Valve Positioner Market by Type (Pneumatic Positioners, Electro-pneumatic Positioners, Digital Positioners), Actuation (Single Acting Positioners, Double Acting Positioners), Industry (Oil & Gas, Energy & Power) and Region - Global Forecast to 2030

상품코드:1795417

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 218 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

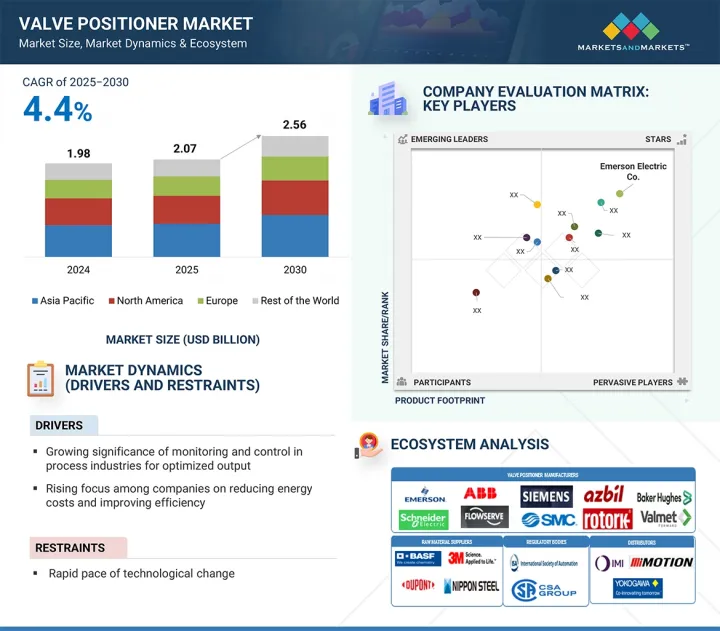

세계의 밸브 포지셔너 시장 규모는 4.4%의 연평균 복합 성장률(CAGR)로 확대되고 2025년 20억 7,000만 달러에서 2030년까지 25억 6,000만 달러로 성장할 것으로 예측됩니다.

성장의 원동력이 되는 것은 정밀 제어, 흐름 프로세스의 자동화, 산업 운영 전체의 지능형 밸브 관리로의 시프트에 대한 요구 증가입니다. 산업계는 공정의 응답성을 최적화하고, 밸브와 관련된 고장을 줄이고, 엄격한 품질 기준을 충족시키는 것을 목표로 하므로, 밸브 포지셔너는 변동하는 작동 조건 하에서 일관된 성능을 달성하기 위한 중요한 구성 요소가 되었습니다. 금속 및 광업, 화학 처리, 제약, 발전 등의 업계에서는 압력에 민감하고 미션 크리티컬한 용도를 확실히 제어하기 위해 첨단 밸브 포지셔너의 사용을 확대하고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

작동형별, 업계별, 유형별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

게다가 배치가 변경되고 흐름이 변화하는 제조 환경에서는 처리량을 향상시키고 낭비를 줄이기 위해 포지셔너가 채택됩니다. 스마트 계측 네트워크, 상태 모니터링 시스템, 플랜트 제어 아키텍처와의 통합은 운영 유연성을 높이고 수동 개입을 줄입니다. 적응 제어, 원격 성능 최적화, 라이프사이클 효율화에 대한 수요가 높아짐에 따라 밸브 포지셔너는 세계 섹터에서 차세대 산업 자동화 전략을 가능하게 하는 역할을 할 것으로 예측됩니다.

