철 및 강철 시장 : 유형별, 생산 기술별, 최종 이용 산업별, 지역별 예측(-2030년)

Iron & Steel Market by Type (Iron and Steel), Iron Production Technology, Steel Production Technology, End-use Industry (Construction & Building, Automotive & Transportation, Mechanical Equipment, Metal Products), and Region - Global Forecast to 2030

상품코드:1787263

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 395 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

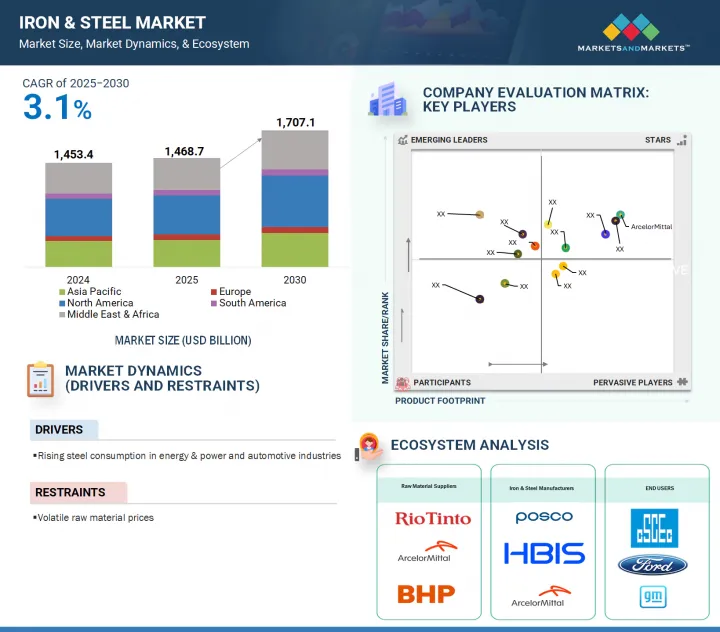

세계의 철 및 강철 시장 규모는 2024년 1조 4,534억 달러에 달했습니다.

이 시장은 CAGR 3.1%로 확대되고 2030년에는 1조 7,071억 달러에 달할 것으로 예측되고 있습니다. 철 및 강철 부문은 선진국 시장과 신흥국 시장의 도시화, 산업화, 인프라 개척 등 여러 요인에 따라 수요가 크게 늘고 있습니다. 건설, 자동차, 에너지, 기계와 같은 주요 최종 용도 부문의 큰 수요가 철 및 강철 제품 수요를 계속 견인하고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러), 100만톤

부문

유형별, 생산기술별, 최종용도 산업별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동, 아프리카, 남미

철 및 강철 제품의 용도는 다양하지만, 국가나 지방자치단체에 의한 대규모 공공 인프라 프로젝트의 전개, 새로운 주택, 상업시설, 정부기관의 지속적인 구조개발, 운송 및 물류 네트워크에 대한 투자가 계속해서 전체적인 성장을 견인하고 있습니다. 또한 중국, 인도, 브라질과 같은 신흥 국가에서 국내 제조를 촉진하고 산업 성장을 자극하는 정부 인센티브는 철 및 강철 이니셔티브의 새로운 산업 운전자로 부상하고 있습니다. 시장의 기세는 생산방법과 생산 공정에서의 기술의 진보에 의해 보완되어, 재활용이나 지속가능성에 관한 변화하는 규제의 기대에 부응하면서 효율성의 향상을 가져오고 있습니다.

고로 공정 부문은 예측 기간 동안 철 및 강철 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이것은 수십년동안 대규모 철 생산의 대부분을 역사적으로 차지해 왔기 때문입니다. 고로 공정은 철광석을 고온에서 코크스와 석회석으로 환원하여 녹은 철(선철)을 생산하는 것으로, 기본 산소 공정에서 철 및 강철을 제조하기 위해 직접 사용되거나 블록에 주조되어 주조소에서 사용됩니다. 철 및 강철업의 미분광석의 고로 루트는 일정한 품질로 대량 생산이 가능하기 때문에 대규모 철 및 강철 생산국에서 사용되고 있는 주요 공정이기도 합니다.

또한, 고로 공정은 원료 분급이 비교적 효율적이며 비용 구조가 전통적으로 연구되고 공유되어 왔기 때문에 특히 중국, 인도, 러시아 등 철 및 강철 소비가 국내 및 수출 요건에 박차를 가하고 있는 국가에서는 훨씬 큰 용량의 일관제철소와 철 및 강철 생산을 가능하게 하고 지원하고 있습니다. 탈탄소화 및 저탄소 비용(전기로 사용 등)을 기반으로 한 대체 기술로의 전환이 진행되고 있지만, 고로 공정은 철근, 강철, 울타리, 강철 지붕 등을 제공합니다. 예를 들어, 고로는 모든 원료를 처리하여 규모의 이점과 비용 절감을 가져오고, 보다 고품질의 철 생산을 가능하게 하며, 이러한 경향은 당분간 지속될 것입니다.

전기 아크로(EAF) 부문은 지속가능하고 비교적 에너지 효율적인 제철로의 전환이 세계적으로 크게 진전되고 있기 때문에 예측 기간 동안 철 및 강철 시장에서 가장 높은 복합 연간 성장률(CAGR)에서 성장할 것으로 예측됩니다. 철광석과 코크스에 크게 의존하는 기존의 고로와 달리, EAF는 재활용된 금속 스크랩을 주요 원료로 사용하므로 탄소 배출량과 에너지 소비가 크게 줄어듭니다.

EAF 생산에는 많은 이점이 있습니다. 기술은 유연하고 자본 집약적이지 않으며 고로보다 시작 시간이 짧습니다. 환경 규제가 강화되고 재활용과 순환 경제가 중시되는 가운데, EAF 생산은 재활용 및 금속 거래 인프라를 유지하는 지역에서 운영하는 생산자에게 점점 매력적이 되고 있습니다. 많은 국가들이 탈탄소화 목표에 관심을 보이게 되었기 때문에 각국은 실천의 동향을 쫓아, 결국 제철소에 대해, 이 이행과 철 및 강철 생산에 의한 환경에 대한 영향의 삭감을 촉구하고 있습니다.

북미와 유럽과 같은 선진 지역에서 철 및 강철 제조업체는 EAF 기반 생산으로 전환하고 있습니다. 한편, 신흥지역에서는 새로운 투자가 철 및 강철 부문의 갱신에 도움이 되기 때문에 EAF 설비에 대한 투자가 점차 진행되고 있습니다. 특히 EAF에서 DRI(직접 환원철)를 사용할 수 있게 된 기술적 진보는 철 및 강철 생산 효율을 개선하고, 에너지 소비를 줄이고, 제품 품질을 향상시켰습니다. 결과적으로 EAF 기반 철 및 강철 생산은 빠르게 성장하고 지속 가능한 철 및 강철 제조의 향후 개발에 중요한 역할을 할 것으로 예측됩니다.

중동 및 아프리카는 인프라 개발, 산업 성장, 인구 증가를 위한 철 및 강철 사용 증가로 예측 기간 동안 철 및 강철 시장에서 가장 높은 복합 연간 성장률(CAGR)에서 성장할 것으로 예측됩니다. 중동 및 아프리카의 많은 나라(사우디아라비아, 아랍에미리트(UAE), 이집트, 남아프리카)는 대규모 건설 프로젝트, 교통망, 에너지 관련 프로젝트에 투자하고 있으며, 이는 철 및 강철 수요를 창출하고 있습니다. 사우디아라비아에서는 '비전 2030', UAE에서는 경제의 다각화와 산업화 프로그램의 확대에 임하고 있으며, 철 및 강철의 국내 생산을 촉진하는 등 정부의 이니셔티브가 이 성장을 지지하고 있습니다. 동시에 석유 및 가스, 광업, 재생가능에너지산업으로부터의 투자 증가도 MEA 지역에서의 철 및 강철 사용을 증가시키고 있습니다. MEA지역은 이용가능한 원재료와 금속부문에 대한 외국 직접투자를 활용하여 전 세계 주요 철 및 강철 제조업체에 대한 지역 경쟁력을 전략적으로 개발하고 있습니다. 진행 중인 도시화, 주택 수요, 경제 다양화의 필요성으로 인해 MEA는 성장하는 입장에 있습니다. 이러한 원동력의 각각이 함께, MEA는 향후 몇 년간, 철 및 강철 업계에 있어서 가장 역동적이고 고성장을 이루는 지역의 하나가 될 것으로 보입니다.

