폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 등급별, 용도별, 최종 이용 산업별, 지역별 예측(-2030년)

Polybutylene Adipate Terephthalate Market by Grade, Application (Films, Sheets & Bin Liners, Coatings & Adhesives, Molded Products, Fibers), End-use Industry (Packaging, Consumer Goods, Agriculture, Bio-medical), and Region - Global Forecast to 2030

상품코드:1788518

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 289 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

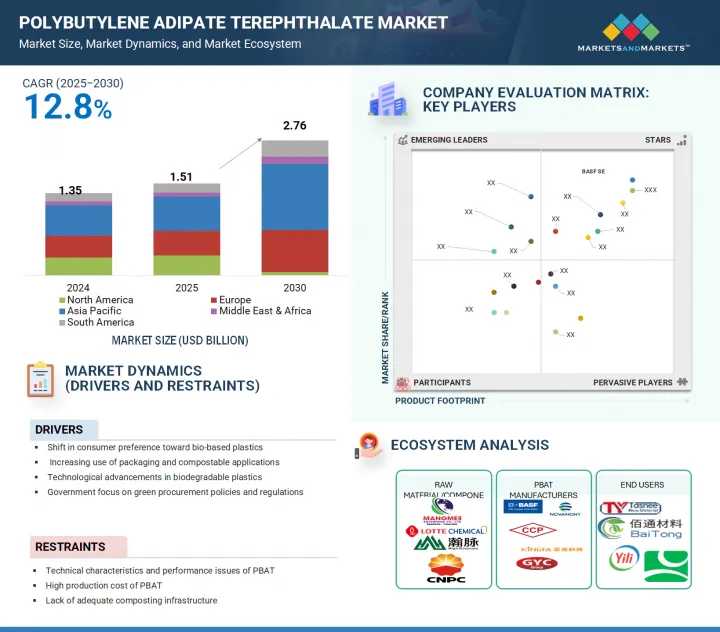

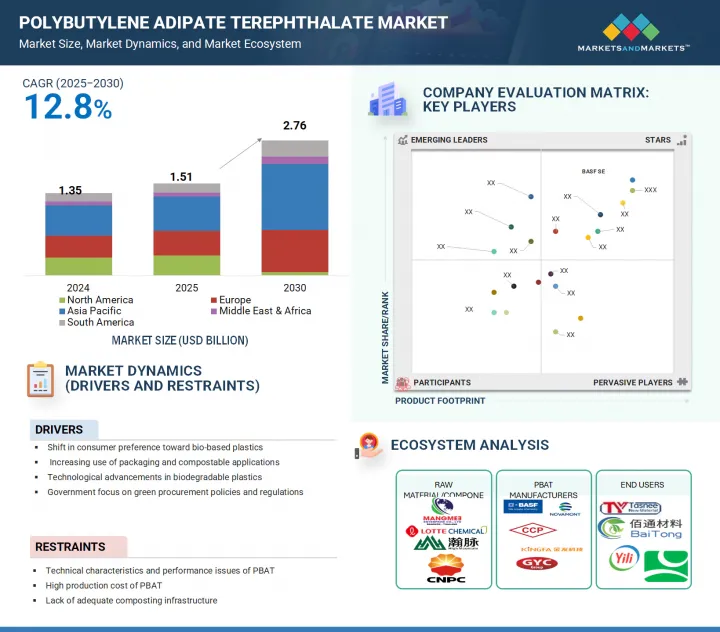

세계의 폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 규모는 2025년 15억 1,000만 달러에서 2030년까지 27억 6,000만 달러에 이를 것으로 예측되며, 2025-2030년에 CAGR 12.8%의 성장이 예상됩니다.

조사 범위

조사 대상 연도

2022-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러, 톤

부문

등급, 최종 용도, 산업, 지역

대상 지역

유럽, 북미, 아시아태평양, 중동, 아프리카, 남미

경질 포장 및 반경질 포장 용도에서의 사용이 증가하고 있기 때문에 열성형 등급이 PBAT 시장에서 2위 점유율을 차지할 것으로 예측됩니다. PBAT는 유연성, 내열성 및 생분해성을 특별히 혼합하여 열 성형 공정에 사용할 수 있으며 일회용 식기, 크램쉘 용기, 퇴비화 가능한 식품 트레이, 뚜껑 등의 제품을 만드는 데 자주 사용됩니다.

