SCADA Market by Component (Programmable Logic Controllers, Remote Terminal Units, Human-machine Interfaces, Communication Systems, Input/Output Devices, Sensors, Actuators, Terminal Blocks, Connectors) - Global Forecast to 2030

상품코드:1783247

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 296 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

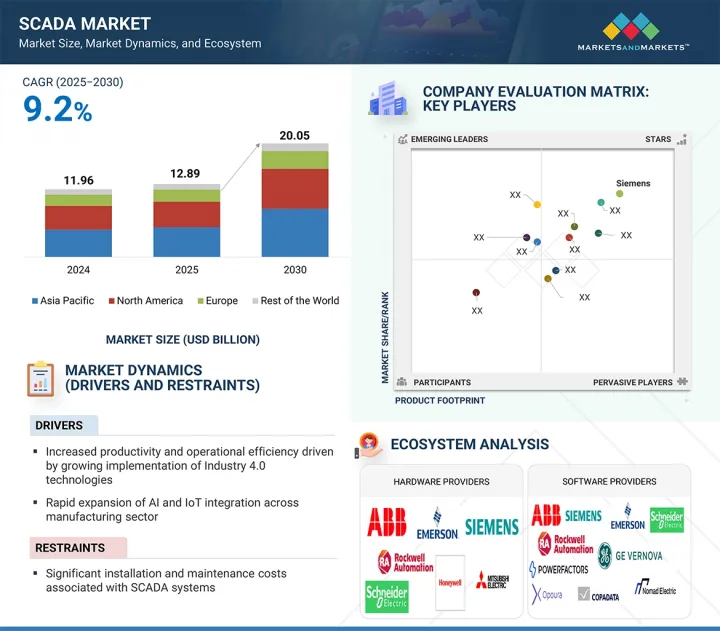

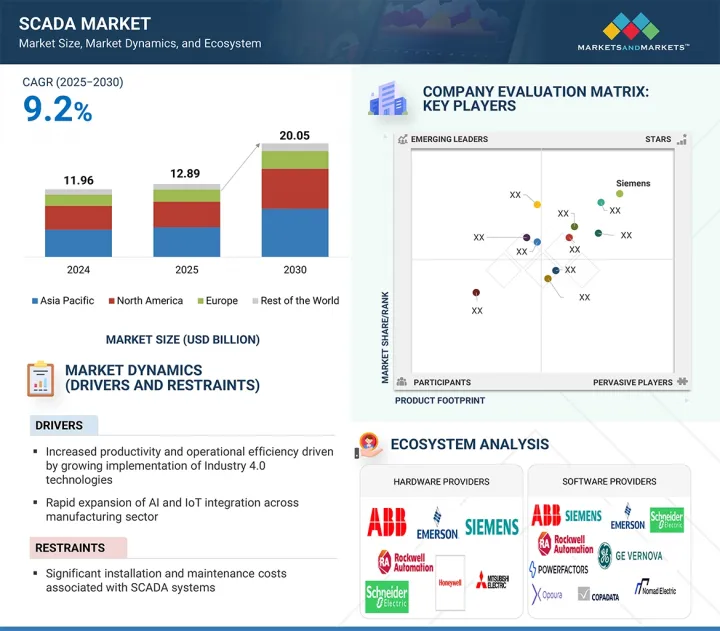

세계의 SCADA 시장 규모는 9.2%의 CAGR로 확대하며, 2025년 128억 9,000만 달러에서 2030년에는 200억 5,000만 달러로 성장할 것으로 예측됩니다.

성장의 원동력은 유틸리티, 개별 제조업, 공정 산업에서의 자동화 발전과 인프라 디지털화에 대한 투자 증가입니다. 산업계가 실시간 가시성, 업무 효율성, 시스템 복원력 향상을 요구하고 있는 가운데, SCADA 솔루션은 중앙 집중식 모니터링과 지능형 제어를 가능하게 하는 데 중요한 역할을 하고 있습니다. 전력, 상하수도, 교통, 통신 등 유틸리티 부문은 레거시 네트워크를 현대화하고 서비스 연속성을 보장하기 위해 SCADA 시스템을 도입하고 있습니다.

조사 범위

조사 대상연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

금액(10억 달러)

부문별

오퍼링별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

전자기기 및 반도체와 같은 개별 산업은 정확한 제조를 위해 SCADA를 사용하고 있으며, 식품 및 음료와 같은 공정 분야는 품질 보증 및 규제 준수를 위해 SCADA에 의존하고 있습니다. SCADA와 산업용 IoT, AI 기반 분석, 클라우드 플랫폼의 통합은 SCADA의 기능을 더욱 혁신적으로 변화시켜 예지보전, 데이터베이스 의사결정, 확장 가능한 배포 모델을 지원합니다. 전 세계 산업계가 보다 스마트한 운영과 디지털 인프라를 추구함에 따라 첨단 SCADA 시스템에 대한 수요는 주요 용도에서 빠르게 확대될 것으로 예측됩니다.

서비스 분야는 산업 및 유틸리티 분야의 시스템 통합, 원격 지원, 수명주기 유지보수 수요 증가로 인해 SCADA 시장에서 높은 CAGR로 성장할 것으로 예측됩니다. SCADA 시스템이 더욱 복잡해지고 실시간 의사결정에 필수적인 요소로 자리 잡으면서, 조직은 시스템의 신뢰성, 사이버 보안, 성능 최적화를 보장하는 서비스 제공에 중점을 두고 있습니다. 클라우드 기반 SCADA, 원격 모니터링, 예지보전으로 전환하면서 전문적인 관리형 서비스의 필요성이 더욱 커지고 있습니다. 또한 각 산업계가 디지털 전환 전략을 추진하면서 기술 컨설팅, 시스템 업그레이드, 교육 서비스에 대한 수요도 지속적으로 증가하고 있습니다. 이러한 서비스는 다운타임을 줄일 뿐만 아니라 SCADA 인프라 투자 가치를 극대화하는 데 도움이 됩니다. 효율성, 안전성, 규제 준수에 대한 관심이 높아지면서 서비스 부문은 다양한 부문에서 SCADA 도입의 장기적인 성장과 확장을 지원하는 데 중요한 역할을 할 것으로 보입니다.

이산 제조 부문은 스마트 팩토리 프레임워크와 산업 자동화 기술의 급속한 채택으로 인해 예측 기간 중 SCADA 시장에서 가장 높은 CAGR을 경험할 것으로 예측됩니다. 자동차, 반도체, 전자제품과 같은 산업은 운영을 최적화하고, 실시간 데이터베이스 의사결정을 가능하게 하며, 경쟁이 치열한 시장에서 제품 품질을 유지하기 위해 SCADA 솔루션에 대한 투자를 늘리고 있습니다. 그 중에서도 반도체 및 전자 산업은 정밀한 제어, 첨단 모니터링 기능, 생산 유연성의 필요성으로 인해 가장 빠르게 성장할 것으로 예측됩니다. SCADA 시스템 통합은 제조업체가 공정의 투명성을 높이고, 다운타임을 줄이며, 예지보전 전략을 지원하는 데 도움이 됩니다. 이산형 제조 산업이 운영 효율화와 디지털 혁신에 집중하고 있는 가운데, SCADA는 확장 가능하고 민첩하며 비용 효율적인 생산 환경에 필수적인 요소로 자리 잡고 있습니다.

아시아태평양은 급속한 산업 성장, 인프라 투자 증가, 주요 부문의 빠른 자동화 도입에 힘입어 예측 기간 중 SCADA 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 중국, 인도, 일본, 한국 등의 국가들은 스마트 제조 능력을 향상시키고 유틸리티 네트워크를 현대화하여 SCADA 시스템에 대한 수요를 증가시키고 있습니다. 디지털 전환, 스마트 그리드 개발, 지능형 교통에 초점을 맞춘 정부의 구상은 시장 성장을 더욱 촉진하고 있습니다. 또한 전자 및 자동차 제조 분야에서 이 지역의 강력한 입지는 생산성 향상, 운영 연속성 보장, 자산 성능 강화를 위한 SCADA 솔루션의 채택을 촉진하고 있습니다. 산업 전반에 걸쳐 확장 가능한 실시간 제어 시스템에 대한 요구가 증가함에 따라 아시아태평양은 전 세계 SCADA 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다.

세계의 SCADA 시장에 대해 조사했으며, 오퍼링별, 최종사용자별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

서론

시장 역학

밸류체인 분석

에코시스템 분석

투자와 자금조달 시나리오

가격 분석

고객 비즈니스에 영향을 미치는 동향/혼란

기술 분석

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

무역 분석

특허 분석

2025-2026년의 주요 컨퍼런스와 이벤트

규제 상황

SCADA 시장에서 AI의 영향

미국 관세가 SCADA 시장에 미치는 영향

제6장 최신 SCADA 시스템의 중요한 기능

서론

고성능 및 신속한 데이터 수집 능력

라이브 및 셀프 서비스 대시보드

고장 탐지에서의 예측 분석

유니버설 접속성과 IoT 대응 오퍼레이션

2D 및 3D 시각화

최신 경보

업계 고유 커스터마이즈와 베스트 프랙티스

미션 크리티컬 장황성

확장성(EXPANDABILITY AND SCALABILITY)

통합된 SMS/이메일 경계체제

사이버 보안과 제로 트러스트 아키텍처

제7장 사이버 보안 관련 위협의 유형과 대책

서론

SCADA 시스템의 유형

SCADA 시스템에 관련된 사이버 보안 리스크와 대책

제8장 SCADA 시장에서의 주요 사용 사례/용도

서론

실시간 모니터링

리모트 액세스와 제어

그리드 통합

데이터 분석과 최적화

고장 탐지와 예지보전

제9장 SCADA 시장(오퍼링별)

서론

하드웨어

소프트웨어

서비스

제10장 SCADA 시장(최종사용자별)

서론

프로세스 산업

디스크리트 제조

유틸리티

제11장 SCADA 시장(지역별)

서론

북미

미국

캐나다

멕시코

유럽

영국

독일

프랑스

이탈리아

스페인

기타

아시아태평양

중국

일본

한국

인도

호주

기타

기타 지역

중동

아프리카

남미

제12장 경쟁 구도

개요

주요 기업이 채택하는 주요 전략(2021-2024년)

시장 점유율 분석, 2024년

주요 기업의 매출 분석(2020-2024년)

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오

제13장 기업 개요

주요 참여 기업

SCHNEIDER ELECTRIC

SIEMENS

ABB

ROCKWELL AUTOMATION

EMERSON ELECTRIC CO.

GE VERNOVA

HONEYWELL INTERNATIONAL INC.

MITSUBISHI ELECTRIC CORPORATION

OMRON CORPORATION

YOKOGAWA ELECTRIC CORPORATION

HITACHI ENERGY LTD

기타 기업

CAPULA LTD

ING. PUNZENBERGER COPA-DATA GMBH

DATA FLOW SYSTEMS

OPOURA

POWER FACTORS

ELYNX TECHNOLOGIES, LLC.

EMR INTEGRATED SOLUTIONS

INDUCTIVE AUTOMATION, LLC.

JFE ENGINEERING CORPORATION

OVAK TECHNOLOGIES

PILZ GMBH & CO. KG

SPRECHER AUTOMATION GMBH

SURVALENT TECHNOLOGY CORPORATION

WILLOWGLEN SYSTEMS

TRIHEDRAL ENGINEERING LIMITED

제14장 부록

KSA

영문 목차

영문목차

With a CAGR of 9.2%, the global SCADA market is expected to grow from USD 12.89 billion in 2025 to USD 20.05 billion by 2030. Growth will be driven by increasing automation across utilities, discrete manufacturing, and process industries, along with rising investments in infrastructure digitalization. As industries seek to improve real-time visibility, operational efficiency, and system resilience, SCADA solutions are playing a key role in enabling centralized monitoring and intelligent control. Utility sectors such as power, water and wastewater treatment, transportation, and telecommunications are implementing SCADA systems to modernize legacy networks and ensure service continuity.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Offering, End User, and Region

Regions covered

North America, Europe, APAC, RoW

Discrete industries like electronics and semiconductors are using SCADA for precise manufacturing, while process sectors such as food & beverage depend on it for quality assurance and regulatory compliance. The integration of SCADA with industrial IoT, AI-based analytics, and cloud platforms is further transforming its capabilities, supporting predictive maintenance, data-driven decisions, and scalable deployment models. As global industries pursue smarter operations and digital infrastructure, the demand for advanced SCADA systems is expected to grow rapidly across key application sectors.

" Rising demand for operational support to drive growth of services segment in the SCADA market."

The services segment is expected to grow at a significant CAGR in the SCADA market, driven by increasing demand for system integration, remote support, and lifecycle maintenance across industrial and utility operations. As SCADA systems become more complex and essential for real-time decision-making, organizations are emphasizing service offerings that ensure system reliability, cybersecurity, and performance optimization. The shift toward cloud-based SCADA, remote monitoring, and predictive maintenance is further increasing the need for professional and managed services. Additionally, as industries pursue digital transformation strategies, the demand for technical consulting, system upgrades, and training services continues to grow. These services not only help reduce downtime but also maximize the value of SCADA infrastructure investments. With the rising focus on efficiency, safety, and regulatory compliance, the services segment is set to play a key role in supporting the long-term growth and expansion of SCADA deployments across various sectors.

" Discrete manufacturing to emerge as the fastest growing end-use segment in the SCADA market "

The discrete manufacturing segment is expected to experience the highest CAGR in the SCADA market during the forecast period, driven by the rapid adoption of smart factory frameworks and industrial automation technologies. Industries such as automotive, semiconductor, and electronics are increasingly investing in SCADA solutions to optimize operations, enable real-time data-driven decisions, and maintain product quality in highly competitive markets. Among these, the semiconductor and electronics industry is projected to grow the fastest, due to the need for precise control, advanced monitoring capabilities, and greater production flexibility. The integration of SCADA systems helps manufacturers improve process transparency, reduce downtime, and support predictive maintenance strategies. As discrete manufacturers focus on operational efficiency and digital transformation, SCADA is becoming a vital component for scalable, agile, and cost-effective production environments.

" Industrial automation and smart infrastructure initiatives to accelerate SCADA market growth in Asia Pacific "

Asia Pacific is expected to have the highest CAGR in the SCADA market during the forecast period, driven by rapid industrial growth, increasing infrastructure investments, and the faster adoption of automation across key sectors. Countries like China, India, Japan, and South Korea are improving their smart manufacturing capabilities and modernizing utility networks, which increases demand for SCADA systems. Government efforts focused on digital transformation, smart grid development, and intelligent transportation further support market growth. Additionally, the region's strong presence in electronics and automotive manufacturing is boosting the adoption of SCADA solutions to improve productivity, ensure operational continuity, and enhance asset performance. As the need for scalable, real-time control systems grows across industries, Asia Pacific is expected to become the fastest-growing region in the global SCADA market.

Breakdown of primaries

A variety of executives from key organizations operating in the SCADA market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

By Company Type: Tier 1 -45%, Tier 2 - 35%, and Tier 3 - 20%

By Designation: Directors - 45%, C-level - 30%, and Others - 25%

By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

Note: Other designations include sales and product managers and project engineers. The three tiers of the companies are defined based on their total revenue in 2024: Tier 1 - revenue greater than or equal to USD 1 billion; Tier 2 - revenue between USD 100 million and USD 1 billion; and Tier 3 revenue less than or equal to USD 100 million.

Major players featured in this report include: Rockwell Automation (US), ABB (Switzerland), Schneider Electric (France), Emerson Electric Co. (US), Siemens (Germany), GE Vernova (US), Honeywell International Inc. (US), Mitsubishi Electric Corporation (Japan), OMRON Corporation (Japan), Yokogawa Electric Corporation (Japan), Capula Ltd (UK), Ing. Punzenberger COPA-DATA GmbH (Austria), Data Flow Systems (US), Power Factors (US), eLynx Technologies, LLC. (US), EMR Integrated Solutions (Ireland), Inductive Automation, LLC. (US), JFE Engineering Corporation (Japan), Ovak Technologies (Armenia), Pilz GmbH & Co. KG (Germany), Sprecher Automation GmbH (Austria), Survalent Technology Corporation (Canada), Willowglen Systems (Canada), and Trihedral Engineering Limited (Canada). These leading companies have a broad product portfolio and maintain a strong presence in both established and emerging markets.

The study provides a detailed competitive analysis of these key players in the SCADA market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

In this report, the SCADA market is segmented by offering, end user, and region. The offer segment includes hardware, software, and services. The end user segment covers process industries, discrete manufacturing, and utilities. The market is divided into four regions - North America, Asia Pacific, Europe, and Rest of the World (RoW).

Reasons to Buy the Report

The report will assist leaders and new entrants in this market by providing estimated revenue figures for the overall market and its sub-segments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and develop appropriate go-to-market strategies. Additionally, the report offers insights into the SCADA market's current state and highlights key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

Analysis of key drivers (increased productivity and operational efficiency driven by growing implementation of Industry 4.0 technologies, rapid expansion of AI and IoT integration across the manufacturing sector, increasing adoption of industrial mobility solutions fueled by rising market demand, increasing rollout of smart city developments, growing governmental backing for the adoption of SCADA systems and unprecedented scale of renewable energy deployment, distributed and remote nature of renewable energy sources), restraints (significant installation and maintenance costs associated with SCADA systems and high complexity and extensive customization requirements of SCADA systems), opportunities (swift progress in wireless sensor network development, shift from on-premise SCADA infrastructure to cloud-based solutions, leveraging SCADA-big data integration for enhanced operational intelligence and growing implementation of SCADA systems across transportation, smart buildings, and agricultural sectors, floating solar SCADA solutions), and challenges (vulnerability of SCADA systems to cybersecurity threats and incompatibility between communication protocols in SCADA systems) influencing the growth of the SCADA market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the SCADA market

Market Development: Comprehensive information about lucrative markets - the report analyzes the SCADA market across varied regions

Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the SCADA market

Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players such as Rockwell Automation (US), Schneider Electric (France), ABB (Switzerland), Siemens (Germany), Emerson Electric Co. (US) , and others.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNITS CONSIDERED

1.6 STAKEHOLDERS

1.7 LIMITATIONS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 INTRODUCTION

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 Major secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 Key primary interviews with experts

2.1.3.2 Key data from primary sources

2.1.3.3 Key industry insights

2.1.3.4 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Market size estimation using bottom-up approach (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Market size estimation using top-down approach (supply side)

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS AND LIMITATIONS

2.4.1 RESEARCH ASSUMPTIONS

2.4.2 RESEARCH LIMITATIONS

2.5 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ASIA PACIFIC TO CREATE LUCRATIVE OPPORTUNITIES FOR PLAYERS IN SCADA MARKET

4.2 SCADA MARKET, BY OFFERING

4.3 SCADA MARKET, BY END USER

4.4 SCADA MARKET, BY REGION/COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increased productivity and operational efficiency due to growing implementation of Industry 4.0

5.2.1.2 Rapid expansion of AI and IoT integration across manufacturing sector

5.2.1.3 Increasing adoption of industrial mobility solutions

5.2.1.4 Increasing rollout of smart city developments

5.2.1.5 Growing governmental backing for adoption of SCADA systems

5.2.1.6 Unprecedented scale of renewable energy deployment

5.2.1.7 Distributed and remote nature of renewable energy sources

5.2.2 RESTRAINTS

5.2.2.1 Significant installation and maintenance costs associated with SCADA systems

5.2.2.2 High complexity and extensive customization requirements of SCADA systems

5.2.3 OPPORTUNITIES

5.2.3.1 Rapid progress in wireless sensor network development

5.2.3.2 Shift from on-premise SCADA infrastructure to cloud-based solutions

5.2.3.3 Leveraging SCADA-big data integration for enhanced operational intelligence

5.2.3.4 Increasing implementation of SCADA systems across transportation, smart buildings, and agricultural sectors

5.2.3.5 Floating solar SCADA solutions

5.2.4 CHALLENGES

5.2.4.1 Vulnerability of SCADA systems to cybersecurity threats

5.2.4.2 Incompatibility between communication protocols in SCADA systems

5.3 VALUE CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 INVESTMENT AND FUNDING SCENARIO

5.6 PRICING ANALYSIS

5.6.1 INDICATIVE PRICING OF PLCS OFFERED BY KEY PLAYERS

5.6.2 AVERAGE SELLING PRICE FOR RTUS

5.6.3 PRICING OF SCADA SOFTWARE OFFERED BY KEY PLAYERS, 2025

5.6.4 AVERAGE SELLING PRICE OF RTUS, BY REGION

5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 IoT

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Cloud computing

5.8.2.2 Edge computing

5.8.2.3 AI

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 5G

5.8.3.2 Cybersecurity

5.9 PORTER'S FIVE FORCES ANALYSIS

5.9.1 BARGAINING POWER OF SUPPLIERS

5.9.2 BARGAINING POWER OF BUYERS

5.9.3 THREAT OF NEW ENTRANTS

5.9.4 THREAT OF SUBSTITUTES

5.9.5 INTENSITY OF COMPETITIVE RIVALRY

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDY ANALYSIS

5.11.1 EMERSON ELECTRIC CO.'S SCADA DEPLOYED AT SHOPPING MALL IN ITALY

5.11.2 MADTREE BREWING COMPANY'S IMPLEMENTS IGNITION BY INDUCTIVE AUTOMATION, LLC. FOR SCADA AND HMI

5.11.3 OVARRO HELPS ENVIRONMENTAL MONITORING SOLUTIONS (EMS) IN IMPROVING DATA PRESENTATION TO CLIENTS

5.11.4 INDIAN OIL'S GUJARAT REFINERY AUTOMATES PLANT WITH HONEYWELL'S SCADA SOLUTION

5.11.5 MICRON TECHNOLOGY ENHANCES SEMICONDUCTOR PRODUCTION WITH GENERAL CONTROL SYSTEM'S SCADA SYSTEM

5.11.6 SCADA & WATER LEAK SOFTWARE FOR MCWD WATER NETWORK STABILITY AND EFFICIENCY

5.11.7 DEPCOM POWER ENHANCES SOLAR OPERATIONS WITH IGNITION

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 903289)

5.12.2 EXPORT SCENARIO (HS CODE 903289)

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 REGULATORY LANDSCAPE

5.15.1 NORTH AMERICA

5.15.1.1 US

5.15.1.2 Canada

5.15.2 EUROPE

5.15.2.1 European Union

5.15.2.2 Germany

5.15.2.3 Russia

5.15.3 ASIA PACIFIC

5.15.3.1 China

5.15.3.2 Japan

5.15.3.3 Australia

5.15.4 REST OF THE WORLD

5.15.4.1 Brazil

5.15.4.2 Kenya

5.15.5 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS RELATED TO SCADA MARKET

5.15.6 MAJOR STANDARDS RELATED TO SCADA MARKET

5.16 IMPACT OF AI ON SCADA MARKET

5.16.1 INTRODUCTION

5.16.2 IMPACT OF AI ON KEY END-USE INDUSTRIES

5.16.2.1 Utilities

5.16.2.2 Water & wastewater

5.16.3 USE CASES

5.16.4 FUTURE OF AI/GEN AI IN SCADA ECOSYSTEM

5.17 IMPACT OF US TARIFFS ON SCADA MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 IMPACT ON DIFFERENT COUNTRIES/REGIONS

6 IMPORTANT FEATURES OF LATEST SCADA SYSTEMS

6.1 INTRODUCTION

6.2 HIGH PERFORMANCE AND RAPID DATA COLLECTION CAPACITY

6.3 LIVE AND SELF-SERVICE DASHBOARDS

6.4 PREDICTIVE ANALYTICS IN FAULT DETECTION

6.5 UNIVERSAL CONNECTIVITY AND IOT-READY OPERATIONS

6.6 2D AND 3D VISUALIZATION

6.7 UP-TO-DATE ALARMING

6.8 INDUSTRY-SPECIFIC CUSTOMIZATION AND BEST PRACTICES

6.9 MISSION-CRITICAL REDUNDANCY

6.10 EXPANDABILITY AND SCALABILITY

6.11 INTEGRATED SMS/E-MAIL ALERTS

6.12 CYBERSECURITY AND ZERO TRUST ARCHITECTURE

7 TYPES AND CYBERSECURITY-RELATED THREATS AND COUNTERMEASURES

7.1 INTRODUCTION

7.2 TYPES OF SCADA SYSTEMS

7.2.1 FIRST GENERATION

7.2.2 SECOND GENERATION

7.2.3 THIRD GENERATION

7.2.4 FOURTH GENERATION

7.3 CYBERSECURITY RISKS ASSOCIATED WITH SCADA SYSTEMS AND COUNTERMEASURES

7.3.1 CYBER THREATS

7.3.1.1 Hacking

7.3.1.2 Malware

7.3.1.3 Inside errors

7.3.2 ROOT CAUSES OF CYBERATTACKS

7.3.2.1 Software development loopholes

7.3.2.2 Monitoring issues

7.3.2.3 Poor training and maintenance

7.3.3 PROTECTION SOLUTIONS

7.3.3.1 Software management

7.3.3.2 Network management

7.3.3.3 User access management

8 TOP USE CASES/APPLICATIONS IN SCADA MARKET

8.1 INTRODUCTION

8.2 REAL-TIME MONITORING

8.3 REMOTE ACCESSIBILITY AND CONTROL

8.4 GRID INTEGRATION

8.5 DATA ANALYSIS AND OPTIMIZATION

8.6 FAULT DETECTION AND PREDICTIVE MAINTENANCE

9 SCADA MARKET, BY OFFERING

9.1 INTRODUCTION

9.2 HARDWARE

9.2.1 DIRECT COMMUNICATION WITH INDUSTRIAL DEVICES TO ENABLE EFFICIENT CONTROL AND DRIVE MARKET GROWTH

9.2.2 COMPONENT

9.2.2.1 Programmable logic controller

9.2.2.1.1 Safe and efficient plant operations to accelerate segment expansion

9.2.2.2 Remote terminal unit

9.2.2.2.1 Rising demand for real-time data acquisition and remote monitoring to drive segment growth

9.2.2.3 Human-machine interface

9.2.2.3.1 Growing need for clear graphical representation of critical data to support timely decision-making

9.2.2.3.2 Communication systems

9.2.2.3.3 Wired communication systems

9.2.2.3.4 Wireless communication systems

9.2.2.4 Other components

9.3 SOFTWARE

9.3.1 NEED FOR DATA ACQUISITION, VISUALIZATION, AND ANALYSIS TO SUPPORT EFFICIENT MONITORING AND CONTROL OF SCADA SYSTEMS

9.3.2 SOFTWARE DEPLOYMENT MODES

9.3.2.1 On-premises deployment

9.3.2.2 Cloud deployment

9.4 SERVICES

9.4.1 RISING DEMAND FOR INSTALLATION, MAINTENANCE, CONFIGURATION, AND TRAINING SERVICES TO PROPEL MARKET GROWTH

9.4.2 PROFESSIONAL SERVICES

9.4.3 MANAGED SERVICES

10 SCADA MARKET, BY END USER

10.1 INTRODUCTION

10.2 PROCESS INDUSTRIES

10.2.1 CHEMICALS

10.2.1.1 Enhanced reliability and advanced safety features in oil & gas facilities to drive market expansion

10.2.2 PHARMACEUTICALS

10.2.2.1 Strict compliance standards and safety to unlock growth potential for SCADA solution providers

10.2.3 FOOD & BEVERAGE

10.2.3.1 Quality enhancement and reduced downtime to drive segment growth

10.2.4 OIL & GAS

10.2.4.1 Rising need for SCADA solutions to manage intricate processes to fuel market growth

10.2.5 OTHER PROCESS INDUSTRIES

10.3 DISCRETE MANUFACTURING

10.3.1 AUTOMOTIVE

10.3.1.1 Real-time monitoring and process optimization drive market expansion

10.3.2 SEMICONDUCTOR & ELECTRONICS

10.3.2.1 Emerging technologies and increasing production intricacies to boost SCADA adoption

10.3.3 OTHER DISCRETE MANUFACTURING

10.4 UTILITIES

10.4.1 POWER

10.4.1.1 Rising adoption of SCADA to enhance stability and reliability of power distribution

10.4.2 WATER & WASTEWATER TREATMENT

10.4.2.1 Adoption of Water 4.0 to drive demand for SCADA systems

10.4.3 TRANSPORTATION

10.4.3.1 Increasing adoption for advanced network monitoring and control in sector

10.4.3.2 Traffic signals

10.4.3.3 Mass transit systems and railway traction systems

10.4.4 TELECOMMUNICATION

10.4.4.1 Remote monitoring and management of network infrastructure, along with growing adoption of 5G, to drive market growth

11 SCADA MARKET, BY REGION

11.1 INTRODUCTION

11.2 NORTH AMERICA

11.2.1 US

11.2.1.1 Government initiatives to enhance SCADA cybersecurity and support market growth

11.2.2 CANADA

11.2.2.1 Rapid expansion of utility applications to accelerate demand for SCADA systems

11.2.3 MEXICO

11.2.3.1 SCADA adoption across electric grids to propel market growth

11.3 EUROPE

11.3.1 UK

11.3.1.1 Rising demand for efficient asset management in wind power sector to drive market growth

11.3.2 GERMANY

11.3.2.1 Increasing integration of automation solutions in automotive industry to drive market growth

11.3.3 FRANCE

11.3.3.1 Advancements in transportation systems and industrial automation to propel market growth

11.3.4 ITALY

11.3.4.1 Growing focus on digital automation and smart utilities to propel SCADA demand

11.3.5 SPAIN

11.3.5.1 Infrastructure modernization and renewable energy expansion driving SCADA adoption

11.3.6 REST OF EUROPE

11.4 ASIA PACIFIC

11.4.1 CHINA

11.4.1.1 Rapid adoption of SCADA in power and electronics to drive market growth

11.4.2 JAPAN

11.4.2.1 Rising investments in wind energy and renewable energy to fuel market expansion

11.4.3 SOUTH KOREA

11.4.3.1 Flourishing manufacturing industry to drive market growth

11.4.4 INDIA

11.4.4.1 Digital India initiative and urban infrastructure development to drive SCADA growth

11.4.5 AUSTRALIA

11.4.5.1 Emphasis on remote operations and critical infrastructure automation to boost SCADA usage

11.4.6 REST OF ASIA PACIFIC

11.5 REST OF THE WORLD

11.5.1 MIDDLE EAST

11.5.1.1 Need for efficient and secure monitoring and control solutions in industries to drive market growth

11.5.1.2 GCC countries

11.5.1.3 Rest of Middle East

11.5.2 AFRICA

11.5.2.1 Increased focus on energy production and expansion to support market growth

11.5.3 SOUTH AMERICA

11.5.3.1 Rising investments in energy sector to drive market growth

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS, 2021-2024

12.3 MARKET SHARE ANALYSIS, 2024

12.4 REVENUE ANALYSIS OF KEY COMPANIES, 2020-2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND/PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT, 2024

12.7.5.1 Overall footprint

12.7.5.2 Region footprint

12.7.5.3 Offering footprint

12.7.5.4 End user footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

12.8.1 PROGRESSIVE COMPANIES

12.8.2 RESPONSIVE COMPANIES

12.8.3 DYNAMIC COMPANIES

12.8.4 STARTING BLOCKS

12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES IN ECOSYSTEM, 2024

12.8.5.1 Detailed list of key startups/SMEs in ecosystem