본 보고서에서는 세계의 철 및 강철 시장에 대해 조사했으며, 유형별, 생산기술별, 최종용도 산업별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

제6장 업계 동향

고객의 비즈니스에 영향을 미치는 동향과 혼란

생태계 분석

밸류체인 분석

관세 및 규제 상황

가격 분석

무역 분석

기술 분석

사례 연구 분석

특허 분석

2025-2026년의 주된 회의와 이벤트

투자 및 자금조달 시나리오

철 및 강철 업계의 AI 세대의 영향

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

거시경제 분석

2025년 미국 관세가 철 및 강철 시장에 미치는 영향

제7장 철 및 강철 시장(유형별)

소개

철

강철

제8장 철 시장(생산기술별)

소개

고로 공정

DRI 프로세스

제9장 강철 시장(생산 기술별)

소개

기본 산소로

전기 아크로

기타

제10장 철 및 강철 시장(최종 이용 산업별)

소개

건축 및 건설

자동차 및 운송

기계설비

금속품

기타

제11장 철 및 강철 시장(지역별)

소개

아시아태평양

중국

인도

일본

한국

기타

유럽

독일

이탈리아

프랑스

스페인

영국

러시아

기타

북미

미국

캐나다

멕시코

기타

중동 및 아프리카

GCC 국가

남아프리카

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타

제12장 경쟁 구도

개요

주요 진입기업의 전략

시장 점유율 분석

수익 분석

기업평가와 재무지표

제품/브랜드 비교 분석

기업평가 매트릭스 : 주요 진입기업, 2024년

기업평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오와 동향

제13장 기업 프로파일

주요 진출기업

ARCELORMITTAL

CHINA BAOWU STEEL GROUP CORPORATION LIMITED

ANSTEEL GROUP

HBIS GROUP

NIPPON STEEL CORPORATION

TATA STEEL

JSW

NUCOR CORPORATION

POSCO

SAIL

CSN(NATIONAL STEEL COMPANY)

SSAB AB

기타 기업

JIANGSU SHAGANG GROUP

7 STEEL UK

SONGSHUN STEEL

CD WALZHOLZ GMBH & CO. KG

HUAXIAO METAL CORPORATION LIMITED

HEBEI DONGHAI SPECIAL STEEL GROUP CO., LTD.

FENG HSIN STEEL CO., LTD.

WORTHINGTON STEEL

LIBERTY STEEL GROUP

GERDAU

DS METAL

ARJAS STEEL

SHREE JI STEEL

RAHUL STEEL INDIA

CORROS METALS PVT. LTD.

제14장 인접 시장과 관련 시장

제15장 부록

JHS

영문 목차

영문목차

The market for iron & steel was valued at USD 1,453.4 billion in 2024 and is projected to reach USD 1,707.1 billion by 2030, at a CAGR of 3.1%. The iron and steel sector is experiencing strong growth in demand due to several factors, including urbanization, industrialization, and infrastructure development across developed and emerging markets. Significant demand from major end-use sectors like construction, automotive, energy, and machinery, continues to drive demand for iron and steel products.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion) Volume (Million Ton)

Segments

Type, Iron Production Technology, Steel Production Technology, End-use Industry, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, South America

While there are numerous applications of iron and steel products, the national and local deployment of significant public infrastructure projects, continued structural development of new residential, commercial, and government entities, and investments in transportation and logistics networks, continue to drive overall growth. Additionally, government incentives to promote domestic manufacturing and stimulate industrial growth in emerging countries, such as China, India, and Brazil is emerging as a new industry driver for iron and steel initiatives. Market momentum is supplemented by technology advances in production methods and processes, providing enhancements in efficiency, while continuing to meet changing regulatory expectations regarding recycling and sustainability, which should further enhance demand for iron and steel throughout the world over the long-term.

Based on iron production technology, the blast furnace process segment is projected to account for the largest market share during the forecast period

The blast furnace process segment is expected to account for the largest share of the iron and steel market during the forecast period. This is attributed to the fact that it has historically accounted for the majority of large-scale iron production for decades. The blast furnace process encompasses reducing iron ore either with coke and limestone (at high temperatures) to produce molten iron (pig iron) which is used directly to make steel in a basic oxygen process or cast into blocks and used in foundries. The blast furnace route for pulverized ore in the iron and steel industry also continues to be the main process used in larger steel-producing countries as it allows high volume production with a constant quality of output.

Additionally, the blast furnace process is comparatively efficient at classifying the raw materials, and the cost structure has traditionally been researched and shared that enables and supports much larger capacity integrated steel plants and steel production, especially in countries such as China, India, and Russia, where consumption of iron and steel is fueling domestic and export requirements. Although there is an upward shift in alternative technologies based on decarbonization and lower carbon costs (such as using electric arc furnaces), the blast furnace process provides the rebar, steel frame, fencing, steel roofing, etc. For example, the blast furnace processes all the raw materials and provides economies of scale and lowers costs, enabling the production of a higher-grade iron, and this trend will prevail for the foreseeable future.

Based on steel production technology, the Electric Arc Furnace (EAF) segment is expected to grow at the highest CAGR during the forecast period

The Electric Arc Furnace (EAF) segment is projected to grow at the highest compound annual growth rate (CAGR) in the iron and steel market over the forecast period, as major progress has been made worldwide in the transition to sustainable, relatively energy-efficient steelmaking. Unlike traditional blast furnaces, which are heavily reliant on iron ore and coke, EAFs use recycled scrap metal as their main raw material, resulting in a significant reduction in carbon emissions and energy consumption.

EAF production has a number of advantages: the technology is flexible, is less capital-intensive, and has shorter startup times than blast furnaces. With stricter environmental regulations, and a stronger emphasis on recycling and circular economies, EAF production is increasingly attractive for producers that operate in regions that maintain recycling and metal trading infrastructures. As many nations have increasingly expressed interest in decarbonization goals, they are following practice trends and ultimately encouraging mills to make this transition and reduce the environmental impact of steel production.

In developed regions like North America and Europe, steel producers are shifting toward EAF-based production. While in emerging regions, there is gradual investment in EAF facilities, as new investments are helping update the steel sector. In particular, technological advancements which allowed for DRI (direct reduced iron) to be used in EAFs, have improved steel production efficiency, reduced energy consumption, and improved product quality. As a result, EAF based steel production is expected to grow rapidly and play a crucial role in the future developments in sustainable steelmaking.

Middle East & Africa region is expected to grow at highest CAGR during forecast period

The Middle East & Africa (MEA) region is expected to grow at the highest compound annual growth rate (CAGR) in the iron and steel market during the forecast period due to the increased use of iron and steel for infrastructure development, industrial growth, and population growth. A number of countries in the MEA (Saudi Arabia, UAE, Egypt. and South Africa) have been investing in larger-scale construction projects, transportation networks, and projects associated with energy, which create demand for iron and steel. Governmental initiatives are supporting this growth, with programs such as Vision 2030 in Saudi Arabia and the UAE's commitment to diversify its economy and expand industrialization programs to facilitate domestic manufactured steel. At the same time, growing investments from the oil & gas, mining, and renewable energy industries are also increasing steel use in the MEA region. The MEA region is being strategic about developing the competitiveness of the region against large global producers of iron and steel, taking advantage of accessible raw materials and foreign direct investments in the metals sector. With ongoing urbanization, demand for housing, and a need to diversify their economies, MEA is in a position for growth. Each of these drivers, together, will see MEA as one of the most dynamic and high-growth regions for the iron and steel industry over the coming years.

