섬유 재활용 시장 : 소재별, 섬유 폐기물별, 공정별, 유통 채널별, 최종 이용 산업별, 지역별 - 예측(-2030년)

Textile Recycling Market by Material (Cotton, Polyester & Polyester Fibers, Wool, Nylon & Nylon Fibers), Textile Waste, Process, Distribution Channel, End-Use (Apparel, Home Furnishing, Industrial & Institutional), and Region - Global Forecast to 2030

상품코드:1798384

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 232 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

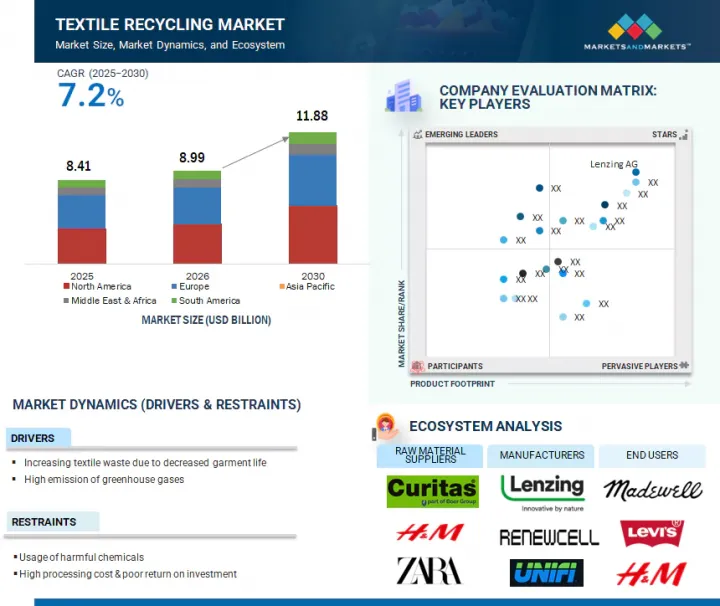

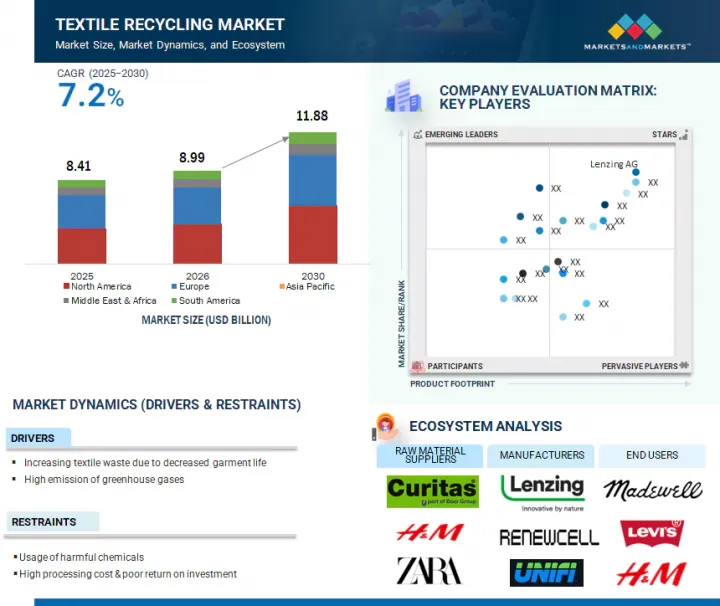

섬유 재활용 시장 규모는 2025년에 84억 1,000만 달러로 추정되며, 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 7.2%로 성장하여 2030년에는 118억 8,000만 달러에 이를 것으로 예측됩니다.