밸브 포지셔너 시장은 안전성, 신뢰성, 에너지 효율을 우선시하는 중요한 공정 산업에서의 채택이 확대됨에 따라 단동식 부문이 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예측됩니다. 석유 및 가스, 물 및 폐수 처리, 화학 처리 등의 업계에서는 페일 세이프 기능(공기에 이상이 발생했을 경우에 밸브를 지정한 위치(개 또는 폐)에 자동적으로 되돌리는 기능)에 의해 단동식 액추에이터를 선택하는 케이스가 증가하고 있습니다. 이 기능은 작동 안전을 보장하고 위험한 환경에서 위험을 최소화할 수 있습니다. 디지털 밸브 포지셔너와 단동 액추에이터의 통합은 정밀 제어, 실시간 진단 및 예측 유지보수를 가능하게 하며 이 부문의 이점을 더욱 강화합니다. 이러한 장점은 시스템 성능을 향상시킬 뿐만 아니라 가동 중지 시간과 유지 보수 비용을 절감합니다. 또한 단동식 액추에이터는 공기 소비가 적고 설치가 쉽기 때문에 단순성과 신뢰성이 필수적인 원격지 및 위험한 장소에 적합합니다. 산업계가 업무의 합리화를 도모하고 지속가능성의 목표를 따르는 것을 목표로 하고 있는 가운데, 단동 액추에이터는 컴플라이언스와 업무 연속성을 지원하는 견고하고 비용 효율적인 솔루션을 제공하여 시장에서의 주도적 지위를 강화하고 있습니다.

에너지 및 전력 섹터는 발전·배전에 있어서의 효율적인 유량 제어와 시스템 신뢰성의 향상에 대한 수요 증가에 힘입어 2024년의 밸브 포지셔너 시장에서 2위의 점유율을 확보했습니다. 세계 에너지 소비가 증가하고 전력망이 복잡해짐에 따라 전력 회사는 화력, 원자력, 재생에너지 발전소의 증기, 가스 및 냉각 시스템의 제어를 최적화하기 위해 고급 밸브 포지셔너를 도입하는 경우가 늘고 있습니다. 최신 전력 시설은 보다 긴밀한 제어 루프를 가능하게 하고, 장비에 대한 기계적 스트레스를 줄이고, 부하 관리를 개선하기 위해 스마트 밸브 포지셔너를 채택하고 있습니다. 바이오매스, 태양열, 지열과 같은 재생에너지원으로의 전환은 정확한 유량 조절의 필요성을 더욱 강화하고 밸브 포지셔너를 공정의 안정성과 효율성을 보장하는 중요한 구성 요소로 만듭니다. 또한, 노후화된 전력 인프라를 업그레이드하고 새로운 발전 능력을 추가하기 위한 지속적인 노력이 전 세계적으로 진행되고 있는 것도 이러한 솔루션의 채용을 뒷받침하고 있습니다. 밸브 포지셔너는 또한 배기 가스 규제를 지원하고 엄격한 에너지 효율 규제를 충족시키는 데 도움이 되며, 진화하는 에너지 상황에서 필수적인 기술로서의 역할을 강화하고 있습니다.

아시아태평양은 밸브 포지셔너 시장에서 가장 급성장하는 지역이며, 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이 급성장의 배경에는 산업화 확대, 인프라 개발, 석유 및 가스, 화학, 상하수도처리, 발전 등 주요 부문에서의 자동화 기술의 채용 확대가 있습니다. 중국, 인도, 한국, 동남아시아 국가 등의 국가들은 생산성을 높이고 국내 및 수출 수요 증가에 대응하기 위해 제조업과 공정산업의 근대화에 많은 투자를 하고 있습니다. 이 지역에서는 Industry 4.0과 스마트 매뉴팩처링을 추진하고 있으며, 정밀 제어, 원격 진단, 시스템 통합 등의 이점을 제공하는 디지털 밸브 포지셔너의 도입이 가속화되고 있습니다. 또한 청정 에너지, 효율적인 물 관리, 산업 자동화를 지원하는 정부의 이니셔티브가 시장 확대에 유리한 환경을 만들어 왔습니다. 노후화된 인프라를 업그레이드하고 보다 엄격한 환경 규제를 충족시킬 필요성이 첨단 밸브 제어 솔루션에 대한 수요를 더욱 촉진하고 있습니다. 에너지 효율, 지속가능성, 운전 신뢰성에 대한 주목이 높아지는 가운데, 아시아태평양은 밸브 포지셔너 채용의 중요한 거점으로 부상하고 있으며, 가장 역동적이고 빠르게 발전하고 있는 지역 시장으로서의 지위를 견인하고 있습니다.

