멤브레인 바이오리액터 시장 : 멤브레인 유형별, 시스템 구성별, 용량별, 용도별, 지역별 예측

Membrane Bioreactor Market by Membrane Type, System Configuration, Capacity, Application, And Region - Global Forecast to 2030

상품코드:1901398

리서치사:MarketsandMarkets

발행일:2025년 11월

페이지 정보:영문 260 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

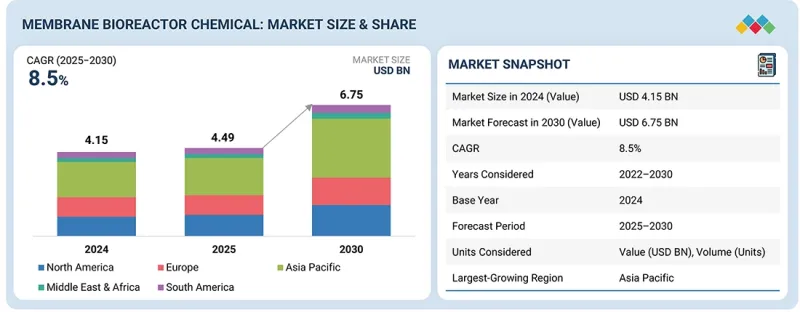

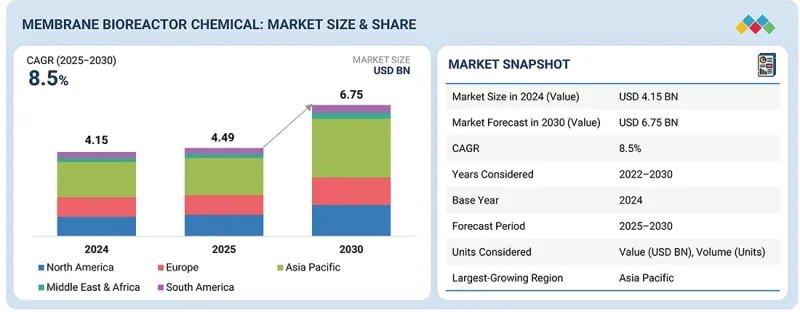

세계의 멤브레인 바이오리액터 시장의 규모는 2025년 44억 9,000만 달러에서 2030년까지 67억 5,000만 달러에 이를 것으로 예측되며, 예측기간 동안 CAGR 8.5%의 성장이 예상됩니다.

조사 범위

조사 대상 기간

2022-2030년

기준연도

2024년

예측기간

2025-2030년

단위

100만 달러, 대

부문

멤브레인 유형, 시스템 구성, 용량, 용도, 지역

대상 지역

유럽, 북미, 아시아태평양, 중동, 아프리카, 남미

중공사막은 폐수처리 용도에서의 수많은 이점으로 인해 멤브레인 바이오리액터 시장에서 두 번째로 성장이 빠른 유형이 되고 있습니다. 중공사막은 높은 표면적 대 체적비를 가지고 여과 효율을 높여 컴팩트한 시스템 설계를 가능하게 하므로 공간 제약이 있는 환경에 이상적입니다. 또한, 설계 구조는 효과적인 바이오매스의 유지를 촉진하고 투과액의 품질 향상을 실현하기 때문에 멤브레인 바이오리액터 시스템 전체의 성능 향상에 기여합니다. 중공사막은 오염(파울링)의 발생률이 낮아, 장기적으로 유지보수의 필요성과 운용 비용을 절감합니다.

중공사막 기술의 지속적인 진보 중에서도 특히 내구성과 내약품성이 우수한 재료의 개발이 채용을 더욱 촉진하고 있습니다. 산업에서 효율적이고 비용 효율적이며 지속 가능한 폐수 처리 솔루션에 대한 수요가 증가함에 따라 중공사막의 매력은 계속 증가하고 있으며 멤브레인 바이오리액터 시장에서 중요한 존재로서의 지위를 확립하고 있습니다.

"시스템 구성별로는 침지형 멤브레인 바이오리액터 시스템이 예측기간 동안 금액 기준으로 2위 성장률을 나타낼 전망입니다."

침지형 멤브레인 바이오리액터 시스템은 막 여과와 생물학적 처리 공정을 효율적으로 통합하여 멤브레인 바이오리액터 시장에서 성장률이 두 번째로 높은 부문이 되었습니다. 이 설계는 멤브레인을 폭기조에 직접 침지시켜 바이오매스의 유지성을 향상시키고 미생물 및 폐수의 접촉을 촉진합니다. 침지 구성은 처리 시설에 필요한 설치 면적을 크게 줄이기 때문에 공간에 제약이 있는 도시 환경에 특히 적합합니다. 또한, 침지형 멤브레인 바이오리액터 시스템은 수중 막이 공기에 노출될 기회가 적고 역세척이 필요하지 않으므로 오염률이 낮고 운영 비용을 절감할 수 있습니다. 효율적이고 공간 절약적인 폐수 처리 솔루션에 대한 수요가 높아지는 가운데 침지형 멤브레인 바이오리액터 시스템은 도시 폐수 처리부터 산업 공정까지 다양한 용도로 채용이 진행되고 있어 시장 성장이 더욱 촉진되고 있습니다.

"용도별로는 산업 폐수 처리가 예측기간 동안 금액 기준으로 2위의 시장 규모를 차지할 전망입니다."

멤브레인 바이오리액터 시장에서 산업 폐수 처리가 제2위의 용도인 요인은 제약, 식품 및 음료, 섬유 등의 산업에서 발생하는 배수의 양과 복잡성 증가에 있습니다. 이 부문은 환경 규제 준수를 위해 엄격한 수질 기준을 충족해야 하며, 오염물질을 효과적으로 제거하고 고품질의 배수를 공급할 수 있는 멤브레인 바이오리액터 등의 첨단 처리 솔루션에 대한 수요가 촉진되고 있습니다. 멤브레인 바이오리액터 기술은 기존의 처리 방법에 비해 컴팩트한 설계, 설치 면적 축소, 운영 비용 절감 등의 이점도 제공합니다. 이는 폐수 관리에서 지속 가능성과 효율성 향상을 목표로 하는 업계에 매력적인 선택이 되었습니다. 게다가 물 재사용과 자원 회수에 대한 관심이 높아짐에 따라 산업용 분야에서 멤브레인 바이오리액터 시스템의 채용이 촉진되고 따라서 큰 시장 점유율이 예상되고 있습니다.

지역별로는 북미가 2023년 멤브레인 바이오리액터 시장에서 금액 기준으로 2위의 규모를 차지하였습니다.

여러 요인들로 인해 북미는 멤브레인 바이오리액터 부문에서 두 번째로 큰 시장이 되었습니다. 이 지역은 견고한 산업 및 공공 인프라를 보유하고 있으며, 제약, 화학, 식품 및 음료, 자동차 제조 등 중요한 부문이 선진 폐수 처리 솔루션 수요를 촉진하고 있습니다. 특히 미국 환경보호청(EPA)에 의한 엄격한 환경규제는 폐수 배출 기준을 높게 설정하고 있으며, 멤브레인 바이오리액터 기술이 규제 준수를 위한 효과적인 선택지가 되고 있습니다. 게다가 물 부족에 대한 우려 증가와 지속 가능한 물 관리 기술의 필요성으로 인해 물 재사용을 지원하는 멤브레인 바이오리액터 시스템에 대한 투자가 증가하고 있습니다. 이 지역의 지속적인 기술 진보와 연구개발 노력도 멤브레인 바이오리액터의 효율성을 높이고 있으며, 북미는 세계의 멤브레인 바이오리액터 시장에서 주요 국가로서의 지위를 강화하고 있습니다.

이 보고서는 세계의 멤브레인 바이오리액터 시장에 대한 조사 분석을 통해 주요 촉진요인 및 억제요인, 제품 개발 및 혁신, 경쟁 구도에 대한 인사이트를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 인사이트

멤브레인 바이오리액터 시장의 기업에게 매력적인 기회

멤브레인 바이오리액터 시장 : 막 유형별

멤브레인 바이오리액터 시장 : 시스템 구성별

멤브레인 바이오리액터 시장 : 용도별

멤브레인 바이오리액터 시장 : 국가별

제5장 시장 개요

시장 역학

촉진요인

억제요인

기회

과제

미충족 요구 및 사업 기회

MBR 시장에서의 미충족 요구

사업 기회

연관 시장 및 부문 간 기회

연관 시장

부문 간 기회

신규 비즈니스 모델 및 생태계 변화

신규 비즈니스 모델

생태계 변화

Tier 1, 2, 3 기업의 전략적 움직임

제6장 업계 동향

Porter's Five Forces 분석

거시경제지표

밸류체인 분석

원재료 공급자

제조자

판매자

최종 소비자

생태계 분석

가격 설정 분석

평균 판매 가격 : 주요 기업별(2024년)

평균 판매 가격 : 지역별(2022-2024년)

무역 분석

수입 시나리오(HS코드 841989)

수출 시나리오(HS코드 841989)

주요 회의 및 이벤트(2026년)

고객 사업에 영향을 끼치는 동향 및 혼란

투자 및 자금조달 시나리오

사례 연구 분석

멤브레인 바이오리액터 시장에 대한 2025년 미국 관세의 영향

주요 관세율

가격 영향 분석

국가 및 지역에 미치는 영향

최종 사용 산업에 대한 영향

제7장 기술, 특허, 디지털, AI의 채용에 의한 전략적 파괴

주요 신기술

MBR 및 폐수 처리 플랜트의 AI 디지털 트윈(DT)

바이오차 이용 MBR

보완 기술

기술 및 제품 로드맵

단기 : 기반 구축과 조기 상업화(2025-2027년)

중기 : 확장과 표준화(2027-2030년)

장기 : 대규모 상업화와 파괴적 변화(2030-2035년 이후)

특허 분석

조사 방법

문서 유형

고찰

특허의 법적 지위

관할 분석

주요 출원인

과거 10년간의 주요 10개 특허 보유사

미래 용도

무방류 시스템(ZLD)

고독성 및 미량오염물질 제거

극한 환경 처리

음용수 재사용

분산형 시스템 패키지

MBR 시장에 대한 AI 및 생성형 AI의 영향

주요 이용 사례와 시장의 장래성

MBR 처리 모범 사례

MBR 시장에서의 AI 도입 사례 연구

연관 인접 생태계와 시장 기업에 미치는 영향

MBR 시장에서의 생성형 AI 채용에 대한 클라이언트의 준비 상황

제8장 지속 가능성과 규제 정세

지역 규제 및 규정 준수

규제기관, 정부기관, 기타 조직

업계 표준

지속 가능성에 대한 노력

지속 가능성에 미치는 영향과 규제 정책의 노력

인증, 라벨, 환경 기준

제9장 고객 상황과 구매 행동

의사결정 프로세스

주요 이해관계자와 구매 기준

채용 장벽과 내부 과제

다양한 최종 사용 산업에서의 미충족 요구

시장의 수익성

잠재적인 수익

비용 역학

주요 최종 사용 산업에서의 사업 기회

제10장 멤브레인 바이오리액터 시장 : 시스템 구성별

침지형 MBR

외부가압식 MBR

제11장 멤브레인 바이오리액터 시장 : 막 유형별

중공사막

플랫 시트

다중 관

제12장 멤브레인 바이오리액터 시장 : 용량별

소

중

대

제13장 멤브레인 바이오리액터 시장 : 용도별

도시 하수 처리

산업 폐수 처리

식품 및 음료

석유 및 가스

펄프 및 제지

의약품

기타 산업 폐수 처리 용도

제14장 멤브레인 바이오리액터 시장 : 지역별

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

튀르키예

기타 유럽

아시아태평양

중국

일본

인도

한국

호주

기타 아시아태평양

중동 및 아프리카

GCC 국가

이집트

남아프리카

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제15장 경쟁 구도

개요

주요 진입기업의 전략 및 강점

수익 분석(2022-2024년)

시장 점유율 분석(2024년)

기업 평가 및 재무지표(2024년)

브랜드 및 제품 비교 분석

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

경쟁 시나리오

제16장 기업 프로파일

주요 기업

VEOLIA

KUBOTA CORPORATION.

XYLEM

TORAY INDUSTRIES, INC.

MANN HUMMEL

MITSUBISHI CHEMICAL CORPORATION

KOVALUS SEPARATION SOLUTIONS

DUPONT

ALFA LAVAL

PENTAIR

CITIC ENVIRONMENTAL TECHNOLOGIES CO., LTD.

AQUATECH

MEMBION GMBH

기타 기업

B&P WATER TECHNOLOGIES SRL

BERGHOF MEMBRANE TECHNOLOGY GMBH

HUBER SE

LENNTECH BV

TRIQUA INTERNATIONAL

WEHRLE-WERK AG

EUROPE MEMBRANE

SIGMADAF

AQUAMATCH

HITACHI, LTD.

CLEAR AQUA TECHNOLOGIES P. LTD.

HYDROTECH

HINADA

제17장 부록

CSM

영문 목차

영문목차

The membrane bioreactor market is projected to grow from USD 4.49 billion in 2025 to USD 6.75 billion by 2030, at a CAGR of 8.5% during the forecast period.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Unit)

Segments

By Membrane Type, System Configuration, Capacity Application, and Region

Regions covered

Europe, North America, Asia Pacific, the Middle East & Africa, and South America

Hollow fiber membranes are the second fastest-growing type in the membrane bioreactor market due to their numerous advantages in wastewater treatment applications. These membranes offer a high surface area-to-volume ratio, which enhances filtration efficiency and allows for compact system designs, making them ideal for space-constrained environments. Their design also facilitates effective biomass retention and provides improved permeate quality, contributing to the overall performance of membrane bioreactor systems. Hollow fiber membranes exhibit lower fouling rates, which reduces maintenance needs and operational costs over time.

The continuous advancements in hollow fiber membrane technology, including the development of more durable and chemically resistant materials, have further boosted their adoption. As industries increasingly seek efficient, cost-effective, and sustainable wastewater treatment solutions, the appeal of hollow fiber membranes continues to grow, positioning them as a key player in the membrane bioreactor market.

