries to drive market

9.3.3.5.2 Australia: Kaolin market, by process

9.3.3.5.3 Australia: Kaolin market, by end-use industry

9.3.3.6 Rest of Asia Pacific

9.3.3.6.1 Rest of Asia Pacific: Kaolin market, by process

9.3.3.6.2 Rest of Asia Pacific: Kaolin market, by end-use industry

9.4 EUROPE

9.4.1 EUROPE: KAOLIN MARKET, BY PROCESS

9.4.2 EUROPE: KAOLIN MARKET, BY END-USE INDUSTRY

9.4.3 EUROPE: KAOLIN MARKET, BY COUNTRY

9.4.3.1 Germany

9.4.3.1.1 Increased use of high-quality paper in packaging applications to drive market

9.4.3.1.2 Germany: Kaolin market, by process

9.4.3.1.3 Germany: Kaolin market, by end-use industry

9.4.3.2 UK

9.4.3.2.1 Growth of construction sector to drive market

9.4.3.2.2 UK: Kaolin market, by process

9.4.3.2.3 UK: Kaolin market, by end-use industry

9.4.3.3 France

9.4.3.3.1 Increasing demand for coated papers from packaging industry to drive market

9.4.3.3.2 France: Kaolin market, by process

9.4.3.3.3 France: Kaolin market, by end-use industry

9.4.3.4 Italy

9.4.3.4.1 Robust growth in food & beverage sector to drive market

9.4.3.4.2 Italy: Kaolin market, by process

9.4.3.4.3 Italy: Kaolin market, by end-use industry

9.4.3.5 Spain

9.4.3.5.1 Growing infrastructural activities to drive market

9.4.3.5.2 Spain: Kaolin market, by process

9.4.3.5.3 Spain: Kaolin market, by end-use industry

9.4.3.6 Russia

9.4.3.6.1 Increased demand for kaolin from various end-use industries to drive market

9.4.3.6.2 Russia: Kaolin market, by process

9.4.3.6.3 Russia: Kaolin market, by end-use industry

9.4.3.7 Rest of Europe

9.4.3.7.1 Rest of Europe: Kaolin market, by process

9.4.3.7.2 Russia: Kaolin market, by end-use industry

9.5 MIDDLE EAST & AFRICA

9.5.1 MIDDLE EAST & AFRICA: KAOLIN MARKET, BY PROCESS

9.5.2 MIDDLE EAST & AFRICA: KAOLIN MARKET, BY END-USE INDUSTRY

9.5.3 MIDDLE EAST & AFRICA: KAOLIN MARKET, BY COUNTRY

9.5.3.1 GCC Countries

9.5.3.1.1 Saudi Arabia

9.5.3.1.1.1 Increase in construction activities to drive market

9.5.3.1.1.2 Saudi Arabia: Kaolin market, by process

9.5.3.1.1.3 Saudi Arabia: Kaolin market, by end-use industry

9.5.3.1.2 Rest of GCC Countries

9.5.3.1.2.1 Rest of GCC Countries: Kaolin market, by process

9.5.3.1.2.2 Rest of GCC Countries: Kaolin market, by end-use industry

9.5.3.2 South Africa

9.5.3.2.1 Increase in consumption of plastics to drive market

9.5.3.2.2 South Africa: Kaolin market, by process

9.5.3.2.3 South Africa: Kaolin market, by end-use industry

9.5.3.3 Iran

9.5.3.3.1 Increase in demand for residential buildings to drive market

9.5.3.3.2 Iran: Kaolin market, by process

9.5.3.3.3 Iran: Kaolin market, by end-use industry

9.5.3.4 Rest of Middle East & Africa

9.5.3.4.1 Rest of the Middle East & Africa: Kaolin market, by process

9.5.3.4.2 Rest of the Middle East & Africa: Kaolin market, by end-use industry

9.6 SOUTH AMERICA

9.6.1 SOUTH AMERICA: KAOLIN MARKET, BY PROCESS

9.6.2 SOUTH AMERICA: KAOLIN MARKET, BY END-USE INDUSTRY

9.6.3 SOUTH AMERICA: KAOLIN MARKET, BY COUNTRY

9.6.3.1 Brazil

9.6.3.1.1 Packaging and paper industries to fuel kaolin market expansion

9.6.3.1.2 Brazil: Kaolin market, by process

9.6.3.1.3 Brazil: Kaolin market, by end-use industry

9.6.3.2 Argentina

9.6.3.2.1 Increasing demand for food packaging applications to drive market

9.6.3.2.2 Argentina: Kaolin market, by process

9.6.3.2.3 Argentina: Kaolin market, by end-use industry

9.6.3.3 Rest of South America

9.6.3.3.1 Rest of South America: Kaolin market, by process

9.6.3.3.2 Rest of South America: Kaolin market, by end-use industry

10 COMPETITIVE LANDSCAPE

10.1 OVERVIEW

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2020-JULY 2025

10.3 REVENUE ANALYSIS

10.4 MARKET SHARE ANALYSIS

10.4.1 MARKET RANKING ANALYSIS

10.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

10.5.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

10.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.6.1 STARS

10.6.2 EMERGING LEADERS

10.6.3 PERVASIVE PLAYERS

10.6.4 PARTICIPANTS

10.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.6.5.1 Company footprint

10.6.5.2 Region footprint

10.6.5.3 Type footprint

10.6.5.4 Process footprint

10.6.5.5 End-use industry footprint

10.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

10.7.1 PROGRESSIVE COMPANIES

10.7.2 RESPONSIVE COMPANIES

10.7.3 DYNAMIC COMPANIES

10.7.4 STARTING BLOCKS

10.7.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

10.8 VALUATION AND FINANCIAL METRICS OF KAOLIN VENDORS