생분해성 열성형 제품은 특히 북미와 유럽의 푸드서비스 제공업체가 EU의 Single-use Plastics Directive 및 미국 여러 주에서의 사용 금지와 같은 법적 요건을 충족하고 지속 가능한 대체품으로의 전환을 추진하고 있기 때문에 점점 인기가 높아지고 있습니다. 업무용 케이터링, 테이크아웃 서비스, 조리된 식품 포장 등 성능과 퇴비화가 중요한 산업에서는 열성형 PBAT 제품의 이용도 증가하고 있습니다.

열성형의 성공에 필수적인 강성과 성형성을 향상시키는 PBAT와 PLA와 전분의 혼합의 이용 가능성이 높아지고 있는 것도 이 시장에 이익을 가져오고 있습니다. 열성형 등급 PBAT 시장은 산업 퇴비화 능력 증가와 환경 친화적인 포장 형식에 대한 소비자의 선호에 의해 지속적으로 강력하게 성장할 것으로 예측됩니다.

"금액에서는 성형 플라스틱 제품 용도가 예측 기간 동안 시장 전체에서 2위 점유율을 차지할 것으로 예측됩니다."

사출 성형된 일회용 제품을 대체하는 생분해성 제품에 대한 수요 증가는 성형 플라스틱 제품 부문의 큰 성장을 가속할 것으로 예측됩니다. 범용성, 생분해성, 사출성형과의 적합성으로부터, PBAT는 식품 용기, 포장 부품, 일회용 식기, 농구 등 폭넓은 성형품의 생산에 이상적인 재료입니다. 또한 특히 푸드서비스, 접객 및 의료 부문에서 퇴비화 불가능한 일회용 플라스틱에 대한 국제 규제 증가가 이러한 성장을 더욱 강화하고 있습니다. EU의 Single-use Plastics Directive와 미국의 다양한 국가 수준 금지와 같은 유럽, 북미 및 아시아태평양 국가들이 시행하는 엄격한 규제로 제조업체는 바이오 성형품으로의 전환을 촉구하고 있습니다.

또한 성형 PBAT 제품은 ASTM D6400 및 EN 13432 표준을 충족하는 경량으로 퇴비화 가능한 대체품이 기존의 경질 플라스틱 부품을 대체하는 업무용 포장 및 테이크아웃 포장으로 인기가 높아지고 있습니다. 성형 플라스틱 제품 부문은 퇴비화 인프라가 진보하고 환경 친화적인 포장에 대한 소비자 수요가 증가함에 따라 PBAT 시장에서 2위 기여자로서의 지위를 유지할 것으로 예측됩니다.

"소비재 최종 이용 산업이 예측 기간에 2위 시장 점유율을 차지합니다."

일용품의 환경 친화적이고 생분해 가능한 대체품에 대한 수요 증가는 소비재 성장을 가속할 것으로 예측됩니다. 우수한 기계적 특성, 퇴비화 가능성, 다양한 혼합물과의 호환성을 갖춘 PBAT는 쇼핑백, 가정용 포장, 반려동물 쓰레기 봉지, 일회용 식기, 위생 용품 등 다양한 소비재에 이상적입니다. 지속가능한 라이프스타일에 대한 소비자 선호도와 환경 의식이 높아짐에 따라 다양한 산업 브랜드들이 PBAT 기반 재료를 도입하고 있습니다. 소매점과 전자상거래를 통해 퇴비화 가능한 가정용품과 퍼스널케어 용품이 확대되고 있는 것도 이 부문의 성장에 기여하고 있습니다. 게다가 북미와 유럽의 주요 슈퍼마켓 체인이 프라이빗 브랜드 제품에 PBAT를 사용함으로써 시장 침투율이 크게 높아지고 있습니다. 각국 정부는 지속가능한 제품설계와 녹색조달정책의 실시를 추진하는 대처를 통해 소비자용도로 기존의 플라스틱을 대체하도록 제조업체에 일하고 있습니다. 소비재 부문은 계속해서 PBAT 수요의 큰 촉진요인이 될 전망이며, 특히 산업적 퇴비화 인프라가 확대되고 일회용 플라스틱에 대한 세계의 규제 압력이 높아짐에 따라 포장 재료에 이어 2위의 응용 분야로서의 지위를 강화하고 있습니다.