본 보고서에서는 세계 밸브 포지셔너 시장에 대해 조사했으며, 작동형별, 업계별, 유형별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

밸류체인 분석

생태계 분석

가격 분석

고객사업에 영향을 주는 동향/혼란

기술 분석

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

사례 연구

무역 분석

특허 분석

2025-2026년의 주된 회의와 이벤트

기준과 규제

AI 및 생성형 AI가 밸브 포지셔너 시장에 미치는 영향

2025년 미국 관세가 밸브 포지셔너 시장에 미치는 영향

제6장 밸브 포지셔너 시장(작동형별)

소개

단동식

복동식

제7장 밸브 포지셔너 시장(업계별)

소개

석유 및 가스

물 및 폐수 처리

에너지 및 전력

화학약품

종이 및 펄프

의약품

금속 및 광업

식음료

기타

제8장 밸브 포지셔너 시장(유형별)

소개

공압 포지셔너

전공 포지셔너

디지털 포지셔너

제9장 밸브 포지셔너 시장(지역별)

소개

북미

미국

캐나다

멕시코

유럽

영국

독일

프랑스

기타

아시아태평양

중국

일본

인도

기타

기타 지역

중동 및 아프리카

남미

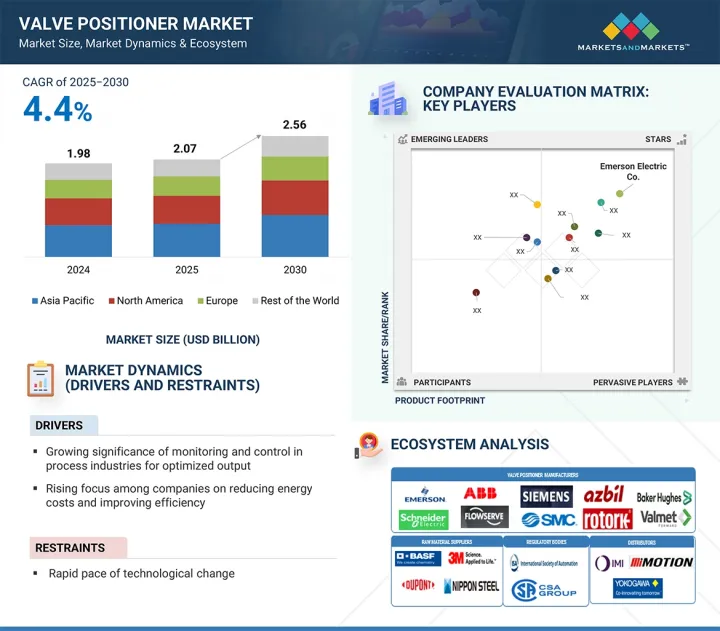

제10장 경쟁 구도

개요

주요 참가 기업의 전략/강점, 2023-2025년

수익 분석, 2020-2024년

시장 점유율 분석, 2024년

경쟁평가 매트릭스 : 주요 진입기업 평가, 2024년

경쟁평가 매트릭스 : 스타트업/중소기업 평가, 2024년

경쟁 시나리오

제11장 기업 프로파일

주요 진출기업

EMERSON ELECTRIC CO.

ABB

FLOWSERVE CORPORATION

SIEMENS

SCHNEIDER ELECTRIC

SMC CORPORATION

AZBIL CORPORATION

BAKER HUGHES

ROTORK PLC

VALMET

기타 기업

SAMSONCONTROLS.NET.

VRG CONTROLS, LLC

FESTO SE & CO. KG(FESTO)

BADGER METER, INC.

CONTROLAIR

CRANE COMPANY

CHRISTIAN BURKERT GMBH & CO. KG

GEMU GROUP

DWYER INSTRUMENTS LTD

VRC

POWER-GENEX LTD.

VAL CONTROLS

BRAY INTERNATIONAL

NIHON KOSO CO., LTD.

SPIRAX SARCO LIMITED

제12장 부록

JHS

영문 목차

영문목차

With a CAGR of 4.4%, the global valve positioner market is projected to grow from USD 2.07 billion in 2025 to USD 2.56 billion by 2030. Growth is expected to be driven by the increasing need for precision control, automation of flow processes, and the shift toward intelligent valve management across industrial operations. As industries aim to optimize process responsiveness, reduce valve-related failures, and meet stringent quality standards, valve positioners are becoming critical components in achieving consistent performance under variable operating conditions. Industries such as metals and mining, chemical processing, pharmaceuticals, and power generation are expanding the use of advanced valve positioners to ensure tight control in pressure-sensitive and mission-critical applications.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Type, Actuation, Industry, and Region

Regions covered

North America, Europe, APAC, RoW

Additionally, manufacturing environments with frequent batch changes and variable flows adopt positioners to improve throughput and reduce waste. Integration with smart instrumentation networks, condition monitoring systems, and plant control architectures enhances operational flexibility and reduces manual intervention. As the demand for adaptive control, remote performance optimization, and lifecycle efficiency increases, valve positioners are expected to play a growing role in enabling next-generation industrial automation strategies across global sectors.

By actuation type, the single-acting segment is expected to hold the largest market share during the forecast period.

The single-acting actuation segment is projected to hold the largest share of the valve positioner market during the forecast period, driven by its growing adoption in critical process industries that prioritize safety, reliability, and energy efficiency. Industries such as oil & gas, water & wastewater treatment, and chemical processing are increasingly selecting single-acting actuators due to their fail-safe capability-automatically returning the valve to a predetermined position (open or closed) in the event of air failure. This functionality ensures operational security and minimizes risks in high-stakes environments. The integration of digital valve positioners with single-acting actuators is further strengthening the segment's dominance, enabling precise control, real-time diagnostics, and predictive maintenance. These benefits not only enhance system performance but also reduce downtime and maintenance costs. Moreover, single-acting actuators consume less air and are easier to install, making them well-suited for remote or hazardous locations where simplicity and reliability are essential. As industries aim to streamline operations and align with sustainability goals, single-acting actuation offers a robust, cost-effective solution that supports compliance and operational continuity, reinforcing its leading position in the market.

Industry

By industry, the energy and power sector is likely to hold the second-largest market share during the forecast period.

The energy and power sector secured the second-largest share in the valve positioner market during 2024, supported by the growing demand for efficient flow control and enhanced system reliability in power generation and distribution. As global energy consumption rises and power grids become more complex, utilities are increasingly implementing advanced valve positioners to optimize control over steam, gas, and cooling systems in thermal, nuclear, and renewable energy plants. Modern power facilities are adopting smart valve positioners to enable tighter control loops, reduce mechanical stress on equipment, and improve load management. The transition toward renewable energy sources-such as biomass, solar thermal, and geothermal-further strengthens the need for accurate flow regulation, making valve positioners a critical component in ensuring process stability and efficiency. Moreover, ongoing efforts to upgrade aging power infrastructure and add new generation capacity worldwide are driving the adoption of these solutions. Valve positioners also support emission control and help meet stringent energy efficiency regulations, reinforcing their role as an essential technology in the evolving energy landscape..

By Region, Asia Pacific is projected to be the fastest-growing market during the forecast period.

