측방유동 어세이 시장 : 제품별, 용도별, 수법별, 샘플 유형별, 최종 사용자별, 지역별, 예측(-2030년)

Lateral Flow Assays Market by Product, Application, Sample, Technique, End User, and Region - Global Forecast to 2030

상품코드:1794016

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 439 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

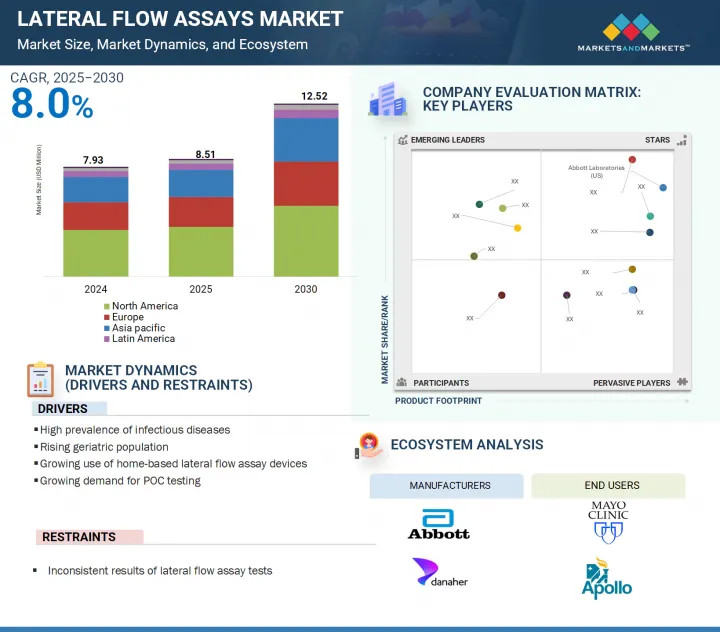

측방유동 어세이 시장 규모는 예측 기간 동안 8.0%의 연평균 복합 성장률(CAGR)로 성장하여, 2025년 85억 1,000만 달러에서 2030년에는 125억 2,000만 달러로 성장할 것으로 예측됩니다.

조사 범위

대상 연도

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문

제품별, 용도별, 수법별, 샘플 유형별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가

이는 세계 감염의 높은 유행과 이에 따른 검사 요구, 노인 인구의 급속한 증가, 가정용 측방유동 어세이 장치의 사용 증가, POC 검사 수요 증가에 의한 것으로, 이들이 이 시장의 성장을 가속하는 주요 요인이 되고 있습니다. 그러나 다른 방법에 비해 정밀도가 안정되지 않거나 의사와 환자가 기존의 진단법에서의 이행에 소극적이라는 것이 측방유동 어세이 시장의 성장을 억제하고 있습니다.

임상 검사 부문은 측방유동 어세이 시장에서 가장 큰 응용 부문입니다. 용도별로는 측방유동 어세이 시장은 임상 검사, 동물 진단, 식품 안전 및 환경 검사, 의약품 개발 및 품질 검사로 구분됩니다. 2024년 측방유동 어세이 시장에서는 임상 검사 분야가 가장 큰 점유율을 차지했습니다. 이 추세는 조사 기간 동안 계속될 것으로 예측됩니다. 이 응용 분야의 큰 점유율은 세계의 만성 질환과 감염의 유병률 증가, 노인 인구 증가, 신속 검사 옵션에 대한 환자 의식 증가, 건강 관리 비용 절감에 대한 압력 증가, 환자 중심 관리에 대한 수요 증가로 인한 것입니다.

최종 사용자별로, 측방유동 어세이 시장은 병원 및 클리닉, 진단 실험실, 재택 케어 환경, 제약 및 생명공학 기업 등으로 구분됩니다. 2024년 시장 점유율은 병원 및 진료소가 가장 큽니다. 기술의 진보, 포인트 오브 케어 검사의 채택 증가, 신속 및 조기 진단에의 지향 고조가, 병원 및 진료소 부문의 성장을 견인하고 있습니다.

세계 측방유동 어세이 시장은 주요 6개 지역(북미, 유럽, 아시아태평양, 라틴아메리카, 중동, 아프리카, GCC 국가)으로 구분됩니다. 북미는 첨단 의료 인프라, 상당한 의료비 및 주요 제조업체의 존재로 인해 이 시장에서 주도적인 지위를 차지하고 있습니다. 고령화 인구 증가, 감염 및 만성 질환의 유병률 증가, 가정용 검사 키트 및 자기 검사 키트에 대한 왕성한 수요가 북미 시장 성장을 더욱 뒷받침하고 있습니다. 이 지역 부문은 예측 기간 동안 지배적인 지위를 유지할 것으로 예측됩니다.

본 보고서에서는 세계 측방유동 어세이 시장에 대해 조사했으며, 제품별, 용도별, 수법별, 샘플 유형별, 최종 사용자별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

기술 분석

Porter's Five Forces 분석

규제 상황

특허 분석

무역 분석

가격 분석

주요 회의 및 이벤트

주요 이해관계자와 구매 기준

측방유동 어세이 시장에 있어서의 미충족 요구/최종사용자의 기대

밸류체인 분석

공급망 분석

AI가 측방유동 어세이 시장에 미치는 영향

생태계 분석

사례 연구 분석

측방유동 어세이의 인접 시장

고객사업에 영향을 주는 동향/혼란

투자 및 자금조달 시나리오

미국 관세 규제별 측방유동 어세이 시장에 대한 영향

제6장 측방유동 어세이 시장(제품별)

소개

키트 및 시약

리더

제7장 측방유동 어세이 시장(용도별)

소개

임상시험

동물 진단

식품안전 및 환경시험

의약품 개발과 품질시험

제8장 측방유동 어세이 시장(기술별)

소개

샌드위치 분석

경쟁 분석

멀티플렉스 검출 분석

제9장 측방유동 어세이 시장(샘플 유형별)

소개

혈액 샘플

소변 샘플

타액 샘플

기타

제10장 측방유동 어세이 시장(최종사용자별)

소개

병원, 클리닉

재택 케어

진단실험실

제약 및 바이오테크놀러지 기업

기타

제11장 측방유동 어세이 시장(지역별)

소개

북미

북미의 거시경제 전망

미국

캐나다

유럽

유럽의 거시 경제 전망

독일

영국

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양의 거시 경제 전망

일본

중국

인도

호주

한국

기타

라틴아메리카

라틴아메리카의 거시 경제 전망

브라질

멕시코

아르헨티나

기타

중동 및 아프리카

GCC 국가

신속하고 비용 효율적인 진단에 대한 수요 증가가 시장을 견인

제12장 경쟁 구도

소개

주요 진입기업의 전략/강점

수익 분석, 2020년-2024년

시장 점유율 분석, 2024년

기업평가와 재무지표

브랜드/제품 비교

기업평가 매트릭스 : 주요 진입기업, 2024년

기업평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

ABBOTT LABORATORIES

F. HOFFMANN-LA ROCHE LTD.

DANAHER CORPORATION

QUIDELORTHOORTHO CORPORATION

SIEMENS AG

BECTON, DICKINSON AND COMPANY

BIOMERIEUX SA

THERMO FISHER SCIENTIFIC INC.

REVVITY, INC.

QIAGEN NV

MERCK KGAA

HOLOGIC, INC.

SURMODICS, INC.

ORASURE TECHNOLOGIES

기타 기업

CHEMBIO DIAGNOSTICS INC.

DCN DIAGNOSTICS

POLYSCIENCES INC.

ABINGDON HEALTH

ORANOXIS INC.

AESKU.GROUP GMBH

BIO GROUP MEDICAL SYSTEM SRL

PHARMACT GMBH

XIAMEN BIOTIME BIOTECHNOLOGY CO., LTD.

BIOPANDA REAGENTS LTD

ARTRON LABORATORIES INC.

제14장 부록

SHW

영문 목차

영문목차

The lateral flow assays market is estimated to grow from USD 8.51 billion in 2025 to USD 12.52 billion by 2030 at a CAGR of 8.0%, during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, Application, Technique, Sample Type, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries

This is due to the high prevalence of infectious diseases worldwide and the subsequent need for testing, rapid growth in the geriatric population, the rising use of home-based lateral flow assay devices, and the growing demand for POC testing, which are the major factors driving the growth of this market. However, inconsistent accuracy compared to other methods and the reluctance of doctors and patients to shift from traditional diagnostics restrain the growth of the lateral flow assays market.

"The clinical testing segment of the lateral flow assays market, by application, is estimated to hold the largest position during the forecast period."

The clinical testing segment is the largest application segment in the lateral flow assays market. Based on applications, the lateral flow assays market is segmented into clinical testing, veterinary diagnostics, food safety & environmental testing, and drug development & quality testing. The clinical testing segment accounted for the largest share of the lateral flow assays market in 2024. This trend is projected to continue during the study period. The large share of this application segment can be attributed to the rising prevalence of chronic diseases and infectious diseases worldwide, the growing geriatric population, increasing patient awareness about rapid test options, the growing pressure to reduce healthcare costs, and the increasing demand for patient-centric care.

"The hospitals & clinics segment accounted for the largest market share in the lateral flow assays market."

Based on end users, the LFA market is segmented into hospitals & clinics, diagnostic laboratories, home care settings, pharmaceutical & biotechnology companies, and others. The hospitals and clinics segment accounted for the largest market share in 2024. Technological advancements, increasing adoption of point-of-care testing, and the growing inclination toward fast and early diagnosis are driving the growth of the hospitals & clinics segment.

"North America segment of the lateral flow assays market, by region, is estimated to account for the largest share during the forecast period."

The global lateral flow assays market is segmented into six major regions: North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries. North America holds the leading position in this market, driven by advanced healthcare infrastructure, significant healthcare expenditure, and the strong presence of key manufacturers. The increasing aging population, rising prevalence of infectious and chronic diseases, and strong demand for home-use and self-test kits further support market growth in North America. This regional segment is expected to maintain its dominant position throughout the forecast period.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 35%

By Designation: C Level: 27%, Director Level: 18%, and Others: 55%

By Region: North America: 50%, Europe: 20%, Asia Pacific: 20%, Latin America: 7%, and Middle East & Africa: 3%

Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = Greater than USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = Less than USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the lateral flow assays market are Abbott Laboratories (US), F. Hoffman-La Roche Ltd. (Switzerland), Danaher Corporation (US), Becton, Dickinson and Company (US), QuidelOrtho Corporation (US), Siemens AG (Germany), bioMerieux SA (France), Thermo Fisher Scientific, Inc. (US), Revvity, Inc. (US), Hologic Inc. (US), QIAGEN N.V. (Netherlands), Merck KGaA (Germany), Surmodics, Inc. (US), and OraSure Technologies Inc. (US).

Research Coverage

This report studies the lateral flow assays market based on product, application, technique, sample type, end user, and region. The report also studies factors (such as drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends. It forecasts the revenue of the market segments with respect to six major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to gain a larger market share. Firms purchasing the report could use one or a combination of the strategies mentioned below to strengthen their market presence.

This report provides insights on the following points:

Analysis of key drivers (High prevalence of infectious diseases, Rising geriatric population, Growing use of home-based lateral flow assay devices, and Growing demand for POC testing), restraints (Inconsistent results of lateral flow assay tests), opportunities (Evolving applications of lateral flow assays and Rising demand for lateral flow assays in food & beverage industry), challenges (Limited reimbursements for lateral flow assay products and Difficulties in procuring quality raw materials to develop tests).

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the lateral flow assays market

Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product launches in the lateral flow assays market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the lateral flow assays market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 INCLUSIONS & EXCLUSIONS

1.3 MARKET SCOPE

1.3.1 MARKETS COVERED

1.3.2 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary sources

2.1.2.2 Key industry insights

2.1.2.3 Key data from primary sources

2.1.2.4 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach 1: Company revenue estimation approach

2.2.1.2 Approach 2: Presentations of companies and primary interviews

2.2.1.3 Approach 3: Primary interviews

2.2.1.4 Approach 4: Growth Forecast

2.2.1.5 CAGR projections

2.2.2 TOP-DOWN APPROACH

2.3 MARKET BREAKDOWN & DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.4.1 STUDY-RELATED ASSUMPTIONS

2.4.2 GROWTH RATE ASSUMPTIONS

2.5 RISK ASSESSMENT

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 LATERAL FLOW ASSAYS MARKET OVERVIEW

4.2 ASIA PACIFIC: LATERAL FLOW ASSAYS MARKET, BY APPLICATION AND COUNTRY

4.3 LATERAL FLOW ASSAYS MARKET, BY COUNTRY

4.4 LATERAL FLOW ASSAYS MARKET: REGIONAL MIX

4.5 LATERAL FLOW ASSAYS MARKET: EMERGING ECONOMIES VS. DEVELOPED MARKETS

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 High prevalence of infectious diseases

5.2.1.2 Rise in geriatric population

5.2.1.3 Growing use of home-based lateral flow assay devices

5.2.1.4 Growth in demand for POC testing

5.2.2 RESTRAINTS

5.2.2.1 Inconsistent results of lateral flow assays

5.2.3 OPPORTUNITIES

5.2.3.1 Evolving applications of lateral flow assays

5.2.3.2 Rise in demand for lateral flow assays in food & beverage industry

5.2.4 CHALLENGES

5.2.4.1 Limited reimbursements for lateral flow assay products

5.2.4.2 Difficulties in procuring quality raw materials to develop tests

5.5.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.5.2.1 North America

5.5.2.2 Europe

5.5.2.3 Asia Pacific

5.5.2.4 Latin America

5.5.2.5 Rest of the world

5.6 PATENT ANALYSIS

5.7 TRADE ANALYSIS

5.7.1 IMPORT DATA (HS CODE 382200)

5.7.2 EXPORT DATA (HS CODE 382200)

5.8 PRICING ANALYSIS

5.8.1 INDICATIVE AVERAGE SELLING PRICE TREND, BY REGION

5.9 KEY CONFERENCES AND EVENTS

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 UNMET NEEDS/END-USER EXPECTATIONS IN LATERAL FLOW ASSAYS MARKET

5.12 VALUE CHAIN ANALYSIS

5.13 SUPPLY CHAIN ANALYSIS

5.14 IMPACT OF AI ON LATERAL FLOW ASSAYS MARKET

5.14.1 INTRODUCTION

5.14.2 MARKET POTENTIAL OF AI IN LATERAL FLOW ASSAYS MARKET

5.14.3 AI USE CASES

5.14.4 KEY COMPANIES IMPLEMENTING AI

5.14.5 FUTURE OF AI IN LATERAL FLOW ASSAYS MARKET

5.15 ECOSYSTEM ANALYSIS

5.16 CASE STUDY ANALYSIS

5.16.1 QUIDEL LAUNCHED NEW TEST WITH BROADER DETECTION WINDOW

5.16.2 ABINGTON OFFERED HIGH-SENSITIVITY TESTS FOR GREATER QUALITY

5.16.3 SIEMENS OFFERS HIGH-SENSITIVITY TROPONIN I ASSAY TO RAPIDLY DETECT ACUTE MYOCARDIAL INFARCTION

5.17 ADJACENT MARKETS FOR LATERAL FLOW ASSAYS MARKET

5.18 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.19 INVESTMENT AND FUNDING SCENARIO

5.20 IMPACT OF US TARIFF REGULATION ON LATERAL FLOW ASSAYS MARKET

5.20.1 INTRODUCTION

5.20.2 KEY TARIFF RATES

5.20.3 PRICE IMPACT ANALYSIS

5.20.4 KEY IMPACTS ON COUNTRY/REGION

5.20.4.1 North America

5.20.4.2 Europe

5.20.4.3 Asia Pacific

5.20.5 IMPACT ON END-USE INDUSTRIES

5.20.5.1 Hospitals and Clinics

6 LATERAL FLOW ASSAYS MARKET, BY PRODUCT

6.1 INTRODUCTION

6.2 KITS & REAGENTS

6.2.1 RISE IN DEMAND FOR POC TESTING TO DRIVE MARKET

6.3 READERS

6.3.1 DIGITAL/HANDHELD READERS

6.3.1.1 Technological evolution and demand for accuracy to drive adoption

6.3.2 BENCHTOP READERS

6.3.2.1 Lower diagnosis cost per patient to drive segment

7 LATERAL FLOW ASSAYS MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 CLINICAL TESTING

7.2.1 INFECTIOUS DISEASE TESTING

7.2.1.1 Mosquito-borne diseases

7.2.1.1.1 Increase in incidence of dengue and introduction of more reliable test kits to drive market

7.2.1.2 Influenza

7.2.1.2.1 Rise in prevalence of influenza globally to boost market growth, despite lower sensitivity of lateral flow assays

7.2.1.3 Sexually transmitted infections

7.2.1.3.1 HIV

7.2.1.3.1.1 Growing need for early detection and awareness of HIV POC testing to drive market

7.2.1.3.2 HPV

7.2.1.3.2.1 Rapid HPV diagnostics and real-time PCR, covering broad range of genotypes, coupled with higher incidence of cervical cancer to drive segment

7.2.1.3.3 Chlamydia

7.2.1.3.3.1 Greater viability of advanced techniques to drive market

7.2.1.3.4 Gonorrhea

7.2.1.3.4.1 Rising incidence of gonorrhea and antimicrobial resistance to augment growth

7.2.1.3.5 Syphilis

7.2.1.3.5.1 Need for early and accessible diagnosis to fuel growth

7.2.1.3.6 Other sexually transmitted infections

7.2.1.4 Hepatitis

7.2.1.4.1 Nucleic acid hybridization-based LFAs to show strong potential in hepatitis testing

7.2.1.5 Tuberculosis

7.2.1.5.1 Rise in prevalence and growing focus on early diagnosis and treatment to propel market

7.2.1.6 Other infectious diseases

7.2.2 CARDIAC MARKER TESTING

7.2.2.1 Troponin I & T

7.2.2.1.1 Introduction of high-sensitivity troponin assays to support market growth

7.2.2.2 CK-MB

7.2.2.2.1 Growing applications of lateral flow tests in acute myocardial injuries to drive market

7.2.2.3 BNP & NT-proBNP

7.2.2.3.1 Increase in demand for cardiac biomarker tests to detect heart stress and damage to support growth

7.2.2.4 Myoglobin

7.2.2.4.1 Availability of new high-sensitivity cardiac troponin assays to restrict market growth

7.2.2.5 D-Dimer

7.2.2.5.1 Rising incidence of CVDs to drive market for D-dimer tests

7.2.2.6 Other cardiac marker testing

7.2.3 PREGNANCY & FERTILITY TESTING

7.2.3.1 Pregnancy testing

7.2.3.1.1 Pregnancy testing to hold larger market share but register slower growth

7.2.3.2 Fertility testing

7.2.3.2.1 Rise in infertility rates to drive demand for POC fertility testing kits

7.2.4 CHOLESTEROL/LIPID TESTING

7.2.4.1 Lifestyle changes, cardiovascular disorder incidence to drive segment

7.2.5 DRUGS-OF-ABUSE TESTING

7.2.5.1 Technological advancements and rising focus on workplace drug testing to drive market

7.2.6 OTHER CLINICAL TESTS

7.3 VETERINARY DIAGNOSTICS

7.3.1 INFECTIOUS DISEASE OUTBREAKS AND TESTS AVAILABLE FOR DIFFERENT SPECIES TO DRIVE FRAGMENTED MARKET

7.4 FOOD SAFETY & ENVIRONMENT TESTING

7.4.1 HIGH SENSITIVITY AND EASE OF USE TO BOOST DEMAND FOR ASSAYS TO CLEAR FOODS FOR MARKET AVAILABILITY

7.5 DRUG DEVELOPMENT & QUALITY TESTING

7.5.1 GREATER FOCUS ON PRODUCT SAFETY AND QUALITY ASSURANCE TO SUPPORT MARKET GROWTH

8 LATERAL FLOW ASSAYS MARKET, BY TECHNIQUE

8.1 INTRODUCTION

8.2 SANDWICH ASSAYS

8.2.1 WIDE RANGE OF APPLICATIONS IN CLINICAL TESTING TO SUPPORT MARKET GROWTH

8.3 COMPETITIVE ASSAYS

8.3.1 REDUCED SELECTIVITY AND SENSITIVITY COMPARED TO SANDWICH ASSAYS TO HAMPER GROWTH

8.4 MULTIPLEX DETECTION ASSAYS

8.4.1 HIGHER ADOPTION OF MULTI-ANALYTE ASSAYS AMONG CLINICIANS TO FUEL MARKET

9 LATERAL FLOW ASSAYS MARKET, BY SAMPLE TYPE

9.1 INTRODUCTION

9.2 BLOOD SAMPLES

9.2.1 SIGNIFICANT USE OF BLOOD SAMPLES FOR INFECTIOUS DISEASE TESTING TO DRIVE MARKET

9.3 URINE SAMPLES

9.3.1 GROWING USE OF URINE SAMPLES FOR PREGNANCY AND DRUGS-OF-ABUSE TESTING TO DRIVE MARKET

9.4 SALIVA SAMPLES

9.4.1 EASY AND LOW-COST COLLECTION, TRANSPORT, AND ANALYSIS OF SALIVA SAMPLES TO SUPPORT ADOPTION