본 보고서는 세계의 폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장에서 기업에게 매력적인 기회

아시아태평양의 폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 최종 이용 산업별, 국가별

폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 등급별

폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 용도별

폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 최종 이용 산업별

폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 국가별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

밸류체인 분석

Porter's Five Forces 분석

생태계 분석

특허 분석

소개

조사 방법

문서의 유형

고찰

관할분석

주요 기업/응모자

가격 설정 분석

평균 판매 가격의 동향 : 지역별(2022-2030년)

평균 판매 가격의 동향 : 용도별(2022-2030년)

주요 기업의 평균 판매 가격 동향 : 최종 이용 산업별(2024년)

관세 및 규제 상황

북미

아시아태평양

유럽

중동, 아프리카 및 남미

규제기관, 정부기관, 기타 조직 목록

구매 결정에 영향을 미치는 주요 요인

품질

서비스

주요 컨퍼런스 및 이벤트(2025-2026년)

고객사업에 영향을 주는 동향/혼란

거시경제지표

기술 분석

폴리부틸렌 아디페이트 테레프탈레이트(PBAT)의 효소 재활용

폴리부틸렌 아디페이트 테레프탈레이트(PBAT)의 3D 프린팅

폴리부틸렌 아디페이트 테레프탈레이트(PBAT)의 생물의학 이용

JOHNSON MATTHEY의 BDO 기술

바이오물질 수지 PBAT

트윈 스크류 압출 기술

무역 분석

수입 시나리오(HS 코드 291712)

수출 시나리오(HS 코드 291712)

AI/생성형 AI의 영향

사례 연구 분석

제6장 PBAT 시장 : 등급별

소개

압출 등급

열성형 등급

기타 등급

제7장 PBAT 시장 : 용도별

소개

필름, 시트 및 쓰레기봉투

코팅 및 접착제

성형품

섬유

기타 용도

제8장 PBAT 시장 : 최종 이용 산업별

소개

포장

소비재

농업

생물의학

기타 최종 이용 산업

제9장 폴리부틸렌 아디페이트 테레프탈레이트(PBAT) 시장 : 지역별

소개

아시아태평양

중국

일본

인도

한국

기타 아시아태평양

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

북미

미국

캐나다

멕시코

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

GCC

남아프리카

기타 중동 및 아프리카

제10장 경쟁 구도

개요

주요 진입기업의 전략

시장 점유율 분석

수익 분석

기업 평가 및 재무 지표

제품/브랜드 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제11장 기업 프로파일

주요 기업

BASF SE

CHANG CHUN GROUP

KINGFA SCI.&TECH. CO., LTD

NOVAMONT SPA

GO YEN CHEMICAL INDUSTRIAL CO LTD

ANHUI JUMEI BIOLOGICAL TECHNOLOGY CO., LTD

HANGZHOU PEIJIN CHEMICAL CO., LTD.

JIN HUI ZHAO LONG HIGH TECH CO., LTD.

T.EN ZIMMER GMBH

MITSUI PLASTICS, INC.

기타 기업

ZHEJIANG BIODEGRADABLE ADVANCED MATERIAL CO. LTD

HENGLI GROUP CO., LTD.

JUNYUAN PETROLEUM GROUP

QINGDAO ZHOUSHI PLASTIC PACKAGING CO., LTD.

RED AVENUE

SGA POLYCHEM PVT LTD

XINJIANG BLUE RIDGE TUNHE SCI.&TECH. CO., LTD.

TAPRATH ELASTOMERS LLP

EASY FLUX

ENTEC POLYMERS

INDOCAL

YUVIKA GREEN EARTH SOLUTIONS

NINGBO CHANGHONG POLYMER SCIENTIFIC AND TECHNICAL INC

POLYROCKS CHEMICAL CO., LTD

SHANDONG DAWN INTERNATIONAL TRADING CO., LTD(DAWN GROUP)

제12장 부록

JHS

영문 목차

영문목차

The global PBAT market is expected to reach USD 2.76 billion by 2030 from USD 1.51 billion in 2025, at a CAGR of 12.8% from 2025 to 2030.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Ton)

Segments

Grade, Application, End-use Industry, and Region

Regions covered

Europe, North America, Asia Pacific, Middle East & Africa, and South America

Because of its increasing use in rigid and semi-rigid packaging applications, the thermoforming grade is projected to hold the second-largest share of the PBAT market. Because of its special blend of flexibility, heat resistance, and biodegradability, PBAT can be used in thermoforming processes, which are frequently used to create products like disposable cutlery, clamshell containers, compostable food trays, and lids.

Biodegradable thermoformed products are becoming increasingly popular as food service providers, particularly in North America and Europe, move toward sustainable alternatives in response to legal requirements such as the EU Single-use Plastics Directive and several state bans in the US. In industries where performance and compostability are crucial, such as institutional catering, takeout services, and ready-to-eat food packaging, thermoformed PBAT products are also being utilized more.

The increasing availability of PBAT blends with PLA or starch, which improve rigidity and moldability-two essentials for successful thermoforming-benefits the market. Second, only to the leading films & sheets segment in terms of volume and revenue, the thermoforming-grade PBAT market is expected to grow strongly and sustainably due to growing industrial composting capabilities and consumer preference for eco-friendly packaging formats.

''In terms of value, the molded plastic products application is expected to account for the second-largest share of the overall market during the forecast period''

The increasing demand for biodegradable alternatives to injection-molded single-use products is expected to drive significant growth in the molded plastic products segment. Because of its versatility, biodegradability, and compatibility with injection molding, PBAT is an ideal material for producing a wide range of molded goods, including food containers, packaging components, disposable cutlery, and agricultural tools. Additionally, the rise of international regulations on non-compostable single-use plastics, especially in the food service, hospitality, and healthcare sectors, is further supporting this growth. Manufacturers are being encouraged to shift toward bio-based molded products due to strict regulations implemented by countries in Europe, North America, and the Asia Pacific, such as the EU Single-use Plastics Directive and various state-level bans in the US.

Additionally, molded PBAT products are becoming more popular in institutional and takeout packaging, where lightweight, compostable alternatives that satisfy ASTM D6400 and EN 13432 standards are replacing conventional rigid plastic components. The molded plastic products segment is expected to maintain its position as the second-largest contributor to the PBAT market, as composting infrastructure advances and consumer demand for environmentally friendly packaging rises.

"Consumer goods end-use industry to account for the second-largest market share during the forecast period"

The increasing demand for eco-friendly and biodegradable alternatives in everyday products is anticipated to drive the growth of consumer goods. With excellent mechanical properties, compostability, and compatibility with various blends, PBAT is ideal for a wide range of consumer goods, including shopping bags, household packaging, pet waste bags, disposable cutlery, and hygiene products. Brands across various industries are incorporating PBAT-based materials in response to rising consumer preferences for sustainable lifestyles and heightened environmental awareness. The expansion of compostable household and personal care products through retail and e-commerce is also contributing to the segment's growth. Additionally, the use of PBAT in private-label products by major supermarket chains in North America and Europe is significantly increasing market penetration. Governments are encouraging manufacturers to replace traditional plastics in consumer applications through initiatives promoting sustainable product design and the implementation of green procurement policies. The consumer goods sector is well-positioned to remain a major driver of PBAT demand, reinforcing its status as the second-largest application segment after packaging, especially as industrial composting infrastructure expands and global regulatory pressure on single-use plastics grows.

"Europe to account for the second-largest share of the PBAT during the forecast period"

Due to robust regulatory frameworks, developed recycling and composting infrastructure, and rising consumer demand for environmentally friendly packaging, Europe is anticipated to hold the second-largest share of the global PBAT market. With stringent laws like the EU Single-use Plastics Directive, the Green Deal, and the Circular Economy Action Plan that encourage the use of biodegradable and compostable substitutes like PBAT, the European Union has been leading the global effort to reduce plastic pollution. Key markets in the region include Germany, Italy, France, and Spain, all of which actively enforce laws prohibiting traditional plastic bags and promote certified compostable packaging for use in waste management, food service, and retail settings. For European manufacturers looking to meet compostability standards like EN 13432, PBAT is a preferred material due to its compatibility with PLA and starch blends and suitability for rigid and flexible packaging, agricultural films, and consumer goods. Europe continues to play a significant role in the global PBAT market, ranking second only to the Asia Pacific in terms of market share and influence, due to sustained innovation, public support for sustainable materials, and a strong emphasis on reducing plastic waste through legislative action.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

By Designation: C Level - 33%, Director Level - 33%, and Managers - 34%

By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, the Middle East & Africa - 15%, and Latin America - 15%