조사 범위

조사 대상 연도

2022-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러), 킬로톤

부문별

소재별, 섬유 폐기물별, 공정별, 유통 채널별, 최종 이용 산업별, 지역별

대상 지역

유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미

면은 전 세계적으로 사용량이 많고, 생분해성이 있으며, 기계적, 화학적 방법으로 재사용할 수 있기 때문에 섬유 재활용에서 두 번째 시장 점유율을 차지하고 있습니다. 의류 및 섬유제품에 많이 사용되는 천연섬유인 면은 소비자 사용 전 및 사용 후 폐기물을 안정적으로 발생시켜 재활용업체에 확장 가능한 투입자원을 제공합니다. 기계적으로 재활용된 면은 단열재, 걸레, 실에 사용되며, 화학적으로 재활용된 면은 리요셀이나 비스코스와 같은 고부가가치 섬유의 선택이 될 수 있습니다. 면화 재활용은 물 사용과 농약에 대한 의존도를 줄이고, 지속가능한 브랜드와 순환 경제에 대한 노력을 어필할 수 있습니다. 내구성과 혼방의 필요성 때문에 폴리에스테르보다 열등하지만, 면의 재생 가능성과 환경 친화적 인 매력은 섬유 재활용에서 면의 중요성을 유지하고 있습니다.

사전소비자 섬유 폐기물은 제조 공정에서 발생하는 폐기물이 일관되게 예측 가능하기 때문에 섬유 폐기물 중 두 번째로 큰 시장 점유율을 차지하고 있습니다. 이 폐기물에는 자투리, 여분의 원단, 생산 공정에서 발생하는 불합격품, 불량품, 비규격품 등이 포함되며, 이들은 모두 깨끗하고 오염되지 않았으며, 소비 후 폐기물보다 분류가 용이합니다. 대규모 섬유 제조업체에서는 이러한 잔류물이 대량으로 발생하기 때문에 재활용을 위한 매력적이고 경제적인 원료가 됩니다. 또한, 일반적으로 소비자 이전 폐기물은 착용, 세탁, 염색되지 않았기 때문에 섬유의 품질이 높고, 기계적 또는 화학적 재활용에 적합합니다. 순환형 패션에 대한 관심과 소비자의 인식이 높아지면서 현재는 소비자계 폐기물이 시장을 독점하고 있지만, 소비자계 폐기물 이전의 폐기물은 신뢰성과 처리의 용이성으로 인해 큰 시장 점유율을 유지하고 있습니다.

기계적 재활용은 비용 효율성, 확장성, 수년간의 산업적 존재감으로 인해 섬유 재활용 공정 분야에서 두 번째 점유율을 차지하고 있습니다. 이 방식은 사용한 섬유를 물리적으로 파쇄, 카드화하여 섬유로 만들어 단열재, 자동차 패드, 산업용 웨스, 재생원사 등의 제품으로 재사용하는 방식입니다. 화학적 재활용과 달리 기계적 방법은 용제나 복잡한 화학 반응이 필요하지 않기 때문에 환경 친화적이며, 기술 인프라가 제한된 지역에 적합합니다. 자본비용이 낮고 운영이 간편하기 때문에 특히 신흥 시장 중소규모의 재활용업체들이 선호하는 선택이 되고 있습니다.

디지털화가 진행되면서 소비자들이 편리한 플랫폼을 선호하기 때문에 온라인 채널은 섬유 재활용 시장에서 두 번째로 큰 시장입니다. 전자상거래, 재활용 포털 사이트, 앱을 통해 소비자는 집에 있으면서 수거, 기부, 재활용 의류 구매를 예약할 수 있습니다. 이는 특히 지속가능성을 중시하는 환경의식이 높은 젊은 소비자들에게 어필할 수 있습니다. 온라인 채널은 또한 직접 상호 작용을 용이하게 하고, 비용을 절감하며, 중간 유통업체를 우회합니다. 오프라인 중심과 B2B가 여전히 지배적이지만, 확장성, 개인화된 데이터, 전 세계 도달 범위로 인해 온라인 방식이 빠르게 성장하고 있습니다. 소셜 미디어와 인식 개선 캠페인은 디지털 섬유 재활용에 대한 접근성을 높이고 있습니다.

북미는 재활용 인프라가 잘 발달되어 있고, 규제적 지원이 잘 되어 있으며, 지속 가능한 제품에 대한 소비자 수요가 증가함에 따라 섬유 재활용 시장에서 두 번째 점유율을 차지하고 있습니다. 이 지역에서는 1인당 의류 소비량이 많고 패스트 패션이 확산되면서 매년 대량의 섬유 폐기물이 발생하고 있습니다. 따라서 재활용 가능한 섬유제품이 안정적으로 공급되고, 재활용 기업 및 비영리단체는 효율적인 회수 시스템 및 소매업체와의 제휴를 통해 이를 활용하고 있습니다. 매립지 전환 의무화 및 생산자책임재활용제도(EPR) 확대와 같은 정부 이니셔티브는 섬유제품 회수 및 순환형 비즈니스 모델을 더욱 촉진하고 있습니다. 북미는 섬유 재활용 제품의 주요 생산국이기도 하며, Unifi, Inc, Patagonia, Inc, Leigh Fibers, Martex Fiber 등의 주요 기업이 있습니다.

세계의 섬유 재활용 시장에 대해 조사했으며, 소재별, 섬유 폐기물별, 공정별, 유통 채널별, 최종 이용 산업별, 지역별 동향, 시장 진출 기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

거시경제 지표

밸류체인 분석

생태계 분석

사례 연구 분석

규제 상황

기술 분석

고객의 비즈니스에 영향을 미치는 동향/혼란

무역 분석

2025년-2026년 주요 컨퍼런스 및 이벤트

가격 분석

특허 분석

제6장 섬유 재활용 시장(소재별)

서론

코튼

폴리에스테르 및 폴리에스테르 섬유

울

나일론 및 나일론 섬유

기타

제7장 섬유 재활용 시장(섬유 폐기물별)

서론

PRE-CONSUMER WASTE

POST-CONSUMER WASTE

제8장 섬유 재활용 시장(공정)

서론

기계

화학제품

제9장 섬유 재활용 시장(유통 채널별)

서론

온라인 채널

소매점 및 백화점

제10장 섬유 재활용 시장(최종 이용 산업별)

서론

의류

인테리어

산업 및 공공기관

기타

제11장 섬유 재활용 시장(지역별)

서론

아시아태평양

중국

일본

인도

한국

호주

인도네시아

베트남

기타

북미

미국

캐나다

멕시코

유럽

영국

독일

러시아

프랑스

이탈리아

스페인

네덜란드

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

기타

제12장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제13장 기업 개요

주요 시장 진출기업

LENZING AG

BIRLA CELLULOSE(GRASIM INDUSTRIES LIMITED)

HYOSUNG TNC.

UNIFI, INC.

RENEWCELL(ALTOR)

PATAGONIA, INC.

TEXTILE RECYCLING INTERNATIONAL(WATERLAND)

LEIGH FIBERS

MARTEX FIBER

THE WOOLMARK COMPANY

TOYOBO TEXTILE CO., LTD.

기타 기업

WORN AGAIN TECHNOLOGIES

PURE WASTE

REMONDIS SE & CO. KG

RETEX TEXTILES INC.

BOER GROUP

INFINITED FIBER COMPANY

PISTONI S.R.L

AMERICAN TEXTILE RECYCLING SERVICE

REJU

ECOTEX GROUP

PROCOTEX

IINOUIIO

ANANDHI TEXSTYLES

USHA YARNS LTD

GEBR. OTTO BAUMWOLLFEINZWIRNEREI GMBH+CO. KG

제14장 부록

LSH

영문 목차

영문목차

The textile recycling market is estimated at USD 8.41 billion in 2025 and is projected to reach USD 11.88 billion by 2030, at a CAGR of 7.2% from 2025 to 2030.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Kilo Tons)

Segments

By Material, Textile Waste, Process, Distribution Channel, End-Use Industry, and Region

Regions covered

Europe, North America, Asia Pacific, Middle East & Africa, and South America

Cotton holds the second-largest market share in textile recycling due to its high global use, biodegradability, and reuse potential in mechanical and chemical methods. As a common natural fiber in apparel and textiles, cotton generates steady pre- and post-consumer waste, providing recyclers with a scalable input. Mechanically recycled cotton is used for insulation, rags, and yarn, while chemically recycled cotton-still in development-offers options for high-value fibers like lyocell or viscose. Recycling cotton reduces water use and pesticide reliance, appealing to sustainable brands and circular economy initiatives. Although it ranks below polyester due to lower durability and blending requirements, cotton's renewability and eco-friendly appeal keep it vital in textile recycling.

''In terms of value, pre-consumer textile waste accounted for the second-largest share of the textile recycling market.''

Pre-consumer textile waste holds the second-largest market share, by textile waste, because the waste generated during manufacturing processes is consistent and predictable. This includes scraps, excess fabrics, production rejects, and off-spec materials-all clean, uncontaminated, and easier to sort than post-consumer waste. Large textile producers generate these residues in large quantities, making them an attractive and economical raw material for recycling. Moreover, pre-consumer waste typically has higher fiber quality since it hasn't been worn, washed, or dyed, making it more suitable for mechanical or chemical recycling. While post-consumer waste currently dominates the market due to rising interest in circular fashion and consumer awareness, the reliability and ease of processing pre-consumer waste help it maintain a significant market share.

"Mechanical process segment will register the second-largest market share, by process."

Mechanical recycling accounts for the second-largest share in the textile recycling process segment due to its cost-effectiveness, scalability, and longstanding industry presence. This approach involves physically shredding and carding used textiles into fiber for reuse in products such as insulation, automotive padding, industrial rags, or regenerated yarns. Unlike chemical recycling, mechanical methods do not require solvents or complex chemical reactions, making them more environmentally friendly and suitable for regions with limited technological infrastructure. Its lower capital costs and simpler operations make it a preferred option for small- to mid-scale recyclers, especially in developing markets.

"The online distribution channel segment is expected to account for a significant share of the market."

The online channel is the second-largest in the textile recycling market due to increased digitalization and consumer preference for convenient platforms. E-commerce, recycling portals, and apps enable consumers to schedule pickups, donate, or buy recycled clothing from home. This appeals especially to environmentally conscious, young consumers valuing sustainability. Online channels also facilitate direct interaction, reducing costs and bypassing middlemen. While offline centers and B2B remain dominant, online methods are growing faster because of scalability, personalized data, and global reach. Social media and awareness campaigns enhance digital textile recycling's accessibility.

"North America is projected to be the second-largest regional market for textile recycling."

North America holds the second-largest share in the textile recycling market due to its well-developed recycling infrastructure, strong regulatory support, and increasing consumer demand for sustainable products. The region produces a significant amount of textile waste annually, fueled by high per capita clothing consumption and the prevalence of fast fashion. This creates a consistent supply of recyclable textiles, which recycling companies and nonprofits have taken advantage of through efficient collection systems and partnerships with retailers. Government initiatives, such as landfill diversion mandates and extended producer responsibility (EPR) frameworks, have further promoted textile recovery and circular business models. North America is also a leading producer of textile recycling products, with major companies like Unifi, Inc., Patagonia, Inc., Leigh Fibers, Martex Fiber, and others.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type: Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

By Designation: C Level- 33%, Director Level- 33%, and Managers- 34%

By Region: North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies Lenzing AG (Austria), Birla Cellulose (India), HYOSUNG TNC (South Korea), Unifi, Inc. (US), Renewcell (Sweden), Patagonia, Inc. (US), Leigh Fibers (US), Martex Fiber (US), The Woolmark Company (Australia), Textile Recycling International (UK), Boer Group (Netherlands), REMONDIS SE & Co. KG (Germany), Procotex (Belgium), Usha Yarns Ltd (India), Infinited Fiber Company (Finland), Worn Again Technologies (UK), Reju (France), iinouiio (UK), Anandhi Texstyles (India), Pure Waste (Finland), Ecotex Group (Germany), PISTONI SRL (Italy), Retex Textiles Inc. (Canada), American Textile Recycling Service (US), Gebr. Otto Baumwollfeinzwirnerei GmbH + Co. KG (Germany).

