핵의학 장비 시장 : 시스템 유형별, 치료 분야별, 차원별, 최종사용자별, 지역별 - 예측(-2030년)

Nuclear Medicine Equipment Market by Product (Imaging: PET, SPECT, Gamma; GM Counter, Dose Calibrator), Software (Image Management, PACS, Treatment, Analytic, Workflow), Therapy (Onco, Cardio, Neuro, Ortho), End User & Region - Global Forecasts to 2030

상품코드:1798382

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 356 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

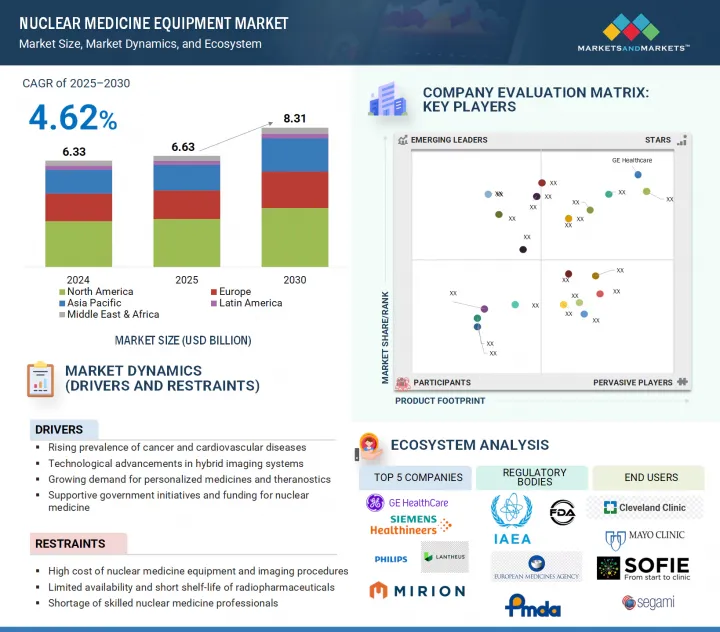

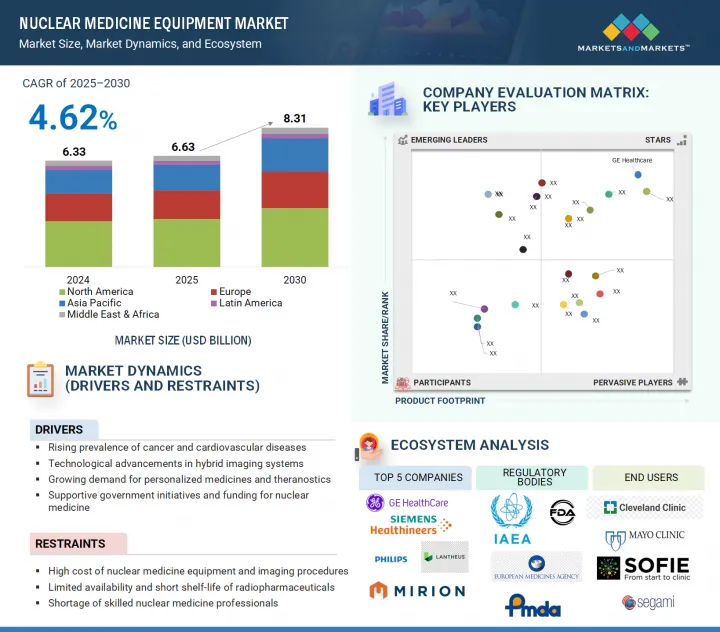

핵의학 장비 시장 규모는 2025년에 66억 3,000만 달러로 평가되었고, 2030년에는 83억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 4.62%를 보일 전망입니다.

암, 심혈관 질환 등 만성질환의 유병률 증가와 조기 및 정확한 영상진단에 대한 수요 증가가 핵의학 장비 시장 성장을 가속하고 있습니다.

