Defibrillator Market by Product (Implantable Cardioverter Defibrillator, External Defibrillator (Automated Defibrillator, Wearable Defibrillator, Manual Defibrillator)), End User (Hospitals & Clinics, Cardiac Centers, Homecare) - Global Forecast to 2030

상품코드:1794019

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 296 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

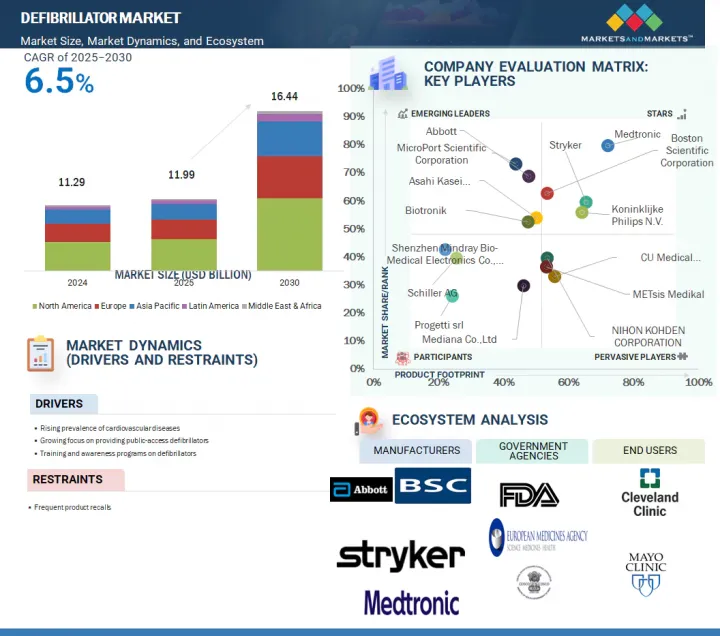

세계 제세동기 시장 규모는 2025년 119억 9,000만 달러, 2030년에는 164억 4,000만 달러에 이르고, 예측 기간 중 CAGR은 6.5%를 나타낼 것으로 보입니다.

조사 범위

대상 연도

2024-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

제품별, 환자 유형별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

제세동기 시장의 성장을 견인하고 있는 것은 심혈관 질환 인구의 비율 증가, 제세동기의 기술적 진보, 무료 교육 및 프로그램 제공, 공공 액세스 제세동기(PAD) 도입 강화에 대한 공공기관과 민간단체의 이니셔티브 증가입니다. 그러나 내장형 제세동기 및 자동 체외식 제세동기와 관련된 문제와 제품의 빈번한 리콜은 시장 성장을 방해합니다.

제세동기 시장은 제품에 의해 내장형 제세동기(ICD)와 체외식 제세동기로 대별됩니다. ICD는 또한 경정맥 이식 제세동기와 피하 이식 제세동기로 구분되며, 체외식 제세동기는 수동 AED, 자동 AED, 웨어러블 제세동기로 나뉩니다. 2024년 세계 제세동기 시장에서 가장 큰 점유율을 차지했습니다. 임베디드 제세동기의 기술적 진보, 피하형 ICD의 장점에 관한 순환기 전문의의 인식 향상, 기술적으로 선진적인 ICD의 발매 등이 배경에 있습니다.

제세동기 시장은 환자 유형에 따라 성인 환자와 소아 환자로 구분됩니다. 2024년 세계 제세동기 시장은 성인 환자 부문이 지배적이었습니다. 성인 인구에서 심혈관 질환의 이환율 증가, 갑작스런 심정지에 매우 취약한 노인 인구의 급증, 성인 환자에게 ICD의 이식 횟수가 증가하면 이 부문의 성장이 촉진될 가능성이 높습니다.

지역별로 보면 제세동기 세계 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동, 아프리카로 분류됩니다. 북미는 예측 기간 동안 높은 시장 점유율이 예상됩니다. 이는 진보된 제세동기의 채택이 증가하고 있는 것, 심정지 환자에게 필요한 케어를 제공하기 위한 정부의 이니셔티브가 증가하고 있는 것, 시장 진출기업의 발판이 견고하다는 것, 유리한 상환 프로그램, 관상동맥 질환의 발생률 증가 등의 요인에 의한 것입니다.

본 보고서에서는 세계 제세동기 시장에 대해 조사했으며, 제품별, 환자 유형별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

The global defibrillator market is expected to reach USD 16.44 billion by 2030 from USD 11.99 billion in 2025, at a CAGR of 6.5% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, Patient Type, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

The growth in the defibrillator market is driven by the increasing proportion of the population with cardiovascular diseases, technological advancements in defibrillators, and rising initiatives by public and private organizations to provide free training and programs, as well as enhance the implementation of public access defibrillators (PADs). However, issues related to implantable and automated external defibrillators and frequent product recalls have impeded market growth.

The implantable cardioverter defibrillators segment accounted for the largest share of the global market in 2024.

Based on product, the defibrillator market is broadly segmented into implantable cardioverter defibrillators (ICDs) and external defibrillators. ICDs are further divided into transvenous implantable cardioverter defibrillators and subcutaneous implantable cardioverter defibrillators, whereas external defibrillators are divided into manual AEDs, automated AEDs, and wearable defibrillators. The ICDs segment accounted for the largest global defibrillator market share in 2024. Technological advancements in implantable defibrillators, rising awareness among cardiologists about the benefits pertaining to subcutaneous ICDs, and the launch of technologically advanced ICDs.

The adult segment dominated the defibrillator market based on the patient type in 2024.

The defibrillator market is segmented into adult and pediatric patients based on patient type. The adult patients segment dominated the global defibrillator market in 2024. The increasing incidence of cardiovascular disease in the adult population, rapid growth in the geriatric population, which is highly susceptible to sudden cardiac arrest, and the increasing number of implantations of ICDs in adult patients are likely to fuel the growth of the segment.

North America is expected to account for the highest market share in the defibrillator market during the forecast period.

Based on the region, the global defibrillator market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America is expected to witness a high market share during the forecast period. This can be attributed to factors such as the rising adoption of advanced defibrillators, increasing efforts by governments to provide the necessary care to cardiac arrest patients, the strong foothold of market players, favorable reimbursement programs, and an increase in the incidence of coronary artery diseases.

Breakdown of supply-side primary interviews by company type, designation, and region:

By Company Type: Tier 1 (45%), Tier 2 (20%), and Tier 3 (35%)

By Designation: C Level (35%), Director Level (25%), and Others (40%)

By Region: North America (40%), Asia Pacific (25%), Europe (20%), Latin America (10%), and Middle East & Africa (5%)

Prominent companies include Medtronic (Ireland), Stryker (US), Koninklijke Philips N.V. (Netherlands), Asahi Kasei Corporation (Japan), Boston Scientific Corporation (US), Abbott (US), MicroPort Scientific Corporation (China), Nihon Kohden Corporation (Japan), Biotronik (Germany), and CU Medical Systems, Inc. (South Korea).

Research Coverage

This research report categorizes the defibrillator market by Product {Implantable cardioverter defibrillators [Transvenous implantable cardioverter defibrillators (Biventricular ICDS/cardiac resynchronization therapy defibrillators, dual-chamber ICDS, and single-chamber ICDS)], Subcutaneous implantable cardioverter defibrillators) External defibrillators [Manual External defibrillators, Automated external defibrillators (semi-automated external defibrillators, fully automated external defibrillators)], Wearable cardioverter defibrillators}, Patient type (Adult, Pediatric), End Users (Hospitals & Clinics, Cardiac centers, Prehospital settings, Public access markets, Home care settings, and Other end users), and region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the defibrillators market. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, and key market strategies.

Reasons to Buy the Report

The report will help established firms, new entrants, and smaller firms gauge the pulse of the market, which in turn would help them gain a more significant share of the market. Firms purchasing the report could use one or any combination of the strategies mentioned below to strengthen their position in the market.

This report provides insights into the following pointers:

Analysis of key drivers (rising prevalence of cardiovascular disease, increase in geriatric patient population, a strong focus of government to boost the installation of public access defibrillators, rising defibrillators training & programs, and expanding healthcare infrastructure), restraints (frequent product recalls, issues related to implantable and automated external defibrillators), opportunities (emerging countries, ongoing developments in ICDs/CRT-Ds, mergers and acquisitions among market players), and challenges (frequent product recalls and lack of awareness about the cardiac arrest in emerging countries) influencing the growth of the defibrillators market

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the defibrillator market

Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product launches in the defibrillator market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the defibrillator market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY RESEARCH

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION METHODOLOGY

2.2.1 PRODUCT-BASED MARKET ESTIMATION

2.2.2 END-USER-BASED MARKET ESTIMATION

2.2.3 PRIMARY RESEARCH VALIDATION

2.2.4 TOP-DOWN APPROACH

2.2.5 GROWTH RATE PROJECTIONS

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 DEFIBRILLATOR MARKET OVERVIEW

4.2 ASIA PACIFIC DEFIBRILLATOR MARKET, BY COUNTRY AND END USER

4.3 GEOGRAPHIC SNAPSHOT OF DEFIBRILLATOR MARKET

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing prevalence of cardiovascular diseases

5.2.1.2 Increasing focus on public-access defibrillators

5.2.1.3 Training and awareness programs on defibrillators

5.2.2 RESTRAINTS

5.2.2.1 Frequent product recalls

5.2.3 OPPORTUNITIES

5.2.3.1 Untapped growth potential in emerging markets

5.2.3.2 Development of S-ICDs and MRI-compatible ICDs & CRT-Ds

5.2.4 CHALLENGES

5.2.4.1 Inadequate awareness of sudden cardiac arrest and limited access to healthcare

5.2.4.2 Challenges associated with pricing pressure

5.3 INDUSTRY TRENDS

5.3.1 NEXT GEN AI-ENABLED PATCH WEARABLE CARDIOVERTER DEFIBRILLATORS

5.3.2 CONNECTED AED ECOSYSTEM

5.3.3 EXPANSION IN EMERGING MARKETS AND PUBLIC ACCESS

5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS