종자 응용 기술 시장/SAT 시장 예측(-2030년) : 기술별, 기능별, 작물 유형별, 지역별

Seed Technologies Market/ SAT Market by Function (Seed Protection, Seed Enhancement, and Precision Seeding), Technology, Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables), and Region - Global Forecast to 2030

상품코드:1796198

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 551 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

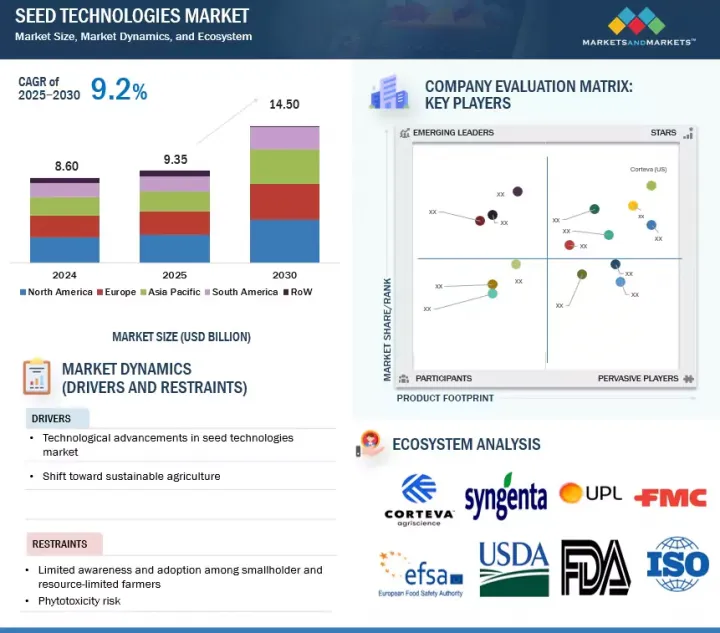

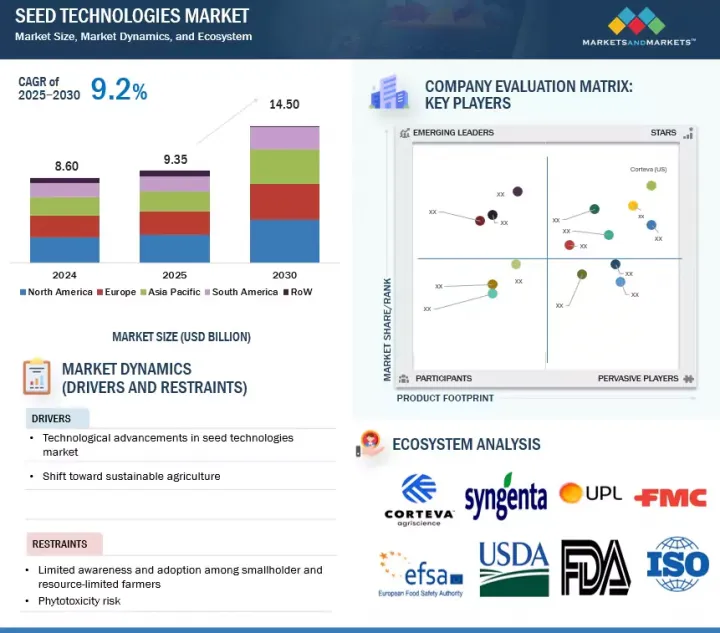

세계의 종자 응용 기술 시장 규모는 2025년에 93억 5,000만 달러로 추정되며, 예측 기간 중 CAGR은 9.2%로 전망되고 있으며, 2030년에는 145억 달러에 달할 것으로 예측됩니다.

조사 범위

조사 대상연도

2025-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(달러) 및 수량(KT)

부문별

기술별, 기능별, 작물 유형별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 남미, RoW

종자 응용기술 시장은 작물의 고수율화 요구 증가, 해충 및 병해충 압력 증가, 제형 및 전달 기술의 발전에 의해 주도되고 있습니다. 고부가가치 하이브리드 종자 및 유전자 변형 종자의 채택이 증가함에 따라 종자 보호 및 성능 향상 종자 처리에 대한 수요가 증가하고 있습니다.

또한 정부의 우호적인 정책과 인센티브에 힘입어 지속가능한 농업으로의 전환이 가속화되면서 생물학적 종자 처리제의 사용이 가속화되고 있습니다. 상업적 농업과 디지털 농업의 확대는 시장의 효율성과 작물 보호를 강화하고 있습니다. 주요 동향은 환경 친화적인 생물학적 및 미생물 기반 종자 처리제의 사용이 증가하고 있으며, 이는 규제 당국과 소비자의 지속가능성에 대한 요구와 일치합니다.

그러나 신흥 시장의 영세 농가에서는 종자 코팅 기술의 장점이 입증되었음에도 불구하고 인지도와 이용 편의성이 제한적이어서 보급에 어려움을 겪고 있으며, 이는 시장 성장을 저해하고 있습니다.

종자 코팅 기술은 종자 성능 향상, 취급 개선, 작물 보호제 및 영양제의 표적 전달에 대한 수요 증가로 인해 상당한 성장을 보일 것으로 예측됩니다. 이러한 기술에는 종자 주변에 균일한 층을 형성하는 폴리머, 착색제, 미네랄, 활성 성분을 적용하여 유동성, 단일성, 기계적 및 정밀농업 시스템에서 심기 정확도를 향상시키는 기술이 포함됩니다. 채소, 옥수수, 곡물 등 고부가가치 작물에서 코팅 종자 채택이 증가하고 있으며, 생물 자극제 및 미생물 접종제를 포함한 생물학적 코팅에 대한 수용이 확대되고 있는 것도 시장 확대를 더욱 촉진하고 있습니다.

또한 종자 코팅은 자동 종자 처리 장비 및 파종 장비와의 호환성을 제공하여 밭에서의 편차 및 인건비를 절감할 수 있습니다. 고분자 제형과 방출 제어형 코팅의 혁신은 보존 기간과 처리 효능의 향상으로 이어질 수 있으므로 많은 지지를 받고 있습니다. 농가가 투입 효율과 균일한 작물 출수를 우선시하는 경향이 강해짐에 따라 종자 코팅 기술은 선진국과 신흥 시장에서 널리 채택될 것으로 예측됩니다.

곡물 및 곡물은 전 세계에서 재배 면적이 넓고 식량안보에 중요한 역할을 하는 만큼 종자 응용 기술 시장의 작물 유형 부문에서 가장 큰 점유율을 차지하고 있습니다. 옥수수, 밀, 쌀, 보리 등의 작물은 많은 지역에서 주식이며, 초기 단계의 해충과 병충해의 압력에 매우 민감하므로 종자 응용 솔루션의 가장 유력한 후보로 꼽히고 있습니다. 농가는 묘목의 활력을 높이고, 균일한 출수를 보장하며, 토양 전염성 병원균과 해충으로부터 보호하기 위해 화학적 및 생물학적 처리를 포함한 종자 적용 기술에 의존하고 있습니다.

특히 옥수수의 경우, 고수율 품종과 유전자변형 품종이 널리 보급되면서 효과적인 종자 보호의 필요성이 더욱 커지고 있습니다. 또한 제형 기술의 발전과 대규모 기계화 농업 시스템에 종자 적용 제품의 통합으로 주요 곡물 생산 지역 전체에서 그 사용이 강화되고 있습니다. 정부의 지원 정책과 주요 농약 및 종자 기업의 존재는 이 부문에서 곡물 및 곡물 시장의 지위 강화에 기여하고 있습니다.

북미는 첨단 농법의 보급, 주요 산업 기업의 존재, 유전자 변형 종자 및 고부가가치 종자의 높은 사용률에 힘입어 예측 기간 중 전 세계 종자 응용 기술 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이 지역의 치료 시장은 이미 잘 확립되어 있으며, 시장 성장에 기여하고 있습니다. 옥수수, 대두, 카놀라는 종자 보호 및 강화 솔루션에 대한 수요를 주도하고 있습니다. 또한 북미는 정밀농업, 종합적 병해충 관리 등의 기술 혁신을 선도하며 시장에서의 우위를 더욱 강화하고 있습니다.

반면, 아시아태평양은 식량 수요 증가, 급속한 인구 증가, 인도, 중국, 동남아시아 국가의 농업 현대화에 힘입어 예측 기간 중 종자 응용 기술 시장에서 가장 빠르게 성장할 것으로 예측됩니다. 농가의 의식 향상, 지속가능한 농업을 지원하는 정부의 구상, 하이브리드 종자 채택 확대 등이 종자 처리 시장 수요를 가속화하고 있습니다. 또한 상업적 농업의 확대, 농업 투입물에 대한 접근성 개선, 세계 종자 응용 기술 기업의 투자 증가는 이 지역 전체 시장 성장을 가속할 것으로 예측됩니다.

세계의 종자 응용 기술 시장/SAT 시장에 대해 조사했으며, 기술별, 기능별, 작물 유형별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

종자 응용 기술 시장의 참여 기업에 매력적인 기회

북미 : 종자 응용 기술 시장(기능별·국가별)

국가별 종자 응용 기술 시장

종자 응용 기술 시장(기술별·지역별)

종자 응용 기술 시장(기능별·지역별)

작물 유형별·지역별 종자 응용 기술 시장

제5장 시장 개요

서론

거시경제 지표

주요 상업용 종자 생산의 성장

고가치 작물 시장 수요의 증가

유기농업 실천의 성장

시장 역학

촉진요인

억제요인

기회

과제

AI/생성형 AI가 종자 응용 기술 시장에 미치는 영향

서론

종자 응용 기술 시장에서 GEN AI의 활용

사례 연구 분석

제6장 업계 동향

서론

2025년 미국 관세의 영향 - 종자 응용 기술 시장

서론

주요 관세율

가격 영향 분석

국가/지역에 대한 영향

최종 용도 산업에 대한 영향

밸류체인 분석

무역 분석

기술 분석

가격 분석

에코시스템 분석

고객 비즈니스에 영향을 미치는 동향/혼란

특허 분석

2025-2026년의 주요 컨퍼런스와 이벤트

규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

투자와 자금조달 시나리오

사례 연구 분석

BIOWEG와 BAYER가 지속가능 농업을 위한 생분해성 종자 코팅의 개발을 위해 제휴

BORREGAARD가 셀룰로오스 기반 생분해성 종자 코팅을 발표

KINZE의 진정한 스피드 혁신 : 고속 정밀 재배를 재정의

AGCO의 전략적 비약 : TRIMBLE AG와의 합병사업을 통해 정밀농업을 추진

제7장 종자 응용 기술 시장(기술별)

서론

종자 코팅

종자 처리

종자 펠릿화

종자 준비와 조정

종자 소독

정밀 파종

제8장 종자 응용 기술 시장(기능별)

서론

종자 보호

종자 강화

정밀 파종

제9장 종자 응용 기술 시장(작물 유형별)

서론

지방 종자와 두류

곡물

과일과 채소

기타 작물

제10장 종자 응용 기술 시장(지역별)

서론

북미

미국

캐나다

멕시코

유럽

프랑스

독일

스페인

이탈리아

영국

기타

아시아태평양

중국

인도

일본

호주와 뉴질랜드

기타

남미

브라질

아르헨티나

기타

기타 지역

아프리카

중동

제11장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석, 2020-2024년

시장 점유율 분석, 2024년

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

기업 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오와 동향

제12장 기업 개요

주요 참여 기업

BASF SE

CORTEVA

SYNGENTA

BAYER AG

UPL

FMC CORPORATION

SUMITOMO CHEMICAL CO., LTD.

CRODA INTERNATIONAL PLC

NUFARM

NOVONESIS GROUP

SYENSQO

AGCO CORPORATION

DEERE & COMPANY

KINZE MANUFACTURING

GERMAINS SEED TECHNOLOGY

기타 기업(스타트업/중소기업)

VERDESIAN LIFE SCIENCES

ANDERMATT GROUP AG

NAIO TECHNOLOGY INC.

IPL BIOLOGICALS

AGRILIFE

ROVENSA NEXT

BIONEMA

BIOCONSORTIA

NORDIA MICROBES A/S

APHEA.BIO

제13장 인접 시장과 관련 시장

제14장 부록

KSA

영문 목차

영문목차

The global market for seed technologies is estimated to be valued at USD 9.35 billion in 2025 and is projected to reach USD 14.50 billion by 2030, at a CAGR of 9.2% during the forecast period.

Scope of the Report

Years Considered for the Study

2025-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD) and Volume (KT)

Segments

By Technology, Function, Crop Type, and Regions

Regions covered

North America, Europe, Asia Pacific, South America, and RoW

The seed technologies market is driven by the growing need for higher crop yields, increasing pest and disease pressures, and advances in formulation and delivery technologies. The rising adoption of high-value hybrid and genetically modified seeds has amplified the demand for protective and performance-enhancing seed treatments.

Additionally, a global shift toward sustainable agriculture, supported by favorable government policies and incentives, is accelerating the use of biological seed treatments. Expanding commercial farming and digital agriculture are enhancing market efficiency and crop protection. A key trend is the rising use of eco-friendly biological and microbe-based seed treatments, aligning with sustainability demands from regulators and consumers.

However, limited awareness and accessibility among smallholder farmers in developing regions hinder widespread adoption despite the proven benefits of seed applied technologies, restraining market growth.

"The seed coating technologies segment will grow at significant rate during the forecast period"

Seed coating technologies are projected to witness significant growth, driven by the increasing demand for enhanced seed performance, improved handling, and targeted delivery of crop protection and nutritional agents. These technologies involve the application of polymers, colorants, minerals, and active ingredients that form a uniform layer around the seed, improving flowability, singulation, and planting precision in mechanical and precision farming systems. The rising adoption of coated seeds in high-value crops such as vegetables, corn, and cereals, along with the growing acceptance of biological coatings, including biostimulants and microbial inoculants, further supports market expansion.

Additionally, seed coating offers compatibility with automated seed treatment and planting equipment, reducing on-field variability and labor costs. Innovations in polymer formulations and controlled-release coatings are also gaining traction as they enhance shelf life and treatment efficacy. As farmers increasingly prioritize input efficiency and uniform crop emergence, seed coating technologies are expected to gain widespread adoption across developed and emerging agricultural markets.

"The cereals & grains segment will hold the largest share in crop type segment during forecast period"

Cereals & grains hold the largest share in the crop type segment of the seed technologies market, driven by their vast global cultivation area and critical role in food security. Crops such as corn, wheat, rice, and barley are staple foods in many regions and are highly sensitive to early-stage pest and disease pressures, making them prime candidates for seed applied solutions. Farmers rely on seed applied technologies, including chemical and biological treatments, to enhance seedling vigor, ensure uniform emergence, and protect against soil-borne pathogens and insects.

The widespread adoption of high-yielding and genetically modified varieties, particularly in corn, further increases the need for effective seed protection. Moreover, advancements in formulation technologies and the integration of seed applied products into large-scale mechanized farming systems have strengthened their use across major cereal-producing regions. Supportive government policies, along with the presence of leading agrochemical and seed companies, have contributed to the strong market position of cereals and grains in this segment.

"North America holds the largest share, while Asia Pacific is expected to be the fastest growing market during the forecast period"

North America is expected to hold the largest share in the global seed technologies market during the forecast period, supported by widespread adoption of advanced farming practices, the presence of key industry players, and high use of genetically modified and high-value seeds. The region's well-established treatment market has contributed to market growth. Corn, soybean, and canola drive strong demand for seed protection and enhancement solutions. Additionally, North America leads in technological innovation, including precision agriculture and integrated pest management, further strengthening its dominance in the market.

In contrast, the Asia Pacific region is anticipated to be the fastest-growing market for seed applied technologies during the forecast period, driven by increasing food demand, rapid population growth, and the modernization of agriculture in India, China, and Southeast Asian nations. Rising farmer awareness, government initiatives supporting sustainable agriculture, and growing adoption of hybrid seeds are accelerating demand for the seed treatment market. Additionally, the expansion of commercial farming, improved access to agri-inputs, and increased investment from global seed applied technologies companies are expected to fuel market growth across the region.

Break-up of primaries

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the seed technologies market:

By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

By Designation: Directors- 20%, Managers - 50%, Executives - 30%

By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World - 10%

Prominent companies in the market include BASF SE (Germany), Bayer AG (Germany), UPL (India), Corteva (US), Croda (UK), FMC (US), Nufarm (Australia), Syngenta (US), Germains Seed (UK), Sumitomo Chemicals (Japan), Deere & Company (US), Kinze Manufacturing (US), Novonesis Group (Denmark), Syensqo (Belgium), and AGCO Corporation (US).

Other players include Verdesian Life Sciences (US), Andermatt Group AG (Switzerland), IPL Biologicals (India), Naio Technologies (France), Rovensa Next (Spain), Bionema (UK), BioConsortia (US), Nordic microbe's A/S (Denmark), Aphea.Bio (Belgium), and AgriLife (India).

Research Coverage

This research report categorizes the seed technologies market by function (seed protection, seed enhancement, and precision seeding), technology (seed dressing, seed pelleting, seed coating, seed priming & conditioning, seed disinfection, and precision seeding), crop type (cereals & grains, oilseeds, fruits & vegetables, and other crop types), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding drivers, restraints, challenges, and opportunities influencing the growth of the seed technologies market.

A detailed analysis of the key industry players was done to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the seed technologies market. This report covers competitive analysis of upcoming startups in the applied technologies market ecosystem. Furthermore, the study also covers industry-specific trends such as technology analysis, ecosystem and market mapping, and patent and regulatory landscape, among others.

Reasons to buy this report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall seed applied technologies and the subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

It provides insights into the following pointers:

Analysis of key drivers (technological advancements in seed applied technologies), restraints (limited crop variety), opportunities (integration of smart home technology), and challenges (high initial cost) influencing the growth of the seed technologies market

New Product Launch/Innovation: Detailed insights on research & development activities and new product launches in the seed technologies market

Market Development: Comprehensive information about lucrative markets - analysis of the seed treatment market across varied regions

Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the seed technologies market

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparisons, and product footprints of leading players such as BASF (Germany), Bayer AG (Germany), UPL (India), Corteva (US), FMC (US), and others in the seed technologies market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 REGIONS COVERED

1.4 YEARS CONSIDERED

1.5 UNIT CONSIDERED

1.5.1 CURRENCY/VALUE UNIT

1.5.2 VOLUME CONSIDERED

1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SEED APPLIED TECHNOLOGIES MARKET

4.2 NORTH AMERICA: SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION & COUNTRY

4.3 SEED APPLIED TECHNOLOGY MARKET, BY COUNTRY

4.4 SEED APPLIED TECHNOLOGIES MARKET, BY TECHNOLOGY AND REGION

4.5 SEED APPLIED TECHNOLOGIES MARKET, BY FUNCTION AND REGION

4.6 SEED APPLIED TECHNOLOGIES MARKET, BY CROP TYPE AND REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MACROECONOMIC INDICATORS

5.2.1 GROWTH IN MAJOR COMMERCIAL SEED PRODUCTION

5.2.2 RISE IN MARKET DEMAND FOR HIGH-VALUE CROPS

5.2.3 GROWTH IN ORGANIC AGRICULTURE PRACTICES

5.3 MARKET DYNAMICS

5.3.1 DRIVERS

5.3.1.1 Technological advancements in precision agriculture

5.3.1.2 Climate change impact on agricultural practices

5.3.1.3 Demand for low-cost production solution

5.3.1.4 Growing adoption of integrated pest management

5.3.2 RESTRAINTS

5.3.2.1 Shorter shelf life of biological seed treatments

5.3.2.2 Limited adoption among smallholder farmers

5.3.2.3 Technical complexity and skill requirements

5.3.3 OPPORTUNITIES

5.3.3.1 Rising demand for bio-based technologies

5.3.3.2 Integrated seed treatment solution

5.3.3.3 Growing adoption of digital agriculture tools

5.3.4 CHALLENGES

5.3.4.1 High costs of new products

5.3.4.2 Regulatory barriers in seed treatments

5.3.4.3 Raw material price volatility

5.4 IMPACT OF AI/GEN AI ON SEED APPLIED TECHNOLOGIES MARKET

5.4.1 INTRODUCTION

5.4.2 USE OF GEN AI IN SEED APPLIED TECHNOLOGIES MARKET

5.4.3 CASE STUDY ANALYSIS

5.4.3.1 Syngenta & TraitSeq - Advancing Biostimulant Innovation Through AI

5.4.3.2 Syngenta and InstaDeep - Accelerating Trait Discovery through AI Large Language Models

5.4.3.3 Syngenta and InstaDeep - Accelerating Trait Discovery through AI Large Language Models

6 INDUSTRY TRENDS

6.1 INTRODUCTION

6.2 IMPACT OF 2025 US TARIFF - SEED APPLIED TECHNOLOGIES MARKET

6.2.1 INTRODUCTION

6.2.2 KEY TARIFF RATES

6.2.3 PRICE IMPACT ANALYSIS

6.2.4 IMPACT ON COUNTRY/REGION

6.2.4.1 US

6.2.4.2 Europe

6.2.4.3 Asia Pacific

6.2.5 IMPACT ON END-USE INDUSTRIES

6.3 VALUE CHAIN ANALYSIS

6.3.1 RESEARCH & DEVELOPMENT

6.3.2 MANUFACTURING

6.3.3 DISTRIBUTION

6.3.4 MARKETING & SALES

6.3.5 POST-SALE SERVICES

6.4 TRADE ANALYSIS

6.4.1 EXPORT SCENARIO OF HS CODE 3808

6.4.2 IMPORT SCENARIO OF HS CODE 3808

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGIES

6.5.1.1 Electrostatic seed treatment application systems

6.5.2 COMPLEMENTARY TECHNOLOGIES

6.5.2.1 Smart coating polymers and advanced seed film technologies

6.5.3 ADJACENT TECHNOLOGIES

6.5.3.1 RNA interference (RNAi) delivery systems

6.6 PRICING ANALYSIS

6.6.1 INTRODUCTION

6.6.2 AVERAGE SELLING PRICE TREND OF SEED APPLIED TECHNOLOGIES, BY FUNCTION, 2020-2024

6.6.3 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024

6.6.4 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY FUNCTION, 2024

6.7 ECOSYSTEM ANALYSIS

6.7.1 DEMAND SIDE

6.7.2 SUPPLY SIDE

6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.9 PATENT ANALYSIS

6.10 KEY CONFERENCES & EVENTS, 2025-2026

6.11 REGULATORY LANDSCAPE

6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.11.2 NORTH AMERICA

6.11.2.1 US

6.11.2.2 Canada

6.11.3 EUROPE

6.11.4 ASIA PACIFIC

6.11.4.1 India

6.11.4.2 China

6.11.4.3 Australia

6.11.5 SOUTH AMERICA

6.11.5.1 Brazil

6.11.5.2 Argentina

6.11.6 REST OF WORLD

6.11.6.1 South Africa

6.12 PORTER'S FIVE FORCES ANALYSIS

6.12.1 THREAT OF NEW ENTRANTS

6.12.2 THREAT OF SUBSTITUTES

6.12.3 BARGAINING POWER OF BUYERS

6.12.4 BARGAINING POWER OF SUPPLIERS

6.12.5 INTENSITY OF COMPETITIVE RIVALRY

6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.13.2 BUYING CRITERIA

6.14 INVESTMENT AND FUNDING SCENARIO

6.15 CASE STUDY ANALYSIS

6.15.1 BIOWEG AND BAYER PARTNER TO DEVELOP BIODEGRADABLE SEED COATINGS FOR SUSTAINABLE AGRICULTURE