조사 범위

조사 대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

시스템 유형별, 치료 분야별, 차원별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

또한, 개인 맞춤형 의료에 대한 인식 증가, 방사성의약품의 용도 확대, 정부 지원책, 방사성의약품에 대한 접근성 개선 등이 시장 성장에 기여하고 있습니다. AI 통합, 모바일/원격 접속 등의 기술 혁신은 진단 효율을 향상시키고, 시장 진출기업에게 큰 비즈니스 기회를 제공할 것으로 보입니다.

차원별로는 2024년 3D 부문이 핵의학 기기 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 3D 시스템의 뛰어난 이미징 능력으로 인해 2D 이미징보다 더 높은 공간 해상도, 더 상세한 해부학적 디테일, 더 정확한 병변 국소화를 제공합니다. 이러한 장점은 정확한 시각화가 진단, 병기 결정, 치료 계획에 필수적인 종양학, 심장학, 신경학에서 특히 유용합니다. PET/CT 및 SPECT/CT와 같이 기본적으로 3D 영상을 제공하는 첨단 영상기법의 채택이 증가하고 정량적 영상 및 맞춤 치료 접근법에 대한 수요가 증가함에 따라 3D 부문의 우위에 기여하고 있습니다.

2024년 핵의학 기기 시장은 북미 시장이 독점했습니다. 이러한 우위는 첨단 의료 인프라와 핵의학 시술의 보급 등 다양한 요인에 의해 가속화되고 있습니다. 미국 학술원(NCBI)의 보고에 따르면, 방사성의약품과 영상진단기기를 이용한 핵의학 시술은 미국에서만 연간 2,000만 건 가까이 시행되고 있으며, 하이브리드 PET/CT와 SPECT/CT 시스템의 성장이 증가하고 있다고 합니다. 또한, 만성질환, 특히 암 증가는 2024년까지 미국에서 200만 명 이상의 신규 환자와 612만 명의 사망자를 차지할 것으로 예측되고 있어, 북미에서는 조기에 정확한 진단 기술이 더욱 중요해지고 있습니다. 세계 핵의학 기기 시장에서 북미가 우위를 점하고 있는 주요 요인은 유리한 상환 정책, 민관 양 부문의 막대한 연구개발비, GE Healthcare, Siemens Healthineers, Cardinal Health 등 주요 업계 진출 기업의 존재 등입니다.

세계의 핵의학 기기 시장에 대해 조사했으며, 시스템 유형별, 치료 분야별, 차원별, 최종사용자별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

서론

시장 역학

고객의 비즈니스에 영향을 미치는 동향/혼란

업계 동향

가격 분석

밸류체인 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

특허 분석

무역 분석

2025년-2026년 주요 컨퍼런스 및 이벤트

사례 연구 분석

관세 및 규제 상황

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

최종사용자 분석

비즈니스 모델

AI/생성형 AI의 영향

2025년 미국 관세의 영향-개요

제6장 핵의학 장비 시장(시스템 유형별)

서론

영상 진단 장비

비영상 진단법

제7장 핵의학 장비 시장(치료 분야별)

서론

종양과

신경과

심장병과

정형외과

갑상선

기타

제8장 핵의학 장비 시장(차원별)

서론

2D

3D

제9장 핵의학 장비 시장(최종사용자별)

서론

병원

진단영상센터

암 치료센터

기타

제10장 핵의학 장비 시장(지역별)

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

스웨덴

기타

아시아태평양

아시아태평양의 거시경제 전망

일본

중국

인도

한국

호주

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타

제11장 경쟁 구도

개요

주요 시장 진출기업의 전략

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

시장 순위 분석

브랜드/제품 비교

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제12장 기업 개요

주요 시장 진출기업

GE HEALTHCARE

SIEMENS HEALTHINEERS AG

KONINKLIJKE PHILIPS N.V.

MIRION TECHNOLOGIES, INC.

CANON MEDICAL SYSTEMS CORPORATION

HERMES MEDICAL SOLUTIONS

DOSISOFT SA

SEGAMI CORPORATION

WINKGEN MEDICAL SYSTEMS GMBH & CO. KG

COMECER S.P.A.

SYNTERMED INC.

ULTRASPECT INC.

LABLOGIC SYSTEMS LTD.

MEDISO LTD.

