농업용 드론 시장 예측(-2030년) : 제공 유형(하드웨어, 소프트웨어, Drone-as-a-Service), 기술 유형, 페이로드 용량, 컴포넌트, 농산물, 농장 규모, 비행 범위, 용도, 농업 환경, 지역별

Agriculture Drones Market by Offering Type (Hardware, Software, Drone-as-a-Service), Technology Type, Payload Capacity, Component, Farm Produce, Farm Size, Range, Application, Farming Environment, and Region - Global Forecast to 2030

상품코드:1858529

리서치사:MarketsandMarkets

발행일:2025년 10월

페이지 정보:영문 429 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

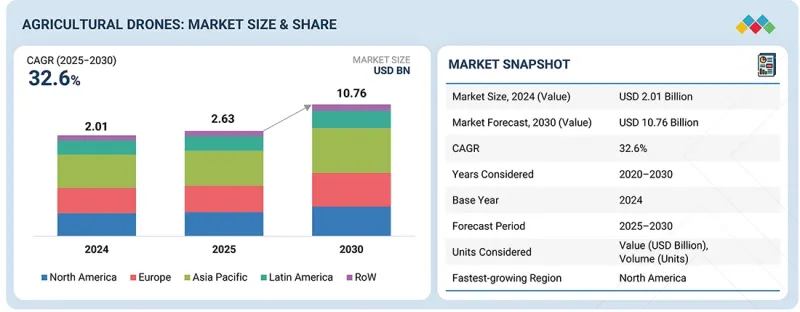

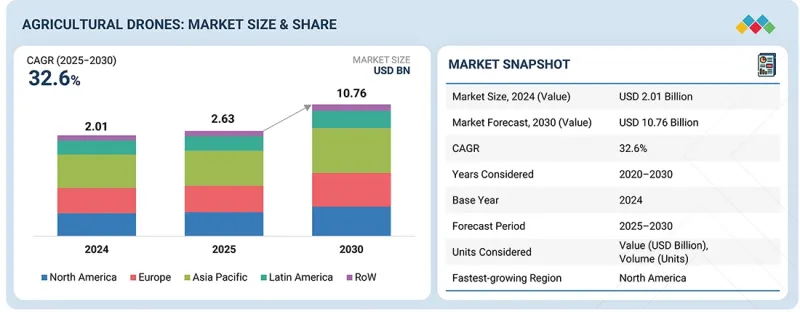

농업용 드론 시장 규모는 2025년 26억 3,000만 달러에서 2025-2030년의 예측 기간 중 32.6%의 CAGR로 추이하며, 2030년에는 107억 6,000만 달러에 달할 것으로 예측됩니다.

FAA의 농업용 드론 사용 승인으로 도입이 가속화되면서 농업용 드론 시장은 큰 성장 기회를 맞이하고 있습니다. 규제 장벽이 낮아짐에 따라 관계자들은 최소한의 컴플라이언스 요건만 충족하면 드론 기술을 도입할 수 있게 되어 시장 보급이 확대되고 있습니다. 드론과 데이터 분석 플랫폼의 활용으로 의사결정의 효율화, 자원의 최적화, 생산성 향상을 실현합니다. 또한 지속가능한 농업에 대한 관심이 높아지는 가운데, 드론은 환경 친화적인 농업 방식을 가능하게 하고 있습니다. FAA의 면제 조치도 드론 이용의 용이성을 촉진하고 있습니다. 또한 규제 완화로 인해 드론 운영과 관련된 교육 프로그램 및 컨설팅 서비스에 대한 수요도 증가하고 있습니다. 이는 시장 성장을 지원하는 새로운 사업 기회로 작용하고 있습니다. 이 면제 조치는 농업용 드론 시장 성장에 유리한 환경을 조성하는 중요한 요인으로 작용하고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준연도

2024년

예측 기간

2025-2030년

단위

금액(달러)·수량(수량)

부문별

제공 유형, 기술, 페이로드 용량, 컴포넌트, 농산물, 농장 규모, 비행 범위, 용도, 농업 환경, 지역

대상 지역

북미, 유럽, 아시아태평양, 남미, 기타 지역

드론의 민간 및 상업적 활용에 따른 보안 및 안전 문제: 민간 및 상업적 용도로 드론을 활용함에 있으며, 보안 및 안전 문제가 존재하며, 이는 농업용 드론 시장의 성장을 저해하는 요인으로 작용할 수 있습니다. 첫 번째 우려는 프라이버시 침해입니다. 카메라나 센서가 탑재된 드론은 사유지의 이미지나 데이터를 무단으로 취득할 우려가 있고, 법적 문제나 사회적 반발을 불러일으킬 위험이 있으며, 사생활 침해를 우려하는 농가의 도입 의욕을 떨어뜨릴 수 있습니다. 또한 다른 항공기와의 충돌 및 사고 위험도 문제시되고 있습니다. 드론은 농업 공역을 사용하므로 사고가 발생하면 인명사고나 물적 피해로 이어질 수 있고, 규제 강화와 책임 문제 증가가 발생해 농민들에게 드론 도입에 대한 부담이 될 수 있다는 우려가 있습니다.

"용도별로는 정밀농업 부문이 시장을 독점하고 있습니다."

그 이유로는 전 세계 인구 증가에 따른 식량안보의 필요성과 농업 생산성 최적화의 중요성을 들 수 있습니다. 정밀농업은 농가가 데이터에 기반한 의사결정을 통해 작물 수확량을 향상시키고 자원 활용을 최적화할 수 있습니다. 이 과정에서 드론은 필수적인 역할을 수행하며, 실시간 데이터와 상세한 분석 정보를 제공합니다. 또한 고해상도 이미지, 멀티 스펙트럼 센서, AI 통합 등 기술의 발전으로 작물과 토양의 성장 패턴, 건강 상태의 고도화된 분석이 가능해졌습니다. 이는 환경 규제 준수 및 지속가능한 제품에 대한 소비자 지향과도 일치합니다. 또한 정부의 첨단 농업 기술에 대한 보조금과 지원책은 농가가 드론과 정밀농업 솔루션에 대한 투자를 촉진하여 이 분야의 성장을 촉진하고 있습니다.

"아시아태평양이 예측 기간 중 높은 CAGR을 보일 것입니다."

이 지역에서는 정밀농업의 도입률이 매우 높아 농가는 드론을 작물 모니터링, 토양 분석, 정밀 방제 등에 적극 활용하고 있습니다. 또한 농업 현대화를 위한 정부의 구상도 시장 확대에 힘을 보태고 있습니다. 아시아 국가들은 식량안보와 지속가능성 향상을 위해 자금 지원, 보조금, 교육 프로그램을 통해 첨단 기술 도입을 촉진하고 있으며, 이는 드론 시장의 성장을 더욱 가속화하고 있습니다.

세계의 농업용 드론 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

거시경제 전망

시장 역학

촉진요인

억제요인

기회

과제

농업용 드론에서 생성형 AI의 영향

제6장 업계 동향

밸류체인 분석

무역 분석

공급망 분석

기술 분석

가격 분석

에코시스템 분석

고객 사업에 영향을 미치는 동향/혼란

특허 분석

2025-2026년의 주요 컨퍼런스와 이벤트

규제 상황

Porter's Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

투자와 자금조달 시나리오

2025년 미국 관세가 농업용 드론 시장에 미치는 영향

제7장 농업용 드론 시장 : 용도별

정밀농업

필드 지도제작

가변시용

작물 스카우팅

작물 살포

기타

가축 모니터링

정밀 양식

스마트 그린하우스

기타

제8장 농업용 드론 시장 : 컴포넌트별

프레임

컨트롤러 시스템

추진 시스템

센서 & 카메라 시스템

레이더 센서

LIDAR 센서

멀티스펙트럴 시스템

적외선 카메라

열 카메라

기타

내비게이션 시스템

GPS

GIS

배터리

기타

제9장 농업용 드론 시장 : 농장 규모별

소규모 농장(180에이커 미만)

중규모 농장(180-500에이커)

대규모 농장(500-2,000에이커)

초대형 규모 농장(2,000에이커 초과)

제10장 농업용 드론 시장 : 농업 환경별

야외

실내

제11장 농업용 드론 시장 : 제공 유형별

하드웨어

고정익 드론

회전익 드론

하이브리드 드론

소프트웨어

데이터 관리 소프트웨어

이미징 소프트웨어

데이터 분석 소프트웨어

기타 소프트웨어

DaaS(Drone-as-a-Service)

드론 플랫폼 서비스

유지보수·수리·점검(MRO) 서비스

드론 트레이닝 & 시뮬레이션 서비스

제12장 농업용 드론 시장 : 페이로드 용량별

소형 페이로드 드론(최대 2kg)

중형 페이로드 드론(2-20kg)

대형 페이로드 드론(20-50kg)

초대형 페이로드 드론(50kg 이상)

제13장 농업용 드론 시장 : 비행 범위별

목시내 비행(VLOS)

목시외 비행(BVLOS)