By Company Type: Tier 1: 40%, Tier 2: 25%, Tier 3: 35%

By Designation: C Level: 35%, Director Level: 30%, Others: 35%

By Region: North America: 25%, Europe: 20%, Asia Pacific: 45%, Middle East & Africa: 5%, and South America: 5%

Companies Covered:

ArcelorMittal (Luxembourg), China Baowu Steel group Corporation Limited (China ), TATA Steel (India), JSW (India), Nucor Corporation (US), NIPPON STEEL CORPORATION (Japan), Ansteel Group Corporation Limited (China), POSCO (UK), HBIS Group (China), and SAIL (India) are some key players in iron & steel market.

Research Coverage

The market study covers the iron & steel market across various segments. It aims to estimate the market size and the growth potential of this market across different segments based on type, iron production technology, steel production technology, end-use industry, and region. The study also includes an in-depth competitive analysis of key players in the market, their company profiles, key observations related to their products and business offerings, recent developments undertaken by them, and key growth strategies adopted by them to improve their positions in the iron & steel market.

Key Benefits of Buying the Report

The report is expected to help the market leaders/new entrants in this market share the closest approximations of the revenue numbers of the overall iron & steel market and its segments and subsegments. This report is projected to help stakeholders understand the competitive landscape of the market, gain insights to improve the positions of their businesses and plan suitable go-to-market strategies. The report also aims to help stakeholders understand the pulse of the market and provides them with information on the key market drivers, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Rising steel consumption in energy & power and automotive industries), restraints (Volatile raw material prices), opportunities (Growing investments and government support in emerging economies), and challenges (Global climate change and environmental degradation due to fossil fuel combustion) influencing the growth of the iron & steel market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the iron & steel market

Market Development: Comprehensive information about profitable markets - the report analyzes the iron & steel market across regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the iron & steel market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like as ArcelorMittal (Luxembourg), China Baowu Steel group Corporation Limited (China ), TATA Steel (India), JSW (India), Nucor Corporation (US) , NIPPON STEEL CORPORATION (Japan), Ansteel Group Corporation Limited (China), POSCO (UK), HBIS Group (China), and SAIL (India) and others in the iron & steel market. The report also helps stakeholders understand the pulse of the iron & steel market and provides them with information on the key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNITS CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.1.2 List of secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key primary participants

2.1.2.2 Key data from primary sources

2.1.2.3 Breakdown of interviews with experts

2.1.2.4 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 TOP-DOWN APPROACH

2.2.2 BOTTOM-UP APPROACH

2.3 BASE NUMBER CALCULATION

2.3.1 SUPPLY-SIDE APPROACH

2.4 GROWTH FORECAST

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 FACTOR ANALYSIS

2.8 RESEARCH LIMITATIONS

2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN IRON & STEEL MARKET

4.2 IRON & STEEL MARKET, BY TYPE

4.3 IRON MARKET, BY PRODUCTION TECHNOLOGY

4.4 STEEL MARKET, BY PRODUCTION TECHNOLOGY

4.5 IRON & STEEL MARKET, BY END-USE INDUSTRY

4.6 ASIA PACIFIC: IRON & STEEL MARKET, BY TYPE AND COUNTRY

4.7 IRON & STEEL MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Abundance of iron ore & other minerals for steel production

5.2.1.2 Rapid urbanization

5.2.1.3 Rising steel consumption in energy & power and automotive industries

5.2.2 RESTRAINTS

5.2.2.1 Vulnerability of construction industry to crisis

5.2.2.2 Volatile raw material prices

5.2.3 OPPORTUNITIES

5.2.3.1 Transition toward net-zero steel

5.2.3.2 Growing investments and government support in emerging economies

5.2.4 CHALLENGES

5.2.4.1 Environmental challenge

5.2.4.2 Problem of excess capacity

6 INDUSTRY TRENDS

6.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.2 ECOSYSTEM ANALYSIS

6.3 VALUE CHAIN ANALYSIS

6.3.1 RAW MATERIAL SUPPLIERS

6.3.2 MANUFACTURERS

6.3.3 DISTRIBUTORS

6.3.4 END USERS

6.4 TARIFF AND REGULATORY LANDSCAPE

6.4.1 TARIFF ANALYSIS (HS CODE: 72)

6.4.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.4.3 KEY REGULATIONS

6.4.3.1 Bureau of Indian Standards (BIS) - IS Standards for Steel Products

6.4.3.2 ASTM International - Steel Standards

6.4.3.3 European Norms (EN) - Steel Harmonized Standards

6.4.3.4 Import Monitoring and Analysis System (IMAS) - US Department of Commerce

6.5 PRICING ANALYSIS

6.5.1 PRICING ANALYSIS BASED ON REGION

6.6 TRADE ANALYSIS

6.6.1 EXPORT SCENARIO (HS CODE 72)

6.6.2 IMPORT SCENARIO (HS CODE 72)

6.7 TECHNOLOGY ANALYSIS

6.7.1 KEY TECHNOLOGIES

6.7.1.1 Hydrogen steel plant

6.7.1.2 Organic Rankine Cycle

6.7.2 COMPLEMENTARY TECHNOLOGIES

6.7.2.1 HYBRIT process

6.7.2.2 Potato-based biodegradable foam

6.8 CASE STUDY ANALYSIS

6.9 PATENT ANALYSIS

6.9.1 INTRODUCTION

6.9.2 METHODOLOGY

6.9.3 IRON & STEEL MARKET, PATENT ANALYSIS (2015-2024)

6.10 KEY CONFERENCES AND EVENTS, 2025-2026

6.11 INVESTMENT AND FUNDING SCENARIO

6.12 IMPACT OF GEN AI ON IRON & STEEL

6.12.1 INTEGRATING AI IN IRON & STEEL

6.12.2 BEST PRACTICES TO LEVERAGE AI FOR IRON & STEEL MARKET

6.12.3 USE CASES OF GENERATIVE AI IN IRON & STEEL MARKET

6.12.3.1 Future of generative AI in iron & steel market

6.13 PORTER'S FIVE FORCES ANALYSIS

6.13.1 THREAT OF NEW ENTRANTS

6.13.2 THREAT OF SUBSTITUTES

6.13.3 BARGAINING POWER OF SUPPLIERS

6.13.4 BARGAINING POWER OF BUYERS

6.13.5 INTENSITY OF COMPETITIVE RIVALRY

6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.14.2 BUYING CRITERIA

6.15 MACROECONOMIC ANALYSIS

6.15.1 INTRODUCTION

6.15.2 GDP TRENDS AND FORECASTS

6.16 IMPACT OF 2025 US TARIFF ON IRON & STEEL MARKET

6.16.1 INTRODUCTION

6.16.2 KEY TARIFF RATES

6.16.3 PRICE IMPACT ANALYSIS

6.16.4 IMPACT ON COUNTRY/REGION

6.16.4.1 US

6.16.4.2 China

6.16.4.3 Germany

6.16.5 END-USE INDUSTRY IMPACT

7 IRON & STEEL MARKET, BY TYPE

7.1 INTRODUCTION

7.2 IRON

7.2.1 WIDE-SCALE AVAILABILITY OF IRON ORE TO FUEL MARKET GROWTH

7.3 STEEL

7.3.1 SUSTAINABILITY, URBANIZATION, AND DRIVE FOR DECARBONIZATION TO BOOST MARKET

7.3.2 CARBON STEEL

7.3.3 STAINLESS STEEL

7.3.4 ALLOY STEEL

7.3.5 TOOL STEEL

7.3.6 TYPES, BY STEEL FORMING

7.3.6.1 Hot rolled coil

7.3.6.2 Hot rolled plates

7.3.6.3 Cold rolled coils

7.3.6.4 Hot dipped galvanized coils

7.3.6.5 Electro zinc-coated coils

7.3.6.6 Wire rods

7.3.6.7 Sections & beams

8 IRON MARKET, BY PRODUCTION TECHNOLOGY

8.1 INTRODUCTION

8.2 BLAST FURNACE PROCESS

8.2.1 STRONG DEMAND FOR HIGH-QUALITY PIG IRON TO BOOST DEMAND

8.3 DRI PROCESS

8.3.1 ONGOING URBANIZATION AND INFRASTRUCTURE DEVELOPMENT IN EMERGING ECONOMIES TO DRIVE MARKET

9 STEEL MARKET, BY PRODUCTION TECHNOLOGY

9.1 INTRODUCTION

