캐슈넛 껍질액 시장 : 용도별, 제품 유형별, 추출 공정별, 등급별, 지역별 예측(-2030년)

Cashew Nutshell Liquid Market by Product, Application, Region - Global Forecast to 2030

상품코드:1787258

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

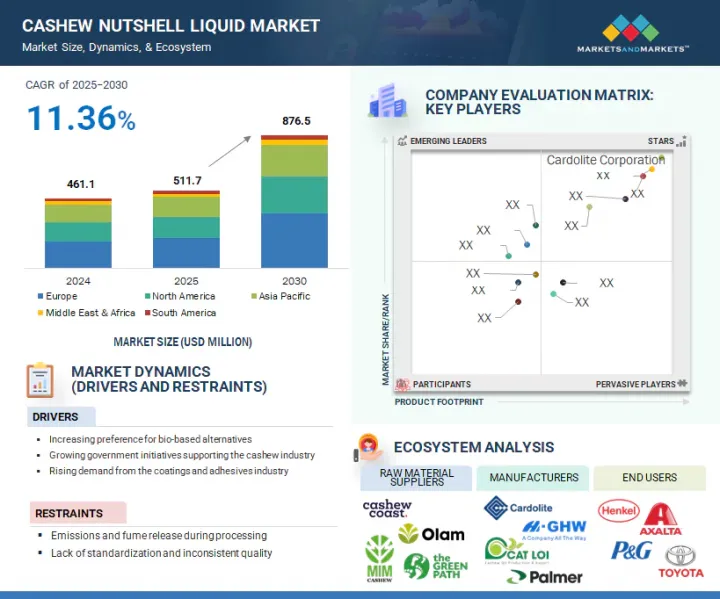

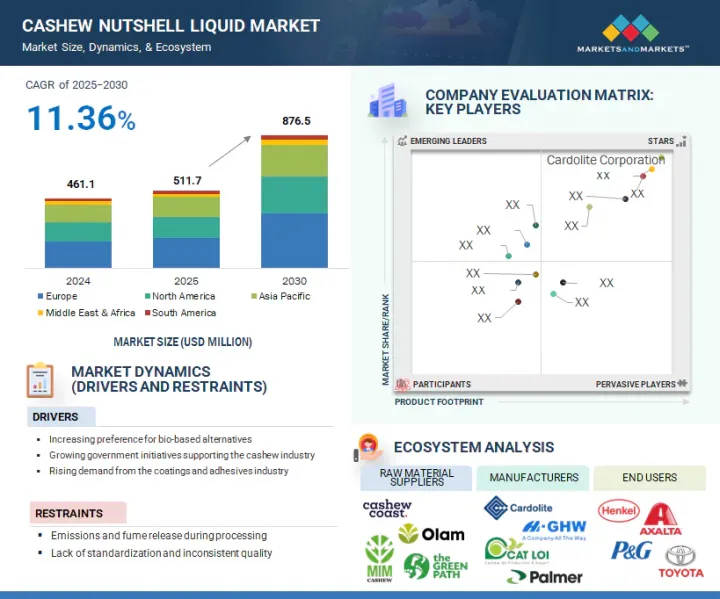

세계의 캐슈넛 껍질액 시장 규모는 2025년부터 2030년까지 성장률 11.36%로 예상되며, 2030년에는 8억 7,650만 달러에 달할 것으로 예측되고 있습니다.

조사 범위

조사 대상 연도

2020-2030년

기준연도

2024년

예측 기간

2025-2030년

대상 유닛

금액(100만 달러) 및 킬로톤

부문

용도별, 제품 유형별, 추출 공정별, 등급별, 지역별

대상 지역

아시아태평양, 유럽, 북미, 중동, 아프리카, 남미

접착제, 코팅, 폼, 단열재, 계면활성제, 라미네이트 등의 용도로 높은 수요를 획득하고 있습니다. 이 중 코팅제는 2024년 1억 3,000만 달러로 가장 높은 점유율을 차지했으며 접착제는 1억 1300만 달러였습니다. 캐슈넛 껍질액(CNSL)은 환경 친화적이고 재생 가능하며 열적 및 화학적 안정성이 높으며 많은 중합체 및 수지와 상용성이 있는 것이 CNSL을 주성분으로하는 코팅제 및 접착제의 주요 특징이며 시장 수요를 결정하고 있습니다.

CNSL에 포함된 페놀 화합물은 접착 강도와 내구성을 향상시키기 위해 자동차, 건축, 전자 분야에서 이상적인 성능을 발휘합니다. 또한 환경문제와 석유계 화학물질에 대한 규제압력이 높아짐에 따라 제조업체의 선호도가 CNSL과 같은 바이오 제품으로 바뀌기 시작했습니다. 또한 지속가능하고 비용 효율적인 재료가 산업제품과 소비자제품의 배합에 있어서 호감을 얻고 있는 것도 성장의 요인이 되고 있습니다.

페놀포름알데히드(PF) 수지는 2024년 CNSL 시장에서 제품 유형별 점유율로 7,630만 달러로 가장 크며, 에폭시 개질제 및 수지 및 경화제가 각각 7,620만 달러와 7,590만 달러로 약간 차이가 납니다. CNSL의 반응성 페놀 구조를 이용할 수 있는 제품 유형도 있어, 수지나 플라스틱의 배합에 있어서, 강력하고 유연한 화학 중간체로서 사용할 수 있습니다.

일렉트로닉스 산업에서 자동차 산업, 그리고 건설 산업으로 이어지는 제조업에서는 고성능으로 내열성이 뛰어나 지속 가능한 재료에 대한 요구가 높아지고 있으며, CNSL 유래의 PF나 에폭시 수지의 사용이 가속되고 있습니다. 특히 CNSL 기반 경화제는 저독성과 생분해성의 장점이 있기 때문에 기존의 아민 기반 시스템을 대체하는 안전한 옵션으로 인기가 높아지고 있습니다. 또한 폴리올 & NCO 차단제와 마찰재는 브레이크 라이닝, 클러치, 폴리우레탄 폼에 중요한 역할을 하기 때문에 수요가 높아지고 있습니다. 고성능 제품의 원료로서 바이오 원료를 사용하는 것에 대한 관심이 높아지고 있는 가운데, CNSL 기반 제품은 기존 원료를 대체하는 완벽한 녹색 대체품이며 세계가 요구하는 지속가능성 요구에 부응합니다.

유럽 시장은 가장 중요한 지역 CNSL 시장입니다. 그 주된 이유는 환경에 대한 엄격한 정책, 이미 개발된 제조 시설, 바이오 화학 물질의 적극적인 추구입니다. 특히 자동차, 건설, 전자산업에 있어서의 코팅제, 접착제, 에폭시 시스템, 마찰재 등의 용도로, 이 지역 수요에 일관성을 볼 수 있습니다. EU의 녹색 거래 및 순환 경제 지표는 석유 원료에 대한 의존성을 CNSL과 같은 재생 가능한 자원으로 대체합니다.

독일, 프랑스, 네덜란드에서는 제조업체가 CNSL에 포함된 페놀분의 재생가능성을 이용하여 포름알데히드를 포함하지 않고 휘발성 유기화합물(VOC)이 적고 환경에 무해한 수지, 도료, 단열재를 제조하고 있습니다. 또한 자동차 마찰재(브레이크 패드, 클러치 플레이트 등)에 CNSL을 사용하는 것은 유럽의 자동차 기술 혁신 동향과 이산화탄소 배출 감소 정책에도 적합합니다.

본 보고서에서는 세계의 캐슈넛 껍질 시장에 대해 조사했으며, 용도별, 제품 유형별, 추출 공정별, 등급별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

거시경제지표

제6장 업계 동향

공급망 분석

가격 분석

고객사업에 영향을 주는 동향/혼란

생태계 분석

기술 분석

사례 연구 분석

무역 분석

규제 상황

2025-2026년의 주된 회의와 이벤트

투자 및 자금조달 시나리오

특허 분석

2025년 미국 관세의 영향-개요

AI/생성형 AI가 CNSL 시장에 미치는 영향

제7장 캐슈넛 껍질액(CNSL) 시장(용도별)

소개

접착제

코팅제

발포재 및 단열재

라미네이트

마찰 라이닝

퍼스널케어

연료

기타

제8장 캐슈넛 껍질액(CNSL) 시장(제품 유형별)

소개

페놀포름알데히드(PF) 수지

에폭시 개질제 및 수지

에폭시 경화제

계면활성제

폴리올 및 NCO 블로킹제

마찰재

기타

제9장 캐슈넛 껍질액(CNSL) 시장(추출 공정별)

소개

기계 추출 공정

용매 추출 공정

화학 추출 공정

제10장 캐슈넛 껍질액(CNSL) 시장(그레이드별)

소개

주요 특징

제11장 캐슈넛 껍질액(CNSL) 시장(지역별)

소개

아시아태평양

중국

인도

일본

한국

인도네시아

베트남

북미

미국

멕시코

캐나다

유럽

독일

프랑스

영국

이탈리아

네덜란드

남미

브라질

중동 및 아프리카

GCC 국가

남아프리카

제12장 경쟁 구도

소개

주요 진입기업의 전략 및 강점

시장 점유율 분석, 2024년

2020-2024년의 최상위 5대 기업 수익 분석

기업평가 매트릭스 : 주요 진입기업, 2024년

기업평가 매트릭스 : 스타트업 및 중소기업, 2024년

브랜드 및 제품 비교 분석

기업평가와 재무지표

경쟁 시나리오

제13장 기업 프로파일

주요 진출기업

CARDOLITE CORPORATION

GHW(VIETNAM) CO., LTD

PALMER INTERNATIONAL

LC BUFFALO CO. LTD.

CAT LOI CASHEW OIL PRODUCTION & EXPORT JOINT STOCK COMPANY(CAT LOI)

ZHEJIANG WANSHENG CO., LTD.

CASHEW CHEM INDIA

SRI DEVI GROUP

ADMARK POLYCOATS PVT. LTD.

GOLDEN CASHEW PRODUCTS PVT. LTD.

기타 기업

PALADIN PAINTS & CHEMICALS PVT. LTD

SATYA CASHEW CHEMICALS PRIVATE LIMITED

K2P CHEMICALS

ZANTYE AGRO INDUSTRIES

SON CHAU CO.,LTD

SHIVAM CASHEW INDUSTRY

HUNG LOC PHAT CASHEW OIL CO. LTD.

KUMARASAMY INDUSTRIES

MIRAE GREEN CHEMICAL CO., LTD.

VIKO BIOFUEL COMPANY LIMITED

THINH DAI CHEMICAL

PT COMEXTRA MAJORA

CUONG THINH CASHEW OIL PRODUCTION COMPANY LIMITED

CNSL INDUSTRIAL CO., LTD.

TAN LOC CASHEW OIL PRODUCTION COMPANY LIMITED

제14장 인접 시장과 관련 시장

소개

제한 사항

코팅 수지 시장

코팅 수지 시장(지역별)

제15장 부록

JHS

영문 목차

영문목차

The CNSL market is expected to grow at a rate of 11.36% between 2025 and 2030, projected to be USD 876.5 million globally by 2030.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Product Type, Application, and Region

Regions covered

Asia Pacific, Europe, North America, Middle East & Africa, and South America

It is gaining high demand in the following applications, i.e., adhesives, coatings, foams, insulation, surfactants, and laminates. Of these, coatings had the highest share of USD 130.0 million in 2024 and that of the adhesives was USD 113.0 million. Its eco-friendly, renewable character, high thermal and chemical stability, compatibility with numerous polymers and resins are the main qualities of CNSL-based coatings and adhesives which predetermine their demand in the market.

The phenolic compounds present in CNSL enhance the outcomes of better bonding strength and durability, which makes it ideal in the automotive, construction, and electronics sectors. Besides, environmental issues and increased regulatory pressure of petroleum-based chemicals have started changing preferences among manufacturers to bio-based products like CNSL. The growth is also devoid of the fact that sustainable and cost-effective materials are gaining positive affinities in the industrial and consumer product formulations.

"Phenol formaldehyde resins and epoxy systems were leading product types in the CNSL market, 2024"

Phenol Formaldehyde (PF) resins have the largest share of CNSL market by product type valued at USD 76.3 million in 2024 and are closely followed by epoxy modifiers & resins and curing agents with a value of USD 76.2 million and USD 75.9 million, respectively. There are such product types which can take advantage of CNSL reactive phenolic structure, so that it could be used as a strong and flexible chemical intermediating in resin and plastic compounding.

The escalating need for high performance, heat-resistant and sustainable materials in the manufacturing industries starting with electronics to automotive industries then to construction industries is boosting the use of the CNSL-derived PF and epoxy systems. Specifically, CNSL-based curing agents are picking up popularity as they have the advantage of low toxicity and biodegradability, and thus, they can substitute the traditional amine-based systems offering a safer option. Also, polyols & NCO blocking agents and friction materials are experiencing high demand because they are important in brake linings, clutches, and polyurethane foams. With the growing interest of industries in the use of bio-based feedstocks as raw materials in making high-performance products, CNSL-based products come as perfect green alternatives to existing raw materials which meet the demands of sustainability that the world is gearing toward.

"Europe dominated the global CNSL market in 2024, driven by sustainable regulations and industrial innovation"

The European market is the most significant regional CNSL market. This is principally because of its strict policies on environment, the already developed manufacturing facilities and its active pursuit of bio-based chemicals. Consistency has been witnessed in the demand for the region in applications, such as coatings, adhesives, epoxy systems, and friction materials, especially in automotive, construction, and electronic industries. Green Deal and circular economy indicators in the EU with reliance on petroleum-based raw materials have been replaced by renewable sources such as CNSL.

In Germany, France, and the Netherlands, manufacturers are also taking advantage of the renewability of the phenolic content in CNSL to compile resins, coatings, and insulation materials that are free of formaldehyde and low in volatile organic compounds (VOCs), as well as environmentally harmless. In addition to this, the use of CNSL in automotive friction materials (such as brake pads, clutch plates) also suits well the trend of automotive innovations in Europe and its policy toward carbon emission reductions.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the CNSL marketplace.

By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

By Designation: Directors - 50%, Managers - 30%, and Others - 20%

By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, Rest of the World - 5%

The key players profiled in the report include Cardolite Corporation (US), GHW (Vietnam) Co. Ltd., Palmer International (US), LC Buffalo Co.Ltd. (Vietnam), Cat Loi Cashew Oil Production & Export Joint Stock Company (Vietnam), Senese (Poland), Zhejiang Wansheng Co., Ltd. (China), Cashew Chem India (India), Sri Devi Group (India), and ADMARK Polycoats Pvt. Ltd. (India).

Research Coverage

This report segments the market for CNSL based on product type, application, and region and provides estimations of value (USD Million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies, associated with the market for CNSL.

Reasons to Buy this Report

This research report is focused on various levels of analyses - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the CNSL market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights into the following points:

Market Penetration: Comprehensive information on CNSL offered by top players in the global market.

Analysis of key drivers: (Increasing preference for bio-based alternatives, growing government initiatives supporting the cashew industry) restraints (Emissions and fume release during processing, lack of standardization and inconsistent quality) opportunities (CNSL biofuel blends for marine fuel) and challenges (availability of substitutes) influencing the growth of CNSL market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the CNSL market.

Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for CNSL across regions.

Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global CNSL market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the CNSL market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 MARKET DEFINITION AND INCLUSIONS, BY PRODUCT TYPE

1.3.4 MARKET DEFINITION AND INCLUSIONS, BY APPLICATION

1.3.5 YEARS CONSIDERED

1.3.6 CURRENCY CONSIDERED

1.3.7 UNITS CONSIDERED

1.4 STAKEHOLDERS

1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Key primary participants

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 GROWTH FORECAST

2.4.1 SUPPLY-SIDE ANALYSIS

2.4.2 DEMAND-SIDE ANALYSIS

2.5 ASSUMPTIONS

2.6 LIMITATIONS

2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CNSL MARKET

4.2 CNSL MARKET, BY REGION

4.3 ASIA PACIFIC: CNSL MARKET, BY APPLICATION AND COUNTRY

4.4 CNSL MARKET, BY APPLICATION AND REGION

4.5 CNSL MARKET, BY KEY COUNTRIES

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing preference for bio-based alternatives

5.2.1.2 Growing government initiatives supporting cashew industry

5.2.1.3 Rising demand from coatings and adhesives industries

5.2.2 RESTRAINTS

5.2.2.1 Emissions and fume release during processing

5.2.2.2 Lack of standardization and inconsistent quality

5.2.3 OPPORTUNITIES

5.2.3.1 CNSL biofuel blends for marine fuel

5.2.3.2 R&D in CNSL applications accelerating commercial adoption

5.2.4 CHALLENGES

5.2.4.1 Availability of substitutes

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 INTENSITY OF COMPETITIVE RIVALRY

