VSAT 시장 : 최종 용도별, 용도별, 주파수별, 네트워크별, 지역별 예측(-2030년)

VSAT Market by End Use (Broadband, Voice Communication, Private Network), Application (Maritime, Aviation, Automotive, Government & Defense), Frequency (L, S, C, X, Ku, Ka, Multi-Band), Network (Standard VSAT, USAT) and Region - Global Forecast to 2030

상품코드:1781107

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 337 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

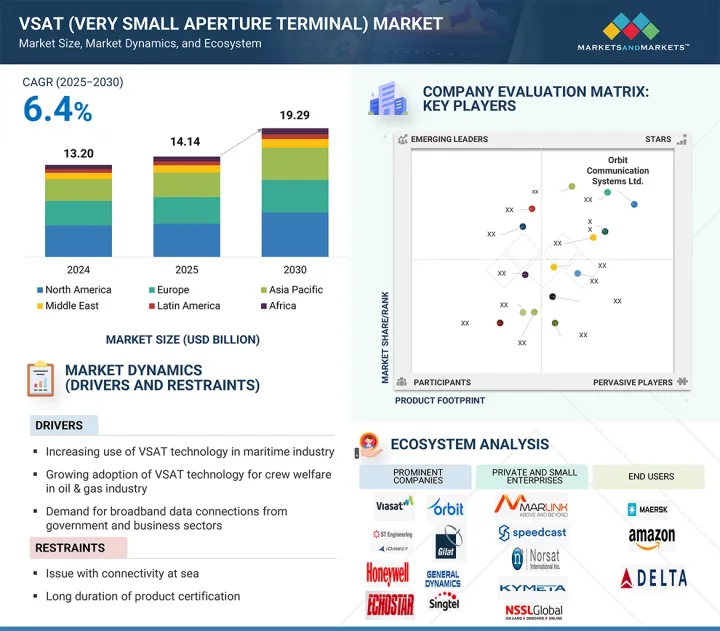

세계의 VSAT(Very Small Aperture Terminal) 시장 규모는 2025년에 추정 141억 4,000만 달러로 평가되었고, 2030년까지 192억 9,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR은 6.4%로 성장할 전망입니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

최종 용도, 용도, 주파수, 네트워크 및 지역별 부문

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

기술적 발전과 변화하는 시장 상황이 VSAT 시장의 주요 촉진요인입니다.

라기드 VSAT 디자인이 가장 높은 CAGR을 기록할 것으로 예상됩니다.

설계에 따르면, 라기드 VSAT는 열악한 환경 및 미션 크리티컬한 용도에서 사용이 증가함에 따라 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. 이 단말기는 고온, 진동, 먼지, 습도 및 충격을 견딜 수 있어 국방, 재해 복구, 석유 및 가스 현장, 광산에 이상적입니다. 지정학적 긴장이 고조되고 재해 관리의 필요성이 증가함에 따라 국방 기관과 정부는 라기드 장비가 필요한 현장 배치형 및 이동식 통신 장치에 더 많은 투자를 하고 있습니다. 에너지 및 인프라 분야에서의 해상 및 원격 지역 탐사 프로젝트도 혹독한 환경에서도 원활한 연결을 제공하는 이동식 및 중량급 VSAT 단말기를 요구하고 있습니다. 동적 비도시 지역에서의 보안 및 고대역폭 통신 수요 증가로 인해 내구성과 이동성, 신속한 배치 능력을 갖춘 라기드 VSAT가 점점 더 선호되고 있습니다. 경량 소재 및 소형 엔지니어링의 발전에 자극을 받은 이러한 발전은 예측 기간 동안 시장 성장을 촉진할 것으로 예상됩니다.

스타 토폴로지 네트워크는 2025년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

네트워크를 기준으로, 스타 토폴로지 부문은 기업 및 정부 네트워크에서 폭넓게 사용되고 있기 때문에 2025년에 VSAT 시장에서 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 스타 토폴로지에서는 모든 원격 단말기가 중앙 노드에 연결되어 중앙 집중식 제어, 대역폭 할당 편의성, 네트워크 관리를 가능하게 합니다. 이 아키텍처는 비디오 컨퍼런싱, 인터넷 접속, VoIP에 적합하며, 특히 단일 사무실에 안전한 확장 가능한 연결이 필요한 기업, 고등 교육 기관, 소매점, 은행 등에서 널리 사용됩니다. 허브 앤 스포크 아키텍처는 또한 더 간단한 네트워크 디버깅과 정책 적용을 지원하므로, 지역적으로 분산된 사업을 운영하는 조직에 가장 적합합니다. 스타 토폴로지는 메쉬 네트워크 전체에서 지연 시간을 최소화하고 처리량에서 더 큰 일관성을 제공하기 때문에 농촌 및 반도시 지역 가입자를 위한 위성 광대역 서비스에 선호적으로 사용됩니다. HTS 및 GEO 위성 시스템을 모두 활용할 수 있는 능력도 확장성 요인을 높입니다. 네트워크의 안정성과 비용 효율성이 여전히 최우선 과제인 상황에서 스타 토폴로지는 VSAT 네트워크 구성에서 계속해서 우위를 차지하고 있습니다.

아시아태평양 지역은 빠른 디지털화, 거대한 농촌 인구, 위성 통신 인프라에 대한 투자 증가에 힘입어 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. 인도, 인도네시아, 베트남, 필리핀은 섬과 외딴 지역의 디지털 격차를 해소하기 위해 위성 기반 광대역에 대한 수요가 증가하고 있습니다. 정부가 주도하는 농촌 연결 이니셔티브, 보편적 서비스 의무(USO) 및 민관 파트너십이 교육, 원격 의료 및 전자 정부를 위한 VSAT 배포를 촉진하고 있습니다. 이 지역 전체에 걸쳐 해상 무역, 상업용 항공 운송 및 국방 인프라가 성장하면서 모바일 VSAT 단말기의 사용도 증가하고 있습니다. 지역 위성 사업자와 지역 위성 군의 발전으로 서비스가 더욱 저렴하고 접근하기 쉬워지고 있습니다. LEO 및 HTS 위성 프로그램이 인기를 끌면서 아시아태평양 지역은 고정 및 이동 기반 용도에서 VSAT 보급률이 증가하는 고성장 지역으로 자리매김하고 있습니다.

이 보고서는 세계의 VSAT 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

VSAT 시장(2025-2030년)

VSAT 시장 : 최종 용도별

VSAT 시장 : 솔루션별

VSAT 시장 : 네트워크별

VSAT 시장 : 주파수별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

고객사업에 영향을 주는 동향 및 혼란

밸류체인 분석

생태계 분석

저명 기업

민간기업과 중소기업

시장 생태계

규제 상황

무역 데이터

수입 시나리오

수출 시나리오(HS 코드 880260)

주요 이해관계자와 구매 기준

기술 분석

주요 기술

보완 기술

인접 기술

사례 연구 분석

사례 연구 1 : L3HARRIS 전술 단말 - 방위군용 미션 크리티컬 VSAT 통신 실현

사례 연구 2 : KYMETA의 평면 패널 VSAT 안테나 발사와 ONEWEB LEO를 통한 해상 연결

사례 연구 3 : Exterter University, Technical Composite Systems, Cobham Aerospace Connectivity에 의한 메타물질 안테나 개발

주요 컨퍼런스 및 이벤트(2025-2026년)

VSAT 시장에 대한 미국 관세의 영향(2025년)

소개

주요 관세율

가격의 영향 분석

국가 및 지역에 미치는 영향

미국

유럽

아시아태평양

최종 이용 산업에 미치는 영향

상업

정부 및 방위

산업 및 모빌리티

거시경제 전망

소개

북미

유럽

아시아태평양

중동

라틴아메리카

아프리카

VSAT 시장에 대한 AI/생성형 AI의 영향

네트워크 최적화 및 예측 유지보수

AI 기반 빔 관리 및 동적 대역폭 할당

자동화된 고장 탐지 및 원격 진단

네트워크 시뮬레이션 및 설계

개인 맞춤형 서비스 제공 및 사용자 경험

운용 데이터

가격 설정 분석

비즈니스 모델

기술 로드맵

투자 및 자금조달 시나리오

총 소유 비용

부품표

소개

기술 동향

다양한 중요 용도를 지원하는 라우터 기술의 혁신

VSAT 시스템의 처리량 향상을 위한 대역폭 효율 개선

VSAT 시스템에서 시분할 다중 접속(TDMA) 기술 사용

4축 안정화 VSAT 안테나 시스템

고급 1M KA-/KU-BAND 해상 VSAT 안테나

위성 통신에서 KA 대역와 KU 대역 VSAT의 이용

다중 대역 전술 통신 증폭기

차세대 VSAT을 가능하게 하는 고급 안테나

초소형 및 고대역폭 이동 중(OTM) 터미널 전술용 무인 항공기(UAV)용

하이브리드 해상 VSAT 네트워크 솔루션

메가 트렌드의 영향

공급망의 혼란

스마트 안테나 개발

하이브리드 빔포밍 방식

특허 분석

제6장 VSAT 시장 : 유형별

소개

표준 VSAT

USAT

제7장 VSAT 시장 : 설계별

소개

라기드 VSAT

비라기드 VSAT

제8장 VSAT 시장 : 주파수별

소개

L 대역

S 대역

C 대역

X 대역

KU 대역

KA 대역

멀티 대역

제9장 VSAT 시장 : 네트워크별

소개

스타 토폴로지

메쉬 토폴로지

하이브리드 토폴로지

포인트 투 포인트 링크

제10장 VSAT 시장 : 솔루션별

소개

장치

지원 서비스

접속성 서비스

제11장 VSAT 시장 : 플랫폼별

소개

육상 VSAT

해상 VSAT

항공 VSAT

제12장 VSAT 시장 : 최종 용도별

소개

광대역/데이터 네트워크 서비스

음성통신 서비스

프라이빗 네트워크 서비스

방송 서비스

기타

제13장 VSAT 시장 : 용도별

소개

의료

에너지 및 전력

교육

BFSI

미디어 및 엔터테인먼트

소매

수송 및 물류

통신

선박

항공

농업 및 임업

광업 및 건설

제조

자동차

정부 및 방위

기타

제14장 지역 분석

소개

북미

PESTLE 분석

미국

캐나다

유럽

PESTLE 분석

영국

프랑스

독일

기타 유럽

아시아태평양

PESTLE 분석

중국

인도

일본

한국

기타 아시아태평양

중동

PESTLE 분석

GCC

기타 중동

라틴아메리카

PESTLE 분석

브라질

멕시코

기타 라틴아메리카

아프리카

PESTLE 분석

남아프리카

나이지리아

기타 아프리카

제15장 경쟁 구도

소개

수익 분석

시장 점유율 분석

기업 평가 매트릭스 : 주요 기업(2024년)

기업 실적

기업의 평가 매트릭스 : 스타트업 및 중소기업(2024년)

브랜드/제품 비교

기업 평가 및 재무 지표

경쟁 시나리오

제16장 기업 프로파일

주요 기업

ORBIT COMMUNICATION SYSTEMS LTD.

L3HARRIS TECHNOLOGIES INC.

VIASAT INC.

GILAT SATELLITE NETWORKS LTD.

ECHOSTAR CORPORATION(US)

COMTECH TELECOMMUNICATIONS CORPORATION

ST ENGINEERING IDIRECT

KVH INDUSTRIES, INC.

GENERAL DYNAMICS CORPORATION

THALES GROUP

HONEYWELL INTERNATIONAL INC.

SINGTEL

MITSUBISHI ELECTRIC CORPORATION

ULTRA ELECTRONICS

SATIXFY COMMUNICATIONS LTD

기타 기업

THE MARLINK GROUP

THURAYA TELECOMMUNICATIONS COMPANY

SPEEDCAST INTERNATIONAL LTD.

ND SATCOM GMBH

NORSAT INTERNATIONAL INC.

NSSL GLOBAL SOLUTIONS PVT. LTD.

OMNIACCESS SL

KYMETA CORPORATION

KOGNITIVE NETWORKS

VIKING SATCOM LLC

제17장 부록

HBR

영문 목차

영문목차

The VSAT (Very Small Aperture Terminal) market is estimated at USD 14.14 billion in 2025 and is projected to reach USD 19.29 billion by 2030 at a CAGR of 6.4% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By End Use, Application, Frequency, Network and Region

Regions covered

North America, Europe, APAC, RoW

Technological advancements and changing market conditions are the key drivers of the VSAT market.

"The rugged VSAT design is projected to register the highest CAGR."

Based on design, rugged VSAT is projected to register the highest CAGR during the forecast period due to its increasing use in hostile and mission-critical applications. The terminals withstand high temperatures, vibration, dust, humidity, and shock, making them ideal for defense, disaster recovery, oil & gas sites, and mines. With rising geopolitical tensions and disaster management needs, defense agencies and governments are spending more on field-deployable and mobile communication units that demand ruggedized equipment. Off-shore and remote-area exploration ventures in sectors such as energy and infrastructure also demand transportable and heavy-duty VSAT units capable of providing seamless connectivity under harsh conditions. With the increasing demand for secure, high-bandwidth communications in dynamic, non-metropolitan regions, rugged VSATs are increasingly favored for their durability, mobility, and rapid deployment capabilities. This development, stimulated by advancements in lightweight materials and miniaturized engineering, is expected to drive market growth during the forecast period.

"The star topology network is estimated to hold the largest market share in 2025."

Based on network, the star topology segment is estimated to hold the largest market share in 2025 in the VSAT market due to its broad use in enterprise and government networks. In a star topology, all remote terminals are connected to a central node, enabling centralized control, bandwidth allocation ease, and network management. This architecture works for video conferencing, internet access, and VoIP, especially for business organizations, institutions of higher education, retail stores, and banks, where there are single offices that need secure and scalable links. Hub-and-spoke architecture also supports simpler network debugging as well as policy imposition, so it is best suited to organizations that have geographically distributed businesses. Star topology is preferably utilized for satellite broadband services to rural and semi-urban subscribers due to its capability to minimize latency throughout mesh networks as well as providing greater consistency in throughput. Its ability to utilize both HTS and GEO satellite systems also increases its scalability factor. As network reliability and cost-effectiveness remain top priorities, star topology continues to dominate VSAT network configurations.

"Asia Pacific is projected to be the fastest-growing market during the forecast period."

Asia Pacific is projected to register the highest CAGR during the forecast period, driven by rapid digitalization, a huge rural population, and growing investments in satellite communications infrastructure. India, Indonesia, Vietnam, and the Philippines are witnessing a growing need for satellite-based broadband to fill the digital divide in island and remote geographies. Government-initiated rural connectivity initiatives, universal service obligations (USOs), and public-private partnerships are driving VSAT deployment for education, telemedicine, and e-governance. Growing maritime commerce, commercial air transport, and defense infrastructure build-up throughout the region are also driving the use of mobile VSAT terminals. The development of regional satellite operators and regional satellite constellations is making services more affordable and accessible. With LEO and HTS satellite programs becoming more popular, Asia Pacific is positioned as a high-growth region experiencing growing VSAT penetration in fixed and mobility-based applications.

The breakdown of the profile of primary participants in the VSAT market is as follows:

By Company Type: Tier 1- 35%, Tier 2- 45%, and Tier 3- 20%

By Designation: Directors- 25%, Managers- 35%, Others- 40%

By Region: North America- 30%, Europe- 20%, Asia Pacific- 35%, Middle East- 10%, Rest of World- 5%

Research Coverage

The study covers the VSAT market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different segments. This study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their solutions and business offerings, recent developments undertaken by them, and key market strategies adopted by them.

This report segments the VSAT (Very Small Aperture Terminal) market across five key regions: North America, Europe, Asia Pacific, the Middle East, and the Rest of the World, as well as their respective key countries. The report's scope includes in-depth information on significant factors, such as drivers, restraints, challenges, and opportunities that influence the growth of the VSAT market.

A comprehensive analysis of major industry players has been conducted to provide insights into their business profiles, solutions, and services. This analysis also covers key aspects like agreements, collaborations, product launches, contracts, expansions, acquisitions, and partnerships associated with the VSAT market.

Reasons to Buy the Report

This report serves as a valuable resource for market leaders and new entrants in the VSAT market, offering data that closely approximates revenue figures for both the overall market and its subsegments. It equips stakeholders with a comprehensive understanding of the competitive landscape, facilitating informed decisions to enhance their market positioning and formulating effective go-to-market strategies. The report imparts valuable insights into the market dynamics, offering information on crucial factors such as drivers, restraints, challenges, and opportunities, enabling stakeholders to gauge the market's pulse.

The report provides insights into the following pointers:

Analysis of key drivers and factors, such as increasing use of VSAT technology in the maritime industry, growing adoption of VSAT technology for crew welfare in the oil & gas industry, demand for broadband data connections from government and business sectors, low investment and operating costs, and the increasing use of Ku- and Ka-band VSATs

Market Penetration: Comprehensive information on VSAT solutions offered by the top players in the market

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the VSAT market

Market Development: Comprehensive information about lucrative markets (the report analyzes the VSAT market across varied regions)

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the VSAT market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the VSAT market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 VSAT (VERY SMALL APERTURE TERMINAL) MARKET SEGMENTATION AND REGIONAL SNAPSHOT

1.3.2 YEARS CONSIDERED

1.4 CURRENCY AND PRICING

1.5 INCLUSIONS AND EXCLUSIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.3 KEY PRIMARY SOURCES

2.2 FACTOR ANALYSIS

2.2.1 INTRODUCTION

2.2.2 DEMAND-SIDE INDICATORS

2.2.3 SUPPLY-SIDE INDICATORS

2.3 RESEARCH APPROACH AND METHODOLOGY

2.3.1 BOTTOM-UP APPROACH

2.3.1.1 Market size estimation & methodology

2.3.1.2 Regional split of VSAT market

2.3.2 TOP-DOWN APPROACH

2.4 DATA TRIANGULATION

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 VSAT (VERY SMALL APERTURE TERMINAL) MARKET, 2025-2030

4.2 VSAT (VERY SMALL APERTURE TERMINAL) MARKET, BY END USE

4.3 VSAT (VERY SMALL APERTURE TERMINAL) MARKET, BY SOLUTION

4.4 VSAT (VERY SMALL APERTURE TERMINAL) MARKET, BY NETWORK

4.5 VSAT (VERY SMALL APERTURE TERMINAL) MARKET, BY FREQUENCY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Growing adoption of VSAT technology for crew welfare in oil & gas industry

5.2.1.2 Increasing need for VSAT systems in maritime industry

5.2.1.3 Surging demand for broadband data connections from government and business sectors

5.2.1.4 Low investment and operating costs

5.2.1.5 Increasing use of Ku- and Ka-band VSATs

5.2.1.6 High use of USATs for on-the-move applications

5.2.2 RESTRAINTS

5.2.2.1 Issues with connectivity at sea

5.2.2.2 Long duration of product certification

5.2.3 OPPORTUNITIES

5.2.3.1 Rising need for VSAT systems to enable telemedicine in remote locations

5.2.3.2 Growing demand for autonomous and connected vehicles

5.2.3.3 Increasing use of ultra-compact Ku-band VSATs for tactical UAVs

5.2.3.4 Rising number of LEO-HTS constellations

5.2.4 CHALLENGES

5.2.4.1 Cybersecurity concerns

5.2.4.2 Radio spectrum availability issues

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.5.1 PROMINENT COMPANIES

5.5.2 PRIVATE AND SMALL ENTERPRISES

5.5.3 MARKET ECOSYSTEM

5.6 REGULATORY LANDSCAPE

5.6.1 REGULATORY FRAMEWORK

5.6.1.1 North America

5.6.1.2 Europe

5.7 TRADE DATA

5.7.1 IMPORT SCENARIO

5.7.2 EXPORT SCENARIO (HS CODE 880260)

5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.8.2 BUYING CRITERIA

5.9 TECHNOLOGY ANALYSIS

5.9.1 KEY TECHNOLOGIES

5.9.1.1 Beamforming technology

5.9.1.2 Software-defined networking (SDN) in satellite networks

5.9.2 COMPLEMENTARY TECHNOLOGIES

5.9.2.1 Power over Ethernet (PoE) Systems

5.9.2.2 Remote terminal management software

5.9.3 ADJACENT TECHNOLOGIES

5.9.3.1 5G Non-terrestrial networks (NTN)

5.9.3.2 Network management systems (NMS)

5.10 CASE STUDY ANALYSIS

5.10.1 CASE STUDY 1: L3HARRIS TACTICAL TERMINALS - ENABLING MISSION-CRITICAL VSAT COMMUNICATIONS FOR DEFENSE FORCES

5.10.2 CASE STUDY 2: KYMETA'S FLAT-PANEL VSAT ANTENNA LAUNCH FOR MARITIME CONNECTIVITY VIA ONEWEB LEO

5.10.3 CASE STUDY 3: METAMATERIAL ANTENNA DEVELOPMENT BY UNIVERSITY OF EXETER, TECHNICAL COMPOSITE SYSTEMS, AND COBHAM AEROSPACE CONNECTIVITY

5.11 KEY CONFERENCES AND EVENTS, 2025-2026

5.12 IMPACT OF 2025 US TARIFFS ON VSAT MARKET

5.13 INTRODUCTION

5.14 KEY TARIFF RATES

5.15 PRICE IMPACT ANALYSIS

5.16 IMPACT ON COUNTRY/REGION

5.16.1 US

5.16.2 EUROPE

5.16.3 ASIA PACIFIC

5.17 IMPACT ON END-USE INDUSTRIES

5.17.1 COMMERCIAL

5.17.2 GOVERNMENT & DEFENSE

5.17.3 INDUSTRIAL & MOBILITY

5.18 MACROECONOMIC OUTLOOK

5.18.1 INTRODUCTION

5.18.2 NORTH AMERICA

5.18.3 EUROPE

5.18.4 ASIA PACIFIC

5.18.5 MIDDLE EAST

5.18.6 LATIN AMERICA

5.18.7 AFRICA

5.19 IMPACT OF AI/ GENERATIVE AI ON VSAT MARKET

5.19.1 NETWORK OPTIMIZATION AND PREDICTIVE MAINTENANCE

5.19.2 AI-BASED BEAM MANAGEMENT AND DYNAMIC BANDWIDTH ALLOCATION

5.19.3 AUTOMATED FAULT DETECTION AND REMOTE DIAGNOSTICS

5.19.4 NETWORK SIMULATION AND DESIGN

5.19.5 PERSONALIZED SERVICE DELIVERY AND USER EXPERIENCE

5.20 OPERATIONAL DATA

5.21 PRICING ANALYSIS

5.21.1 AVERAGE SELLING PRICE OF VSAT FOR TOP 3 PLATFORMS, BY KEY PLAYERS

5.22 BUSINESS MODELS

5.22.1 BUSINESS MODELS IN VSAT MARKET

5.23 TECHNOLOGY ROADMAP

5.24 INVESTMENT AND FUNDING SCENARIO

5.25 TOTAL COST OF OWNERSHIP

5.26 BILL OF MATERIALS

5.27 INTRODUCTION

5.28 TECHNOLOGY TRENDS

5.28.1 INNOVATIONS IN ROUTER TECHNOLOGY TO SUPPORT WIDE RANGE OF CRITICAL APPLICATIONS

5.28.2 IMPROVEMENT IN BANDWIDTH EFFICIENCY TO ACHIEVE MORE THROUGHPUT IN VSAT SYSTEMS

5.28.3 USE OF TIME DIVISION MULTIPLE ACCESS (TDMA) TECHNOLOGY IN VSAT SYSTEMS