지게차 시장 예측(-2032년) : 추진력별, 톤수별, 최종 용도 산업별, 클래스별, 조작별, 용도별, 배터리 유형별, 리프팅 능력별, 타이어별, 제품 유형별, 지역별

Forklift Market by Propulsion (Electric, ICE, Fuel Cell), Tonnage Capacity, End-Use Industry, by Class (1, 2, 31, 32, 4/5), Operation, Application, Battery Type (Li-ion, Lead Acid), Lifting Capacity, Tire, Product Type, Region - Global Forecast to 2032

상품코드:1858524

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 362 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

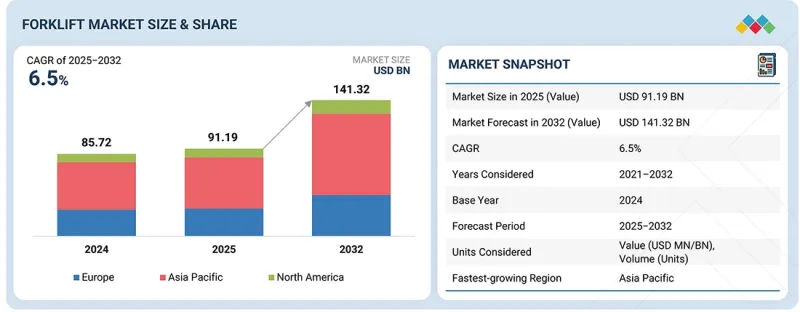

세계의 지게차 시장 규모는 2025년 911억 9,000만 달러에서 2032년까지 1,413억 2,000만 달러에 달할 것으로 예측되며, CAGR로 6.5%의 성장이 전망됩니다.

지게차는 가장 일반적인 물류 시스템 중 하나이며, 다양한 용도의 자재를 효율적으로 취급하는 것으로 알려져 있습니다. 컴팩트한 크기, 중량물 운반 능력, 범용성으로 인해 지게차는 자재관리 작업에서 선호되는 선택이 되었습니다. 아시아태평양 시장은 예측 기간 중 성장하여 세계 지게차 시장을 장악할 것으로 예측됩니다. Toyota Industries Corporation, Kion Group, Jungheinrich AG 등 주요 OEM들은 생산성과 효율성을 높이는 혁신적인 전기 및 자율주행 모델로 전환을 추진하고 있습니다.

조사 범위

조사 대상 연도

2021-2032년

기준연도

2025년

예측 기간

2025-2032년

단위

금액, 수량(대)

부문

추진력, 톤수, 최종 용도 산업, 클래스, 조작, 용도, 배터리 유형, 리프팅 능력, 타이어, 제품 유형, 지역

대상 지역

아시아태평양, 북미, 유럽, 기타 지역

또한 지게차에 탑재된 실시간 위치 모니터링 및 자동 자재관리 기능을 갖춘 AI의 등장은 최고 수준의 창고 자동화에 혁명을 가져왔으며, 세계 창고 업계의 주요 기업이 최적화된 경영을 위해 자율 지게차를 더 많이 배치하도록 유도하고 있습니다. 하고 있습니다. 미국의 NIOSH(National Institute for Occupational Safety and Health)와 OSHA(Occupational Safety and Health Administration)와 같은 기관은 자율 지게차 시장에서 센서가 장착된 지게차가 보다 안전한 탐색과 적재물 관리를 촉진하여 작업장 사고를 줄일 수 있다는 점을 강조하며, 이러한 진전을 강조하고 있습니다.

"전동 지게차는 예측 기간 중 세계 시장에서 우위를 유지할 것으로 예측됩니다."

전동 지게차는 세계 시장에서 가장 큰 점유율을 차지하고 있습니다. 클래스 1, 클래스 2, 클래스 3, 클래스 2로 분류되는 이 지게차는 전동식이며, 2024년 기준 시장의 70% 이상을 차지할 것으로 예측됩니다. 전동 지게차 수요는 전 세계에서 산업 차량에 대한 엄격한 배기가스 배출 기준을 준수해야 할 필요성으로 인해 증가하는 추세입니다. 또한 전기 지게차는 내연기관(ICE) 지게차에 비해 소유 비용을 절감하고 투자수익률(ROI)을 향상시킵니다.

리튬이온 배터리의 보급은 전동 지게차의 우위를 보장하는 또 다른 추세입니다. 이 리튬이온 배터리는 빠른 충전, 최소한의 정비 및 기존 납축 배터리 유형보다 긴 수명을 제공합니다. 예를 들어 리튬인산철(LFP) 배터리는 안전 프로파일, 긴 수명, 비용 우위성으로 인해 대부분의 OEM이 선호하고 있으며, 다교대 창고 운영 및 저온 저장 환경에 매력적입니다. BloombergNEF에 따르면 2024년 12월까지 리튬이온 배터리 팩의 가격은 1kWh당 115달러로 사상 최저 수준으로 하락하여 2023년 대비 20% 하락하여 2017년 이후 가장 큰 연간 하락률을 기록할 것으로 예상했습니다. 이처럼 배터리 기술의 발전과 더불어 엄격한 배출 기준과 저비용으로 효율적인 창고 관리에 대한 수요가 증가함에 따라 전동 지게차 수요는 향후 수년간 증가할 것으로 예측됩니다.

"E-Commerce 산업에서 지게차 수요는 조사 기간 중 가장 빠른 CAGR로 성장할 것으로 예측됩니다."

지게차는 보다 빠르고 효율적인 상품 취급이 가능하므로 E-Commerce 산업에서 매우 유용하며, 이 부문의 성장을 직접적으로 지원하고 있습니다. 소비자의 구매가 오프라인 매장에서 디지털 플랫폼으로 이동하는 가운데, 지게차는 창고와 물류센터에서 대량의 상품을 관리하는 데 도움을 주고 있습니다. 지게차는 화물의 상하차 및 재고 이동 속도를 높여 당일 배송 및 빠른 배송 수요에 대응하는 데 중요한 역할을 하고 있습니다. E-Commerce 기업은 혁신적인 창고 관리 기술을 통합하여 업무 효율성을 향상시키는 첨단 전동 지게차 및 자율 지게차에 대한 의존도를 높이고 있습니다. 지게차의 유용성은 전 세계에서 분명하지만, 북미와 유럽에서 더욱 두드러지며, E-Commerce 기업이 더 빠른 배송을 약속하는 데 도움이 되고 있습니다.

세계의 지게차 시장에 대해 조사분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 제공하고 있습니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 중요 인사이트

미충족 요구와 화이트 스페이스

상호접속된 시장과 부문 횡단적인 기회

새로운 비즈니스 모델과 에코시스템의 변화

OEM과 Tier 1 공급업체에 의한 전략적 움직임

VC/사모펀드 투자 동향과 스타트업의 상황

지속가능성에 대한 영향과 규제 정책 구상

제5장 시장 개요

서론

시장 역학

촉진요인

억제요인

기회

과제

고객 비즈니스에 영향을 미치는 동향과 혼란

가격결정 분석

평균 판매 가격 동향 : 지역별

주요 제조업체가 제공하는 지게차의 평균 판매 가격

사례 연구 분석

에코시스템 분석

공급망 분석

무역 분석

수입 시나리오(HS 코드 8427)

수출 시나리오(HS 코드 8427)

주요 컨퍼런스와 이벤트

투자와 자금조달 시나리오

OEM 분석

배터리 용량과 리프팅 능력

리프팅 능력과 리프팅 전압

배터리 전압과 지게차 시장 규모

기존 지게차와 전동 지게차 ROI

부품 표

총소유 비용

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

AI/생성형 AI의 영향

규제 상황

규제기관, 정부기관, 기타 조직

국제기준

환경과 배출 규제

미국

유럽연합

중국

인도

장려책과 그린 펀딩 프로그램

주요 이해관계자와 구입 기준

제6장 지게차 시장 : 추진력별

서론

전기

ICE

연료전지

중요 인사이트

제7장 지게차 시장 : 톤수별

서론

5톤 미만

5-10톤

11-36톤

36톤 초과

중요 인사이트

제8장 지게차 시장 : 최종 용도 산업별

서론

서드파티 물류

식품 및 음료

자동차

E-Commerce

항공

펄프·제지

화학제품

의료

반도체·전자

금속·중기

기타

중요 인사이트

제9장 지게차 시장 : 클래스별

서론

클래스 1

클래스 2

클래스 3

클래스4/5

중요 인사이트

제10장 지게차 시장 : 조작별

서론

수동

자율형

중요 인사이트

제11장 지게차 시장 : 용도별

서론

실내

야외

실내·야외

중요 인사이트

제12장 전동 지게차 시장 : 배터리 유형별

서론

리튬이온

납축전지

중요 인사이트

제13장 전동 지게차 시장 : 리프팅 능력별

서론

2톤 미만

2-5톤

5톤 초과

중요 인사이트

제14장 지게차 시장 : 제품 유형별

서론

창고

카운터밸런스

중요 인사이트

제15장 지게차 시장 : 타이어 유형별

서론

쿠션

공압

중요 인사이트

제16장 지게차 시장 : 지역별

서론

아시아태평양

거시경제 전망

중국

인도

일본

한국

유럽

거시경제 전망

독일

영국

프랑스

이탈리아

스페인

러시아

튀르키예

동유럽

기타 유럽

북미

거시경제 전망

미국

멕시코

캐나다

기타 지역

거시경제 전망

아프리카

호주와 오세아니아

중요 인사이트

제17장 경쟁 구도

서론

주요 참여 기업의 전략/강점(2021-2025년)

시장 점유율 분석(2024년)

매출 분석(2021-2024년)

기업의 평가와 재무 지표

제품/브랜드의 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제18장 기업 개요

주요 기업

TOYOTA INDUSTRIES CORPORATION

KION GROUP AG

JUNGHEINRICH AG

MITSUBISHI LOGISNEXT CO., LTD.

CROWN EQUIPMENT CORPORATION

HYSTER-YALE MATERIALS HANDLING

CLARK MATERIAL HANDLING COMPANY

HYUNDAI CONSTRUCTION EQUIPMENT

KOMATSU LTD.

BOBCAT COMPANY

기타 기업

KALMAR

ANHUI HELI CO., LTD.

BYD COMPANY LTD.

GODREJ MATERIAL HANDLING

EP EQUIPMENT

LONKING

HANGCHA FORKLIFT

KONECRANES

COMBILIFT

VALLEE

FLEXI NARROW AISLE

MANITOU

HOIST MATERIAL HANDLING

AGILOX SERVICES GMBH

E80 GROUP S.P.A.

SCOTT AUTOMATION

BASTIAN SOLUTIONS

SEEGRID CORPORATION

VECNA ROBOTICS

MURATA MACHINERY, LTD.

제19장 제안

아시아태평양이 예측 기간에 지게차 시장을 선도한다.

E-Commerce가 지게차 제조업체에서의 중요한 초점이 된다.

결론

제20장 부록

KSA

영문 목차

영문목차

The forklift market is projected to grow from USD 91.19 billion in 2025 to USD 141.32 billion in 2032, at a CAGR of 6.5%. Forklifts are one of the most common intralogistics systems and are seen as efficient in handling materials for various applications. The compact size, heavy-weight carrying capacity, and versatility make forklifts the preferred choice in material handling operations. The Asia Pacific market is expected to grow and dominate the global forklift market over the forecast period. Major OEMs such as Toyota Industries Corporation, Kion Group, and Jungheinrich AG are driving a shift towards innovative electric and autonomous models that enhance productivity and efficiency.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2025

Forecast Period

2025-2032

Units Considered

Value, and Volume (Units)

Segments

by Propulsion, Tonnage Capacity, End-Use Industry, by Class, Operation, Application, Battery Type, Lifting Capacity, Tire, Product Type, Region

Regions covered

Asia Pacific, North America, Europe, Rest of the world

In addition, the emergence of artificial intelligence with real-time location monitoring and automated material handling capabilities in forklifts has revolutionized warehouse automation at the highest level, thereby encouraging global warehousing industry giants to increase the deployment of autonomous forklifts for optimized operations. Institutional entities like the U.S. National Institute for Occupational Safety and Health (NIOSH) and the Occupational Safety and Health Administration (OSHA) emphasize these advancements in the autonomous forklift market, noting that sensor-equipped forklifts can reduce workplace incidents by promoting safer navigation and load management.

"Electric forklifts are projected to remain dominant in the global market during the forecast period."

Electric forklifts represent the largest share of the global market. Classified as Class 1, Class 2, Class 3, and Class 2, these forklifts are electrically powered and account for over 70% of the market as of 2024. The demand for electric forklifts is on the rise due to the need to comply with strict emissions standards for industrial vehicles worldwide. Additionally, electric forklifts reduce ownership costs and offer a better return on investment (ROI) compared to internal combustion engine (ICE) forklifts.

The widespread adoption of lithium-ion batteries is another trend ensuring the dominance of electric forklifts. These lithium-ion batteries offer rapid charging, minimal maintenance, and a longer lifespan than traditional lead-acid types. For example, lithium iron phosphate (LFP) batteries are favored by most OEMs for their safety profile, long cycle life, and cost advantages, which make them attractive for multi-shift warehouse operations and cold storage environments. According to BloombergNEF, by December 2024, lithium-ion battery pack prices had fallen to a record low of USD 115 per kilowatt-hour, representing a 20% decline from 2023 and marking the largest annual drop since 2017. Thus, with advancements in battery technologies coupled with emerging stringent emission norms and demand for low-cost and efficient warehouse management, the demand for electric forklifts is expected to increase in the coming years.

"Forklift demand in the E-commerce industry is expected to grow at the fastest CAGR during the review period."

Forklifts are highly useful in the e-commerce industry as they enable faster and more efficient handling of goods, directly supporting the sector's growth. With consumer buying shifting from physical shops to digital platforms, forklifts help manage large volumes of goods in warehouses and distribution centers. They play a key role in meeting same-day or quick delivery demands by speeding up loading, unloading, and inventory movement. E-commerce players increasingly rely on advanced electric and autonomous forklifts, which integrate with innovative warehousing technologies to improve operational efficiency. Their usefulness is evident globally, though more pronounced in North America and Europe, where forklifts help e-commerce companies meet faster delivery commitments, often tied to premium services.

"Europe is estimated to be the second-largest forklift market during the forecast period."

By 2032, Europe is projected to be the second-biggest consumer market for forklifts worldwide. This can be attributed to stringent workplace safety guidelines, high labor costs, high real estate prices, which limit warehouse space, and the stringent European emission norms. Most of the forklift market in Europe falls in three countries, namely Germany, France, and the UK, which are experiencing high growth rates in e-commerce, retail, and manufacturing sectors.

In Europe, forklifts below 5 tons command the most significant and fastest-growing market share, reflecting the region's strong emphasis on space-efficient, high-throughput indoor material handling. By class, Class 3 (electric pedestrian trucks) and Class 2 (electric narrow aisle trucks) lead the market, driven by high demand in warehousing, retail, and automation-focused sectors across Germany, France, and the UK. The fastest-growing segment, however, is Class 1 (electric motor rider trucks), underpinned by rising e-commerce activity, accelerating automation investments, and stringent emission and safety standards that favor electric, ergonomic, and flexible forklift solutions for Europe's modern logistics environments. To conclude, Europe is leading the warehouse automation and material handling market due to high labor costs, limited space, and strict safety standards. Further, the surging pharma and chemicals industries are likely to continue boosting the forklift market in the European region.

The break-up of the profile of primary participants in the forklift market:

By Company Type: Forklift OEMs - 80%, Others - 20%

By Designation: C Level - 60%, Director-level - 30%, Others - 10%

By Region: North America- 25%, Europe - 30%, Asia Pacific - 40%, Rest of the World-5%

Mitsubishi Logisnext Co., Ltd. (Japan) is the leading manufacturer of forklifts in the global market. The other key companies include Toyota Industries Corporation (Japan), KION Group AG (Germany), Jungheinrich AG (Germany), and Crown Equipment Corporation (US).

Research Coverage:

The study segments the forklift market and forecasts the market size based on Tonnage Capacity (below 5 tons, 5-10 tons, 11-36 tons, and above 36 tons), Application (indoor, outdoor, and indoor and outdoor), Class (Class 1, Class 2, Class 3 (Class 31, Class 32), and Class 4/5), Industry (3PL, food & beverage, automotive, pulp & paper, metals & heavy machinery, e-commerce, aviation, semiconductors & electronics, chemical, healthcare, and others), Propulsion (electric and ICE), Operation (manual and autonomous), Product Type (warehouse and counterbalance), by Battery Type (lithium-ion and lead-acid), Tire Type (cushion and pneumatic) and Region (Asia Pacific, Europe, North America, and Rest of the World).

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall forklift market and the subsegments. The report includes a comprehensive market share analysis, supply chain analysis, extensive lists and insights into component manufacturers, chapter segmentation based on materials, a thorough supply chain analysis, and a competitive landscape. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Rising GHG emissions, government incentives and policies, overall targets to reduce fleet-level emissions and increasing demand for emission-free vehicles), restraints (safety concerns in EV batteries and high development cost), opportunities (transition towards hydrogen fuel cell electric mobility), and challenges (high cost of developing charging infrastructure) that are influencing the growth of the forklift market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the forklift market

Market Development: Comprehensive information about lucrative markets - the report analyzes the forklift market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the forklift market

Deep dive segments on the electric forklift market and their trends

OEM analysis for electric forklifts

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the forklift market, such as Toyota Industries Corporation (Japan), KION Group AG (Germany), Jungheinrich AG (Germany), Crown Equipment Corporation (US), and Mitsubishi Logisnext Co. Ltd. (Japan)

The report also helps stakeholders understand the pulse of the forklift market by providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary interview participants

2.1.2.2 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 UNMET NEEDS AND WHITE SPACES

4.1.1 UNMET NEEDS

4.1.2 WHITE SPACES

4.2 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.2.1 INTERCONNECTED MARKETS

4.2.2 CROSS-SECTOR OPPORTUNITIES

4.3 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

4.3.1 EMERGING BUSINESS MODELS

4.3.2 ECOSYSTEM SHIFTS

4.4 STRATEGIC MOVES BY OEMS AND TIER-1 SUPPLIERS

4.5 VC/PRIVATE EQUITY INVESTMENT TRENDS AND START-UP LANDSCAPE

4.5.1 INVESTMENT TRENDS

4.5.2 START-UP LANDSCAPE

4.6 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rapid growth in e-commerce and warehousing industries

5.2.1.2 Government incentives and regulations promoting growth of electric forklifts

5.2.1.3 Automation and fleet integration

5.2.2 RESTRAINTS

5.2.2.1 Expansion of third-party logistics services

5.2.2.2 Elevated demand for stacker cranes

5.2.3 OPPORTUNITIES

5.2.3.1 Evolution of refurbished and rental forklifts

5.2.3.2 Modular solutions to optimize customer productivity

5.2.3.3 Integration of AI, IoT, and predictive analytics for fleet optimization

5.2.4 CHALLENGES

5.2.4.1 High initial cost of electric forklifts

5.2.4.2 Substantial integration and technology cost of autonomous forklifts

5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE TREND, BY REGION

5.4.2 AVERAGE SELLING PRICE OF FORKLIFTS OFFERED BY KEY PLAYERS

5.4.2.1 Linde

5.4.2.2 Hangcha

5.4.2.3 Manitou

5.4.2.4 Komatsu

5.4.2.5 CLARK

5.5 CASE STUDY ANALYSIS

5.5.1 MITSUBISHI FORKLIFTS SUPPLIED ELECTRIC COUNTERBALANCE TRUCKS TO KELLOGG'S MANCHESTER SITE

5.5.2 TOYOTA DELIVERED SUSTAINABLE AGV SOLUTIONS FOR PANASONIC ENERGY

5.5.3 L'OREAL INSTALLED DEMATIC'S AUTONOMOUS FORKLIFTS TO REDUCE DELIVERY TIME

5.5.4 AER MANUFACTURING REPLACED AGING AUTONOMOUS FLOOR-TO-FLOOR MATERIAL HANDLING SYSTEMS WITH DEMATIC'S COMPACT AUTONOMOUS TUGGERS

5.5.5 MITSUBISHI FORKLIFTS SUPPLIED ELECTRIC FORKLIFTS TO CWT COMMODITIES

5.6 ECOSYSTEM ANALYSIS

5.7 SUPPLY CHAIN ANALYSIS

5.8 TRADE ANALYSIS

5.8.1 IMPORT SCENARIO (HS CODE 8427)

5.8.2 EXPORT SCENARIO (HS CODE 8427)

5.9 KEY CONFERENCES AND EVENTS

5.10 INVESTMENT AND FUNDING SCENARIO

5.11 OEM ANALYSIS

5.11.1 BATTERY CAPACITY VS. LIFTING CAPACITY

5.11.2 LIFTING CAPACITY VS. LIFTING VOLTAGE

5.11.3 BATTERY VOLTAGE VS. MARKET SIZE OF FORKLIFTS

5.12 ROI OF CONVENTIONAL VS. ELECTRIC FORKLIFTS

5.13 BILL OF MATERIALS

5.14 TOTAL COST OF OWNERSHIP

5.15 TECHNOLOGY ANALYSIS

5.15.1 KEY TECHNOLOGIES

5.15.1.1 Autonomous forklifts

5.15.1.2 Electric powertrains

5.15.1.3 Internet of Things

5.15.2 COMPLEMENTARY TECHNOLOGIES

5.15.2.1 Industry 4.0

5.15.2.2 Hydrogen fuel cells

5.15.3 ADJACENT TECHNOLOGIES

5.15.3.1 5G connectivity

5.15.3.2 Solid-state batteries

5.16 PATENT ANALYSIS

5.17 IMPACT OF AI/GEN AI

5.18 REGULATORY LANDSCAPE

5.18.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.18.2 INTERNATIONAL STANDARDS

5.18.3 ENVIRONMENTAL AND EMISSION REGULATIONS

5.18.4 US

5.18.5 EUROPEAN UNION

5.18.6 CHINA

5.18.7 INDIA

5.18.8 INCENTIVES AND GREENFUNDING PROGRAMS

5.19 KEY STAKEHOLDERS AND BUYING CRITERIA

5.19.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.19.2 BUYING CRITERIA

6 FORKLIFT MARKET, BY PROPULSION

6.1 INTRODUCTION

6.2 ELECTRIC

6.2.1 EMPHASIS ON ENVIRONMENTAL SUSTAINABILITY TO DRIVE MARKET

6.3 ICE

6.3.1 ABILITY TO WITHSTAND HARSH WEATHER CONDITIONS TO DRIVE MARKET

6.3.2 GASOLINE

6.3.3 DIESEL

6.3.4 ALTERNATE FUEL

6.4 FUEL CELL

6.5 PRIMARY INSIGHTS

7 FORKLIFT MARKET, BY TONNAGE CAPACITY

7.1 INTRODUCTION

7.2 <5 TONS

7.2.1 NEED FOR OPERATIONAL FLEXIBILITY IN COMPACT WAREHOUSES TO DRIVE MARKET

7.3 5-10 TONS

7.3.1 RISE OF ELECTRIC INFRASTRUCTURE TO DRIVE MARKET

7.4 11-36 TONS

7.4.1 LARGE-SCALE ADOPTION IN LOGISTICS AND FREIGHT INDUSTRIES TO DRIVE MARKET

7.5 >36 TONS

7.5.1 EXTENSIVE USE IN HANDLING EXTREMELY HEAVY MATERIALS TO DRIVE MARKET

7.6 PRIMARY INSIGHTS

8 FORKLIFT MARKET, BY END-USE INDUSTRY

8.1 INTRODUCTION

8.2 THIRD-PARTY LOGISTICS

8.2.1 INCREASED ADOPTION OF FORKLIFTS DUE TO FAST LOADING, TRANSPORTATION, AND UNLOADING OPERATIONS TO DRIVE MARKET

8.3 FOOD & BEVERAGES

8.3.1 PRESSURE ON MANUFACTURERS TO REDUCE OPERATIONAL COSTS TO DRIVE MARKET

8.4 AUTOMOTIVE

8.4.1 NEED FOR EFFICIENT INVENTORY MANAGEMENT TO DRIVE MARKET

8.5 E-COMMERCE

8.5.1 RISING DEMAND FOR SHORTER DELIVERY TIMES TO DRIVE MARKET

8.6 AVIATION

8.6.1 INCORPORATION OF FORKLIFTS IN MANUFACTURING AND ASSEMBLY OPERATIONS TO DRIVE MARKET

8.7 PULP & PAPER

8.7.1 SUBSTANTIAL INVESTMENTS IN AUTONOMOUS FORKLIFT SOLUTIONS TO DRIVE MARKET

8.8 CHEMICALS

8.8.1 FOCUS ON ENSURING WORKPLACE SAFETY AND MANAGING WORKFLOW EFFECTIVELY TO DRIVE MARKET

8.9 HEALTHCARE

8.9.1 STRICT REGULATORY REQUIREMENTS FOR PRODUCTION, STORAGE, AND DISTRIBUTION OF DRUGS TO DRIVE MARKET

8.10 SEMICONDUCTORS & ELECTRONICS

8.10.1 MANUFACTURERS' EMPHASIS ON ENHANCING INTRALOGISTICS OPERATIONS TO DRIVE MARKET

8.11 METALS & HEAVY MACHINERY

8.11.1 RISE IN INFRASTRUCTURAL DEVELOPMENT TO DRIVE MARKET

8.12 OTHERS

8.13 PRIMARY INSIGHTS

9 FORKLIFT MARKET, BY CLASS

9.1 INTRODUCTION

9.2 CLASS 1

9.2.1 PREDOMINANCE IN ASIA PACIFIC REGION TO DRIVE MARKET

9.3 CLASS 2

9.3.1 LIMITED MARKET DUE TO AVAILABILITY OF MORE VERSATILE OPTIONS

9.4 CLASS 3

9.4.1 SUSTAINABILITY TARGETS FOR ZERO-EMISSION EQUIPMENT TO DRIVE MARKET

9.4.2 CLASS 31

9.4.3 CLASS 32

9.4.4 CLASS 31 VS. CLASS 32 FORKLIFTS

9.5 CLASS 4/5

9.5.1 RELIABILITY OF INTERNAL COMBUSTION ENGINES TO DRIVE MARKET

9.6 PRIMARY INSIGHTS

10 FORKLIFT MARKET, BY OPERATION

10.1 INTRODUCTION

10.2 MANUAL

10.2.1 LOW INITIAL COST AND EASE OF INTEGRATION TO DRIVE MARKET

10.3 AUTONOMOUS

10.3.1 RAPID FORKLIFT DEVELOPMENT TO INCREASE WORKPLACE PRODUCTIVITY TO DRIVE MARKET

10.4 PRIMARY INSIGHTS

11 FORKLIFT MARKET, BY APPLICATION

11.1 INTRODUCTION

11.2 INDOOR

11.2.1 RAPIDLY EXPANDING E-COMMERCE AND LOGISTICS INDUSTRIES TO DRIVE MARKET

11.3 OUTDOOR

11.3.1 SIGNIFICANT PRESENCE OF CONSTRUCTION, MINING, AND MARINE FREIGHT INDUSTRIES IN NORTH AMERICA TO DRIVE MARKET

11.4 INDOOR & OUTDOOR

11.4.1 RISING NEED FOR DUAL-USE FORKLIFTS TO DRIVE MARKET

11.5 PRIMARY INSIGHTS

12 ELECTRIC FORKLIFT MARKET, BY BATTERY TYPE

12.1 INTRODUCTION

12.2 LITHIUM-ION

12.2.1 HIGH ENERGY DENSITY AND LONGER BATTERY LIFE THAN OTHER BATTERIES TO DRIVE MARKET

12.2.2 LITHIUM IRON PHOSPHATE

12.2.3 NICKEL MANGANESE COBALT

12.2.4 OTHERS

12.3 LEAD ACID

12.3.1 LARGE CURRENT CAPABILITY AND LOW MANUFACTURING COST TO DRIVE MARKET

12.4 PRIMARY INSIGHTS

13 ELECTRIC FORKLIFT MARKET, BY LIFTING CAPACITY

13.1 INTRODUCTION

13.2 <2 TONS

13.2.1 WIDE RANGE OF APPLICATIONS IN VARIOUS INDUSTRIES TO DRIVE MARKET

13.3 2-5 TONS

13.3.1 ADVANCEMENTS IN BATTERY TECHNOLOGY TO DRIVE MARKET

13.4 >5 TONS

13.4.1 INCREASED PREFERENCE FOR SUSTAINABLE FORKLIFTS WITH MORE LIFTING CAPACITY TO DRIVE MARKET

13.5 PRIMARY INSIGHTS

14 FORKLIFT MARKET, BY PRODUCT TYPE

14.1 INTRODUCTION

14.2 WAREHOUSE

14.2.1 ABILITY TO MANEUVER IN NARROW SPACES TO DRIVE MARKET

14.3 COUNTERBALANCE

14.3.1 NEED FOR STABLE HEAVY MATERIAL HANDLING OPERATIONS TO DRIVE MARKET

14.4 PRIMARY INSIGHTS

15 FORKLIFT MARKET, BY TIRE TYPE

15.1 INTRODUCTION

15.2 CUSHION

15.2.1 RISING DEMAND FOR LIFTING PACKETS IN WAREHOUSING AND MANUFACTURING INDUSTRIES TO DRIVE MARKET

15.3 PNEUMATIC

15.3.1 EXTENSIVE USE IN LIFTING HEAVY GOODS AND CARRIAGES TO DRIVE MARKET

15.4 PRIMARY INSIGHTS

16 FORKLIFT MARKET, BY REGION

16.1 INTRODUCTION

16.2 ASIA PACIFIC

16.2.1 MACROECONOMIC OUTLOOK

16.2.2 CHINA

16.2.2.1 Growing demand for automation across industries to drive market

16.2.3 INDIA

16.2.3.1 Booming automobile and e-commerce industries to drive market

16.2.4 JAPAN

16.2.4.1 Lack of proper warehousing facilities to drive market

16.2.5 SOUTH KOREA

16.2.5.1 Demand for increased efficiency to drive market

16.3 EUROPE

16.3.1 MACROECONOMIC OUTLOOK

16.3.2 GERMANY

16.3.2.1 Robust logistics industry to drive market

16.3.3 UK

16.3.3.1 Need for efficient material handling solutions in automotive industry to drive market

16.3.4 FRANCE

16.3.4.1 Rapid expansion of online retail to drive market

16.3.5 ITALY

16.3.5.1 Advancements in domestic e-commerce industry to drive market

16.3.6 SPAIN

16.3.6.1 Strategic location for logistics and warehousing to drive market

16.3.7 RUSSIA

16.3.7.1 Steady growth in diverse industries to drive market

16.3.8 TURKEY

16.3.8.1 Rising internet penetration and expanding mobile commerce to drive market

16.3.9 EASTERN EUROPE

16.3.10 REST OF EUROPE

16.4 NORTH AMERICA

16.4.1 MACROECONOMIC OUTLOOK

16.4.2 US

16.4.2.1 Inclination toward automation to drive market

16.4.3 MEXICO

16.4.3.1 Growth of foreign manufacturing units to drive market

16.4.4 CANADA

16.4.4.1 Robust export infrastructure to drive market

16.5 REST OF THE WORLD

16.5.1 MACROECONOMIC OUTLOOK

16.5.2 AFRICA

16.5.2.1 Expansion of warehouses due to growing export activities to drive market

16.5.3 AUSTRALIA & OCEANIA

16.5.3.1 Growing industrial activities to drive market

16.6 PRIMARY INSIGHTS

17 COMPETITIVE LANDSCAPE

17.1 INTRODUCTION

17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

17.3 MARKET SHARE ANALYSIS, 2024

17.4 REVENUE ANALYSIS, 2021-2024

17.5 COMPANY VALUATION AND FINANCIAL METRICS

17.6 PRODUCT/BRAND COMPARISON

17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

17.7.1 STARS

17.7.2 EMERGING LEADERS

17.7.3 PERVASIVE PLAYERS

17.7.4 PARTICIPANTS

17.7.5 COMPANY FOOTPRINT

17.7.5.1 Company footprint

17.7.5.2 Region footprint

17.7.5.3 Propulsion footprint

17.7.5.4 Operation footprint

17.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

17.8.1 PROGRESSIVE COMPANIES

17.8.2 RESPONSIVE COMPANIES

17.8.3 DYNAMIC COMPANIES

17.8.4 STARTING BLOCKS

17.8.5 COMPETITIVE BENCHMARKING

17.8.5.1 List of start-ups/SMEs

17.8.5.2 Competitive benchmarking of start-ups/SMEs

17.9 COMPETITIVE SCENARIO

17.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

17.9.2 DEALS

17.9.3 EXPANSIONS

18 COMPANY PROFILES

18.1 KEY PLAYERS

18.1.1 TOYOTA INDUSTRIES CORPORATION

18.1.1.1 Business overview

18.1.1.2 Products offered

18.1.1.3 Recent developments

18.1.1.3.1 Product launches/developments

18.1.1.3.2 Deals

18.1.1.3.3 Expansions

18.1.1.3.4 Other developments

18.1.1.4 MnM view

18.1.1.4.1 Key strengths

18.1.1.4.2 Strategic choices

18.1.1.4.3 Weaknesses and competitive threats

18.1.2 KION GROUP AG

18.1.2.1 Business overview

18.1.2.2 Products offered

18.1.2.3 Recent developments

18.1.2.3.1 Product launches/developments

18.1.2.3.2 Deals

18.1.2.3.3 Expansions

18.1.2.4 MnM view

18.1.2.4.1 Key strengths

18.1.2.4.2 Strategic choices

18.1.2.4.3 Weaknesses and competitive threats

18.1.3 JUNGHEINRICH AG

18.1.3.1 Business overview

18.1.3.2 Products offered

18.1.3.3 Recent developments

18.1.3.3.1 Product launches/developments

18.1.3.3.2 Deals

18.1.3.3.3 Expansions

18.1.3.3.4 Other developments

18.1.3.4 MnM view

18.1.3.4.1 Key strengths

18.1.3.4.2 Strategic choices

18.1.3.4.3 Weaknesses and competitive threats

18.1.4 MITSUBISHI LOGISNEXT CO., LTD.

18.1.4.1 Business overview

18.1.4.2 Products offered

18.1.4.3 Recent developments

18.1.4.3.1 Product launches/developments

18.1.4.3.2 Expansions

18.1.4.3.3 Other developments

18.1.4.4 MnM view

18.1.4.4.1 Key strengths

18.1.4.4.2 Strategic choices

18.1.4.4.3 Weaknesses and competitive threats

18.1.5 CROWN EQUIPMENT CORPORATION

18.1.5.1 Business overview

18.1.5.2 Products offered

18.1.5.3 Recent developments

18.1.5.3.1 Product launches/developments

18.1.5.3.2 Expansions

18.1.5.3.3 Other developments

18.1.5.4 MnM view

18.1.5.4.1 Key strengths

18.1.5.4.2 Strategic choices

18.1.5.4.3 Weaknesses and competitive threats

18.1.6 HYSTER-YALE MATERIALS HANDLING

18.1.6.1 Business overview

18.1.6.2 Products offered

18.1.6.3 Recent developments

18.1.6.3.1 Product launches/developments

18.1.6.3.2 Deals

18.1.6.3.3 Other developments

18.1.7 CLARK MATERIAL HANDLING COMPANY

18.1.7.1 Business overview

18.1.7.2 Products offered

18.1.7.3 Recent developments

18.1.7.3.1 Product launches/developments

18.1.7.3.2 Deals

18.1.7.3.3 Other developments

18.1.8 HYUNDAI CONSTRUCTION EQUIPMENT

18.1.8.1 Business overview

18.1.8.2 Products offered

18.1.8.3 Recent developments

18.1.8.3.1 Product launches/developments

18.1.8.3.2 Deals

18.1.8.3.3 Other developments

18.1.9 KOMATSU LTD.

18.1.9.1 Business overview

18.1.9.2 Products offered

18.1.9.3 Recent developments

18.1.9.3.1 Product launches/developments

18.1.9.3.2 Deals

18.1.10 BOBCAT COMPANY

18.1.10.1 Business overview

18.1.10.2 Products offered

18.1.10.3 Recent developments

18.1.10.3.1 Product launches/developments

18.1.10.3.2 Other developments

18.2 OTHER PLAYERS

18.2.1 KALMAR

18.2.2 ANHUI HELI CO., LTD.

18.2.3 BYD COMPANY LTD.

18.2.4 GODREJ MATERIAL HANDLING

18.2.5 EP EQUIPMENT

18.2.6 LONKING

18.2.7 HANGCHA FORKLIFT

18.2.8 KONECRANES

18.2.9 COMBILIFT

18.2.10 VALLEE

18.2.11 FLEXI NARROW AISLE

18.2.12 MANITOU

18.2.13 HOIST MATERIAL HANDLING

18.2.14 AGILOX SERVICES GMBH

18.2.15 E80 GROUP S.P.A.

18.2.16 SCOTT AUTOMATION

18.2.17 BASTIAN SOLUTIONS

18.2.18 SEEGRID CORPORATION

18.2.19 VECNA ROBOTICS

18.2.20 MURATA MACHINERY, LTD.

19 RECOMMENDATIONS

19.1 ASIA PACIFIC TO BE LEADING MARKET FOR FORKLIFTS DURING FORECAST PERIOD

19.2 E-COMMERCE TO BE KEY FOCUS FOR FORKLIFT MANUFACTURERS