초전도 선재 시장 : 유형별, 판매 채널별, 용도별, 최종 사용자별, 지역별 예측(-2030년)

Superconducting Wire Market by Type, Application, End User, Sales Channel, and Region - Global Forecast to 2030

상품코드:1784316

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

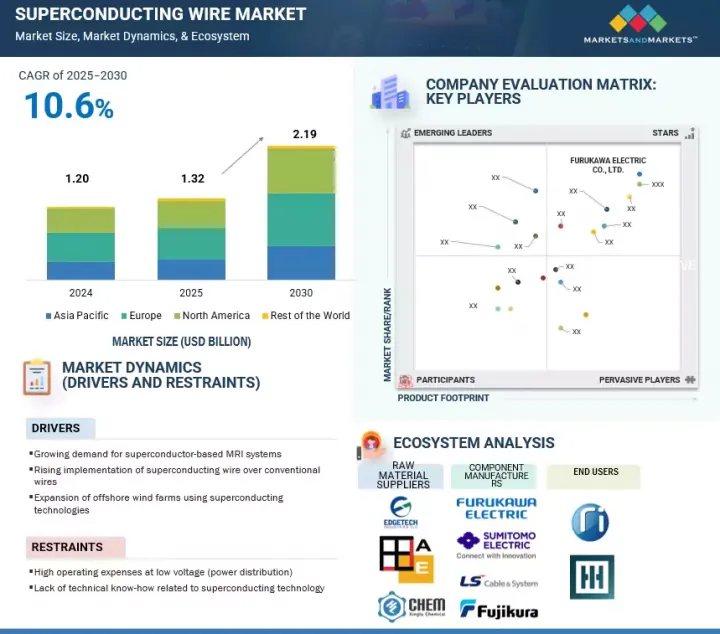

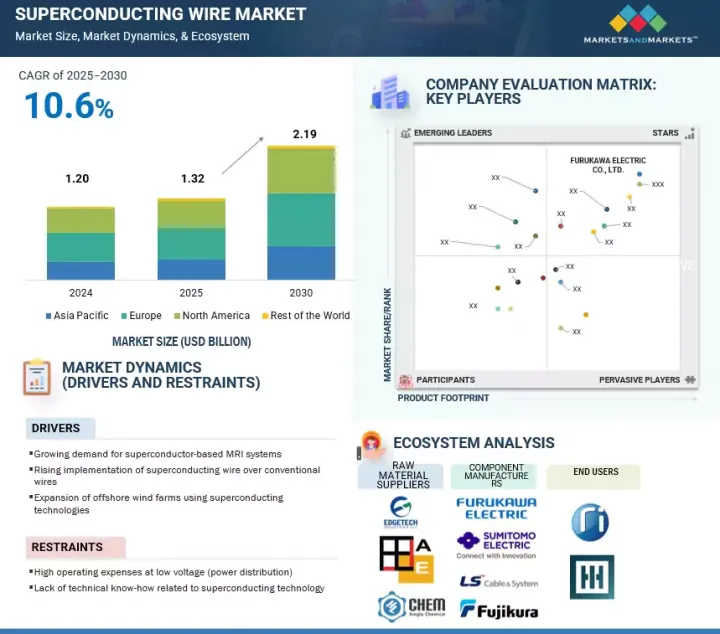

세계의 초전도 선재 시장 규모는 2025년 13억 2,000만 달러에서 2030년에는 21억 9,000만 달러에 이를 것으로 예측되며, CAGR은 10.6%를 나타낼 전망입니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위 가치

금액(100만 달러/10억 달러) 및 km

부문별

초전도 선재 시장 : 유형별, 판매 채널별, 용도별, 최종 사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

초전도 기반 자기 공명 영상(MRI) 시스템에 대한 수요가 증가하고 있으며, 기존 전도체의 우수한 대체재로 초전도 선재의 채택이 증가하고 있는 것이 초전도 선재 시장의 성장을 촉진하는 주요 요인입니다.

초전도 선재 시장은 유형별로 저온, 중온 및 고온 초전도로 나뉩니다. 2025년에는 고온 초전도 선재이 두 번째로 큰 시장 점유율을 차지할 것으로 보입니다. 기존 선재에 대한 초전도 선재의 사용이 증가함에 따라 고온 초전도는 자기 공명 영상(MRI) 및 자기 부상(마그레브)과 같은 용도에 이상적입니다.

초전도 선재 시장은 최종 사용자별로 에너지, 의료, 운송, 연구 및 기타 부문으로 분류됩니다. 의료 부문은 예측 기간 동안 시장을 주도할 것으로 예상됩니다. MRI 및 NMR 시스템에 초전도 권선 자석을 사용하는 전 세계의 강력한 전환은 의료 부문에서 초전도 선재의 수요를 촉진할 것으로 예상됩니다.

북미는 해상 풍력 에너지 부문에 대한 투자 증가, 자기 부상 열차 개발, 북미 국가, 특히 미국에서 의료 시설 개발에 대한 정부의 관심 증가로 인해 두 번째로 큰 시장이 될 것으로 예상됩니다. 초전도 선재 기반 자기 공명 영상(MRI) 스캐너의 채택이 북미의 초전도 선재 시장 성장을 촉진할 것으로 예상됩니다.

초전도 선재 시장을 독점하고 있는 것은 폭넓은 지역에서 사업을 전개하는 소수의 대기업입니다. 주요 진출기업은 스미토모 전기 공업 주식회사(일본), 주식회사 후지쿠라(일본)입니다.(일본), 후루카와 전기공업 주식회사(일본), Bruker(미국), American Superconductor(미국)입니다.

이 보고서는 유형, 수직 시장, 용도, 판매 채널 및 지역별로 전 세계 초전도 선재 시장을 정의, 설명 및 예측합니다. 또한 시장에 대한 상세한 정성적 및 정량적 분석도 제공합니다. 이 보고서는 주요 시장 촉진요인, 제약, 기회 및 과제를 종합적으로 검토합니다. 또한 시장의 다양한 중요한 측면도 다룹니다. 여기에는 경쟁 환경, 시장 역학, 가치 측면의 시장 추정 및 초전도 선재 시장의 미래 동향에 대한 분석이 포함됩니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

고객사업에 영향을 주는 동향 및 혼란

밸류체인 분석

생태계 분석

사례 연구 분석

세계 거시경제 전망

투자 및 자금조달 시나리오

기술 분석

가격 분석

무역 분석

생성형 AI/AI가 초전도선 시장에 미치는 영향

특허 분석

주요 컨퍼런스 및 이벤트(2025년)

관세 및 규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

2025년 미국 관세가 초전도선 시장에 미치는 영향

제6장 초전도선 시장(유형별)

소개

LTS 선재

MTS 선재

HTS 선재

제7장 초전도선 시장(판매 채널별)

소개

직접 판매 채널

간접 판매 채널

제8장 초전도선 시장(용도별)

소개

자기 공명 영상

전력망 인프라

초전도 고장 전류 제한 장치

자기 부상

기타

제9장 초전도선 시장(최종 사용자별)

소개

에너지

의료

운송

연구

기타

제10장 초전도선 시장(지역별)

소개

북미

미국

캐나다

멕시코

아시아태평양

중국

일본

인도

한국

호주

뉴질랜드

기타

유럽

독일

영국

이탈리아

프랑스

스위스

스웨덴

기타

기타 지역

제11장 경쟁 구도

소개

주요 참가 기업의 전략 및 강점(2021-2024년)

시장 점유율 분석(2024년)

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타트업/중소기업(2024년)

기업평가와 재무지표

브랜드/제품 비교

경쟁 시나리오

제12장 기업 프로파일

주요 진출기업

SUMITOMO ELECTRIC INDUSTRIES, LTD.

FUJIKURA LTD.

FURUKAWA ELECTRIC CO., LTD.

BRUKER

AMERICAN SUPERCONDUCTOR

NEXANS

LS CABLE & SYSTEM LTD.

KISWIRE ADVANCED TECHNOLOGY CO., LTD.

METOX TECHNOLOGIES, INC.

SAM DONG

THEVA DUNNSCHICHTTECHNIK GMBH

FIRMETAL GROUP

SUPEROX

ASG SUPERCONDUCTORS SPA

SUPERCON, INC.

기타 기업

LUVATA

JAPAN SUPERCONDUCTOR TECHNOLOGY, INC.(JASTEC)

HYPER TECH RESEARCH, INC.

AMPEERS LLC

WESTERN SUPERCONDUCTING TECHNOLOGIES CO., LTD.

SUNAM CO., LTD

SUPERNODE

CUTTING EDGE SUPERCONDUCTORS, INC.

SOLID MATERIAL SOLUTIONS LLC

CRYOMAGNETICS

제13장 부록

HBR

영문 목차

영문목차

The global superconducting wire market is anticipated to grow from USD 1.32 billion in 2025 to USD 2.19 billion by 2030, at a CAGR of 10.6%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/Billion) and Volume (KM)

Segments

Superconducting wire market, by type, end user, sales channel, application, and region

Regions covered

North America, Europe, Asia Pacific, and Rest of the World

The increasing demand for superconductor-based magnetic resonance imaging (MRI) systems, coupled with the growing adoption of superconducting wires as a superior alternative to conventional conductors, are key factors driving the growth of the superconducting wire market.

"High-temperature superconductor to be second-largest segment of superconducting wire market, by type"

The superconducting wire market is split by type into low-temperature, medium-temperature, and high-temperature superconductors. In 2025, high-temperature superconductor wires are likely to account for the second-largest market share. The rising implementation of superconducting wires over conventional wires makes high-temperature superconductors ideal for applications such as magnetic resonance imaging (MRI) and magnetic levitation (maglev).

"Medical segment to capture prominent share of superconducting wire market based on end user"

The superconducting wire market has been segmented by end user into energy, medical, transportation, research, and others. The medical segment is expected to command the market throughout the forecast period. A strong global shift toward using superconductor-wound magnets in MRI and NMR systems is expected to drive the demand for superconducting wires in the medical segment.

"North America to be second-largest market during forecast period"

North America is expected to be the second-largest market due to the Increasing investments in the offshore wind energy sector, development of maglev trains, and increasing focus of the governments on developing medical facilities in North American countris, specifically the US, is anticipated to boost the adoption of superconducting wire-based magnetic resonance imaging (MRI) scanners are expected to drive the growth of the superconducting wire market in North America.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects.

The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 65%, Tier 2 - 24%, and Tier 3 - 11%

By Designation: C-level Executives - 30%, Directors - 25%, and Others - 45%

By Region: North America - 27%, Europe - 20%, and Asia Pacific - 53%

Note: Others include product engineers, product specialists, and engineering leads.

The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: >USD 1 billion, Tier 2: from USD 500 million to USD 1 billion, and Tier 3: <USD 500 million

A few major players with a wide regional presence dominate the superconducting wire market. The leading players are Sumitomo Electric Industries, Ltd. (Japan), Fujikura Ltd. (Japan), Furukawa Electric Co., Ltd. (Japan), Bruker (US), and American Superconductor (US).

Research Coverage:

The report defines, describes, and forecasts the global superconducting wire market based on type, vertical, application, sales channel, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates, in terms of value, and future trends in the superconducting wire market.

Key Benefits of Buying the Report.

Product Development/Innovation: Key drivers (growing demand for zero-loss power transmission, compact high-field magnet systems, and advanced grid technologies), restraints (high material and cryogenic costs), opportunities (advancements in HTS wire fabrication and fusion energy projects), and challenges (technical complexity in manufacturing and limited commercial-scale deployment outside niche applications) influence the market.

Market Development: In March 2025, Furukawa Electric's SuperPower Inc. division delivered next-generation 2G HTS wire for a grid-scale superconducting cable project in South Korea. The development marked a significant milestone in long-distance, high-capacity energy transmission, aligning with global goals for grid decarbonization and improved efficiency.

Market Diversification: The superconducting wire market has witnessed increasing product diversification, including LTS, MTS, and HTS types, catering to varied end uses from MRI and NMR imaging in healthcare to maglev trains, particle accelerators, and SFCLs in the energy and transportation sectors. Enhanced performance at higher operating temperatures and innovation in flexible, durable HTS tapes have broadened adoption across developed and emerging markets.

Competitive Assessment: An evaluation of the competitive positioning of key players in the superconducting wire market includes leading companies such as Sumitomo Electric Industries, Ltd. (Japan), Fujikura Ltd. (Japan), Furukawa Electric Co., Ltd. (Japan), Bruker Corporation (United States), and American Superconductor Corporation (United States).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 INCLUSIONS AND EXCLUSIONS

1.3.2 MARKETS COVERED AND REGIONAL SCOPE

1.3.3 YEARS CONSIDERED

1.4 UNIT CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Intended participants and key opinion leaders

2.1.2.2 Key industry insights

2.1.2.3 Key data from primary sources

2.1.2.4 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Regional analysis

2.2.1.2 Country-level analysis

2.2.1.3 Demand-side assumptions

2.2.1.4 Demand-side calculations

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Supply-side assumptions

2.2.2.2 Supply-side calculations

2.3 DATA TRIANGULATION

2.4 FORECAST

2.5 RESEARCH ASSUMPTION

2.6 RESEARCH LIMITATIONS

2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SUPERCONDUCTING WIRE MARKET

4.2 SUPERCONDUCTING WIRE MARKET, BY SALES CHANNEL AND TYPE

4.3 SUPERCONDUCTING WIRE MARKET, BY SALES CHANNEL

4.4 SUPERCONDUCTING WIRE MARKET, BY TYPE

4.5 SUPERCONDUCTING WIRE MARKET, BY END USER

4.6 SUPERCONDUCTING WIRE MARKET, BY REGION

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing need for advanced MRI systems globally

5.2.1.2 Cost and performance advantages of superconducting wires over conventional wires

5.2.1.3 Expansion of offshore wind farms using superconducting technologies

5.2.2 RESTRAINTS

5.2.2.1 Cost constraints hampering superconducting adoption in low-voltage and medium-voltage applications

5.2.2.2 Slow rate of commercialization due to lack of skilled workforce

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing R&D activities in medical and transportation fields

5.2.4 CHALLENGES

5.2.4.1 High manufacturing costs of superconductors

5.2.4.2 Limited testing infrastructure

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.6 CASE STUDY ANALYSIS

5.6.1 BRUKER SUPPLIES CHROMIUM-PLATED NIOBIUM-TIN SUPERCONDUCTING WIRES FOR ITER PROJECT

5.6.2 SUPERPOWER INC. PROVIDES 2G HTS WIRES TO ENDESA TO PROTECT GRID AGAINST SHORT CIRCUITS

5.6.3 ENHANCING MGB2 SUPERCONDUCTING WIRE PERFORMANCE THROUGH INITIAL FILLING DENSITY OPTIMIZATION AND THERMOMECHANICAL TREATMENT

5.7 GLOBAL MACROECONOMIC OUTLOOK

5.7.1 INTRODUCTION

5.7.2 GDP TRENDS AND FORECAST

5.7.3 IMPACT OF INFLATION ON SUPERCONDUCTING WIRE MARKET

5.8 INVESTMENT AND FUNDING SCENARIO

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Powder-in-tube (PIT)

5.9.2 ADJACENT TECHNOLOGIES

5.9.2.1 Cryogenic cooling technologies

5.10 PRICING ANALYSIS

5.10.1 PRICING RANGE OF SUPERCONDUCTING WIRES, BY TYPE, 2024

5.10.2 AVERAGE SELLING PRICE TREND OF SUPERCONDUCTING WIRES, BY REGION, 2021-2024

5.11 TRADE ANALYSIS

5.11.1 IMPORT SCENARIO (HS CODE 854419)

5.11.2 EXPORT SCENARIO (HS CODE 854419)

5.12 IMPACT OF GENERATIVE AI/AI ON SUPERCONDUCTING WIRE MARKET

5.12.1 USE CASES OF GENERATIVE AI/AI IN SUPERCONDUCTING WIRE MARKET

5.12.2 IMPACT OF GENERATIVE AI/AI ON KEY END USERS, BY REGION

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025

5.15 TARIFF AND REGULATORY LANDSCAPE

5.15.1 TARIFF ANALYSIS

5.15.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.16 PORTER'S FIVE FORCES ANALYSIS

5.16.1 THREAT OF SUBSTITUTES

5.16.2 BARGAINING POWER OF SUPPLIERS

5.16.3 BARGAINING POWER OF BUYERS

5.16.4 THREAT OF NEW ENTRANTS

5.16.5 INTENSITY OF COMPETITIVE RIVALRY

5.17 KEY STAKEHOLDERS AND BUYING CRITERIA

5.17.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.17.2 BUYING CRITERIA

5.18 IMPACT OF 2025 US TARIFF ON SUPERCONDUCTING WIRE MARKET

5.18.1 INTRODUCTION

5.18.2 KEY TARIFF RATES

5.18.3 IMPACT ON COUNTRIES/REGIONS

5.18.3.1 North America

5.18.3.2 Europe

5.18.3.3 Asia Pacific

5.18.3.4 RoW

5.18.4 IMPACT ON END USERS

6 SUPERCONDUCTING WIRE MARKET, BY TYPE

6.1 INTRODUCTION

6.2 LTS WIRES

6.2.1 ENHANCED CRITICAL CURRENT DENSITY AND DURABILITY TO DRIVE ADOPTION IN SCIENTIFIC INFRASTRUCTURE

6.3 MTS WIRES

6.3.1 RISING USE IN MEDICAL IMAGING TO FOSTER MARKET GROWTH

6.4 HTS WIRES

6.4.1 ABILITY TO OPERATE AT HIGHER MAGNETIC FIELDS AND CURRENT DENSITIES TO STIMULATE ADOPTION IN ENERGY SECTOR

6.4.2 FIRST-GENERATION

6.4.2.1 Cost-sensitive and cryogen-free applications to accelerate demand

6.4.3 SECOND-GENERATION

6.4.3.1 Enhanced performance and scalability to increase implementation in future power systems

7 SUPERCONDUCTING WIRE MARKET, BY SALES CHANNEL

7.1 INTRODUCTION

7.2 DIRECT SALES CHANNEL

7.2.1 NEED FOR CUSTOMIZED WIRES TO MEET SPECIFIC APPLICATION REQUIREMENTS TO FUEL SEGMENTAL GROWTH

7.3 INDIRECT SALES CHANNEL

7.3.1 WIDE GEOGRAPHIC REACH OF LARGE CONGLOMERATES TO PROPEL SEGMENTAL GROWTH

8 SUPERCONDUCTING WIRE MARKET, BY APPLICATION

8.1 INTRODUCTION

8.2 MAGNETIC RESONANCE IMAGING

8.2.1 PERFORMANCE AND COST ADVANTAGES OF SUPERCONDUCTING WIRES TO DRIVE ADOPTION

8.3 POWER GRID INFRASTRUCTURE

8.3.1 GREATER EFFICIENCY AND MINIMUM ENERGY LOSSES UNDER HIGH CURRENT LOADS TO SPIKE DEMAND

8.4 SUPERCONDUCTING FAULT CURRENT LIMITER

8.4.1 NEED FOR SAFETY, EFFICIENCY, AND RESILIENCE ACROSS DIVERSE AND EVOLVING POWER APPLICATIONS TO SUPPORT MARKET GROWTH

8.5 MAGLEV

8.5.1 SURGING DEMAND FOR SUSTAINABLE AND HIGH-SPEED TRANSPORTATION SOLUTIONS TO CONTRIBUTE TO MARKET GROWTH

8.6 OTHER APPLICATIONS

9 SUPERCONDUCTING WIRE MARKET, BY END USER

9.1 INTRODUCTION

9.2 ENERGY

9.2.1 ELEVATING DEMAND FOR SUSTAINABLE ENERGY SOLUTIONS TO DRIVE MARKET

9.3 HEALTHCARE

9.3.1 REQUIREMENT FOR MRI MACHINES WITH SUSTAINED MAGNETIC FIELD STRENGTH TO CREATE GROWTH OPPORTUNITIES

9.4 TRANSPORTATION

9.4.1 INCREASING FOCUS ON ENHANCING RAIL LINE CAPACITY AND OPERATIONAL EFFICIENCY TO STIMULATE DEMAND

9.5 RESEARCH

9.5.1 ONGOING RESEARCH FUELING SUPERCONDUCTING WIRE INNOVATION ACROSS KEY SECTORS TO BOOST DEMAND

9.6 OTHER END USERS

10 SUPERCONDUCTING WIRE MARKET, BY REGION

10.1 INTRODUCTION

10.2 NORTH AMERICA

10.2.1 US

10.2.1.1 Substantial investments in quantum computing, fusion energy, and power grid modernization to drive market

10.2.2 CANADA

10.2.2.1 Exploration of superconducting technologies for grid reliability and clean energy applications to propel market

10.2.3 MEXICO

10.2.3.1 Elevating use of MRI and diagnostic imaging systems across public and private healthcare facilities to fuel market growth

10.3 ASIA PACIFIC

10.3.1 CHINA

10.3.1.1 Government investment in high-speed rail and next-generation computing to contribute to market growth

10.3.2 JAPAN

10.3.2.1 Strategic role of country in fusion, transportation, and medical applications to boost demand

10.3.3 INDIA

10.3.3.1 Rising MRI installations in Tier 2 and Tier 3 cities to accelerate demand

10.3.4 SOUTH KOREA

10.3.4.1 Installation of power grid pilot projects to fuel market growth

10.3.5 AUSTRALIA

10.3.5.1 Active participation and investment in superconductivity-related R&D to support market development

10.3.6 NEW ZEALAND

10.3.6.1 Involvement of research institutes in cryogenics and magnetic field studies to facilitate market growth

10.3.7 REST OF ASIA PACIFIC

10.4 EUROPE

10.4.1 GERMANY

10.4.1.1 Energy transition policies, medical innovation, and advanced scientific research to promote adoption

10.4.2 UK

10.4.2.1 NHS-backed investment in AI-powered diagnostics and infrastructure modernization to support upward market trajectory

10.4.3 ITALY

10.4.3.1 National energy transition goals to trigger opportunities for market players

10.4.4 FRANCE

10.4.4.1 Surging demand for advanced power transmission technologies to boost market uptake

10.4.5 SWITZERLAND

10.4.5.1 Excellence in applied superconductivity research to strengthen market momentum

10.4.6 SWEDEN

10.4.6.1 Electrification of transportation sector to drive market

10.4.7 REST OF EUROPE

10.5 REST OF THE WORLD (ROW)

11 COMPETITIVE LANDSCAPE

11.1 INTRODUCTION

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2024

11.3 MARKET SHARE ANALYSIS, 2024

11.4 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.4.1 STARS

11.4.2 EMERGING LEADERS

11.4.3 PERVASIVE PLAYERS

11.4.4 PARTICIPANTS

11.4.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.4.5.1 Company footprint

11.4.5.2 Region footprint

11.4.5.3 Type footprint

11.4.5.4 End user footprint

11.4.5.5 Sales channel footprint

11.5 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024