Asia Pacific is projected to be the fastest-growing region in the valve positioner market, registering the highest CAGR during the forecast period. This rapid growth is driven by expanding industrialization, infrastructure development, and increasing adoption of automation technologies across key sectors such as oil & gas, chemicals, water and wastewater treatment, and power generation. Countries like China, India, South Korea, and Southeast Asian nations are making significant investments in modernizing their manufacturing and process industries to enhance productivity and meet rising domestic and export demands. The region's push toward Industry 4.0 and smart manufacturing is accelerating the deployment of digital valve positioners, which offer benefits such as precise control, remote diagnostics, and system integration. Moreover, government initiatives supporting clean energy, efficient water management, and industrial automation are creating a favorable environment for market expansion. The need to upgrade aging infrastructure and meet stricter environmental regulations further fuels demand for advanced valve control solutions. With growing focus on energy efficiency, sustainability, and operational reliability, the Asia Pacific is emerging as a key hub for valve positioner adoption, driving its position as the most dynamic and rapidly advancing regional market..

Breakdown of primaries

A variety of executives from key organizations operating in the valve positioner market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

By Designation: Directors - 45%, C-level - 30%, and Others - 25%

By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

Note: Other designations include sales and product managers and project engineers. The three tiers of the companies are defined based on their total revenue in 2024: Tier 1 - revenue greater than or equal to USD 1 billion; Tier 2 - revenue between USD 100 million and USD 1 billion; and Tier 3 revenue less than or equal to USD 100 million.

Major players profiled in this report are as follows:

Emerson Electric Co. (US), Siemens (Germany), ABB (Switzerland), Flowserve Corporation (US), Schneider Electric (France), SMC Corporation (Japan), Azbil Corporation (Japan), Baker Hughes (US), Rotork plc (UK), Valmet (Finland), samsoncontrols.net. (Germany), VRG Controls, LLC (US), Festo SE & Co. KG (Festo) (Germany), Badger Meter, Inc. (US), ControlAir (US), Crane Company (US), Christian Burkert GmbH & Co. KG (Germany), GEMU Group (Germany), Dwyer Instruments, LLC (US), VRC (US), POWER GENEX (South Korea), Val Controls (Denmark), Bray International (US), NIHON KOSO CO., LTD. (Japan), Spirax Sarco Limited (UK).

The study provides a detailed competitive analysis of these key players in the valve positioner market, presenting their company profiles, most recent developments, and key market strategies.

Study Coverage

In this report, the valve positioner market has been segmented based on type, actuation, industry, and region. The type segment includes digital, electro-pneumatic, and pneumatic. The actuation segment comprises single-acting and double-acting. The industry segment comprises oil & gas, energy & power, water & wastewater treatment, food & beverages, metals & mining, chemicals, pharmaceuticals, pulp & paper, and other industries. The market has been segmented into four regions - North America, Asia Pacific, Europe, and Rest of the World (RoW).

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the valve positioner market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

Analysis of key drivers (growing significance of monitoring and control in process industries for optimized output, valve positioners are helping industries cut energy costs and improve efficiency as global energy demand continues to rise, rising adoption of smart valve positioners in various plant operations), restraints (fast-changing technology are slowing the adoption of valve positioners), opportunities (increasing focus on remote operations and decentralized plants, focus of industry players on offering improved customer service), and challenges (positioner overshoot and oversized valves hinder operation of control valves) influencing the growth of the valve positioner market.

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the valve positioner market.

Market Development: Comprehensive information about lucrative markets - the report analyses the valve positioner market across varied regions.

Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the valve positioner market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Emerson Electric Co. (US), ABB (Switzerland), Siemens (Germany), Flowserve Corporation (US), Schneider Electric (France), and others.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of key primary interview participants

2.1.3.2 Breakdown of primaries

2.1.3.3 Key data from primary sources

2.1.3.4 Key industry insights

2.2 MARKET SIZE ESTIMATION METHODOLOGY

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR KEY PLAYERS IN VALVE POSITIONER MARKET

4.2 VALVE POSITIONER MARKET, BY TYPE

4.3 VALVE POSITIONER MARKET, BY ACTUATION

4.4 VALVE POSITIONER MARKET, BY INDUSTRY

4.5 VALVE POSITIONER MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing significance of monitoring and control in process industries for optimized output

5.2.1.2 Increasing pressure to cut costs and operate more efficiently

5.2.1.3 Seamless integration with advanced control systems

5.2.2 RESTRAINTS

5.2.2.1 Rapid changes in industrial automation technologies

5.2.3 OPPORTUNITIES

5.2.3.1 Shift toward remote operations and decentralized facilities

5.2.3.2 Unlocking automation with self-powered valve positioners in remote sites

5.2.4 CHALLENGES

5.2.4.1 Challenges associated with oversized control valves and positioner overshoot

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF DIFFERENT TYPES OF VALVE POSITIONERS, BY KEY PLAYER, 2024

5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Digital communication protocols

5.7.1.2 Position feedback sensors

5.7.2 ADJACENT TECHNOLOGIES

5.7.2.1 SCADA

5.7.3 COMPLEMENTARY TECHNOLOGIES

5.7.3.1 Digital twin

5.8 PORTER'S FIVE FORCES ANALYSIS

5.8.1 THREAT OF NEW ENTRANTS

5.8.2 THREAT OF SUBSTITUTES

5.8.3 BARGAINING POWER OF SUPPLIERS

5.8.4 BARGAINING POWER OF BUYERS

5.8.5 INTENSITY OF COMPETITIVE RIVALRY

5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.9.2 BUYING CRITERIA

5.10 CASE STUDIES

5.11 TRADE ANALYSIS

5.11.1 IMPORT DATA (HS CODE 8481)

5.11.2 EXPORT DATA (HS CODE 8481)

5.12 PATENT ANALYSIS

5.13 KEY CONFERENCES AND EVENTS, 2025-2026

5.14 STANDARDS AND REGULATIONS

5.14.1 STANDARDS

5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15 IMPACT OF AI/GENERATIVE AI ON VALVE POSITIONER MARKET

5.15.1 INTRODUCTION

5.15.2 IMPACT OF AI ON VALVE POSITIONER MARKET

5.15.3 TOP USE CASES AND MARKET POTENTIAL

5.16 IMPACT OF 2025 US TARIFF ON VALVE POSITIONER MARKET

5.16.1 INTRODUCTION

5.16.2 KEY TARIFF RATES

5.16.3 PRICE IMPACT ANALYSIS

5.16.4 IMPACT ON COUNTRY/REGION

5.16.4.1 US

5.16.4.2 Europe

5.16.4.3 Asia Pacific

5.16.5 IMPACT ON INDUSTRIES

6 VALVE POSITIONER MARKET, BY ACTUATION

6.1 INTRODUCTION

6.2 SINGLE-ACTING

6.2.1 EASY WORKING MECHANISM TO FUEL MARKET GROWTH

6.3 DOUBLE-ACTING

6.3.1 GROWING DEMAND FOR COMPACT-SIZE VALVES TO DRIVE MARKET

7 VALVE POSITIONER MARKET, BY INDUSTRY

7.1 INTRODUCTION

7.2 OIL & GAS

7.2.1 EMPHASIS ON REDUCING OPERATIONAL COSTS AND ENHANCE EFFICIENCY OF PLANTS TO DRIVE MARKET

7.3 WATER & WASTEWATER TREATMENT

7.3.1 RISING DEMAND FOR EFFECTIVE WATER MANAGEMENT ACROSS ENERGY AND URBAN INFRASTRUCTURE SECTORS TO FUEL MARKET GROWTH

7.4 ENERGY & POWER

7.4.1 INCREASING INVESTMENTS IN ENERGY SECTORS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

7.5 CHEMICALS

7.5.1 RISING FOCUS ON BOOSTING CHEMICAL PLANT SAFETY TO FUEL MARKET GROWTH

7.6 PAPER & PULP

7.6.1 ADOPTION OF DIGITALIZED PROCESSES TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

7.7 PHARMACEUTICALS

7.7.1 STRINGENT REGULATORY GUIDELINES AND INCREASING COMPLEXITIES IN PRODUCT LINES TO BOOST DEMAND

7.8 METALS & MINING

7.8.1 INCREASING PRESSURE TO OPTIMIZE PROCESSES AND REDUCE UNPLANNED DOWNTIME TO SUPPORT MARKET GROWTH

7.9 FOOD & BEVERAGES

7.9.1 RISING SUSTAINABLE INTENSIFICATION OF AGRICULTURE TO BOOST PRODUCTIVITY TO FUEL MARKET GROWTH

7.10 OTHER INDUSTRIES

8 VALVE POSITIONER MARKET, BY TYPE

8.1 INTRODUCTION

8.2 PNEUMATIC POSITIONERS

8.2.1 ABILITY TO WORK EFFICIENTLY IN ADVERSE ENVIRONMENTAL CONDITIONS TO BOOST DEMAND

8.3 ELECTRO-PNEUMATIC POSITIONERS

8.3.1 ABILITY TO OFFER SOLUTIONS WITHOUT SIGNIFICANT INFRASTRUCTURE OR WORKFORCE TRAINING UPGRADES TO FUEL MARKET GROWTH

8.4 DIGITAL POSITIONERS

8.4.1 RISING DEMAND FOR AUTOMATED AND DATA-DRIVEN PLANT OPERATIONS TO FOSTER MARKET GROWTH

9 VALVE POSITIONER MARKET, BY REGION

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 US

9.2.1.1 Growing investment in automation technologies to drive market

9.2.2 CANADA

9.2.2.1 Emphasis on improving water and wastewater infrastructure to foster market growth

9.2.3 MEXICO

9.2.3.1 Focus on expanding electricity generation, transmission, and distribution infrastructure to support market growth

9.3 EUROPE

9.3.1 UK

9.3.1.1 Rising focus digital automation to offer lucrative growth opportunities

9.3.2 GERMANY

9.3.2.1 Development of national hydrogen core network to foster market growth

9.3.3 FRANCE

9.3.3.1 Increasing demand for precision control technologies across energy sector to fuel market growth

9.3.4 REST OF EUROPE

9.4 ASIA PACIFIC

9.4.1 CHINA

9.4.1.1 Emphasis on industrial modernization to boost demand

9.4.2 JAPAN

9.4.2.1 Need to optimize flow regulation and pressure control in fuel-based power plants to support market growth

9.4.3 INDIA

9.4.3.1 Government-led initiatives to boost adoption of automation components to fuel market growth

9.4.4 REST OF ASIA PACIFIC

9.5 ROW

9.5.1 MIDDLE EAST & AFRICA

9.5.1.1 GCC

9.5.1.1.1 Adoption of Industry 4.0 technologies to offer lucrative growth opportunities

9.5.1.2 Africa & Rest of Middle East

9.5.2 SOUTH AMERICA

9.5.2.1 Brazil

9.5.2.1.1 Expanding public utilities and improving service reliability to support market growth

9.5.2.2 Rest of South America

10 COMPETITIVE LANDSCAPE

10.1 OVERVIEW

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2025

10.3 REVENUE ANALYSIS, 2020-2024

10.4 MARKET SHARE ANALYSIS, 2024

10.5 COMPETITIVE EVALUATION MATRIX, 2024

10.5.1 STARS

10.5.2 EMERGING LEADERS

10.5.3 PERVASIVE PLAYERS

10.5.4 PARTICIPANTS

10.5.5 VALVE POSITIONER MARKET: COMPANY FOOTPRINT

10.5.5.1 Company footprint

10.5.5.2 Region footprint

10.5.5.3 Type footprint

10.5.5.4 Industry footprint

10.6 COMPANY EVALUAITON MATRIX: STARTUPS/SMES EVALUATION, 2024