Photovoltaics (PV) Films Market by Raw material (EVA, PVB, POE), Application (Ground-mounted PV, Building-integrated PV) - Forecast to 2034

상품코드:1786132

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 234 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

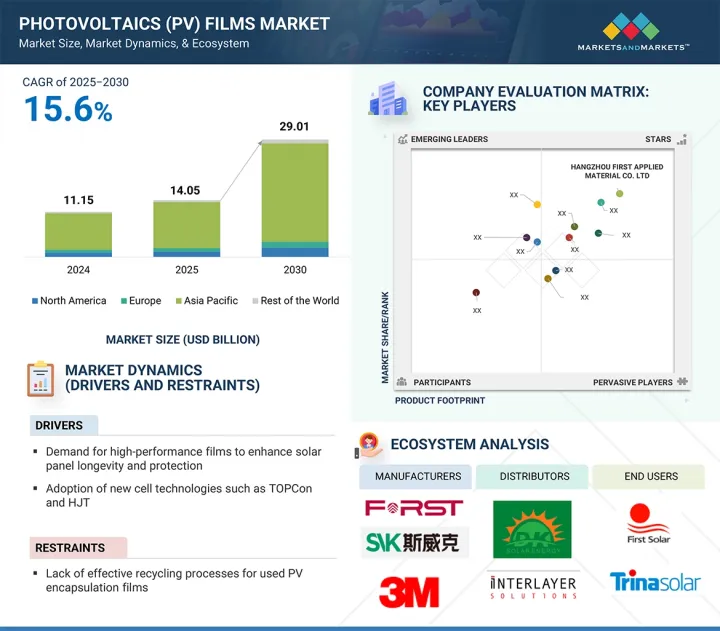

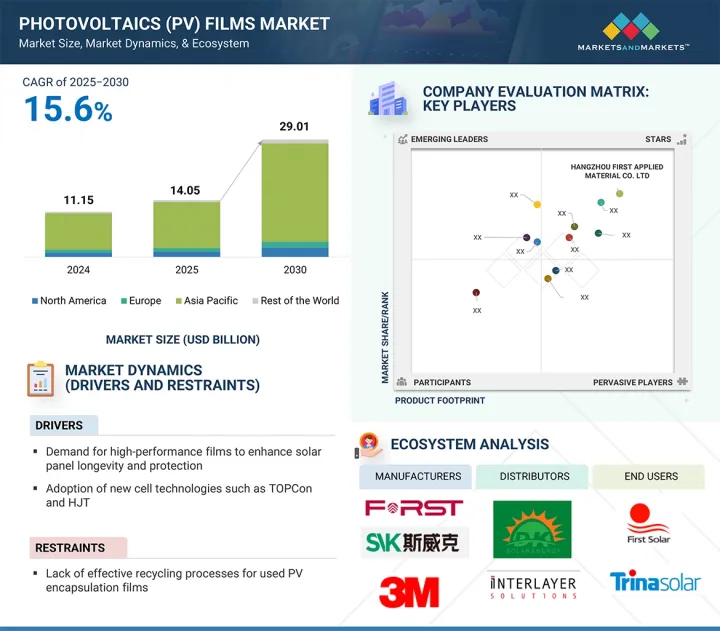

태양광발전(PV) 필름 시장 규모는 2025년 140억 5,000만 달러에서 2030년에는 290억 1,000만 달러로 성장할 전망이며, 예측 기간 중 CAGR 15.6%로 성장할 것으로 예측됩니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2034년

검토 단위

금액(100만 달러/10억 달러)과 수량

부문

원재료별, 용도별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

국가와 산업계가 저탄소 에너지 시스템을 추진하는 가운데, 지속가능성이 점점 중시되고 있습니다. 최근의 재료 동향은 새로운 밀봉 재료, 즉 EVA에서 폴리비닐부티랄(PVB) 및 열가소성 폴리 우레탄(TPU)과 같은 비 EVA 재료로의 전환이 있습니다. 이것은 각국이 직면한 극단적인 기후 조건 때문에 중요하며, 이러한 밀봉재는 우수한 자외선 안정성 및 탁월한 기계적 강도를 가지고 있습니다. 또한 가볍고 유연한 밀봉 필름도 등장하며, 특히 건물 일체형 태양광발전(BIPV) 시스템 및 오프 그리드 시스템에서의 용도와 관련이 있습니다.

폴리올레핀계 엘라스토머(POE)는 EVA 등의 기존 재료에 비해 우수한 성능 특성을 갖고 있기 때문에 태양광발전 필름 시장에서 가장 급성장하고 있는 제품 부문으로 계속되고 있습니다. POE의 급성장 배경에는 많은 요인이 있지만, 가장 큰 이유 중 하나는 POE 필름의 뛰어난 내습성이며, 이는 습도가 높은 고전압 환경에서 사용할 때 잘 알려진 위험인 전위 유도 열화(PID)의 가능성을 낮추는 것입니다. 또한 POE는 열 안정성 및 자외선 안정성이 뛰어나 태양전지판의 투명층이 오래 지속되기 때문에 특히 가혹한 기상 환경에서 높은 성능과 내구성을 발휘합니다. POE는 유틸리티 스케일 태양광 프로젝트에 항상 도입되는 이면체 모듈 및 고효율 태양전지 등 대부분의 최신 모듈 기술에 특히 적합합니다.

지상 설치형 PV 시스템은 유틸리티 규모 및 대규모 상업용 태양광발전 프로젝트에서 널리 볼 수 있기 때문에 태양광발전 필름 시장에서 가장 급성장하고 있는 분야입니다. 지상 설치형 태양광발전 시스템은 주로 그늘이 없는 오픈 스페이스에 대용량 어레이를 설치하므로 일괄 발전에 최적입니다. 많은 지역에서는 중국, 인도, 미국, 중동 국가 등 신흥 경제 국가와 에너지 대 소비국이 요구하는 깨끗한 재생에너지에 대응하기 위해 대규모 태양광발전소의 개발이 활발히 이루어지고 있습니다. 이에 따라 이러한 태양전지 모듈이 사용되는 가혹한 환경에 대한 장기적인 신뢰성과 보호가 강하게 요구되고 있습니다. 따라서 태양전지 모듈의 사용 장소나 용도에 따라, 특히 자외선, 열, 습기에 대한 노출에 관해서, 수년간 수십년간 신뢰성을 유지할 수 있는 내구성이 있는 고성능 밀봉 필름에 대한 수요가 급선무가 되고 있습니다.

아시아태평양이 태양광발전 필름 시장에서 가장 급성장하고 있는 것은 태양광발전 용량의 급성장, 정부의 지원, 견고한 제조 생태계가 배경에 있습니다. 이 지역, 특히 중국, 인도, 일본, 한국의 태양전지 용량 증가는 이산화탄소 배출량 감축, 에너지 수요 증가, 에너지 자급 강화가 원동력이 되고 있습니다. 중국은 태양전지판의 가장 큰 생산국이자 소비국이기도 하며, 태양광발전용 밀봉 필름의 제조를 포함한 세계 공급망의 중요한 지역이기도 합니다. 호의적인 정책, 보조금, 신재생 에너지 목표는 이 지역 전체에서 태양광발전 확대에 박차를 가하고 있습니다. 한편 인도에서는 국가 솔라 미션이나 각 주의 우대 조치 등 정부의 시책이 공공시설이나 옥상에서의 태양광발전 프로젝트를 뒷받침하고 있습니다. 풍부한 일조량, 저비용의 노동력, 아시아태평양 전역에서의 태양광발전에 대한 대처의 고조가 조합되고 있는 것도, 태양광발전용 필름 시장에 있어서 좋은 재료가 되고 있습니다. 또한 아시아태평양에는 많은 주요 봉지재 필름 제조업체가 존재하기 때문에 신제품의 혁신이 촉진되어 가격 효율도 향상되고 있습니다.

본 보고서에서는 세계의 태양광발전(PV) 필름 시장에 대해 조사했으며, 원재료별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

서문

시장 역학

생성형 AI가 태양광발전(PV) 필름 시장에 미치는 영향

제6장 업계 동향

서문

고객 사업에 영향을 주는 동향 및 혼란

공급망 분석

미국 관세가 태양광발전(PV) 필름 시장에 미치는 영향(2025년)

투자 및 자금조달 시나리오

가격 분석

생태계 분석

기술 분석

특허 분석

무역 분석

주된 회의 및 이벤트(2025-2026년)

관세 및 규제 상황

Porter's Five Forces 분석

주요 이해관계자 및 구매 기준

거시 경제 전망

사례 연구 분석

제7장 태양광발전(PV) 필름 시장 : 원재료별

서문

에틸렌 비닐 아세테이트(EVA)

폴리비닐부티랄(PVB)

폴리올레핀 엘라스토머(POE)

기타

제8장 태양광발전(PV) 필름 시장 : 용도별

서문

지상 설치형 태양광발전

건물 일체형 태양광발전

제9장 태양광발전(PV) 필름 시장 : 지역별

서문

아시아태평양

중국

일본

인도

한국

대만

기타

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

프랑스

영국

스페인

러시아

기타

행

사우디아라비아

아랍에미리트(UAE)

오만

이집트

남아프리카

기타

제10장 경쟁 구도

서문

주요 진입기업의 전략 및 강점

시장 점유율 분석

수익 분석

기업 평가 매트릭스 : 주요 진입기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

브랜드 및 제품 비교 분석

기업 평가 및 재무지표

경쟁 시나리오

제11장 기업 프로파일

주요 진출기업

HB FULLER COMPANY

3M

KURARAY CO., LTD.

KO SOLAR TECHNOLOGY CO., LTD.

BOREALIS GMBH

JIANGSU SVECK PHOTOVOLTAIC NEW MATERIAL CO., LTD.

HANGZHOU FIRST APPLIED MATERIAL CO., LTD.

SHANGHAI HIUV NEW MATERIALS CO., LTD.

GUANGZHOU LUSHAN NEW MATERIALS CO., LTD.

BETTERIAL

MITSUI CHEMICALS, INC.

HANWHA GROUP

ZHEJIANG SINOPONT TECHNOLOGY CO., LTD.

CYBRID TECHNOLOGIES INC.

기타 기업

SATINAL SPA

LUCENT CLEANENERGY

THE COMPOUND COMPANY

DR. HANS WERNER CHEMIKALIEN

FILMTEC

CROWN ADVANCED MATERIAL CO., LTD.

HANGZHOU XINDONGKE ENERGY TECHNOLOGY CO., LTD

FELIX NONWOVENS

HUIZHOU BAOJUN MATERIAL TECHNOLOGY CO., LTD

DANA POLY, INC.

VISHAKHA RENEWABLES PVT. LTD.

NOVOPOLYMERS

ENRICH ENCAP PVT. LTD.

ZHEJIANG FEIYU NEW ENERGY CO., LTD.

FUYIN GROUP

제12장 부록

AJY

영문 목차

영문목차

The photovoltaics (PV) films market size is projected to grow from USD 14.05 billion in 2025 to USD 29.01 billion by 2030, registering a CAGR of 15.6% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2034

Units Considered

Value (USD Million/Billion) and Volume

Segments

Raw Material, Application, and Region

Regions covered

North America, Europe, Asia Pacific, Rest of the World

The main driver is the increasing emphasis on sustainability, as countries and industries push for low-carbon energy systems, which require durable encapsulants for solar panels for long-lasting energy production and efficiency. Recent material trends include new encapsulation materials, namely, the movement away from EVA in favor of non-EVA materials like polyvinyl butyral (PVB) and thermoplastic polyurethane (TPU). It is critical due to the extreme climate conditions faced by the countries, and these encapsulation materials have superior UV stability and outstanding mechanical strength. Lightweight and flexible encapsulation films have also emerged, particularly related to applications in building-integrated photovoltaic (BIPV) systems and off-grid systems.

" POE raw material to account for the fastest-growth of photovoltaics (PV) films market in terms of value, during the forecast period"

Polyolefin elastomers (POEs) continue to be the fastest-growing product segment in the photovoltaics films market due to their superior performance properties when compared with conventional materials such as EVA. While there are many drivers behind POE's rapid growth, one of the biggest reasons is POE film's superior moisture resistance, which leads to a lower likelihood of Potential Induced Degradation (PID), a well-known risk when operating in humid and high-voltage environments. POE is also very thermally stable and UV stable, which contributes to a ,longer-lasting transparent layer on the solar panels for high performance and durability, especially in extreme weather environments. POE is particularly suited for most modern module technologies, including bifacial modules and high-efficiency solar cells, which are constantly deployed in utility-scale solar projects.

"Ground-mounted PV to account for the fastest growth of the photovoltaics (PV) films market in terms of value, during the forecast period"

Ground-mounted PV systems are the fastest-growing segment in the photovoltaic film market because they are widely found in utility-scale and large commercial solar projects. Ground-mounted PV systems are mainly found in open and unshaded spaces with high-capacity arrays, making them ideally suited to create bulk power. In many regions, active development of utility-scale solar farms is occurring to meet the clean renewable energy requirements from emerging economies and large energy consumers, such as China, India, the US, and countries in the Middle East. Subsequently, there is a strong demand for long-term reliability and protection against the harsh environment in which these solar modules are utilized. Therefore, there is a pressing demand for durable, high-performance encapsulation films for solar modules that will provide reliability for many years or decades, depending on the location and use of the module, specifically with respect to exposure to UV rays, heat, and moisture.

"Asia Pacific is projected to be the fastest-growing region in the photovoltaics (PV) films market in terms of value, during the forecast period"

Asia Pacific is the fastest-growing region in the photovoltaics films market because of the rapidly growing solar energy capacity, government support, and a robust manufacturing ecosystem. Growing solar capacity in the region, particularly in China, India, Japan, and South Korea, is driven by reducing carbon emissions, increasing energy demands, and bolstering energy independence. China is the largest producer and consumer of solar panels and an integral player in the global supply chain, which includes the manufacture of photovoltaic encapsulation films. Favorable policies, subsidies, and renewable energy targets are fueling the expansion of solar across the region. Meanwhile, government action, such as the National Solar Mission and state incentives, are driving utility-scale and rooftop solar projects in India. The combination of abundant sunlight, low-cost labor, and a growing commitment to solar across the Asia Pacific is also a boon for the photovoltaics films market. Additionally, Asia Pacific includes many leading encapsulant film manufacturers, which facilitate new product innovation and support pricing efficiencies.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the photovoltaics films market, and information was gathered from secondary research to determine and verify the market size of several segments.

By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

By Designation: Managers- 15%, Directors - 20%, and Others - 65%

By Region: North America - 30%, Europe - 20%, Asia Pacific - 40%, Rest of the World - 10%.

The Photovoltaics (PV) Films market comprises major players, such as H.B. Fuller Company (US), 3M (US), Kuraray Co., Ltd (Japan), JA SOLAR Technology Co., Ltd. (China), Borealis AG (Austria)., Jiangsu Sveck Photovoltaic New Material Co., Ltd (China), HANGZHOU FIRST APPLIED MATERIAL CO.,LTD. (China), Shanghai HIUV New Materials Co.,Ltd. (China), Guangzhou Lushan New Materials Co., Ltd. (China), Betterial (China), Mitsui Chemicals, Inc. (Japan), Hanwha Group (South Korea), Zhejiang Sinopont Technology Co.,Ltd. (China), and Cybrid Technologies Inc. (China). The study includes in-depth competitive analysis of these key players in the photovoltaic films market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for photovoltaic films market on the basis of raw material, application, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the market for photovoltaic films.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the photovoltaic films market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of drivers: (Demand for high-performance films to enhance solar panel longevity and protection), restraints (Lack of effective recycling process for used photovoltaic films), opportunities (Innovations in encapsulation materials elevate panel efficiency and performance, driving investments), and challenges (Performance Concerns of solar films in regions with climate variability).

Market Penetration: Comprehensive information on the Photovoltaic Films market offered by top players in the Photovoltaic Films market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, product launches, partnerships, agreements, joint ventures, collaborations, announcements, awards, and expansions in the market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for photovoltaic films across regions.

Market Capacity: Production capacities of companies producing photovoltaic films are provided wherever available with upcoming capacities.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the photovoltaic films market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 RESEARCH LIMITATIONS

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key primary sources

2.1.2.3 Key participants for primary interviews

2.1.2.4 Breakdown of interviews with experts

2.1.2.5 Key industry insights

2.2 BASE NUMBER CALCULATION

2.2.1 SUPPLY-SIDE ANALYSIS

2.2.2 DEMAND-SIDE ANALYSIS

2.3 GROWTH FORECAST

2.3.1 SUPPLY SIDE

2.3.2 DEMAND SIDE

2.4 MARKET SIZE ESTIMATION

2.4.1 BOTTOM-UP APPROACH

2.4.2 TOP-DOWN APPROACH

2.5 DATA TRIANGULATION

2.6 RESEARCH ASSUMPTIONS

2.7 GROWTH FORECAST

2.8 RISK ASSESSMENT

2.9 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PHOTOVOLTAIC (PV) FILMS MARKET

4.2 PHOTOVOLTAIC (PV) FILMS MARKET, BY RAW MATERIAL

4.3 PHOTOVOLTAIC (PV) FILMS MARKET, BY APPLICATION

4.4 PHOTOVOLTAIC (PV) FILMS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing demand for high-performance films to enhance solar panel longevity and protection

5.2.1.2 Adoption of new cell technologies - Tunnel Oxide Passivated Contact (TOPCon) and Heterojunction Technology (HJT)

5.2.1.3 Government-led policies for solar energy

5.2.2 RESTRAINTS

5.2.2.1 Lack of effective recycling processes for used PV encapsulation films

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing deployment of floating solar installations

5.2.3.2 Innovations in encapsulation materials to elevate panel efficiency and performance

5.2.4 CHALLENGES

5.2.4.1 Performance concerns associated with solar films in regions with climate variability

5.3 IMPACT OF GENERATIVE AI ON PHOTOVOLTAICS (PV) FILMS MARKET

5.3.1 INTRODUCTION

6 INDUSTRY TRENDS

6.1 INTRODUCTION

6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.3 SUPPLY CHAIN ANALYSIS

6.4 IMPACT OF 2025 US TARIFF ON PHOTOVOLTAIC (PV) FILMS MARKET

6.4.1 INTRODUCTION

6.4.2 KEY TARIFF RATES

6.4.3 PRICE IMPACT ANALYSIS

6.4.4 IMPACT ON REGIONS

6.4.4.1 North America

6.4.4.2 Europe

6.4.4.3 Asia Pacific

6.4.5 IMPACT ON MATERIALS

6.5 INVESTMENT AND FUNDING SCENARIO

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

6.6.2 AVERAGE SELLING PRICE TREND, BY RAW MATERIAL, 2021-2024

6.6.3 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY RAW MATERIAL, 2024

6.7 ECOSYSTEM ANALYSIS

6.8 TECHNOLOGY ANALYSIS

6.8.1 KEY TECHNOLOGIES

6.8.2 COMPLEMENTARY TECHNOLOGIES

6.8.3 ADJACENT TECHNOLOGIES

6.9 PATENT ANALYSIS

6.9.1 METHODOLOGY

6.9.2 PATENTS GRANTED WORLDWIDE

6.9.3 PATENT PUBLICATION TRENDS

6.9.4 INSIGHTS

6.9.5 LEGAL STATUS OF PATENTS

6.9.6 JURISDICTION ANALYSIS

6.9.7 TOP APPLICANTS

6.10 TRADE ANALYSIS

6.10.1 IMPORT SCENARIO (HS CODE 392010)

6.10.2 EXPORT SCENARIO (HS CODE 392010)

6.11 KEY CONFERENCES AND EVENTS, 2025-2026

6.12 TARIFF AND REGULATORY LANDSCAPE

6.12.1 TARIFF ANALYSIS

6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.12.3 STANDARDS AND REGULATIONS

6.13 PORTER'S FIVE FORCES ANALYSIS

6.13.1 THREAT OF NEW ENTRANTS

6.13.2 THREAT OF SUBSTITUTES

6.13.3 BARGAINING POWER OF SUPPLIERS

6.13.4 BARGAINING POWER OF BUYERS

6.13.5 INTENSITY OF COMPETITIVE RIVALRY

6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.14.2 BUYING CRITERIA

6.15 MACROECONOMIC OUTLOOK

6.15.1 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

6.16 CASE STUDY ANALYSIS

6.16.1 COMPARATIVE DURABILITY ANALYSIS OF POE AND EVA ENCAPSULANTS IN PHOTOVOLTAIC MODULES

6.16.2 CHARACTERIZATION OF EVA FILMS FOR PHOTOVOLTAIC MODULES

7 PHOTOVOLTAIC (PV) FILMS MARKET, BY RAW MATERIAL

7.1 INTRODUCTION

7.2 ETHYLENE VINYL ACETATE (EVA)

7.2.1 RAPID GROWTH OF GLOBAL SOLAR INFRASTRUCTURE AND RISING NEED FOR HIGH-PERFORMANCE FILMS TO DRIVE MARKET

7.3 POLYVINYL BUTYRAL (PVB)

7.3.1 STRONG BINDING PROPERTIES, OPTICAL CLARITY, ADHESION TO VARIOUS SURFACES, TOUGHNESS, AND FLEXIBILITY TO FUEL DEMAND