5.3.2 BARGAINING POWER OF BUYERS

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 THREAT OF SUBSTITUTES

5.3.5 THREAT OF NEW ENTRANTS

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES, 2021-2030

6 INDUSTRY TRENDS

6.1 SUPPLY CHAIN ANALYSIS

6.1.1 RAW MATERIAL SUPPLIERS

6.1.2 MANUFACTURERS

6.1.3 DISTRIBUTION NETWORKS

6.1.4 END-USE INDUSTRIES

6.2 PRICING ANALYSIS

6.2.1 AVERAGE SELLING PRICE OF CNSL OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

6.2.2 AVERAGE SELLING PRICE TREND OF CNSL, BY REGION, 2022-2030

6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.4 ECOSYSTEM ANALYSIS

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGIES

6.5.1.1 Cardanol-derived epoxy compounds and modifiers

6.5.1.2 CNSL-based polyols for polyurethane systems

6.5.1.3 Integrated extraction, refinement, and blending technology for CNSL-based marine fuels

6.5.2 COMPLEMENTARY TECHNOLOGIES

6.5.2.1 Bio-based epoxy resins from glycerol and sugar derivatives

6.5.2.2 Advanced extraction and catalytic processing

6.6 CASE STUDY ANALYSIS

6.6.1 CNSL BIOFUEL'S ROLE IN DECARBONIZING MARINE TRANSPORT

6.6.2 REPLACING VOC-HEAVY EPOXIES WITH CNSL-BASED PHENALKAMINES

6.7 TRADE ANALYSIS

6.7.1 IMPORT SCENARIO (HS CODE 1302)

6.7.2 EXPORT SCENARIO (HS CODE 1302)

6.8 REGULATORY LANDSCAPE

6.8.1 GLOBAL: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.8.2 REGULATORY FRAMEWORK

6.8.2.1 REACH Regulation (European Union)

6.8.2.2 Circular Economy Action Plan (European Union)

6.8.2.3 Clean Air Act (US)

6.8.2.4 TSCA (Toxic Substances Control Act) (US)

6.8.2.5 ISO 9001 and ISO 14001 Standards (Global)

6.9 KEY CONFERENCES AND EVENTS, 2025-2026

6.10 INVESTMENT AND FUNDING SCENARIO

6.11 PATENT ANALYSIS

6.11.1 APPROACH

6.11.2 DOCUMENT TYPES

6.11.3 TOP APPLICANTS

6.11.4 JURISDICTION ANALYSIS

6.12 IMPACT OF 2025 US TARIFF - OVERVIEW

6.12.1 INTRODUCTION

6.12.2 KEY TARIFF RATES

6.12.3 PRICE IMPACT ANALYSIS

6.12.4 IMPACT ON COUNTRY/REGION

6.12.4.1 US

6.12.4.2 Europe

6.12.4.3 Asia Pacific

6.12.5 IMPACT ON APPLICATION SECTORS

6.13 IMPACT OF AI/GEN AI ON CNSL MARKET

7 CASHEW NUTSHELL LIQUID MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 ADHESIVES

7.2.1 WATER, CHEMICAL, THERMAL, SHOCK RESISTANCE, AND EXCELLENT MECHANICAL PROPERTIES TO BOOST GROWTH

7.3 COATINGS

7.3.1 HIGH DEMAND FOR ANTI-CORROSIVE PROTECTIVE COATINGS TO DRIVE MARKET

7.4 FOAMS & INSULATION

7.4.1 EXCELLENT PROCESSING, DIMENSIONAL STABILITY, AND UNIFORM STRUCTURE TO FUEL GROWTH

7.5 LAMINATES

7.5.1 SUPERIOR MOISTURE RESISTANCE AND HIGHER FLEXIBILITY TO PROPEL MARKET

7.6 FRICTION LININGS

7.6.1 NEED TO INCREASE FRICTION, REDUCE ROTOR WEAR, AND CONTROL NOISE TO BOOST MARKET

7.7 PERSONAL CARE

7.7.1 INCREASING DISPOSABLE INCOME TO DRIVE DEMAND

7.8 FUELS

7.8.1 ENHANCED FUEL STABILITY, REDUCED ENGINE WEAR, AND IMPROVED COMBUSTION EFFICIENCY TO BOOST GROWTH

7.9 OTHER APPLICATIONS

8 CASHEW NUTSHELL LIQUID MARKET, BY PRODUCT TYPE

8.1 INTRODUCTION

8.2 PHENOL FORMALDEHYDE (PF) RESINS

8.2.1 GROWING CONSUMER AND INDUSTRY PREFERENCE FOR GREEN CHEMISTRY AND REDUCED ENVIRONMENTAL IMPACT TO FUEL ADOPTION

8.3 EPOXY MODIFIERS & RESINS

8.3.1 EXCELLENT WATER RESISTANCE AND HIGHER FLEXIBILITY TO SUPPORT MARKET GROWTH

8.4 EPOXY CURING AGENTS

8.4.1 DEMAND FOR INDUSTRIAL, MARINE, PROTECTIVE COATINGS, TRANSPORTATION, AND FLOORING APPLICATIONS TO DRIVE MARKET

8.5 SURFACTANTS

8.5.1 GROWING DEMAND IN PERSONAL CARE FOR SAFETY TO BOOST MARKET GROWTH

8.6 POLYOLS & NCO BLOCKING AGENTS

8.6.1 IMPROVED PERFORMANCE AND DESIRED PROPERTIES OF END-USE PRODUCTS TO FUEL GROWTH

8.7 FRICTION MATERIALS

8.7.1 INCREASING DEMAND IN AUTOMOTIVE INDUSTRY TO BOOST MARKET

8.8 OTHER PRODUCT TYPES

9 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY EXTRACTION PROCESS

9.1 INTRODUCTION

9.1.1 MECHANICAL EXTRACTION PROCESS

9.1.2 SOLVENT EXTRACTION PROCESS

9.1.3 CHEMICAL EXTRACTION PROCESS

10 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY GRADE

10.1 INTRODUCTION

10.1.1 KEY CHARACTERISTICS

10.1.1.1 Raw CNSL

10.1.1.2 Degummed CNSL

10.1.1.3 Refined CNSL

10.1.1.4 Distilled CNSL

11 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Growing demand for processed and semi-processed CNSL products to drive market

11.2.2 INDIA

11.2.2.1 Rising middle-class population, rapid urbanization, and continuous influx of multinational companies to boost market

11.2.3 JAPAN

11.2.3.1 Demand from automobile industry to fuel market

11.2.4 SOUTH KOREA

11.2.4.1 Increasing demand for bio-based products from electronic and automotive industries to support growth

11.2.5 INDONESIA

11.2.5.1 Rapid industrialization and rising consumer spending to propel market

11.2.6 VIETNAM

11.2.6.1 Significant global exports to propel growth

11.3 NORTH AMERICA

11.3.1 US

11.3.1.1 Rising environmental concerns and regulations to meet zero-emission norms to boost growth

11.3.2 MEXICO

11.3.2.1 Rising demand for coatings and adhesives to influence market growth

11.3.3 CANADA

11.3.3.1 Growing environmental concerns over petroleum-based products to support market growth

11.4 EUROPE

11.4.1 GERMANY

11.4.1.1 Growing developments and investments in chemical industry and exports to drive growth

11.4.2 FRANCE

11.4.2.1 Increasing investments in renewable energy sector to boost market

11.4.3 UK

11.4.3.1 Stringent environmental standards to drive market growth

11.4.4 ITALY

11.4.4.1 Growing automotive sector to drive market

11.4.5 NETHERLANDS

11.4.5.1 Demand in coatings, electrical and electronics, and construction to boost market

11.5 SOUTH AMERICA

11.5.1 BRAZIL

11.5.1.1 Strong export activity and industrial growth to drive market

11.6 MIDDLE EAST & AFRICA

11.6.1 GCC COUNTRIES

11.6.1.1 UAE

11.6.1.1.1 Infrastructural projects to provide growth opportunities

11.6.1.2 Saudi Arabia

11.6.1.2.1 Rising demand from infrastructure, transportation, and manufacturing sectors to boost market

11.6.2 SOUTH AFRICA

11.6.2.1 Private sector investments to fuel market growth

12 COMPETITIVE LANDSCAPE

12.1 INTRODUCTION

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

12.3 MARKET SHARE ANALYSIS, 2024

12.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2024

12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.5.1 STARS

12.5.2 EMERGING LEADERS

12.5.3 PERVASIVE PLAYERS

12.5.4 PARTICIPANTS

12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.5.5.1 Company footprint

12.5.5.2 Region footprint

12.5.5.3 Product type footprint

12.5.5.4 Application footprint

12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024