The report provides a comprehensive analysis of company profiles of prominent companies such as BASF SE (Germany), Chang Chun Group (China), Kingfa Sci. & Tech. Co., Ltd. (China), Novamont S.p.A. (Italy), GO YEN CHEMICAL INDUSTRIAL CO LTD (Taiwan), Anhui Jumei Biological Technology Co., Ltd. (China), Hangzhou Peijin Chemical Co., Ltd. (China), Jin Hui Zhao Long High Tech Co., Ltd. (China), T.EN Zimmer GmbH (Germany), Mitsui Plastics, Inc. (US), Zhejiang Baidigorei Biomaterials Co., Ltd. (China), Hengli Group Co., Ltd. (China), Junyuan Petroleum Group (China), Qingdao Zhoushi Plastic Packaging Co., Ltd. (China), Red Avenue New Materials Group Co., Ltd. (China), SGA POLYCHEM PVT LTD (India), Xinjiang Blue Ridge Tunhe Sci. & Tech. Co., Ltd. (China), Taprath Elastomers LLP (India), Easy Flux (India), Entec Polymers (US), Indocal (India), Yuvika Green Earth Solutions (India), Ningbo Changhong Polymer Scientific and Technical Inc. (China), Polyrocks Chemical Co., Ltd. (China), and Shandong Dawn Polymer Co., Ltd. (Dawn Group) (China).

Research Coverage

This research report categorizes the PBAT market by grade (extrusion and thermoforming), application (films, sheets & bin liners, coatings & adhesives, molded products, and fibers), end-use industry (packaging, consumer goods, agriculture, and bio-medical), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the PBAT market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions & services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the PBAT market are all covered. This report includes a competitive analysis of upcoming startups in the PBAT market ecosystem.

Reasons to Buy this Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the PBAT market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following points:

Analysis of key drivers (shift in consumer preference toward bio-based plastics, increasing use of packaging and compostable applications, technological advancements in biodegradable plastics, and government focus on green procurement policies and regulations), restraints (technical characteristics and performance issues of PBAT, high production cost of PBAT, and lack of adequate composting infrastructure), opportunities (development of new applications, high potential of PBAT in emerging economies, and building a strong green branding strategy), and challenges (competition from alternative bioplastics and consumer misunderstanding regarding biodegradability) influencing the growth of the PBAT market.

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and service launches in the PBAT market.

Market Development: Comprehensive information about lucrative markets - the report analyses the PBAT market across varied regions.

Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the PBAT market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as BASF SE (Germany), Chang Chun Group (China), Kingfa Sci. & Tech. Co., Ltd. (China), Novamont S.p.A. (Italy), GO YEN CHEMICAL INDUSTRIAL CO LTD (Taiwan), Anhui Jumei Biological Technology Co., Ltd. (China), Hangzhou Peijin Chemical Co., Ltd. (China), Jin Hui Zhao Long High Tech Co., Ltd. (China), T.EN Zimmer GmbH (Germany), Mitsui Plastics, Inc. (US), Zhejiang Baidigorei Biomaterials Co., Ltd. (China), Hengli Group Co., Ltd. (China), Junyuan Petroleum Group (China), Qingdao Zhoushi Plastic Packaging Co., Ltd. (China), Red Avenue New Materials Group Co., Ltd. (China), SGA POLYCHEM PVT LTD (India), Xinjiang Blue Ridge Tunhe Sci. & Tech. Co., Ltd. (China), Taprath Elastomers LLP (India), Easy Flux (India), Entec Polymers (US), Indocal (India), Yuvika Green Earth Solutions (India), Ningbo Changhong Polymer Scientific and Technical Inc. (China), Polyrocks Chemical Co., Ltd. (China), and Shandong Dawn Polymer Co., Ltd. (Dawn Group) (China).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants-demand and supply sides

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 FORECAST NUMBER CALCULATION