9.5 OTHER SAMPLES

10 LATERAL FLOW ASSAYS MARKET, BY END USER

10.1 INTRODUCTION

10.2 HOSPITALS & CLINICS

10.2.1 HIGH DEMAND FOR DIAGNOSTICS ACROSS LARGE POOLS OF PATIENTS IN HOSPITALS TO DRIVE MARKET

10.3 HOME CARE SETTINGS

10.3.1 GROWING ACCEPTANCE OF REMOTE MONITORING TO PROPEL MARKET

10.4 DIAGNOSTIC LABORATORIES

10.4.1 LABORATORY TESTING LARGELY PREFERRED OVER PROFESSIONAL SETTINGS FOR URINE AND BLOOD TESTING

10.5 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

10.5.1 INCREASE IN FOCUS ON PRODUCT SAFETY TO DRIVE ADOPTION OF LATERAL FLOW ASSAYS

10.6 OTHER END USERS

11 LATERAL FLOW ASSAYS MARKET, BY REGION

11.1 INTRODUCTION

11.2 NORTH AMERICA

11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

11.2.2 US

11.2.2.1 Large patient base to drive market growth

11.2.3 CANADA

11.2.3.1 Availability of research funding and implementation of favorable government initiatives to drive market

11.3 EUROPE

11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

11.3.2 GERMANY

11.3.2.1 Well-developed healthcare system and rise in geriatric population to fuel growth

11.3.3 UK

11.3.3.1 Growth in incidence of chronic conditions to propel market growth

11.3.4 FRANCE

11.3.4.1 High prevalence of age-related chronic diseases and infectious diseases to drive market

11.3.5 ITALY

11.3.5.1 Growth in initiatives toward decentralization of medical services to support market growth

11.3.6 SPAIN

11.3.6.1 Aging population and strong healthcare infrastructure to drive market

11.3.7 REST OF EUROPE

11.4 ASIA PACIFIC

11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

11.4.2 JAPAN

11.4.2.1 Growing elderly population and well-developed healthcare system to drive market

11.4.3 CHINA

11.4.3.1 Modernized healthcare system to drive market

11.4.4 INDIA

11.4.4.1 Growth in healthcare concerns and rise in income levels to propel market growth, despite lack of reimbursement and insurance coverage for lateral flow assay products

11.4.5 AUSTRALIA

11.4.5.1 Rise in prevalence of infectious disease and healthcare expenditure to support growth

11.4.6 SOUTH KOREA

11.4.6.1 Growth in healthcare infrastructure to drive market

11.4.7 REST OF ASIA PACIFIC

11.5 LATIN AMERICA

11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

11.5.2 BRAZIL

11.5.2.1 High private healthcare expenditure and rise in geriatric population to drive market

11.5.3 MEXICO

11.5.3.1 Increase in demand for advanced medical equipment to drive market

11.5.4 ARGENTINA

11.5.4.1 Availability of health insurance to favor market growth

11.5.5 REST OF LATIN AMERICA

11.6 MIDDLE EAST & AFRICA

11.7 GCC COUNTRIES

11.7.1 RISE IN DEMAND FOR RAPID AND COST-EFFECTIVE DIAGNOSTICS TO DRIVE MARKET

12 COMPETITIVE LANDSCAPE

12.1 INTRODUCTION

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN LATERAL FLOW ASSAYS MARKET

12.3 REVENUE ANALYSIS, 2020-2024

12.4 MARKET SHARE ANALYSIS, 2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND/PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Regional Footprint

12.7.5.3 Product Footprint

12.7.5.4 Technique Footprint

12.7.5.5 Application Footprint

12.7.5.6 Sample type Footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024