9.2 BASIC OXYGEN FURNACE

9.2.1 HIGH PRODUCTION RATE, LOW NITROGEN CONTENT, AND MINIMAL LABOR REQUIREMENTS TO BOOST MARKET

9.3 ELECTRIC ARC FURNACE

9.3.1 USE OF 100% STEEL SCRAP - COST-EFFECTIVE AND ENERGY-EFFICIENT PROCESS

9.4 OTHER PRODUCTION TECHNOLOGIES

10 STEEL MARKET, BY END-USE INDUSTRY

10.1 INTRODUCTION

10.2 BUILDING & CONSTRUCTION

10.2.1 RISING DEMAND FOR HOUSING, TRANSPORTATION, AND OTHER INFRASTRUCTURE TO DRIVE MARKET

10.3 AUTOMOTIVE & TRANSPORTATION

10.3.1 RISING DEMAND FOR HIGH-STRENGTH STEEL IN AUTOMOTIVE INDUSTRY TO BOOST MARKET

10.4 MECHANICAL EQUIPMENT

10.4.1 RISING DEMAND FROM INDUSTRIAL MACHINERY AND EQUIPMENT MANUFACTURING TO DRIVE STEEL CONSUMPTION

10.5 METAL PRODUCTS

10.5.1 WIDESPREAD USE OF STEEL IN FABRICATED AND FINISHED METAL PRODUCTS TO DRIVE MARKET GROWTH

10.6 OTHER END-USE INDUSTRIES

11 IRON & STEEL MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Smart and sustainable urban construction to drive demand

11.2.2 INDIA

11.2.2.1 Increased manufacturing output and growing purchasing power to drive market

11.2.3 JAPAN

11.2.3.1 New industrial and infrastructure programs to drive steel demand

11.2.4 SOUTH KOREA

11.2.4.1 Clean energy and digital infrastructure initiatives to boost steel demand

11.2.5 REST OF ASIA PACIFIC

11.3 EUROPE

11.3.1 GERMANY

11.3.1.1 Growth fueled by rising infrastructure spending and electric vehicle production

11.3.2 ITALY

11.3.2.1 Transition toward electromobility to drive market

11.3.3 FRANCE

11.3.3.1 Growth of construction sector and government initiatives for automotive industry to drive demand

11.3.4 SPAIN

11.3.4.1 Growing construction and automotive industries to drive market

11.3.5 UK

11.3.5.1 Focus on domestic production of steel to drive market

11.3.6 RUSSIA

11.3.6.1 Russia's infrastructure push faces steel demand challenges amid war and sanctions

11.3.7 REST OF EUROPE

11.4 NORTH AMERICA

11.4.1 US

11.4.1.1 Infrastructure gaps and electric vehicle sales to drive market

11.4.2 CANADA

11.4.2.1 Growing residential and non-residential construction activities to drive market

11.4.3 MEXICO

11.4.3.1 High investment in infrastructure and automotive manufacturing to drive market

11.4.4 REST OF NORTH AMERICA

11.5 MIDDLE EAST & AFRICA

11.5.1 GCC COUNTRIES

11.5.1.1 Saudi Arabia

11.5.1.1.1 Saudi Vision 2030 to boost demand for iron and steel in infrastructure development

11.5.1.2 UAE

11.5.1.2.1 Rapid expansion of construction sector to drive market

11.5.1.3 Other GCC countries

11.5.2 SOUTH AFRICA

11.5.2.1 Sustained economic growth driven by private investments to drive market

11.5.3 REST OF MIDDLE EAST & AFRICA

11.6 SOUTH AMERICA

11.6.1 BRAZIL

11.6.1.1 Rapid economic growth and rising automotive demand to drive market

11.6.2 ARGENTINA

11.6.2.1 Infrastructure and industrial expansion to drive market

11.6.3 REST OF SOUTH AMERICA

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES

12.3 MARKET SHARE ANALYSIS

12.4 REVENUE ANALYSIS

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 PRODUCT/BRAND COMPARISON ANALYSIS

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Region footprint

12.7.5.3 Type footprint

12.7.5.4 Iron production technology footprint

12.7.5.5 Steel production technology footprint

12.7.5.6 End-use industry footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024