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET

4.2 ASIA PACIFIC POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY END-USE INDUSTRY AND COUNTRY

4.3 POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY GRADE

4.4 POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY APPLICATION

4.5 POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY END-USE INDUSTRY

4.6 POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Shift in consumer preference toward bio-based plastics

5.2.1.2 Increasing use of packaging and compostable applications

5.2.1.3 Technological advancements in biodegradable plastics

5.2.1.4 Government focuses on green procurement policies and regulations

5.2.2 RESTRAINTS

5.2.2.1 Technical characteristics and performance issues of PBAT

5.2.2.2 High production cost

5.2.2.3 Lack of adequate composting infrastructure

5.2.3 OPPORTUNITIES

5.2.3.1 Widening application scope

5.2.3.2 High potential of PBAT in emerging economies

5.2.3.3 Adoption of green branding strategies

5.2.4 CHALLENGES

5.2.4.1 Competition from alternative bioplastics

5.2.4.2 Misunderstanding regarding biodegradability among consumers

5.3 VALUE CHAIN ANALYSIS

5.4 PORTER'S FIVE FORCES ANALYSIS

5.4.1 THREAT OF NEW ENTRANTS

5.4.2 THREATS OF SUBSTITUTES

5.4.3 BARGAINING POWER OF SUPPLIERS

5.4.4 BARGAINING POWER OF BUYERS

5.4.5 INTENSITY OF COMPETITIVE RIVALRY

5.5 ECOSYSTEM ANALYSIS

5.6 PATENT ANALYSIS

5.6.1 INTRODUCTION

5.6.2 METHODOLOGY

5.6.3 DOCUMENT TYPE

5.6.4 INSIGHTS

5.6.5 JURISDICTION ANALYSIS

5.6.6 TOP COMPANIES/APPLICANTS

5.7 PRICING ANALYSIS

5.7.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2030

5.7.2 AVERAGE SELLING PRICE TREND, BY APPLICATION, 2022-2030

5.7.3 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY, 2024

5.8 TARIFF AND REGULATORY LANDSCAPE

5.8.1 NORTH AMERICA

5.8.1.1 US

5.8.1.2 Canada & Mexico

5.8.2 ASIA PACIFIC

5.8.3 EUROPE

5.8.4 MIDDLE EAST & AFRICA AND SOUTH AMERICA

5.8.4.1 Middle East & Africa

5.8.4.2 South America

5.8.5 LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.9 KEY FACTORS AFFECTING BUYING DECISIONS

5.9.1 QUALITY

5.9.2 SERVICE

5.10 KEY CONFERENCES AND EVENTS, 2025-2026

5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.12 MACROECONOMIC INDICATORS