''Based on system configuration, submerged membrane bioreactor system is the second fastest-growing market during the forecast period, in terms of value.''

The submerged membrane bioreactor system is the second fastest-growing segment in the membrane bioreactor market due to its efficient integration of membrane filtration and biological treatment processes. This design allows the membranes to be submerged directly in the aeration tank, enhancing the retention of biomass and promoting better contact between microorganisms and wastewater. The submerged configuration significantly reduces the footprint required for treatment facilities, making it particularly suitable for urban environments with space constraints. Additionally, the submerged membrane bioreactor system tends to experience lower fouling rates and reduced operational costs, as the submerged membranes are less exposed to air and do not require backwashing. With increasing demand for effective and space-saving wastewater treatment solutions, the submerged membrane bioreactor system is gaining traction in various applications, from municipal wastewater treatment to industrial processes, further driving its market growth.

"Based on application, industrial wastewater treatment is projected to be the second-largest market during the forecast period, in terms of value."

Industrial wastewater treatment is the second-largest application in the membrane bioreactor market, primarily due to the increasing volume and complexity of wastewater produced by industries such as pharmaceuticals, food and beverage, and textiles. These sectors are subject to stringent water quality standards that must be met to comply with environmental regulations, driving the demand for advanced treatment solutions, such as membrane bioreactors, that can effectively remove contaminants and deliver high-quality effluent. Membrane bioreactor technology also offers benefits, including a compact design, a smaller footprint, and lower operational costs compared to traditional treatment methods, making it an appealing choice for industries seeking to enhance sustainability and efficiency in wastewater management. Furthermore, the growing focus on water reuse and resource recovery is enhancing the adoption of membrane bioreactor systems in industrial applications, thereby reinforcing their significant market share.

"Based on region, North America is the second-largest market for membrane bioreactor in 2023, in terms of value."

North America is the second-largest market for membrane bioreactors due to several key factors. The region boasts a robust industrial and municipal infrastructure, with significant sectors such as pharmaceuticals, chemicals, food and beverage, and automotive manufacturing driving the demand for advanced wastewater treatment solutions. Stringent environmental regulations, particularly from the U.S. Environmental Protection Agency (EPA), mandate high standards for wastewater discharge, making membrane bioreactor technology an effective option for compliance. Furthermore, growing concerns over water scarcity and the need for sustainable water management practices are leading to increased investments in membrane bioreactor systems that support water reuse. Ongoing technological advancements and research and development efforts in the region also enhance the efficiency and effectiveness of membrane bioreactors, reinforcing North America's position as a major player in the global membrane bioreactor market.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies include Veolia (France), KUBOTA Corporation (Japan), Mitsubishi Chemical Corporation (Japan), TORAY INDUSTRIES, INC. (Japan), Kovalus Separation Solutions (US), Dupont (US), Xylem (US), Pentair (UK), Mann+Hummel (Germany), ALFA LAVAL (Sweden), CITIC Envirotech (China), and Aquatech (Canada).

Research Coverage

This research report categorizes the membrane bioreactor market by membrane type (hollow fiber, flat sheet, multi-tubular), system configuration (submerged membrane bioreactor system, external membrane bioreactor system), capacity (small capacity, medium capacity, large capacity), application, and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the membrane bioreactor market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions, services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the membrane bioreactor market are all covered. This report includes a competitive analysis of upcoming startups in the membrane bioreactor market ecosystem.

Reasons to buy this report:

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall membrane bioreactor market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (increasing demand for effective wastewater treatment, rising stringent environmental regulations standards, growing concern over water scarcity), restraints (membrane fouling, high initial capital investment), opportunities (Increasing focus on sustainability, integration of membrane bioreactor technology with other advanced treatment processes), and challenges (technical complexity of membrane bioreactor systems, high energy consumption).

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the membrane bioreactor market.

Market Development: Comprehensive information about lucrative markets - the report analyses the membrane bioreactor market across varied regions.

Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the membrane bioreactor market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Veolia (France), KUBOTA Corporation (Japan), Mitsubishi Chemical Corporation (Japan), TORAY INDUSTRIES, INC. (Japan), Kovalus Separation Solutions (US), Dupont (US), Xylem (US), Pentair (UK), Mann+Hummel (Germany), ALFA LAVAL (Sweden), CITIC Envirotech (China), and Aquatech (Canada) in the membrane bioreactor market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 INCLUSIONS AND EXCLUSIONS

1.3.2 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 List of primary interview participants-demand and supply sides

2.1.2.2 Key data from primary sources

2.1.2.3 Breakdown of primary interviews

2.1.2.4 Insights from industry experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 FORECAST NUMBER CALCULATION

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 RESEARCH ASSUMPTIONS

2.7 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS