기업 이미징 IT 시장 예측(-2030년) : 기능별, 모달리티별, 용도별, 치료별, 최종사용자별, 지역별

Enterprise Imaging IT Market by Function (VNA, PACS, Universal Viewer, Analytics), Modality (X-ray, MRI, CT, PET, SPECT, Mammo), Application (Diagnosis, Therapeutic, Theranostic), Therapy (Onco, Cardio, Neuro), End User, Region - Global Forecast to 2030

상품코드:1796194

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 4113 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

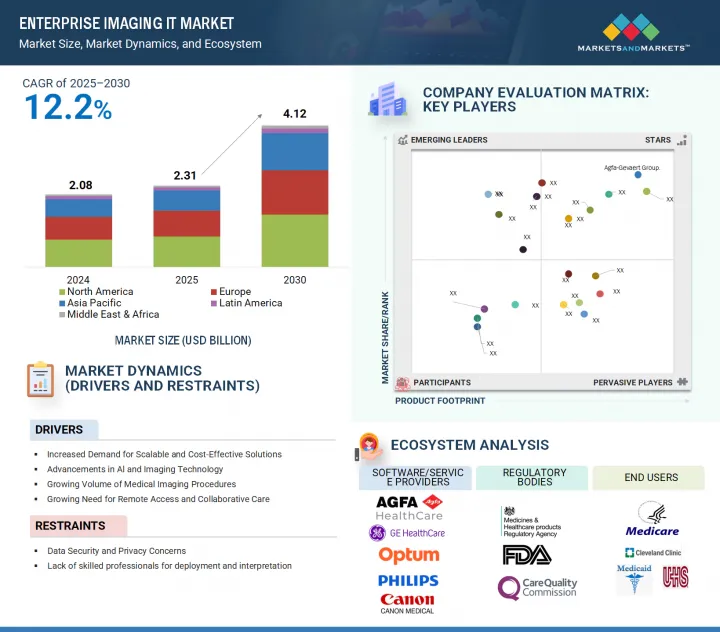

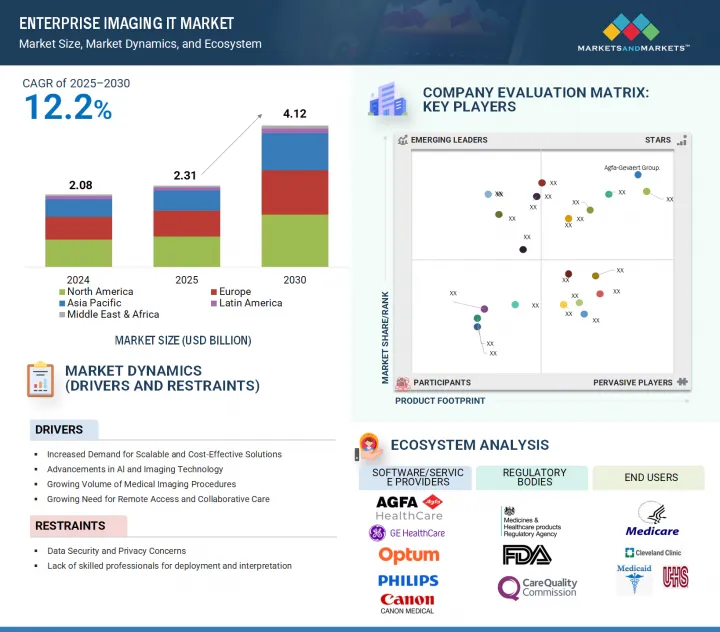

세계의 기업 이미징 IT 시장 규모는 2025년 23억 1,000만 달러에서 2030년까지 41억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 12.2%의 성장이 전망됩니다.

자본에 편중된 라이선스 모델에서 클라우드 네이티브 SaaS 배포로 전환하여 초기 비용을 낮추고 업그레이드를 가속화함으로써 수요를 촉진하고 있습니다.

조사 범위

조사 대상연도

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

기능, 모달리티, 용도, 제공, 배포 방식, 치료 영역, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

블록체인을 기반으로 한 이미지 증명 플랫폼의 등장으로 멀티 벤더 생태계에서 데이터의 무결성과 감사 가능성이 강화되고 있습니다. 의료관광 네트워크의 확장으로 표준화된 국경 간 영상 교환 허브의 필요성이 증가하고 있으며, POC(Point-Of-Care) 초음파 영상 장치 및 웨어러블 영상 장치의 보급으로 기업의 워크플로우가 병상에서의 실시간 획득을 포함하여 확대되고 있습니다. 확대되고 있습니다.

"진단 부문은 예측 기간 중 기업 이미징 IT 시장에서 가장 빠르게 성장하는 부문입니다. "

진단 부문이 기업 이미징 IT 시장에서 가장 큰 점유율을 차지하고 있습니다. 이 부문의 높은 점유율과 높은 성장세는 폐암 검진 프로그램의 전국적인 확산으로 저선량 CT 수가 급증하면서 기업 아카이브에 대한 수요가 급증했기 때문인 것으로 분석됩니다. 또한 두개내 출혈, 폐색전증과 같은 중요한 소견에 자동으로 플래그를 표시하는 AI 기반 분류 엔진의 통합은 의료 서비스 프로바이더의 진단 플랫폼 업그레이드를 촉진하고 있습니다. 또한 종양학 영상 및 신경학 영상에서 정량적 방사성동위원소 및 텍스처 분석 워크플로우가 증가함에 따라 고차원 피처셋을 대규모로 저장, 처리 및 추출할 수 있는 솔루션에 대한 수요가 증가하고 있습니다.

"2024년 기업 이미징 IT 시장에서 치료 영역별로는 순환기 분야가 가장 큰 점유율을 차지할 것으로 추정됩니다. "

순환기 부문은 계산 모델과 고충실도 CT 아카이브의 원활한 통합을 필요로 하는 CT 기반 관상동맥 혈류 예비율(FFR CT) 워크플로우의 급증으로 인해 2024년 가장 큰 점유율을 차지했습니다. 하이브리드 카테터 랩/수술실(Hybrid Catheter Lab/Or Suite)의 급속한 확장은 경피적 카테터 판막 중재술 및 구조적 중재술 중 실시간으로 3D 혈관 재구성을 중첩할 수 있는 기업 뷰어에 대한 수요를 촉진하고 있습니다. AI를 통한 박출률 정량화 및 심실 용적 측정을 위한 새로운 CPT 코드도 병원이 심혈관 분석이 통합된 플랫폼을 개발하도록 동기를 부여하고 있습니다. 또한 웨어러블 ECG와 이식형 디바이스의 데이터 스트림이 급증함에 따라 순환기내과에서는 종합적인 심혈관 위험 계층화를 위해 영상 검사와 다중 소스 신호를 통합하는 기업 솔루션을 채택하고 있습니다.

세계의 기업 이미징 IT 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요한 인사이트

기업 이미징 IT 시장의 개요

북미의 기업 이미징 IT 시장 : 용도별, 지역별

기업 이미징 IT 시장 : 지역적 스냅숏

기업 이미징 IT 시장 : 선진국과 신흥 국가

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향/혼란

산업 동향

AI를 활용한 진단과 예측 분석

통합 영상 데이터 통합과 공동 진단

클라우드 기반 이미징 IT 플랫폼과 디지털 전환

에코시스템 분석

공급망 분석

기술 분석

주요 기술

보완 기술

인접 기술

규제 분석

규제기관, 정부기관, 기타 조직

규제 상황

가격결정 분석

기업 IT 이미징 솔루션의 참고 가격 : 기능별(2024년)

기업 IT 이미징 솔루션의 참고 가격 : 지역별(2024년)

Porter's Five Forces 분석

특허 분석

기업 이미징 IT 시장에서 특허 공보의 동향

인사이트 : 관할과 주요 신청자의 분석

주요 이해관계자와 구입 기준

최종사용자 분석

미충족 요구

최종사용자 기대

2025년 - 주요 컨퍼런스와 이벤트(2026년)

사례 연구 분석

투자와 자금조달 시나리오

비즈니스 모델 분석

기업 이미징 IT 시장에 대한 생성형 AI의 영향

주요 사용 사례와 시장의 장래성

AI/생성형 AI 실장 사례 연구

상호접속된 인접 시장

사용자 준비 상황과 영향의 평가

기업 이미징 IT 시장에 대한 2025년 미국 관세의 영향

서론

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종사용자에 대한 영향

제6장 기업 IT 시장 : 기능별

서론

VNA

PACS

영상 교환

유니버설 뷰어

워크플로우 오케스트레이션

애널리틱스

기타 기능

제7장 기업 이미징 IT 시장 : 용도별

서론

진단

치료

임상 연구

제8장 기업 이미징 IT 시장 : 모달리티별

서론

X선

자기공명영상(MRI)

컴퓨터단층촬영(CT)

초음파

핵이미징

내시경검사

맘모그래피

투시 검사

심장 초음파 검사

기타 모달리티

제9장 기업 이미징 IT 시장 : 제공별

서론

소프트웨어

서비스

제10장 기업 이미징 IT 시장 : 배포 방식별

서론

온프레미스 솔루션

클라우드 기반 솔루션

하이브리드 솔루션

제11장 기업 이미징 IT 시장 : 치료 영역별

서론

신경

순환기

종양

정형외과

기타 치료 영역

제12장 기업 이미징 IT 시장 : 최종사용자별

서론

병원

진단 센터

진료소·외래 진료

제약·바이오테크놀러지 기업

의료 기술 기업

연구·학술기관

기타 최종사용자

제13장 기업 이미징 IT 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시경제 전망

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

일본

인도

기타 아시아태평양

라틴아메리카

라틴아메리카의 거시경제 전망

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타 중동 및 아프리카

제14장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석, 2020년 - 2024년

시장 점유율 분석(2024년)

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

기업의 평가와 재무 지표

브랜드/소프트웨어의 비교

경쟁 시나리오

제15장 기업 개요

주요 기업

AGFA-GEVAERT GROUP

FUJIFILM HOLDINGS CORPORATION

GE HEALTHCARE

KONINKLIJKE PHILIPS N.V.

SIEMENS HEALTHINEERS AG

OPTUM, INC.

SECTRA AB

CANON MEDICAL SYSTEMS CORPORATION

MERATIVE

PRO MEDICUS, LTD.

INTELERAD MEDICAL SYSTEMS INCORPORATED

HYLAND SOFTWARE, INC.

INFINITT HEALTHCARE CO., LTD.

NOVARAD

MACH7 TECHNOLOGIES

HERMES MEDICAL SOLUTIONS

KONICA MINOLTA, INC.

BRIDGEHEAD SOFTWARE LTD.

SCIMAGE, INC.

VISUS HEALTH IT GMBH

기타 기업

DICOM SYSTEMS, INC.

POSTDICOM

QAELUM

ADVAHEALTH SOLUTIONS

PAXERAHEALTH

RAD AI

제16장 부록

KSA

영문 목차

영문목차

The global enterprise imaging IT market is projected to reach USD 4.12 billion by 2030 from USD 2.31 billion in 2025, at a CAGR of 12.2% during the forecast period. Demand is propelled by the shift from capital-heavy license models to cloud native SaaS deployments, which lower upfront costs and accelerate upgrades.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Function, Modality, Application, Offering, Deployment Mode, Therapeutic Area, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and Latin America

The emergence of blockchain-backed image provenance platforms is enhancing data integrity and auditability across multi-vendor ecosystems. Growing medical tourism networks are driving the need for standardized, cross-border image exchange hubs, while the proliferation of point-of-care ultrasound and wearable imaging devices is expanding enterprise workflows to include real-time, bedside acquisitions.

"The diagnostics segment is the fastest-growing segment in the enterprise imaging IT market within the forecast period."

Based on applications, the enterprise imaging IT market has been divided into diagnostics, therapeutics, and clinical research. The diagnostics segment accounts for the largest share of the enterprise imaging IT market. This segment's large share and high growth can be attributed to the nationwide rollout of lung cancer screening programs, which has surged low-dose CT volumes and driven enterprise archive demand. The integration of AI-driven triage engines that automatically flag critical findings such as intracranial hemorrhages or pulmonary emboli has also pushed providers to upgrade diagnostic platforms. Additionally, the rise of quantitative radiomics and texture analysis workflows for oncology and neurology imaging is creating demand for solutions that can store, process, and mine high-dimensional feature sets at scale.

"The cardiology segment is estimated to hold the largest share of the enterprise imaging IT market in 2024, by therapeutic area."

Based on therapeutic area, the enterprise imaging IT market is segmented into neurology, cardiology, oncology, orthopedics, and other therapeutic areas. The cardiology segment held the largest share in 2024 due to the surge in CT-derived fractional flow reserve (FFR CT) workflows, which require seamless integration of computational models and high-fidelity CT archives. The rapid expansion of hybrid cath lab/OR suites is driving the demand for enterprise viewers that can overlay 3D vessel reconstructions in real time during transcatheter valve and structural interventions. New CPT codes for AI-quantified ejection fraction and chamber volumetrics are also incentivizing hospitals to deploy platforms with built-in cardiac analytics. Additionally, the proliferation of wearable ECG and implantable device data streams is pushing cardiology departments to adopt enterprise solutions that fuse multi source signals with imaging studies for comprehensive cardiac risk stratification.

"The Asia Pacific region is expected to register the highest growth rate in the enterprise imaging IT market during the forecast period."

The global enterprise imaging IT market is segmented into five major regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, Asia Pacific is expected to register the highest growth for enterprise imaging IT in the forecast period. Factors such as India's National Digital Health Mission integrating imaging data into its Health Locker for unified patient records, the rise of medical tourism hubs in Malaysia and Thailand demanding seamless cross border image exchange, public-private partnerships deploying mobile CT and MRI units in rural China, and the explosive uptake of low cost, AI powered handheld ultrasound devices in South Korea and India are all fueling Asia Pacific's rapid enterprise imaging IT adoption.

The breakdown of primary participants is as mentioned below:

By Company Type: Tier 1 (41%), Tier 2 (31%), and Tier 3 (28%)

By Designation: C-level Executives (44%), Directors (31%), and Others (25%)

By Region: North America (45%), Europe (28%), Asia Pacific (20%), Latin America (4%), and the Middle East & Africa (3%)

Key Players

The prominent players in this market are Agfa-Gevaert Group (Belgium), FUJIFILM Corporation (Japan), Merative (US), Pro Medicus, Ltd. (Australia), Optum, Inc. (US), GE HealthCare (US), Intelerad (Canada), Sectra AB (Sweden), CANON MEDICAL SYSTEMS CORPORATION (Japan), Hyland Software, Inc. (US), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), INFINITT Healthcare Co., Ltd. (South Korea), Novarad (US), Mach7 Technologies (US), Hermes Medical Solutions (Sweden), Konica Minolta, Inc. (Japan), BridgeHead Software Ltd. (England), Sclmage, Inc. (US), VISUS Health IT GmbH (Germany), Dicom Systems, Inc. (US), PostDICOM (Netherlands), Qaelum (Belgium), AdvaHealth Solutions (Singapore), PaxeraHealth (US), and Rad AI (US). Players adopted organic and inorganic growth strategies such as solution launches, enhancements, and upgrades; collaborations; partnerships; acquisitions; agreements; and expansions to increase their offerings, cater to customers' unmet needs, increase their profitability, and expand their presence in the global market.

Research Coverage

The report studies the enterprise imaging IT market based on function, modality, application, offering, deployment mode, therapeutic area, end user, and region.

The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

The report studies micromarkets with respect to their growth trends, prospects, and contributions to the total enterprise imaging IT market.

The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

The report can help established firms, as well as new entrants/smaller firms, gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the five strategies mentioned below.

This report provides insights into the following pointers:

Analysis of key drivers, restraints, opportunities, and challenges influencing the growth of the enterprise imaging IT market.

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the enterprise imaging IT market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of enterprise imaging IT solutions across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the enterprise imaging IT market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the enterprise imaging IT market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY

1.6 LIMITATIONS

1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakdown of primary sources

2.2 RESEARCH APPROACH

2.3 MARKET SIZE ESTIMATION

2.4 MARKET BREAKDOWN & DATA TRIANGULATION

2.5 RESEARCH ASSUMPTIONS

2.5.1 MARKET SIZING ASSUMPTIONS

2.5.2 OVERALL STUDY ASSUMPTIONS

2.6 RISK ASSESSMENT

2.7 RESEARCH LIMITATIONS

2.7.1 METHODOLOGY-RELATED LIMITATIONS

2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ENTERPRISE IMAGING IT MARKET OVERVIEW

4.2 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION & REGION

4.3 ENTERPRISE IMAGING IT MARKET: GEOGRAPHIC SNAPSHOT

4.4 ENTERPRISE IMAGING IT MARKET: DEVELOPED VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increased demand for scalable and cost-effective solutions

5.2.1.2 Advancements in AI and imaging technologies

5.2.1.3 Growing volume of medical imaging procedures

5.2.1.4 Growing need for remote access and collaborative care

5.2.1.5 Government initiatives and favorable policies

5.2.2 RESTRAINTS

5.2.2.1 Data security and privacy concerns

5.2.2.2 Lack of skilled professionals for deployment and interpretation

5.2.3 OPPORTUNITIES

5.2.3.1 Expansion into emerging markets

5.2.3.2 Multi modality and advanced visualization

5.2.3.3 Partnerships with AI and analytics providers

5.2.3.4 Value-based care and population health management

5.2.3.5 Cloud native and edge computing innovations

5.2.4 CHALLENGES

5.2.4.1 Interoperability with legacy and vendor-specific systems

5.2.4.2 High upfront integration and deployment costs

5.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, & OTHER ORGANIZATIONS

5.8.2 REGULATORY LANDSCAPE

5.8.2.1 North America

5.8.2.2 Europe

5.8.2.3 Asia Pacific

5.8.2.4 Latin America

5.8.2.5 Middle East & Africa

5.9 PRICING ANALYSIS

5.9.1 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY FUNCTION (2024)

5.9.2 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY REGION (2024)

5.10 PORTER'S FIVE FORCES ANALYSIS

5.10.1 BARGAINING POWER OF SUPPLIERS

5.10.2 BARGAINING POWER OF BUYERS

5.10.3 THREAT OF SUBSTITUTES

5.10.4 THREAT OF NEW ENTRANTS

5.10.5 INTENSITY OF COMPETITIVE RIVALRY

5.11 PATENT ANALYSIS

5.11.1 PATENT PUBLICATION TRENDS FOR ENTERPRISE IMAGING IT MARKET

5.11.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

5.12 KEY STAKEHOLDERS & BUYING CRITERIA

5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.12.2 BUYING CRITERIA

5.13 END-USER ANALYSIS

5.13.1 UNMET NEEDS

5.13.2 END-USER EXPECTATIONS

5.14 KEY CONFERENCES & EVENTS, 2025-2026

5.15 CASE STUDY ANALYSIS

5.16 INVESTMENT & FUNDING SCENARIO

5.17 BUSINESS MODEL ANALYSIS

5.18 IMPACT OF GENERATIVE AI ON ENTERPRISE IMAGING IT MARKET

5.18.1 TOP USE CASES & MARKET POTENTIAL

5.18.1.1 Key use cases

5.18.2 CASE STUDIES OF AI/GENERATIVE AI IMPLEMENTATION

5.18.2.1 Case Study 1: Enabling interoperability and scalability across enterprise imaging networks with Dicom Systems' Unifier Platform

5.18.2.2 Case Study 2: More images, more insight, more collaboration - San Gerardo Hospital transforms radiology with Agfa HealthCare's Enterprise Imaging