제14장 농업용 드론 시장 : 농산물별

곡물

옥수수

밀

쌀

기타

지방 종자·두류

대두

해바라기

기타

과일·채소

핵과류

감귤류

베리

근채류

잎 채소

기타

기타

제15장 농업용 드론 시장 : 기술별

열화상

멀티스펙트럴 이미징

초분광 이미징

광 검출·측거

RGB 이미징

합성 개구 레이더

근적외선 이미징

전지구 항법 위성 시스템

제16장 농업용 드론 시장 : 지역별

북미

미국

캐나다

멕시코

유럽

스페인

이탈리아

프랑스

독일

영국

기타

아시아태평양

중국

인도

일본

호주와 뉴질랜드

기타

남미

브라질

아르헨티나

기타

기타 지역

아프리카

중동

제17장 경쟁 구도

개요

주요 참여 기업의 전략/강점

매출 분석

시장 점유율 분석

기업 평가 매트릭스 : 주요 기업

기업 평가 매트릭스 : 신규 기업/중소기업

기업 평가와 재무 지표

브랜드/제품 비교

경쟁 시나리오·동향

제18장 기업 개요

주요 기업

DJI

TRIMBLE INC.

PARROT DRONE SAS

YAMAHA MOTOR CO., LTD.

AGEAGLE AERIAL SYSTEMS INC.

DRONEDEPLOY

SENTERA

XAG CO., LTD.

AUTEL ROBOTICS

YUNEEC

MICRODRONES

DESTINUS

GAMAYA

HYLIO

HIPHEN

기타 기업

JOUAV

SHENZHEN GC ELECTRONICS CO., LTD.

ARIES SOLUTIONS

WINGTRA AG

SKY-DRONES TECHNOLOGIES LTD

DELAIR

SHENZHEN GREPOW BATTERY CO., LTD.

APPLIED AERONAUTICS

VISION AERIAL, INC.

QUANTUM-SYSTEMS GMBH

제19장 인접 시장·관련 시장

제20장 부록

KSA

영문 목차

영문목차

The agriculture drones market is estimated to be USD 2.63 billion in 2025 and is projected to reach USD 10.76 billion by 2030, at a CAGR of 32.6% from 2025 to 2030. The FAA's approval of drones for agricultural use has led to an increase in their adoption. This will open a huge opportunity in the market for agricultural drones. With fewer regulatory hurdles, stakeholders may adopt drone technology with minimal compliance requirements, thereby opening the market to wider penetration. The use of drones and data analytics platforms will enable effective decision-making, optimizing resources, and leading to improved productivity. The focus on sustainability in agriculture makes it possible to use drones for environmentally friendly practices, and the FAA's waiver of exemption has made the use of drones easier. Lastly, the changed outlook in terms of rules means training programs and consultancy services for the smooth running of drone operations, thereby increasing demand. In conclusion, this exemption significantly contributes to creating a favorable environment for the growth of the agriculture drone market.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Units)

Segments

By Offering, Technology Type, Payload Capacity, Component, Farm Produce, Farm Size, Range, Application, Farming Environment, and Region

Regions covered

North America, Europe, Asia Pacific, South America, and Rest of the World (RoW)

Security and safety concerns associated with civil and commercial application of drones: Security and safety concerns due to civil and commercial use of drones can be a significant restraint for the agriculture drones market in the following ways. The first concern is the invasion of privacy; a camera- and sensor-equipped drone is likely to capture images or data from private properties, which can lead to legal challenges and public backlash, thus dissuading adoption among farmers who fear possible cases of infringement. Further risks include the possibility of accidents and collisions with other aircraft. Drones will occupy agricultural airspace, so any accident could potentially result in injury or property damage, increasing regulation and liability that may burden farmers from using drone technology.

"By application, precision farming segment to dominate agriculture drones market"

With several compelling reasons for the precision farming segment to dominate the agriculture drones market, the demand in this segment is strong. Growing populations worldwide have generated an imperative need for food security, and optimal agricultural productivity has become crucial. In turn, precision farming allows farmers to make data-driven decisions that increase crop yields and optimize resource usage. Drones are essential in the process, providing real-time data and detailed analytics that optimize the operations. Other technological advancements include the enhanced capabilities of drones, featuring high-resolution imaging, multispectral sensors, and integration with AI, which enables sophisticated crop and soil analysis to track growth patterns and assess health. Again, these types of operations align with environmental regulations and consumer preferences for sustainably sourced products. Government funding for contemporary agricultural techniques, by encouraging farmers to invest in drones and precision farming solutions, is thus spearheading the segment.

