환자 등록 소프트웨어 시장(-2030년) : 질환, 제품, 이용 사례, 최종 사용자 및 지역별

Patient Registry Software Market by Disease (Diabetes, Cancer, Rare, Asthma, Kidney), Product (Drugs, Device), Use Case (Population Health, Research), End User [(Profit: Pharma, Payer, Hospital), (Non-Profit: Govt)] & Region - Global Forecast to 2030

상품코드:1780347

리서치사:MarketsandMarkets

발행일:2025년 07월

페이지 정보:영문 381 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

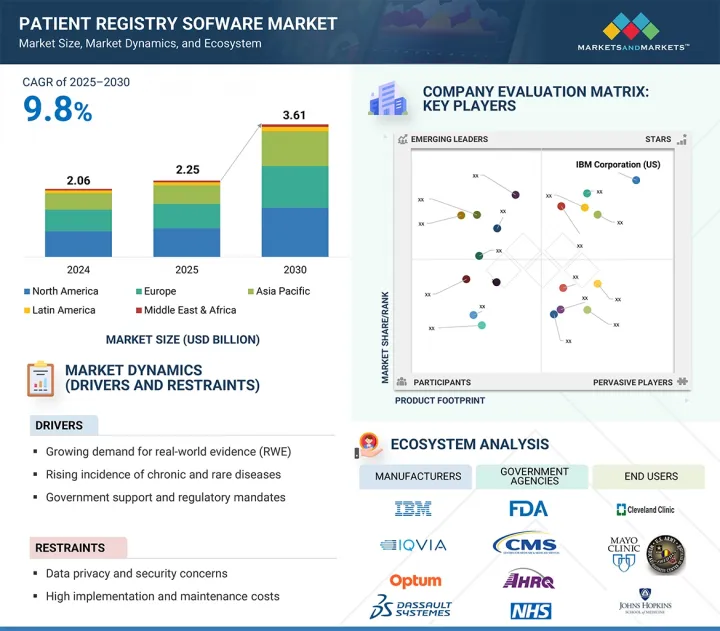

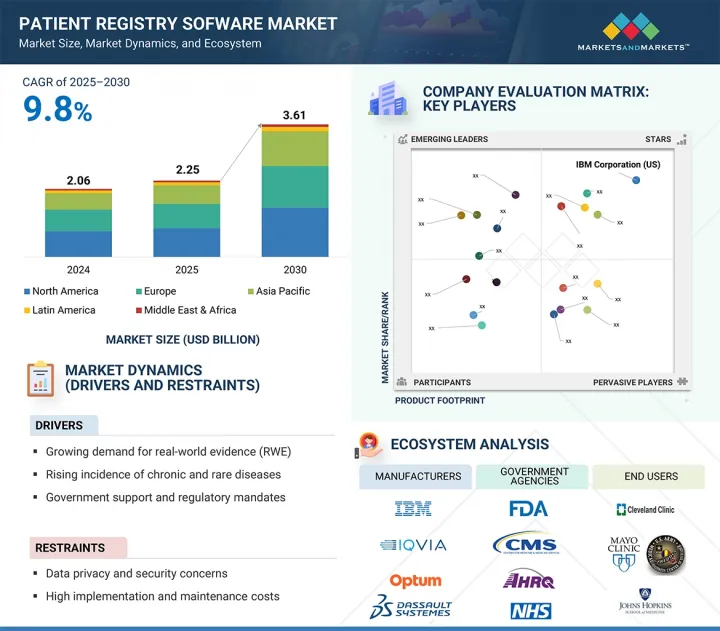

세계의 환자 등록 소프트웨어 시장 규모는 2025년 22억 5,000만 달러로 평가되었고, 2030년에는 36억 1,000만 달러에 이를 것으로 예측되며, CAGR 9.8%로 성장할 전망입니다.

의료 시스템은 케어의 질을 향상시키고 규제 요구 사항을 충족하기 위해 환자 데이터 수집 및 분석에 점점 더 많은 노력을 기울이고 있습니다. 건강 관리를 지원합니다.이 플랫폼은 의약품 평가 및 가치 기반 관리를 지원하는 실제 세계 데이터를 창출하는 데 필수적이며 궁극적으로 의료 비용을 줄이고 시장 성장을 가속하는 역할을합니다.

조사 범위

조사 대상 연도

2023-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

금액(달러)

부문

제품, 이용 사례, 등록 유형, 도입 모델 및 최종 사용자

대상 지역

북미, 유럽, 아시아태평양, 라틴 아메리카, 중동 및 아프리카

환자 직접 등록 부문은 예측 기간 동안 가장 높은 성장을 보일 것으로 예상됩니다.

환자 등록 소프트웨어 시장은 환자 직접 등록과 사이트 기반 및 임상 데이터 등록으로 나뉩니다. 환자 직접 등록 시스템은 환자 참여 증가, 디지털 헬스케어 도구(ePRO 및 모바일 앱 등)의 채택, 환자 기반 실세계 증거에 대한 수요, 환자 보고 결과에 초점을 맞춘 분산형 임상 시험의 확산으로 인해 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 가상 플랫폼은 데이터 수집을 간소화하여 의료 제공자의 부담을 줄이고 장기적 추적 관리 및 다양한 환자 모집을 가능하게 합니다.

2024년에는 의료 연구 및 임상 연구 부문이 이용 사례별로 환자 등록 소프트웨어 시장에서 가장 큰 점유율을 차지할 것입니다.

2024년에는 의료 연구 및 임상 연구 부문이 환자 등록 소프트웨어 시장을 지배할 것입니다. 이러한 성장은 임상 시험 및 의약품 개발에 실제 데이터(RWD) 및 실제 증거(RWE)의 사용이 증가함에 따라 크게 촉진될 것입니다. 환자 등록 소프트웨어는 구조화되고 종단적인 환자 데이터를 캡처하여 연구자가 결과를 분석하고 안전성을 모니터링하는 데 도움을 줍니다. 맞춤형 의약품의 부상과 생명 과학 기업, 학술 센터 및 공중 보건 기관 간의 협력이 강화되면서 강력한 등록 인프라에 대한 필요성이 더욱 높아지고 있습니다. 분산형 임상 시험 및 시판 후 감시로 전환되는 추세도 이 부문의 선도적 위치를 강화하고 있습니다.

2024년에 북미는 환자 등록 소프트웨어 시장에서 가장 큰 점유율을 차지했습니다.

2024년에는 강력한 규제 프레임워크와 디지털 헬스케어의 조기 채택에 힘입어 북미가 환자 등록 소프트웨어 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. MRO Corp 및 ImageTrend와 같은 주요 업체들은 경쟁과 혁신을 강화하고 있습니다. 미국 HHS의 데이터 현대화 및 CDC의 만성 질환 감시에 대한 집중과 같은 연방 정부의 이니셔티브는 등록 플랫폼에 대한 수요를 증가시키고 있습니다. 특히, 2025년 2월, Veradigm과 HealthVerity는 심혈관 및 대사 데이터를 HealthVerity의 개인 정보 보호 준수 플랫폼과 통합하기 위해 제휴를 맺어 환자 여정에 대한 종합적인 연구를 가능하게 했습니다. 또한, 2024년 4월, ESO Solutions는 데이터 기반의 응급 대응을 개선하고 상호 운용성과 환자 치료 결과를 향상시키기 위해 Logis Solutions를 인수했습니다. 이러한 발전은 환자 등록 소프트웨어 혁신 및 데이터 통합 분야에서 북미의 리더십을 더욱 공고히 할 것입니다.

본 보고서에서는 세계의 환자 등록 소프트웨어 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이와 예측, 각종 구분 및 지역 및 주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

시장 역학

시장 역학

시장 성장 억제요인

시장 기회

시장의 과제

고객의 사업에 영향을 미치는 동향 및 혼란

업계 동향

생태계 분석

밸류체인 분석

기술 분석

규제 분석

가격 분석

Porter's Five Forces 분석

특허 분석

주요 이해관계자와 구매 기준

최종 사용자 분석

주요 회의 및 이벤트

사례 연구 분석

투자 및 자금조달 시나리오

비즈니스 모델 분석

AI/생성형 AI가 환자 등록 소프트웨어 시장에 미치는 영향

미국 관세가 환자 등록 소프트웨어 시장에 미치는 영향(2025년)

제6장 환자 등록 소프트웨어 시장 : 등록 유형별

질병 등록

당뇨병 등록

심장혈관 등록

암 등록

희소질환 등록

천식 등록

만성 신질환 등록

정형외과 등록

예방접종 등록

선천성 이상 등록

기타 질환 등록

제품 등록

의료기기 등록

의약품 등록

제7장 환자 등록 소프트웨어 시장 : 제품별

환자 직접 등록(환자 기록 등록)

사이트 기반 및 임상 데이터(공급자 기록) 등록

제8장 환자 등록 소프트웨어 시장 : 이용 사례별

의료 연구 및 임상 연구

품질 향상

환자 케어 관리

집단건강(포퓰레이션헬스)

포인트 오브 케어 서포트

공중 위생 감시

환자의 셀프 케어

환자 참여

기타

제9장 환자 등록 소프트웨어 시장 : 도입 모델별

온프레미스 모델

클라우드 기반 모델

제10장 환자 등록 소프트웨어 시장 : 최종 사용자별

영리목적 등록

제약, 생명공학, 의료기기 기업

의료보험자

의료 제산업체

비영리목적 등록

의료전문학회

환자 단체

정부 및 타사 관리 기관

기타

제11장 환자 등록 소프트웨어 시장 : 지역별

북미

거시경제 전망

미국

캐나다

유럽

거시경제 전망

영국

독일

프랑스

이탈리아

스페인

기타

아시아태평양

거시경제 전망

일본

중국

인도

기타

라틴아메리카

라틴아메리카의 거시 경제 전망

브라질

멕시코

기타

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

GCC 국가

기타

제12장 경쟁 구도

개요

주요 진입기업의 전략 및 강점

수익 분석

시장 점유율 분석

기업 평가 매트릭스 : 주요 기업

기업평가 매트릭스 : 스타트업 및 중소기업

기업평가와 재무지표

브랜드/소프트웨어 비교

경쟁 시나리오

제13장 기업 프로파일

주요 기업

IBM

IQVIA HOLDINGS INC.

HEALTH CATALYST, INC.

ORACLE

UNITEDHEALTH GROUP

CONDUENT INCORPORATED

ELEKTA

NEC CORPORATION(NEC SOFTWARE SOLUTIONS UK LIMITED)

DASSAULT SYSTEMES(MEDIDATA)

EVIDENTIQ(DACIMA SOFTWARE INC.)

MRO(FIGMD, INC.)

IMAGETREND

GLOBAL VISION TECHNOLOGIES, INC.

SYNEOS HEALTH

VERADIGM LLC

ESO

ORDINAL DATA INC.

CEDARON MEDICAL

FIVOS HEALTH

ACROSS HEALTHCARE

기타 기업

VERANA HEALTH

PULSE INFOFRAME INC.

AMPLITUDE CLINICAL OUTCOMES

NPHASE, INC.(REDCAP CLOUD)

OM1

제14장 부록

HBR

영문 목차

영문목차

The global patient registry software market is expected to reach USD 3.61 billion by 2030 from USD 2.25 billion in 2025, at a CAGR of 9.8%. Healthcare systems are increasingly focused on capturing and analyzing patient data to enhance care quality and meet regulatory requirements. Patient registry software collects disease, procedure, and population data, facilitating clinical research and population health management. These platforms are vital for generating real-world evidence to support drug assessments and value-based care, ultimately reducing healthcare costs and driving market growth.

Scope of the Report

Years Considered for the Study

2023-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Product, Use Case, Registry Type, Deployment Model, and End User

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

"The direct-to-patient registries segment is expected to witness the highest growth during the forecast period."

The patient registry software market is divided into direct-to-patient and site-based/clinical data registries. Direct-to-patient registries are expected to register the highest CAGR due to increased patient engagement, adoption of digital health tools (like ePRO and mobile apps), demand for real-world evidence from patients, and the rise of decentralized clinical trials that focus on patient-reported outcomes. Virtual platforms simplify data collection, easing the burden on healthcare providers and allowing for better longitudinal follow-up and diverse patient recruitment.

"The medical research & clinical studies segment held the largest share of the patient registry software market, by use case, in 2024."

In 2024, the medical research & clinical studies segment dominated the patient registry software market. This growth is largely driven by the increasing use of real-world data (RWD) and real-world evidence (RWE) for clinical trials and drug development. Patient registry software captures structured and longitudinal patient data, helping researchers analyze outcomes and monitor safety. The rise of personalized medicine and collaborations among life science companies, academic centers, and public health agencies further enhances the need for robust registry infrastructure. The shift toward decentralized trials and post-marketing surveillance also reinforces this segment's leading position.

"North America accounted for the largest share of the patient registry software market in 2024."

In 2024, North America held the largest share of the patient registry software market, driven by strong regulatory frameworks and early digital health adoption. Key players like MRO Corp and ImageTrend enhance competition and innovation. Federal initiatives, such as the US HHS's data modernization and the CDC's focus on chronic disease surveillance, increase the demand for registry platforms. Notably, in February 2025, Veradigm and HealthVerity partnered to integrate cardiovascular and metabolic data with HealthVerity's privacy-compliant platform, enabling comprehensive research on patient journeys. Additionally, in April 2024, ESO Solutions acquired Logis Solutions to improve data-driven emergency response, enhancing interoperability and patient outcomes. These developments solidify North America's leadership in patient registry software innovation and data integration.

The breakdown of primary participants is listed below:

By Company Type: Tier 1 (45%), Tier 2 (30%), and Tier 3 (25%)

By Designation: C-level Executives (42%), Directors (31%), and Others (27%)

By Region: North America (35%), Europe (30%), Asia Pacific (25%), the Middle East & Africa (5%), and Latin America (5%)

Key Players in the Patient Registry Software Market

The key players in the patient registry software market include IBM (US), IQVIA Holdings Inc. (US), Health Catalyst Inc. (US), Oracle (US), UnitedHealth Group (US), Conduent Inc. (US), Elekta (Sweden), Dassault Systemes (France), EvidentIQ (Dacima Software Inc.) (Germany), MRO (Figmd, Inc.) (US), ImageTrend, Inc. (US), Global Vision Technologies, Inc. (US), Syneos Health (US), Veradigm LLC (US), ESO (US), Ordinal Data, Inc. (US), NEC Corporation (NEC Software Solutions UK Limited) (Japan), Cedaron Medical (US), Fivos Health (US), and Across Health (US).

Research Coverage

The report analyzes the patient registry software market. Its objective is to estimate the market size and future growth potential of various segments, categorized by product, registry type, use case, deployment model, end user, and region. Additionally, the report includes a competitive analysis of the key players in this market, featuring their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will help both established companies and new or smaller firms assess the market's current state, enabling them to capture a larger market share. Organizations that purchase this report can utilize one or more of the strategies outlined below to enhance their market positions.

This report provides insights on:

Analysis of Key Drivers: Drivers (growing demand for real-world evidence (RWE) and rising incidence of chronic and rare diseases), restraints (high setup and operational costs and limited access in low-resource settings), opportunities [integration with AI and analytics tools and expanding use in decentralized clinical trials (DCTs)], and challenges (inconsistent data quality and completeness and limited workforce expertise) influencing the growth of the patient registry software market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the patient registry software market.

Market Development: Comprehensive information on the lucrative emerging markets, products, use cases, registry types, deployment models, end users, and regions.

Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the patient registry software market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the patient registry software market, such as IBM (US), IQVIA Holdings Inc. (US), Health Catalyst Inc. (US), Oracle (US), UnitedHealth Group (US), Conduent Inc. (US), and Elekta (Sweden).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakdown of primary sources

2.2 RESEARCH METHODOLOGY DESIGN

2.3 MARKET SIZE ESTIMATION

2.4 MARKET BREAKDOWN & DATA TRIANGULATION

2.5 RESEARCH ASSUMPTIONS

2.5.1 MARKET SIZING ASSUMPTIONS

2.5.2 OVERALL STUDY ASSUMPTIONS

2.6 RISK ASSESSMENT

2.7 RESEARCH LIMITATIONS

2.7.1 METHODOLOGY-RELATED LIMITATIONS

2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PATIENT REGISTRY SOFTWARE MARKET OVERVIEW

4.2 NORTH AMERICA: PATIENT REGISTRY SOFTWARE MARKET, BY PRODUCT & REGION