7.4 POLYOLEFIN ELASTOMER (POE)

7.4.1 LOW WATER VAPOR TRANSMISSION RATE AND THERMAL STABILITY TO FUEL DEMAND

7.5 OTHER RAW MATERIALS

7.5.1 PDMS

7.5.2 IONOMER

7.5.3 SILICON

7.5.4 TPO

8 PHOTOVOLTAIC (PV) FILMS MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 GROUND-MOUNTED PV

8.2.1 EXPANSION OF GROUND-MOUNTED PV PROJECTS TO DRIVE DEMAND

8.3 BUILDING-INTEGRATED PV

8.3.1 INCREASING DEMAND FOR SUSTAINABLE CONSTRUCTION, SUPPORTIVE GOVERNMENT POLICIES, AND ADVANCEMENTS IN PV TECHNOLOGY TO PROPEL MARKET

9 PHOTOVOLTAIC (PV) FILMS MARKET, BY REGION

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 CHINA

9.2.1.1 Presence of leading PV encapsulation film manufacturers to drive market

9.2.2 JAPAN

9.2.2.1 Subsidies and feed-in tariffs to drive market

9.2.3 INDIA

9.2.3.1 High government-led support through schemes, solar parks, and net metering policies to drive market

9.2.4 SOUTH KOREA

9.2.4.1 Significant investment in R&D for high-quality materials to drive market

9.2.5 TAIWAN

9.2.5.1 High export of solar panels and domestic manufacturing of PV films to propel market

9.2.6 REST OF ASIA PACIFIC

9.3 NORTH AMERICA

9.3.1 US

9.3.1.1 Inflation Reduction Act (IRA) supporting domestic solar manufacturing and installations to drive market

9.3.2 CANADA

9.3.2.1 Expansion of solar projects in Ontario and Alberta to drive market

9.3.3 MEXICO

9.3.3.1 Emergence as manufacturing hub to drive demand

9.4 EUROPE

9.4.1 GERMANY

9.4.1.1 Rising construction of sustainable buildings to drive demand

9.4.2 ITALY

9.4.2.1 Increased production capacity and strong international partnerships to drive market

9.4.3 FRANCE

9.4.3.1 Expansion of floating solar systems on reservoirs, rivers, and coastal waters to fuel market growth

9.4.4 UK

9.4.4.1 Growing focus on renewable energy and solar installations to propel market

9.4.5 SPAIN

9.4.5.1 Expansion of solar parks to drive demand

9.4.6 RUSSIA

9.4.6.1 Ongoing investments in renewable energy infrastructure to drive market

9.4.7 REST OF EUROPE

9.5 ROW

9.5.1 SAUDI ARABIA

9.5.1.1 High focus on diversification under Vision 2030 initiative to drive market

9.5.2 UAE

9.5.2.1 Government-led incentives and policies supporting solar energy to drive demand

9.5.3 OMAN

9.5.3.1 Utility-scale solar projects to boost demand

9.5.4 EGYPT

9.5.4.1 Expanding local manufacturing to boost domestic demand

9.5.5 SOUTH AFRICA

9.5.5.1 Rapid expansion of utility-scale solar farms to drive demand

9.5.6 OTHERS IN ROW

10 COMPETITIVE LANDSCAPE

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3 MARKET SHARE ANALYSIS

10.4 REVENUE ANALYSIS

10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.5.1 STARS

10.5.2 EMERGING LEADERS

10.5.3 PERVASIVE PLAYERS

10.5.4 PARTICIPANTS

10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.5.5.1 Company footprint

10.5.5.2 Region footprint

10.5.5.3 Raw material footprint

10.5.5.4 Application footprint

10.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024