5.12.1 GROSS DOMESTIC PRODUCT TRENDS AND FORECASTS

5.13 TECHNOLOGY ANALYSIS

5.13.1 ENZYMATIC RECYCLING OF POLYBUTYLENE ADIPATE TEREPHTHALATE

5.13.2 3D PRINTING OF POLYBUTYLENE ADIPATE TEREPHTHALATE

5.13.3 BIO-MEDICAL APPLICATIONS OF POLYBUTYLENE ADIPATE TEREPHTHALATE

5.13.4 JOHNSON MATTHEY'S BDO TECHNOLOGY

5.13.5 BIOMASS BALANCED PBAT

5.13.6 TWIN-SCREW EXTRUSION TECHNOLOGY

5.14 TRADE ANALYSIS

5.14.1 IMPORT SCENARIO (HS CODE 291712)

5.14.2 EXPORT SCENARIO (HS CODE 291712)

5.15 IMPACT OF AI/GEN AI

5.16 CASE STUDY ANALYSIS

5.16.1 RELIANCE INDUSTRIES

6 PBAT MARKET, BY GRADE

6.1 INTRODUCTION

6.2 EXTRUSION GRADE

6.2.1 HIGH MELT STRENGTH AND VISCOSITY OF PBAT TO DRIVE DEMAND

6.3 THERMOFORMING GRADE

6.3.1 LOW SHRINKAGE AND EXCELLENT CLARITY OF PBAT TO FUEL DEMAND

6.4 OTHER GRADES

7 PBAT MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 FILMS, SHEETS & BIN LINERS

7.2.1 BIODEGRADABILITY AND COMPOSTABILITY OF PBAT TO DRIVE DEMAND

7.3 COATINGS & ADHESIVES

7.3.1 USE OF PBAT COATINGS FOR IMPROVING SHELF LIFE OF MATERIALS TO FUEL MARKET GROWTH

7.4 MOLDED PRODUCTS

7.4.1 THERMOPLASTIC NATURE OF PBAT TO DRIVE DEMAND

7.5 FIBERS

7.5.1 USE AS BIODEGRADABLE AND COMPOSTABLE MATERIAL IN FIBER PRODUCTION TO PROPEL MARKET

7.6 OTHER APPLICATIONS

8 PBAT MARKET, BY END-USE INDUSTRY

8.1 INTRODUCTION

8.2 PACKAGING

8.2.1 USE AS ALTERNATIVE TO CONVENTIONAL PLASTICS TO DRIVE MARKET

8.2.2 FOOD PACKAGING

8.2.3 NON-FOOD PACKAGING

8.3 CONSUMER GOODS

8.3.1 EXCELLENT PHYSICAL PROPERTIES COMPARED TO CONVENTIONAL PLASTICS TO DRIVE DEMAND

8.4 AGRICULTURE

8.4.1 INCREASED APPLICATIONS IN AGRICULTURE INDUSTRY TO DRIVE MARKET

8.4.2 MULCH FILMS

8.4.3 NETTING

8.5 BIO-MEDICAL

8.5.1 HIGH STRENGTH AND DURABILITY OF PBAT TO DRIVE DEMAND

8.5.2 MEDICAL DEVICES

8.5.3 MEDICAL CONSUMABLES

8.5.4 BONE IMPLANTS

8.6 OTHER END-USE INDUSTRIES

9 POLYBUTYLENE ADIPATE TEREPHTHALATE MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 CHINA

9.2.1.1 Ban on single-use plastics and rising awareness regarding negative impacts of plastic waste to drive market

9.2.2 JAPAN

9.2.2.1 Implementation of policies promoting biodegradable plastics and reducing plastic waste to drive market

9.2.3 INDIA

9.2.3.1 Increasing consumer awareness about negative impact of plastic waste on environment to drive market

9.2.4 SOUTH KOREA

9.2.4.1 Focus on environmental sustainability and reducing plastic waste to boost market

9.2.5 REST OF ASIA PACIFIC

9.3 EUROPE

9.3.1 GERMANY

9.3.1.1 Consumer awareness about the importance of sustainable products and strict government regulations to drive market

9.3.2 UK

9.3.2.1 Implementation of policies and regulations to reduce plastic waste to drive market

9.3.3 FRANCE

9.3.3.1 Demand for sustainable biodegradable plastics from consumers to drive market

9.3.4 ITALY

9.3.4.1 Booming food processing industry to drive market

9.3.5 SPAIN

9.3.5.1 Rising demand for sustainable packaging solutions to drive market

9.3.6 REST OF EUROPE

9.4 NORTH AMERICA

9.4.1 US

9.4.1.1 Focus on manufacturing bioplastic packaging products by private sector companies to boost market

9.4.2 CANADA

9.4.2.1 Prime focus of plastic industry on manufacturing certified compostable bags to drive market

9.4.3 MEXICO

9.4.3.1 Growing developments in biodegradable plastics sector and focus on sustainability to drive market

9.5 SOUTH AMERICA

9.5.1 BRAZIL

9.5.1.1 Rising demand for sustainable packaging solutions from agriculture sector to drive market

9.5.2 ARGENTINA

9.5.2.1 Rising demand for environmentally friendly materials and growing adoption of biodegradable plastics to drive market

9.5.3 REST OF SOUTH AMERICA

9.6 MIDDLE EAST & AFRICA

9.6.1 GCC

9.6.1.1 Saudi Arabia

9.6.1.1.1 Decision of SASO to limit application of technical regulations for biodegradable plastics to drive market

9.6.1.2 UAE

9.6.1.2.1 Growing push for sustainable plastics amid policy reforms to drive market

9.6.1.3 Rest of GCC

9.6.2 SOUTH AFRICA

9.6.2.1 Advancements in bioplastics research to improve management of renewable biological resources and propel market

9.6.3 REST OF MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

10.1 OVERVIEW

10.2 KEY PLAYER STRATEGIES

10.3 MARKET SHARE ANALYSIS

10.4 REVENUE ANALYSIS

10.5 COMPANY VALUATION AND FINANCIAL METRICS

10.6 PRODUCT/BRAND COMPARISON

10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1 STARS

10.7.2 EMERGING LEADERS

10.7.3 PERVASIVE PLAYERS

10.7.4 PARTICIPANTS

10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1 Company footprint

10.7.5.2 Region footprint

10.7.5.3 End-use industry footprint

10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024