"Asia Pacific to witness significant CAGR during the forecast period"

The agriculture drones market is expected to grow significantly in the Asia Pacific region. The rate of adoption of precision agriculture is very high, as farmers increasingly find drones useful for crop monitoring, soil analysis, and targeted pesticide application. Government initiatives aimed at modernizing agriculture also further support this growth, as many Asian governments promote advanced technologies through funding, subsidies, and training programs to improve food security and sustainability.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the agriculture drones market:

By Company Type: Tier 1 - 55%, Tier 2 - 35%, and Tier 3 - 10%

By Designation: CXO's - 33%, Managers - 25%, Executives- 42%

By Region: North America - 30%, Europe - 35%, Asia Pacific - 20%, South America - 10% and Rest of the World -5%

Prominent companies in the market include DJI (China), Trimble Inc. (US), Parrot Drone Sas (France), Yamaha Motor Co., Ltd. (Japan), Ageagle Aerial Systems Inc. (US), Dronedeploy (US), XAG Co., Ltd. (China), Sentera (US), Autel Robotics (China), Yuneec (US), Microdrones (Germany), Gamaya (Brazil), Aerialtronics Dv B.V. (Netherlands), Hiphen (France), and Hylio (US).

Other players include Jouav (China), Shenzhen GC Electronics Co., Ltd. (China), Aries Solutions (India), Wingtra AG (Switzerland), Sky-Drones Technologies Ltd. (UK), Delair (France), Shenzhen Grepow Battery Co., Ltd. (China), Applied Aeronautics (US), and Vision Aerial, Inc. (US)

Research Coverage:

This research report categorizes the agriculture drones market by payload capacity (small payload drones (up to 2 kg), medium payload drones, large payload drones, and heavy payload drones), farm size (small-sized farms, middle-sized farms, large-sized farms, and super large farms), component (frames, controller systems, propulsion systems, sensors and camera systems, navigation systems, batteries, other components), offering type (hardware, software, and drone-as-a-services), technology type (thermal imaging, multispectral imaging, hyperspectral imaging, light detection and ranging (LIDAR), RGB imaging, synthetic aperture radar (SAR), near-infrared (NIR) imaging, global navigation satellite system (GNSS)), farm produce (cereals and grains, oilseeds and pulses, fruits and vegetables, other crop types), range (visual line of sight (VLOS), beyond visual line of sight (BVLOS)),application (precision farming, livestock monitoring, precision fish farming, smart greenhouses, other applications), farming environment (outdoor, indoor), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the agriculture drones market. A detailed analysis of the key industry players has been done to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the agriculture drones market. This report covers the competitive analysis of upcoming startups in the agriculture drones market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem and market mapping, patent analysis, and regulatory landscape, among others.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall agriculture drones and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (government initiatives to promote water conservation), restraints (high initial investment costs of agriculture drones), opportunities (increasing adoption of precision agriculture and sustainable practices), and challenges (lack of training and awareness among farmers) influencing the growth of the agriculture drones market.

New product launch/Innovation: Detailed insights on research & development activities and new product launches in the agriculture drones market.

Market Development: Comprehensive information about lucrative markets - the report analyzes the agriculture drones across varied regions.

Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the agriculture drones market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product food prints of leading players such as DJI (China), Trimble Inc. (US), Parrot Drone Sas (France), Yamaha Motor Co., Ltd. (Japan), Ageagle Aerial Systems Inc. (US), XAG Co., Ltd. (China), Autel Robotics (China), and other players in the agriculture drones market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 UNIT CONSIDERED

1.4.1 CURRENCY/VALUE UNIT

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key insights from industry experts

2.1.2.3 Breakdown of primary profiles

2.2 MARKET SIZE ESTIMATION

2.2.1 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

2.2.2 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AGRICULTURE DRONES MARKET

4.2 ASIA PACIFIC: AGRICULTURE DRONES MARKET, BY OFFERING TYPE AND COUNTRY

4.3 AGRICULTURE DRONES MARKET, BY OFFERING TYPE

4.4 AGRICULTURE DRONES MARKET, BY FARM SIZE

4.5 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY

4.6 AGRICULTURE DRONES MARKET, BY FARM PRODUCE

4.7 AGRICULTURE DRONES MARKET, BY APPLICATION

4.8 AGRICULTURE DRONES MARKET, BY RANGE AND REGION

4.9 AGRICULTURE DRONES MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MACROECONOMIC OUTLOOK

5.2.1 REDUCTION IN ARABLE LAND

5.2.2 RAPID DIGITALIZATION

5.3 MARKET DYNAMICS

5.3.1 DRIVERS

5.3.1.1 Demand for smart farm optimization and resource usage efficiency optimization using agricultural drones

5.3.1.2 Favorable government policies, subsidies, and regulations

5.3.1.3 Availability of software solutions for field surveys and data analytics

5.3.1.4 Growing concerns regarding change in diet and climate patterns

5.3.1.5 Increasing labor shortages

5.3.2 RESTRAINTS

5.3.2.1 Security and safety concerns associated with civil and commercial applications of drones

5.3.2.2 Large number of fragmented lands in developing countries

5.3.2.3 Lack of technical knowledge and training activities

5.3.3 OPPORTUNITIES

5.3.3.1 Exemptions by US FAA for use of agriculture drones

5.3.3.2 High adoption of aerial data collection tools in agriculture

5.3.3.3 Increase in use of agricultural-based software via smartphones

5.3.3.4 Need for early detection of crop diseases and ease of farm management

5.3.4 CHALLENGES

5.3.4.1 Management of data collected by agriculture drones

5.3.4.2 Lack of standardization of communication interfaces and protocols for precision agriculture

5.3.4.3 Lack of technical knowledge among farmers

5.3.4.4 Scarcity of trained pilots

5.3.4.5 High upfront costs of agricultural drones

5.4 IMPACT OF GEN AI ON AGRICULTURE DRONES

5.4.1 INTRODUCTION

5.4.2 USE OF GEN AI ON AGRICULTURE DRONES

5.4.3 CASE STUDY ANALYSIS

5.4.3.1 AI drone revolutionizes weed control in Canadian agriculture

5.4.3.2 Gayama enhanced agricultural productivity and sustainability through innovative AI technologies

5.4.4 IMPACT ON AGRICULTURE DRONES MARKET

5.4.5 ADJACENT ECOSYSTEM WORKING ON GENERATIVE AI

6 INDUSTRY TRENDS

6.1 INTRODUCTION

6.2 VALUE CHAIN ANALYSIS

6.2.1 RESEARCH & DEVELOPMENT EXECUTIVES

6.2.2 DEVICE & COMPONENT MANUFACTURERS

6.2.3 SYSTEM INTEGRATORS

6.2.4 SERVICE PROVIDERS

6.2.5 END USERS

6.2.6 POST-SALES SERVICE PROVIDERS

6.3 TRADE ANALYSIS

6.3.1 EXPORT SCENARIO OF HS CODE 8806

6.3.2 IMPORT SCENARIO OF HS CODE 8806

6.4 SUPPLY CHAIN ANALYSIS

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGIES

6.5.1.1 Internet of Things (IoT)

6.5.1.2 Artificial Intelligence and Machine Learning

6.5.1.3 Machine Learning (ML)

6.5.2 COMPLEMENTARY TECHNOLOGIES

6.5.2.1 Remote sensing technology

6.5.2.2 Crop management software

6.5.3 ADJACENT TECHNOLOGIES

6.5.3.1 Robotics

6.6 PRICING ANALYSIS

6.6.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY PAYLOAD CAPACITY, 2024

6.6.2 AVERAGE SELLING PRICE TREND, BY PAYLOAD CAPACITY, 2020-2024

6.6.3 AVERAGE SELLING PRICE TREND, BY REGION, 2020-2024

6.7 ECOSYSTEM ANALYSIS

6.7.1 DEMAND SIDE

6.7.2 SUPPLY SIDE

6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.9 PATENT ANALYSIS

6.9.1 LIST OF MAJOR PATENTS

6.10 KEY CONFERENCES & EVENTS, 2025-2026

6.11 REGULATORY LANDSCAPE

6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.11.2 REGULATORY FRAMEWORK

6.11.2.1 North America

6.11.2.1.1 US

6.11.2.1.2 Canada

6.11.2.1.3 Mexico

6.11.2.2 Europe

6.11.2.3 Asia Pacific

6.11.2.3.1 India

6.11.2.3.2 China

6.11.2.3.3 Australia

6.11.2.4 South America

6.11.2.4.1 Brazil

6.11.2.5 Rest of the World (RoW)

6.12 PORTER'S FIVE FORCES ANALYSIS

6.12.1 THREAT OF NEW ENTRANTS

6.12.2 THREAT OF SUBSTITUTES

6.12.3 BARGAINING POWER OF SUPPLIERS

6.12.4 BARGAINING POWER OF BUYERS

6.12.5 INTENSITY OF COMPETITIVE RIVALRY

6.13 KEY STAKEHOLDERS & BUYING CRITERIA

6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.13.2 BUYING CRITERIA

6.14 CASE STUDY ANALYSIS

6.14.1 EAVISION LAUNCHED NEW INTELLIGENT AGRICULTURAL SPRAYING DRONE IN CHINA

6.14.2 PARROT LAUNCHED ANAFI THERMAL FOR BETTER CROP SCOUTING, FIELD MONITORING, AND DATA ANALYTICS

6.14.3 ENHANCING TEA PLANTATION PRODUCTIVITY AND SUSTAINABILITY THROUGH DRONE INTEGRATION

6.15 INVESTMENT AND FUNDING SCENARIO

6.15.1 INTRODUCTION

6.16 IMPACT OF 2025 US TARIFF ON AGRICULTURE DRONES MARKET

6.16.1 INTRODUCTION

6.16.2 KEY TARIFF RATES

6.16.3 DISRUPTIONS IN AGRICULTURE DRONES MARKET

6.16.4 PRICE IMPACT ANALYSIS

6.16.5 KEY IMPACTS ON VARIOUS REGIONS

6.16.5.1 North America

6.16.5.2 Europe

6.16.5.3 Asia Pacific

6.16.5.4 South America

6.16.5.5 ROW

6.16.6 END-USE INDUSTRY-LEVEL IMPACT

7 AGRICULTURE DRONES MARKET, BY APPLICATION

7.1 INTRODUCTION

7.2 PRECISION FARMING

7.2.1 GOVERNMENT INITIATIVES TO PROMOTE SMART FARMING TO BOOST DEMAND FOR AGRICULTURE DRONES

7.2.2 FIELD MAPPING

7.2.2.1 Weed Detection

7.2.2.2 Plant Counting

7.2.2.3 Crop Health Monitoring

7.2.2.4 Harvest Season Monitoring

7.2.2.5 Other Field Mapping Applications

7.2.3 VARIABLE RATE APPLICATION

7.2.4 CROP SCOUTING

7.2.5 CROP SPRAYING

7.2.6 OTHER PRECISION FARMING APPLICATIONS

7.3 LIVESTOCK MONITORING

7.3.1 GROWTH OF LIVESTOCK MONITORING TO DRIVE ADVANCEMENTS IN DRONE TECHNOLOGY

7.4 PRECISION FISH FARMING

7.4.1 REAL-TIME DATA AND NON-INVASIVE MONITORING TO BOOST DRONE DEMAND IN FISH FARMING

7.5 SMART GREENHOUSE

7.5.1 IMPROVED CROP QUALITY AND INCREASED OPERATIONAL EFFICIENCY TO BOOST DEMAND IN SMART GREENHOUSES

7.6 OTHER APPLICATIONS

8 AGRICULTURE DRONES MARKET, BY COMPONENT

8.1 INTRODUCTION

8.2 FRAMES

8.2.1 HIGH VERSATILITY OF FIBERGLASS TO DRIVE USE OF FRAMES IN AGRICULTURE DRONES

8.3 CONTROLLER SYSTEMS

8.3.1 ADVANCEMENTS IN REMOTE CONTROLLER SYSTEMS TO DRIVE USAGE IN AUTOMATION

8.4 PROPULSION SYSTEMS

8.4.1 PROPULSIONS SYSTEMS TO EXHIBIT HIGHEST ADOPTION IN HYBRID DRONES IN NEXT FIVE YEARS

8.5 SENSORS & CAMERA SYSTEMS

8.5.1 BOOSTING CROP MONITORING AND YIELD OPTIMIZATION VIA PRECISION DRONE IMAGING

8.5.2 RADAR SENSORS

8.5.3 LIDAR SENSORS

8.5.4 MULTISPECTRAL SYSTEMS

8.5.5 IR CAMERAS

8.5.6 THERMAL CAMERAS

8.5.7 OTHER SENSORS & CAMERA SYSTEMS

8.6 NAVIGATION SYSTEMS

8.6.1 REDUCE NEED FOR HUMAN INTERVENTION AND ENHANCE OPERATIONAL EFFICIENCY

8.6.2 GLOBAL POSITIONING SYSTEM

8.6.3 GEOGRAPHIC INFORMATION SYSTEM

8.7 BATTERIES

8.7.1 LONGER CAPACITY AND LOWER DISCHARGE RATE TO DRIVE USAGE IN SURVEYING AGRICULTURE DRONES

8.8 OTHER COMPONENTS

9 AGRICULTURE DRONES MARKET, BY FARM SIZE

9.1 INTRODUCTION

9.2 SMALL-SIZED FARMS (LESS THAN 180 ACRES)

9.2.1 GOVERNMENT INITIATIVES TO PROMOTE DRONE ADOPTION AMONG SMALLHOLDER FARMERS

9.3 MID-SIZED FARMS (MORE THAN 180 ACRES AND LESS THAN 500 ACRES)

9.3.1 ENHANCED OPERATIONAL EFFICIENCY AND IMPROVED YIELD MANAGEMENT TO DRIVE ADOPTION OF AGRICULTURE DRONES IN MID-SIZED FARMS

9.4 LARGE-SIZED FARMS (MORE THAN 500 ACRES AND LESS THAN 2000 ACRES)

9.4.1 INCREASED LABOR COSTS AND LABOR SHORTAGES IN AGRICULTURE SECTOR TO DRIVE ADOPTION OF AGRICULTURE DRONES

9.5 SUPER LARGE FARMS (MORE THAN 2,000 ACRES)

9.5.1 NECESSITY FOR ENHANCED EFFICIENCY AND URGENCY TO INCREASE CROP YIELDS AMID GLOBAL FOOD INSECURITY TO DRIVE ADOPTION

10 AGRICULTURE DRONES MARKET, BY FARMING ENVIRONMENT

10.1 INTRODUCTION

10.2 OUTDOOR

10.2.1 NEED FOR LARGE-SCALE CROP SPRAYING ACROSS EXPANSIVE FIELDS TO DRIVE MARKET

10.3 INDOOR

10.3.1 INCREASING USE OF DRONES IN POLLINATION TO BOOST DEMAND

11 AGRICULTURE DRONE MARKET, BY OFFERING TYPE

11.1 INTRODUCTION

11.2 HARDWARE

11.2.1 INCREASING DEMAND FOR PRECISION AGRICULTURE PRACTICES IN HARDWARE TECHNOLOGY TO DRIVE DEMAND

11.2.2 FIXED-WING DRONES

11.2.3 ROTARY-BLADE DRONES

11.2.4 HYBRID DRONES

11.3 SOFTWARE

11.3.1 GROWING NEED FOR REAL-TIME DATA ANALYSIS AND ACTIONABLE INSIGHTS FOR DECISION-MAKING TO DRIVE DEMAND

11.3.2 DATA MANAGEMENT SOFTWARE

11.3.3 IMAGING SOFTWARE

11.3.4 DATA ANALYTICS SOFTWARE

11.3.5 OTHER SOFTWARE

11.4 DRONE-AS-A-SERVICE (DAAS)

11.4.1 ADOPTION OF ADVANCED DRONE TECHNOLOGIES WITHOUT HIGH CAPITAL INVESTMENT TO BOOST DEMAND

11.4.2 DRONE PLATFORM SERVICES

11.4.3 DRONE MAINTENANCE, REPAIR, AND OVERHAUL SERVICES

11.4.4 DRONE TRAINING & SIMULATION SERVICES

12 AGRICULTURE DRONES MARKET, BY PAYLOAD CAPACITY

12.1 INTRODUCTION

12.2 SMALL PAYLOAD DRONES (UP TO 2 KG)

12.2.1 INCREASING ADOPTION OF PRECISION AGRICULTURE AMONG SMALL-SCALE FARMS AND USER-FRIENDLY OPERATION TO DRIVE DEMAND

12.3 MEDIUM PAYLOAD DRONES (2-20 KG)

12.3.1 VERSATILITY AND ADVANCED DATA COLLECTION CAPABILITIES TO DRIVE DEMAND

12.4 LARGE PAYLOAD DRONES (20-50 KG)

12.4.1 WIDER AREA COVERAGE AND ABILITY TO CARRY HEAVY LOADS TO BOOST ADOPTION OF LARGE PAYLOAD DRONES

12.5 HEAVY PAYLOAD DRONES (ABOVE 50 KG)

12.5.1 SCALABILITY ADVANTAGES FOR LARGER AGRICULTURAL ENTERPRISES TO DRIVE ADOPTION OF HEAVY PAYLOAD DRONES

13 AGRICULTURE DRONES MARKET, BY RANGE

13.1 INTRODUCTION

13.2 VISUAL LINE OF SIGHT (VLOS)

13.2.1 LENIENT REGULATORY FRAMEWORKS AND LESS RESTRICTIVE OPERATIONAL GUIDELINES TO FUEL ADOPTION

13.3 BEYOND VISUAL LINE OF SIGHT (BVLOS)

13.3.1 GROWING NEED FOR LARGE-SCALE FARMING SOLUTIONS AND ONGOING LABOR SHORTAGE TO BOOST ADOPTION

14 AGRICULTURE DRONES MARKET, BY FARM PRODUCE

14.1 INTRODUCTION

14.2 CEREALS & GRAINS

14.2.1 INNOVATION AND TECHNOLOGICAL ADVANCEMENTS TO DRIVE DEMAND FOR AGRICULTURE DRONES IN CEREALS & GRAINS

14.2.2 CORN

14.2.3 WHEAT

14.2.4 RICE

14.2.5 OTHER CEREALS & GRAINS

14.3 OILSEEDS & PULSES

14.3.1 AGRICULTURE DRONES WITH INFRARED, MULTISPECTRAL, AND HYPERSPECTRAL SENSORS TO DRIVE DEMAND

14.3.2 SOYBEAN

14.3.3 SUNFLOWER

14.3.4 OTHER OILSEEDS & PULSES

14.4 FRUITS & VEGETABLES

14.4.1 GROWING USE OF DATA ANALYTICS FOR OPTIMIZING CROP HEALTH AND NUTRIENT MANAGEMENT TO BOOST DEMAND

14.4.2 POME FRUITS

14.4.3 CITRUS FRUITS

14.4.4 BERRIES

14.4.5 ROOT & TUBER VEGETABLES

14.4.6 LEAFY VEGETABLES

14.4.7 OTHER FRUITS & VEGETABLES

14.5 OTHER CROP TYPES

15 AGRICULTURE DRONES MARKET, BY TECHNOLOGY TYPE

15.1 INTRODUCTION

15.2 THERMAL IMAGING

15.3 MULTISPECTRAL IMAGING

15.4 HYPERSPECTRAL IMAGING

15.5 LIGHT DETECTION AND RANGING

15.6 RGB IMAGING

15.7 SYNTHETIC APERTURE RADAR

15.8 NEAR-INFRARED IMAGING

15.9 GLOBAL NAVIGATION SATELLITE SYSTEM

16 AGRICULTURE DRONES MARKET, BY REGION

16.1 INTRODUCTION

16.2 NORTH AMERICA

16.2.1 US

16.2.1.1 Labor shortages and high agricultural production to drive market

16.2.2 CANADA

16.2.2.1 Constant enhancements and developments in precision farming practices to drive market

16.2.3 MEXICO

16.2.3.1 Financial support for digital agriculture to drive growth

16.3 EUROPE

16.3.1 SPAIN

16.3.1.1 Rising adoption of agriculture drones to create weed infestation maps for farmers

16.3.2 ITALY

16.3.2.1 Rising integration of precision agriculture, robots, and agriculture drones to drive market

16.3.3 FRANCE

16.3.3.1 Application of drones in crop mapping to boost demand

16.3.4 GERMANY

16.3.4.1 High adoption rate of agriculture drones for livestock monitoring to drive growth

16.3.5 UK

16.3.5.1 Availability of user-friendly technologies to drive growth

16.3.6 REST OF EUROPE

16.4 ASIA PACIFIC

16.4.1 CHINA

16.4.1.1 Increasing government spending to drive market

16.4.2 INDIA

16.4.2.1 Adoption of agriculture drones in surveying farms and assessing crop losses

16.4.3 JAPAN

16.4.3.1 Increasing adoption of precision farming technology to drive growth

16.4.4 AUSTRALIA & NEW ZEALAND

16.4.4.1 Different applications and use of agriculture drones to boost demand

16.4.5 REST OF ASIA PACIFIC

16.5 SOUTH AMERICA

16.5.1 BRAZIL

16.5.1.1 Growth in agricultural activities to boost market for digital advancements

16.5.2 ARGENTINA

16.5.2.1 Increase in public-private partnerships for agricultural innovations to drive growth

16.5.3 REST OF SOUTH AMERICA

16.6 REST OF THE WORLD

16.6.1 AFRICA

16.6.1.1 Increase in investments for agriculture innovations to drive growth

16.6.2 MIDDLE EAST

16.6.2.1 Surge in agricultural monitoring activities to boost market for digital agriculture

17 COMPETITIVE LANDSCAPE

17.1 OVERVIEW

17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

17.3 REVENUE ANALYSIS, 2020-2024

17.4 MARKET SHARE ANALYSIS, 2024

17.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

17.5.1 STARS

17.5.2 EMERGING LEADERS

17.5.3 PERVASIVE PLAYERS

17.5.4 PARTICIPANTS

17.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

17.5.5.1 Company footprint

17.5.5.2 Regional footprint

17.5.5.3 Offering type footprint

17.5.5.4 Application footprint

17.5.5.5 Component footprint

17.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024