CATALYST MEDTECH

LEMER PAX

SPECTRUM DYNAMICS MEDICAL

NEUSOFT MEDICAL SYSTEMS CO., LTD.

BRAINLAB SE

MIRADA MEDICAL

기타 기업

TRASIS

SOFIE

ITM ISOTOPE TECHNOLOGIES MUNICH SE

POSITRIGO AG

PAIRE

제13장 부록

LSH

영문 목차

영문목차

The nuclear medicine equipment market was valued at USD 6.63 billion in 2025 and is estimated to reach USD 8.31 billion by 2030, registering a CAGR of 4.62% during the forecast period. The growing prevalence of chronic diseases such as cancer and cardiovascular disorders, as well as the rising demand for early and accurate diagnostic imaging, are driving market growth in nuclear medicine equipment.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product Type, Therapeutic Area, Dimension, End User, Region

Regions covered

North America, Europe, APAC, LATAM, MEA

Furthermore, increased awareness of personalized medicine, expanded applications of radiotheranostics, supportive government initiatives, and improved access to radiopharmaceuticals are all contributing to market growth. Technological innovations, such as AI integration and mobile/remote access, will improve diagnostic efficiency and create significant opportunities for market players.

The 3D segment dominated the nuclear medicine equipment market, by dimension, in 2024.

Based on dimension, the 3D segment is expected to hold the largest share of the nuclear medicine equipment market in 2024. This is due to the superior imaging capabilities of 3D systems, which provide higher spatial resolution, greater anatomical detail, and more accurate localization of lesions than 2D imaging. These benefits are especially useful in oncology, cardiology, and neurology, where accurate visualization is essential for diagnosis, staging, and treatment planning. The growing adoption of advanced modalities such as PET/CT and SPECT/CT, which provide 3D imaging by default, combined with rising demand for quantitative imaging and personalized treatment approaches, contributes to the 3D segment's dominance.

The North American market accounted for the largest share in the nuclear medicine equipment market in 2024.

The North American market dominated the nuclear medicine equipment market in 2024. This dominance is accelerated by various factors such as advanced healthcare infrastructure and the widespread use of nuclear medicine procedures. The US National Academies (NCBI) report that nearly 20 million nuclear medicine procedures using radiopharmaceuticals and imaging instruments are carried out annually in the US alone, with increasing growth in hybrid PET/CT and SPECT/CT systems. Moreover, the rise in chronic diseases, especially cancer, which is predicted to account for over 2 million new cases and 6,12,000 deaths in the US by 2024, makes early and accurate diagnosis technologies even more crucial in North America. The main factors contributing to North America's dominance in the global nuclear medicine equipment market are favorable reimbursement policies, substantial R&D spending by both the public and private sectors, and the presence of major industry players such as GE Healthcare, Siemens Healthineers, and Cardinal Health.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the nuclear medicine equipment marketplace.

The breakdown of primary participants is as mentioned below:

By Company Type - Tier 1 (41%), Tier 2 (31%), and Tier 3 (28%)

By Designation - C-level (44%), Directors (31%), and Others (25%)

By Region - North America (45%), Europe (28%), Asia Pacific (20%), Latin America (4%), Middle East & Africa (3%)

Key Players in the Nuclear Medicine Equipment Market

Prominent players in the nuclear medicine equipment market include Hermes Medical Solutions (Sweden), DOSIsoft (France), Segami Corporation (US), GE HealthCare (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Mirion Technologies, Inc. (US), Comecer S.p.A. (Italy), Syntermed (US), UltraSPECT Inc. (US), LabLogic Systems Ltd. (UK), Mediso Ltd. (Hungary), CANON MEDICAL SYSTEMS CORPORATION (Japan), Catalyst Medtech (US), Lemer Pax (France), Spectrum Dynamics Medical (US), Neusoft Medical Systems Co., Ltd. (China), Brainlab AG(Germany), Mirada Medical(UK), Trasis (Belgium), SOFIE (US), ITM Isotope Technologies Munich SE (Germany), Positrigo AG (Switzerland), PAIRE (France).

Players adopted organic as well as inorganic growth strategies such as product launches and enhancements, and investments, partnerships, collaborations, joint ventures, funding, acquisition, expansions, agreements, contracts, and alliances to increase their offerings, cater to the unmet needs of customers, increase their profitability, and expand their presence in the global market.

The study includes an in-depth competitive analysis of these key players in the nuclear medicine equipment market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report studies the nuclear medicine equipment market based on product type, therapeutic area, dimension, end user, and region.

The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

The report studies micro-markets with respect to their growth trends, prospects, and contributions to the total nuclear medicine equipment market.

The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

The report can help established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the following five strategies.

This report provides insights into the following pointers:

Analysis of key drivers (rising prevalence of cancer and cardiovascular diseases, technological advancements in hybrid imaging systems, growing demand for personalized medicines and theranostics), restraints (high cost of nuclear medicine equipment and imaging procedures, limited availability and short shelf-life of radiopharmaceuticals), opportunities (development of novel radiotracers and targeted imaging agents, integration of AI and data analytics in imaging workflows), and challenges (stringent regulatory approval processes for equipment and radiopharmaceuticals, shortage of skilled nuclear medicine professionals, radioactive waste management and safety concerns) influencing the industry macro dynamics of nuclear medicine equipment market.

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the nuclear medicine equipment market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of nuclear medicine equipment across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the nuclear medicine equipment market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the nuclear medicine equipment market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.1.1 SECONDARY RESEARCH

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY RESEARCH

2.1.2.1 Primary sources

2.1.2.2 Key data from primary sources

2.1.2.3 Breakdown of primary interviews

2.1.2.4 Insights from primary experts

2.2 RESEARCH METHODOLOGY

2.3 MARKET SIZE ESTIMATION

2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

2.5 MARKET SHARE ESTIMATION

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS

2.8 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 OVERVIEW OF NUCLEAR MEDICINE EQUIPMENT MARKET

4.2 ASIA PACIFIC: NUCLEAR MEDICINE EQUIPMENT MARKET, BY THERAPEUTIC AREA

4.3 GEOGRAPHIC SNAPSHOT OF NUCLEAR MEDICINE EQUIPMENT MARKET

4.4 NUCLEAR MEDICINE EQUIPMENT MARKET: REGIONAL MIX

4.5 NUCLEAR MEDICINE EQUIPMENT MARKET: DEVELOPED VS. EMERGING MARKETS

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rapid expansion of theranostics

5.2.1.2 Technological advancements in hybrid imaging modalities

5.2.1.3 Favorable government support and expanding healthcare infrastructure

5.2.1.4 Advancements in radiotracers and radiopharmaceuticals

5.2.1.5 Integration of AI into nuclear medicine equipment

5.2.2 RESTRAINTS

5.2.2.1 Capital-intensive nature of equipment

5.2.2.2 Short half-life of radiopharmaceuticals

5.2.2.3 High maintenance and operational costs

5.2.2.4 Shortage of trained personnel

5.2.3 OPPORTUNITIES

5.2.3.1 Growing preference for personalized and precision medicine

5.2.3.2 Telemedicine and cloud-native platforms & mobile/remote imaging capabilities

5.2.4 CHALLENGES

5.2.4.1 Global isotope supply chain instability

5.2.4.2 Cybersecurity and data privacy issues in imaging IT

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 INDUSTRY TRENDS

5.4.1 SHIFT TOWARD HYBRID AND MULTI-MODALITY IMAGING SYSTEMS

5.4.2 ADVANCEMENTS IN DETECTOR TECHNOLOGIES AND IMAGE QUALITY

5.4.3 GROWING DEMAND FOR COMPACT AND VERSATILE SYSTEMS

5.4.4 INTEGRATION OF ARTIFICIAL INTELLIGENCE AND AUTOMATION

5.4.5 CONNECTIVITY AND CLOUD-ENABLED WORKFLOWS

5.5 PRICING ANALYSIS

5.5.1 INTRODUCTION

5.5.2 INDICATIVE PRICE OF NUCLEAR MEDICINE EQUIPMENT, BY KEY PLAYER

5.5.3 INDICATIVE PRICE OF NUCLEAR MEDICINE EQUIPMENT, BY REGION

5.5.4 AVERAGE SELLING PRICE OF NUCLEAR CARDIOLOGY REPORTING SOFTWARE

5.5.5 PRICING MODELS

5.6 VALUE CHAIN ANALYSIS

5.7 ECOSYSTEM ANALYSIS

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Hybrid imaging systems

5.9.1.2 Digital detection technology

5.9.1.3 Artificial Intelligence (AI) and advanced image reconstruction techniques

5.9.1.4 Time-of-Flight (TOF) technology

5.9.1.5 Solid-state detector technology

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Radiopharmaceutical development and theranostics

5.9.2.2 Advanced computing and big data analytics

5.9.2.3 Robotics and automated dose dispensing systems

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 Magnetic Resonance Imaging (MRI) integration

5.9.3.2 Computed Tomography (CT) advancements

5.10 PATENT ANALYSIS

5.11 TRADE ANALYSIS

5.11.1 IMPORT DATA FOR HS CODE 901814

5.11.2 EXPORT DATA FOR HS CODE 901814

5.12 KEY CONFERENCES AND EVENTS, 2025-2026

5.13 CASE STUDY ANALYSIS

5.13.1 PRECISION IN NUCLEAR MEDICINE WITH NATIONAL STANDARD TRACEABILITY

5.13.2 MULTI-MODALITY IMAGE FUSION FOR IMPROVED DIAGNOSTICS

5.13.3 REMOTE CONSULTATION WITH CLOUD-BASED NUCLEAR MEDICINE ANALYSIS

5.14 TARIFF AND REGULATORY LANDSCAPE

5.14.1 TARIFF DATA FOR HS CODE 901814

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.14.3 REGULATORY ANALYSIS

5.15 PORTER'S FIVE FORCES ANALYSIS

5.15.1 BARGAINING POWER OF SUPPLIERS

5.15.2 BARGAINING POWER OF BUYERS

5.15.3 THREAT OF NEW ENTRANTS

5.15.4 THREAT OF SUBSTITUTES

5.15.5 INTENSITY OF COMPETITIVE RIVALRY

5.16 KEY STAKEHOLDERS AND BUYING CRITERIA

5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.16.2 BUYING CRITERIA

5.17 END-USER ANALYSIS

5.17.1 UNMET NEEDS

5.17.2 END-USER EXPECTATIONS

5.18 BUSINESS MODEL

5.18.1 DIRECT EQUIPMENT SALES MODEL

5.18.2 SERVICE AND MAINTENANCE CONTRACTS

5.18.3 PAY-PER-SCAN (OR PAY-PER-USE) MODEL

5.18.4 EQUIPMENT LEASING AND FINANCING SOLUTIONS

5.18.5 INTEGRATED SOLUTIONS AND MANAGED SERVICES

5.18.6 SOFTWARE AND DATA ANALYTICS SUBSCRIPTION

5.19 IMPACT OF AI/GEN AI

5.19.1 INTRODUCTION

5.19.2 MARKET POTENTIAL OF AI/GEN AI

5.19.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

5.19.3.1 AI-based low-dose PET image reconstruction

5.19.3.2 Dose-aware diffusion models for 3D low-dose PET

5.19.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

5.19.4.1 Medical image analysis software

5.19.4.2 Radiology information systems

5.19.4.3 Clinical decision support systems

5.19.5 USER READINESS AND IMPACT ASSESSMENT

5.19.5.1 User readiness

5.19.5.1.1 User A: Hospitals

5.19.5.1.2 User B: Diagnostic imaging centers

5.19.5.2 Impact assessment

5.19.5.2.1 User A: Hospitals

5.19.5.2.2 User B: Diagnostic imaging centers

5.20 IMPACT OF 2025 US TARIFF - OVERVIEW

5.20.1 INTRODUCTION

5.20.2 KEY TARIFF RATES

5.20.3 PRICE IMPACT ANALYSIS

5.20.3.1 Capital equipment (cyclotrons, PET/SPECT systems)