Research Coverage

This research report categorizes the textile recycling market by materials (cotton, polyester & polyester fibers, wool, nylon & nylon fibers, other materials), by process (mechanical, chemical), by textile waste (pre-consumer, post-consumer), by distribution channel (online channel, retail & department stores), by end-use industry (apparel, industrial & institutional, home furnishing, and other end-use industries), and by region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The report covers detailed information about the main factors influencing the growth of the textile recycling market, including drivers, restraints, challenges, and opportunities. It provides a comprehensive review of key industry players, highlighting their business overview, solutions, services, key strategies, contracts, partnerships, and agreements. Additionally, the report discusses product launches, mergers, and acquisitions, and recent developments within the textile recycling sector. It also offers a competitive analysis of emerging startups in the textile recycling market ecosystem.

Reasons to buy this report:

The report will assist market leaders and new entrants by providing revenue estimates for the overall textile recycling market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report offers key market insights, including major drivers, restraints, challenges, and opportunities, giving stakeholders a clear understanding of the market's current pulse.

The report provides insights on the following pointers:

Analysis of key drivers (increasing textile waste due to decreased garment life, high emission of greenhouse gases, increasing consumption of energy and water), restraints (usage of harmful chemicals, high processing cost & poor return on investment), opportunities (growing adoption of circular industries, expansion in emerging markets), and challenges (fast fashion, lack of global textile waste traceability systems) influencing the growth of the textile recycling market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the textile recycling market.

Market Development: Comprehensive information about lucrative markets - the report analyses the textile recycling market across varied regions.

Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the textile recycling market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Lenzing AG (Austria), Birla Cellulose (India), HYOSUNG TNC (South Korea), Unifi, Inc. (US), Renewcell (Sweden), Patagonia, Inc. (US), Leigh Fibers (US), Martex Fiber (US), and The Woolmark Company (Australia).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of major secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 GROWTH RATE ASSUMPTIONS/FORECAST

2.5.1 SUPPLY SIDE

2.5.2 DEMAND SIDE

2.6 RESEARCH LIMITATIONS & RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TEXTILE RECYCLING MARKET

4.2 TEXTILE RECYCLING MARKET, BY MATERIAL

4.3 TEXTILE RECYCLING MARKET, BY TEXTILE WASTE

4.4 TEXTILE RECYCLING MARKET, BY PROCESS

4.5 TEXTILE RECYCLING MARKET, BY DISTRIBUTION CHANNEL

4.6 TEXTILE RECYCLING MARKET, BY END-USE INDUSTRY

4.7 TEXTILE RECYCLING MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing textile waste due to decreased garment life

5.2.1.2 High emissions of greenhouse gases

5.2.1.3 Increasing consumption of energy and water

5.2.2 RESTRAINTS

5.2.2.1 Usage of harmful chemicals

5.2.2.2 High processing cost and poor return on investment

5.2.3 OPPORTUNITIES

5.2.3.1 Growing adoption of circular industries

5.2.3.2 Expansion in emerging economies

5.2.4 CHALLENGES

5.2.4.1 Fast fashion

5.2.4.2 Lack of global textile waste traceability systems

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 THREAT OF SUBSTITUTES

5.3.2 BARGAINING POWER OF SUPPLIERS

5.3.3 THREAT OF NEW ENTRANTS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GLOBAL GDP TRENDS

5.6 VALUE CHAIN ANALYSIS

5.6.1 COLLECTION

5.6.2 SORTING

5.6.3 RECYCLING

5.6.4 END USERS

5.7 ECOSYSTEM ANALYSIS

5.8 CASE STUDY ANALYSIS

5.8.1 BRAZILIAN TEXTILE AND CLOTHING INDUSTRY

5.8.2 TEXTILE RECYCLING ASSOCIATION

5.8.3 TEXTILE RECYCLING TRANSFORMATION

5.9 REGULATORY LANDSCAPE

5.9.1 REGULATORY SCENARIO

5.9.1.1 Global Recycle Standard (GRS)

5.9.1.2 Recycled Claim Standard (RCS)

5.9.1.3 International Organization for Standardization 14021:2016

5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS