Flexible Packaging Market By Material, Packaging Type, Printing Technology, Application, Region - Global Forecast to 2030

상품코드:1863603

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 450 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

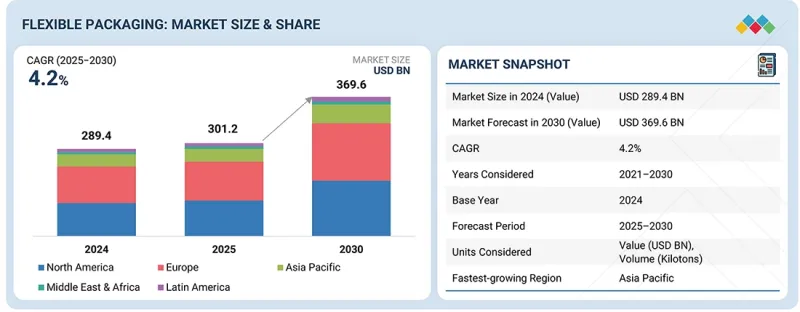

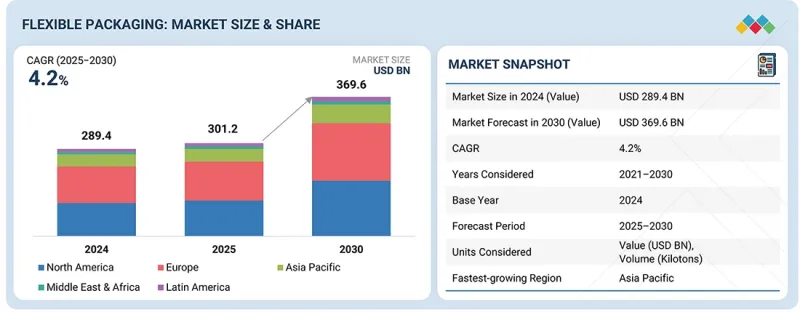

연포장 시장 규모는 예측 기간 중 CAGR 4.2%로 성장하며, 2025년 3,012억 달러에서 2030년까지 3,696억 달러에 달할 것으로 전망되고 있습니다.

제품의 보호성 향상, 유통기한 연장, 운송비용 절감의 필요성으로 인해 연포장에 대한 수요가 증가하고 있습니다.

조사 범위

조사 대상 기간

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

대상 단위

금액(100만 달러), 킬로톤

부문

소재별, 포장 유형별, 인쇄 기술별, 용도별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미

제조업체와 브랜드는 유연한 포맷을 채택하고 있습니다. 그 이유는 업무 효율성 향상, 소량 생산의 실현, 그리고 소비자의 시선을 사로잡는 혁신적이고 매력적인 디자인의 실현이 가능하기 때문입니다. 포장 폐기물을 줄이기 위한 규제 강화와 순환 경제로의 전환도 식품, 음료, 의료, 퍼스널케어 등의 산업에서 유연성, 고차폐성, 친환경 소재의 사용을 촉진하고 있습니다.

예측 기간 중 종이 부문은 연포장 시장에서 두 번째로 큰 규모를 유지할 것으로 예측됩니다. 이러한 성장은 브랜드와 규제 당국이 플라스틱 폐기물 감소에 초점을 맞추고 있는 가운데, 지속가능하고 재활용이 가능하며 친환경적인 포장 솔루션에 대한 수요가 증가함에 따라 성장세를 보이고 있습니다. 코팅지, 라미네이트지, 고배리어지 기술의 발전으로 내구성, 내습성, 제품 보호성이 향상되어 식품, 음료, 퍼스널케어, 의약품 용도에 적합한 소재가 되었습니다. 친환경 포장에 대한 소비자의 선호도가 높아지면서 이 분야는 전 세계에서 더욱 확대되고 있습니다.

예측 기간 중, 가방 부문은 연포장 시장에서 두 번째로 큰 규모를 차지할 것으로 예측됩니다. 식품, 음료, 퍼스널케어, 산업 분야에서의 다용도성, 내구성, 비용 효율성이 성장의 원동력이 되고 있습니다. 가방은 편리한 보관성, 휴대성, 장기 보존성을 제공하므로 소매 포장 및 대량 포장에 적합합니다. 맞춤형, 경량, 지속가능한 소재에 대한 수요 증가와 현대 소매업 및 E-Commerce의 성장은 이 부문의 세계 확장을 더욱 촉진하고 있습니다.

예측 기간 중 로토그라비어 인쇄 부문은 연포장 시장에서 두 번째로 큰 규모를 차지할 것으로 예측됩니다. 특히 고급 식품, 음료 및 퍼스널케어 제품에서 연포장에 대한 고품질의 일관되고 상세한 인쇄에 대한 수요가 증가함에 따라 성장세를 보이고 있습니다. 로토그라비어 인쇄는 뛰어난 발색성, 복잡한 디자인 표현, 효율적인 대량 생산을 실현합니다. 시각적 매력에 대한 브랜드 중요성 증가와 신흥 시장에서의 채택 확대는 시각적으로 매력적인 맞춤형 포장 솔루션의 부상과 함께 이 부문의 꾸준한 성장세를 지원하고 있습니다.

예측 기간 중 퍼스널케어 및 화장품 부문은 연포장 시장에서 두 번째로 큰 규모를 유지할 것으로 예측됩니다. 성장의 원동력은 브랜드 차별화를 강화하는 휴대성이 뛰어나고 가볍고 시각적으로 매력적인 포장에 대한 수요 증가입니다. 지속가능하고 재활용이 가능하며 리필 가능한 포장에 대한 소비자의 선호도가 높아지면서 리필 포장의 채택이 더욱 가속화되고 있습니다. 유연한 파우치, 향 주머니, 튜브는 편리함을 제공하고, 제품을 보호하고, 보관 기간을 연장합니다. 빠른 제품 혁신, E-Commerce 확대, 신흥 시장에서의 스킨케어 및 미용 소비 증가도 이 부문의 견고한 성장을 주도하고 있습니다.

아시아태평양은 급속한 도시화, 가처분 소득 증가, 포장 식품, 음료, 퍼스널케어 제품에 대한 수요 증가를 배경으로 연포장의 가장 큰 시장입니다. 중국, 인도, 동남아시아 국가들의 산업 및 제조업의 견고한 성장과 더불어 E-Commerce의 확대와 현대식 소매업의 보급이 이 지역 수요를 촉진하고 있습니다. 지속가능하고 재활용 가능한 포장에 대한 관심이 높아지고, 세계 및 현지 제조업체들의 생산 능력 확대를 위한 투자로 인해 아시아태평양은 세계 연포장의 주요 성장 거점으로 자리매김하고 있습니다.

본 조사에서는 연포장 시장의 주요 기업에 대해 기업 개요, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 실시했습니다.

조사 범위

본 조사 보고서는 연포장 시장을 소재별, 포장 유형별, 인쇄 기술별, 용도별, 지역별, 지역별로 분류하여 조사했습니다. 이 보고서의 조사 범위에는 연포장 시장의 성장에 영향을 미치는 촉진요인, 시장 성장 저해요인, 과제, 성장 기회에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 진입업체에 대한 종합적인 분석을 통해 사업 개요, 제품 및 연포장 시장과 관련된 제휴, 합병, 제품 출시, 사업 확장, 인수 등 주요 전략에 대한 인사이트를 제공합니다. 또한 유연한 포장 생태계의 신흥 스타트업 기업의 경쟁 분석도 특징적으로 다루고 있습니다.

이 보고서 구매의 장점

이 보고서는 시장 선도기업과 신규 진출기업에게 전체 연포장 시장과 그 하위 부문의 매출 예측치를 제공합니다. 이해관계자들이 경쟁 구도를 이해하고, 자사의 포지셔닝에 대한 인사이트를 높이고, 효과적인 시장 진출 전략을 수립하는 데 도움이 될 것입니다. 또한 주요 시장 성장 촉진요인, 시장 성장 억제요인, 과제, 기회에 대한 정보를 제공함으로써 시장 동향을 파악하는 데 도움이 될 것입니다.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

서론

시장 역학

미충족 요구와 공백

상호접속된 시장과 분야 횡단적인 기회

Tier1/2/3참여 기업의 전략적 움직임

제5장 업계 동향

Porter's Five Forces 분석

주요 이해관계자와 구매 평가 기준

채택 장벽과 내부 과제

다양한 최종 용도 산업으로부터의 미충족 요구

시장 수익성

거시경제 분석

밸류체인 분석

에코시스템 분석

가격 분석

무역 분석

2025-2026년의 주요 컨퍼런스와 이벤트

고객 비즈니스에 영향을 미치는 동향/혼란

투자와 자금조달 시나리오

사례 연구 분석/실세계에 대한 응용

2025년 미국 관세가 연포장 시장에 미치는 영향

제6장 기술, 특허, 디지털, AI의 도입별 전략적 파괴

주요 기술

보완적 기술

인접 기술

기술/제품 로드맵

특허 분석

향후 응용

AI/생성형 AI가 연포장 시장에 미치는 영향

성공 사례와 실세계에 대한 응용

제7장 지속가능성과 규제 상황

지역의 규제와 컴플라이언스

지속가능성 구상

지속가능성에 대한 영향과 규제 정책 구상

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

제9장 연포장 시장(소재별)

서론

종이

플라스틱

금속

제10장 연포장 시장(포장 유형별)

서론

파우치

백

롤스톡

필름·랩

기타

제11장 연포장 시장(인쇄 기술별)

서론

플렉소 인쇄

그라비어 인쇄

디지털 인쇄

기타

제12장 연포장 시장(용도별)

서론

식품

음료

의약품·헬스케어

퍼스널케어·화장품

기타

제13장 연포장 시장(지역별)

서론

북미

미국

캐나다

멕시코

아시아태평양

중국

인도

일본

한국

기타

유럽

독일

영국

프랑스

러시아

스페인

이탈리아

기타

남미

브라질

아르헨티나

칠레

기타

중동 및 아프리카

GCC 국가

사우디아라비아

아랍에미리트

기타 GCC 국가

남아프리카공화국

기타

제14장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석

시장 점유율 분석

기업 평가와 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 참여 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 벤치마킹 : 스타트업/중소기업, 2024년

경쟁 시나리오

제15장 기업 개요

주요 참여 기업

AMCOR PLC

SMURFIT WESTROCK

MONDI

TOPPAN HOLDINGS INC.

SEALED AIR

HUHTAMAKI

CONSTANTIA FLEXIBLES

TRANSCONTINENTAL INC.

UFLEX LIMITED

BISCHOF+KLEIN SE & CO. KG

기타 기업

PROAMPAC

NOVOLEX

SILAFRICA

PPC FLEX COMPANY, INC.

PRINTPACK

NOVUS HOLDINGS LTD.

AHLSTROM

WIHURI GROUP

C-P FLEXIBLE PACKAGING

COSMO FILMS

GUALA PACK S.P.A.

EPAC HOLDINGS, LLC.

제16장 조사 방법

제17장 인접 시장과 관련 시장

제18장 부록

KSA

영문 목차

영문목차

The flexible packaging market is expected to grow from USD 301.2 billion in 2025 to USD 369.6 billion by 2030, at a CAGR of 4.2% during the forecast period. The demand for flexible packaging is rising due to the need for better product protection, longer shelf life, and lower transportation costs.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Kiloton)

Segments

Material, Packaging Type, Printing Technology, Application, and Region

Regions covered

North America, Asia Pacific, Europe, Middle East & Africa, and South America

Manufacturers and brands are adopting flexible formats because they can improve operational efficiency, allow for smaller batch production, and support innovative, eye-catching designs that attract consumers. Increasing regulatory focus on reducing packaging waste and the shift toward circular economy practices are also promoting the use of flexible, high-barrier, and eco-friendly materials across industries like food, beverages, healthcare, and personal care.

"Paper segment predicted to be the second-largest market during the forecast period"

The paper segment is expected to be the second-largest in the flexible packaging market during the forecast period. Its growth is driven by rising demand for sustainable, recyclable, and eco-friendly packaging solutions as brands and regulators focus on reducing plastic waste. Advances in coated, laminated, and high-barrier paper technologies improve durability, moisture resistance, and product protection, making paper suitable for food, beverages, personal care, and pharmaceutical uses. Growing consumer preference for environmentally responsible packaging further supports the segment's global expansion.

"The bags segment is projected to be the second-largest segment during the forecast period"

The bags segment is expected to be the second-largest in the flexible packaging market during the forecast period. Growth is fueled by their versatility, durability, and cost-effectiveness across food, beverage, personal care, and industrial sectors. Bags provide convenient storage, portability, and extended shelf life, making them perfect for retail and bulk packaging. The rising demand for customizable, lightweight, and sustainable materials, along with the growth of modern retail and e-commerce, further drives the segment's global expansion.

"Rotogravure segment predicted to be the second largest market during forecast period"

The rotogravure segment is expected to be the second-largest in the flexible packaging market during the forecast period. Its growth is driven by the demand for high-quality, consistent, and detailed printing on flexible packaging, especially for premium food, beverage, and personal care products. Rotogravure offers superior color reproduction, complex designs, and efficient large-scale production. Increasing brand focus on visual appeal, along with growing adoption in emerging markets, supports the segment's steady growth alongside the rise of customized and visually attractive packaging solutions.

"The personal care & cosmetics segment market is projected to be the second largest market during the forecast period."

The personal care & cosmetics segment is expected to be the second-largest in the flexible packaging market during the forecast period. Growth is fueled by increasing demand for travel-friendly, lightweight, and visually appealing packaging that enhances brand differentiation. Growing consumer preference for sustainable, recyclable, and refillable packaging further encourages adoption. Flexible pouches, sachets, and tubes provide convenience, protect products, and extend shelf life. Rapid product innovation, expansion of e-commerce, and rising skincare and beauty consumption in emerging markets also drive the segment's strong growth.

"In terms of value, the Asia Pacific flexible packaging market is projected to grow at the highest CAGR during the forecast period."

Asia Pacific is the largest market for flexible packaging, driven by rapid urbanization, rising disposable incomes, and growing demand for packaged food, beverages, and personal care products. Strong industrial and manufacturing growth in countries like China, India, and Southeast Asia, along with expanding e-commerce and modern retail penetration, boosts regional demand. An increasing focus on sustainable and recyclable packaging, along with investments by global and local manufacturers to expand production capacities, further strengthens Asia Pacific's dominance, making it the key growth hub for flexible packaging worldwide.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Amcor plc (Switzerland), Smurfit Westrock (Ireland), Mondi (UK), TOPPAN Holdings Inc. (Japan), Sealed Air (US), Huhtamaki (Finland), Constantia Flexibles (Austria), Transcontinental Inc. (Canada), Bischof+Klein SE & CO. KG (Germany), and UFlex Limited (India), among others are covered in the report.

The study includes an in-depth competitive analysis of these key players in the flexible packaging market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the flexible packaging market based on material (plastic, paper, metal), packaging type (pouches, bags, rollstock, films & wraps, other packaging types), printing technologies (flexography, rotogravure, digital), application (food, beverages, pharmaceutical & healthcare, personal care & cosmetics), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities affecting the growth of the flexible packaging market. A comprehensive analysis of the key industry players has been conducted to provide insights into their business overview, products offered, and key strategies such as partnerships, mergers, product launches, expansions, and acquisitions related to the flexible packaging market. This report also features a competitive analysis of emerging startups in the flexible packaging ecosystem.

Reasons to Buy the Report

The report will provide market leaders and new entrants with estimates of the revenue figures for the overall flexible packaging market and its subsegments. This report will assist stakeholders in understanding the competitive landscape, gaining better insights into positioning their businesses, and developing effective go-to-market strategies. Additionally, it will help stakeholders grasp the market's pulse by offering information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (growth of e-commerce platform, and rising demand for disposable packaging from end-use industries), restraints (non-availability of efficient recycling infrastructure, and surge in raw material price), opportunities (commercialization of mono-material high-barrier films, expansion of refill, reuse, and concentrate-compatible formats), and challenges (high dependence on petrochemical-based resins, rapidly evolving sustainability standards and certification requirements)

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the flexible packaging market

Market Development: Comprehensive information about profitable markets - the report analyzes the flexible packaging market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the flexible packaging market

Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players such as Amcor plc (Switzerland), Smurfit Westrock (Ireland), Mondi (UK), TOPPAN Holdings Inc. (Japan), Sealed Air (US), Huhtamaki (Finland), Constantia Flexibles (Austria), Transcontinental Inc. (Canada), Bischof+Klein SE & CO. KG (Germany), UFlex Limited (India)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLEXIBLE PACKAGING MARKET

3.2 FLEXIBLE PACKAGING MARKET, BY MATERIAL AND REGION

3.3 FLEXIBLE PACKAGING MARKET, BY PACKAGING TYPE

3.4 FLEXIBLE PACKAGING MARKET, BY PRINTING TECHNOLOGY

3.5 FLEXIBLE PACKAGING MARKET, BY APPLICATION

3.6 FLEXIBLE PACKAGING MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Growth of E-commerce platform

4.2.1.2 Cost-effectiveness and enhanced product shelf life

4.2.1.3 Rising demand for disposable packaging from end-use industries

4.2.1.4 Growing concerns toward sustainability

4.2.2 RESTRAINTS

4.2.2.1 Non-availability of efficient recycling infrastructure

4.2.2.2 Surge in raw material prices

4.2.3 OPPORTUNITIES

4.2.3.1 Commercialization of mono-material high-barrier films

4.2.3.2 Expansion of refill, reuse, and concentrate-compatible formats

4.2.3.3 Integration of recycled content via advanced mechanical & chemical recycling

4.2.4 CHALLENGES

4.2.4.1 High dependence on petrochemical-based resins

4.2.4.2 Rapidly evolving sustainability standards and certification requirements

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 SHELF-LIFE TRANSPARENCY

4.3.2 MATERIAL LIMITATIONS VS. CONSUMER EXPECTATIONS

4.3.3 PORTIONING AND USABILITY

4.3.4 PREMIUMIZATION WITHOUT PLASTIC WASTE

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES