해저 케이블 시스템 시장 : 케이블 유형별, 컴포넌트별, 절연체별, 유형별 예측(-2030년)

Submarine Cable Systems Market by Cable Type (Communication Cable, Power Cable), Component (Dry Plant Product, Wet Plant Product), Insulation (Cross-linked Polyethylene, Oil-Impregnated Paper) and Type (Single Core, Multicore) - Global Forecast to 2030

상품코드:1788514

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 291 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

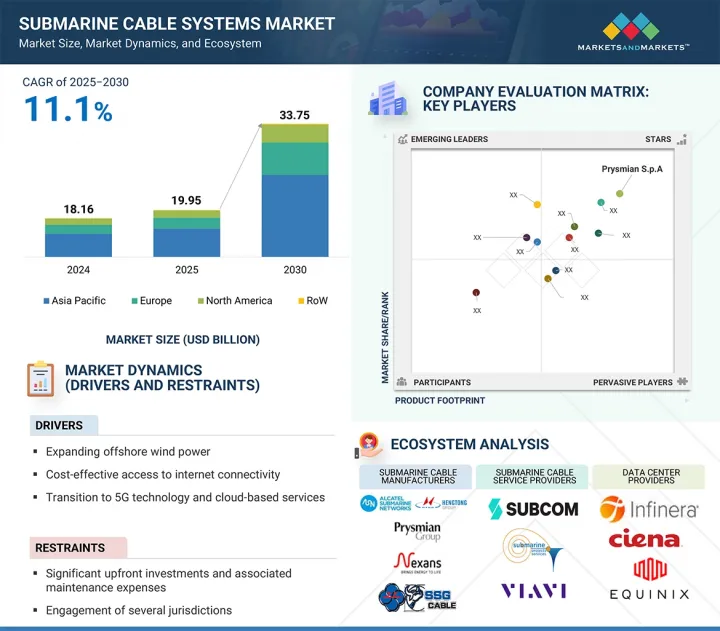

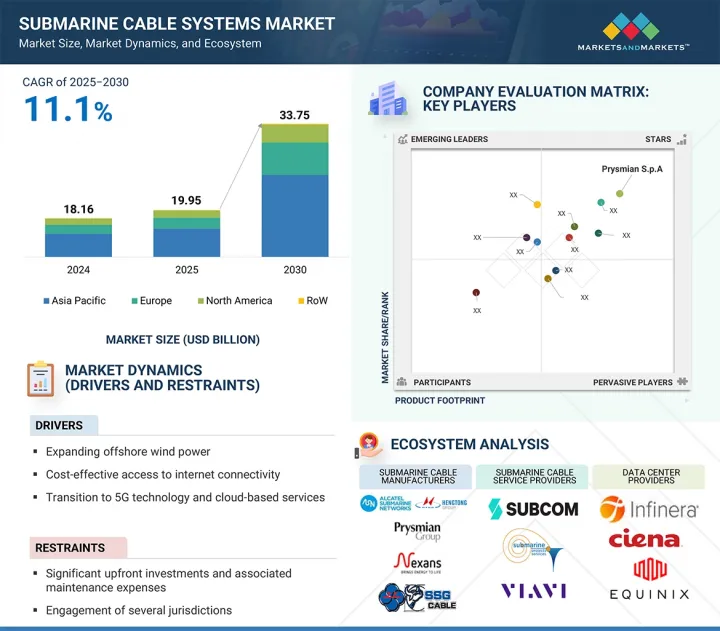

세계의 해저 케이블 시스템 시장 규모는 2025년 199억 5,000만 달러에서 2030년까지 337억 5,000만 달러에 이를 것으로 예측되며, CAGR 11.1%의 성장이 예상됩니다.

5G를 통해 모바일 단말기와 IoT 기기는 속도, 지연, 신뢰성, 전력 소비를 개선하면서 동시에 여러 연결에 대응할 수 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

케이블 유형, 부품, 서비스 제공, 유형, 전압, 절연체, 최종 용도, 지역

대상 지역

북미, 유럽, 아시아태평양 및 기타 지역

주파수 대역의 경매는 거의 종료되고, 5G 대응의 휴대 단말이 발표되어, 세계적으로 네트워크의 구현이 시작되고 있습니다. 5G 개발의 대부분은 B2C 시장에 집중되어 있으며, 이는 네트워크 사업자의 운영 비용 절감 활동 때문입니다. 동영상 및 음성 스트리밍 서비스와 같은 대역폭을 많이 소비하는 용도에 따른 데이터 수요 증가와 클라우드 서비스 및 5G로의 지속적인 이동으로 인해 광섬유 상호 연결의 필요성이 커지고 있으며, 이는 해저 케이블 시스템 시장의 성장을 뒷받침합니다.

"건조 플랜트 제품 부문이 2024년 통신 케이블 해저 케이블 시스템 시장에서 2위를 차지했습니다."

해저 케이블 시스템 시장에서 건식 플랜트 제품에 대한 수요는 해저 케이블 네트워크가 해안에 도달한 후의 지원과 성능 최적화의 필요성에 의해 견인되고 있습니다. 데이터센터의 급속한 확장과 광대역 서비스의 보급은 견고한 지상 인프라를 필요로 합니다.

"부설 및 시운전 부문이 2025-2030년에 해저 통신 케이블 시장에서 가장 높은 CAGR을 나타냅니다."

해저 케이블의 설치와 시운전은 여러 요인에 의해 추진되고 있습니다. 첫째, 빠르고 신뢰할 수 있는 연결성에 대한 세계 수요 증가는 해저 케이블 네트워크를 신속하게 배포하기 위한 효율적인 설치 및 시운전 프로세스에 대한 요구를 뒷받침하고 있습니다. 둘째, 원격조작 무인탐사기(ROV)나 전용선 등 부설기술의 진보로 어려운 수중환경에서도 보다 신속하고 정확한 케이블부설이 가능해 부설시간과 비용 절감에 기여하고 있습니다.

"해외 인프라에 대한 관심 증가는 2024년 아시아태평양을 2위 해저 전력 케이블 시장으로 만들었습니다."

Global Wind Energy Council(GWEC)의 예측에 따르면 아시아태평양은 지난 10년 동안 해외 풍력에너지 확대를 독점할 것으로 예측됩니다. 중국은 신재생에너지와 해외 인프라 개발을 적극적으로 추진하고 있기 때문에 세계 해저전력케이블 시장의 지배자로 대두하고 있습니다. 이 나라는 향후 5년 이내에 64GW의 해양 풍력 발전 용량을 추가하는 목표를 내걸고 있으며, 화석 연료에 대한 의존도를 줄이고 탄소 중립의 달성을 목표로 하고 있습니다.

이 보고서는 세계 해저 케이블 시스템 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

해저 케이블 시스템 시장의 기업에게 매력적인 기회

해저 케이블 시스템 시장 : 케이블 유형별

해저 통신 케이블 시장 : 컴포넌트별

해저 전력 케이블 시장 : 절연체별

유럽의 해저 전력 케이블 시장 : 최종 용도별, 국가별

해저 전력 케이블 시장 : 국가별

제5장 시장 개요

소개

시장 역학

성장 촉진요인

억제요인

기회

과제

고객사업에 영향을 주는 동향 및 혼란

가격 설정 분석

해저 케이블 시스템의 가격대 : 케이블 유형별(2024년)

해저 통신 케이블의 평균 판매 가격 동향(2021-2024년)

주요 기업이 제공하는 해저 케이블 시스템의 가격대 : 케이블 유형별(2024년)

해저 전력 케이블의 평균 판매 가격 동향 : 지역별(2021-2024년)

밸류체인 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

주요 기술

보완 기술

인접 기술

특허 분석

무역 분석

수입 시나리오(HS 코드 8544)

수출 시나리오(HS 코드 8544)

주요 컨퍼런스 및 이벤트(2025-2026년)

사례 연구

CAMBRIDGE MANAGEMENT CONSULTING, PELAGIAN, BAKER BOTTS가 터크스 케이커스 제도에서 내장해성이 뛰어난 대용량의 광섬유 접속 솔루션을 제공

TRATOS, ENI의 멕시코 AREA 1 개발 프로젝트의 특정 요구사항에 대응하는 해저 케이블 부품 공급

CORAL SEA CABLE SYSTEM(CS2) 프로젝트에 의해 파푸아뉴기니와 솔로몬 제도의 인터넷 접속이 고속화

N-SEA, 기상 리스크 관리에 SINAY의 METOCEAN ANALYTICS를 활용하여 프로젝트의 탄력성을 강화

규제 상황

규제기관, 정부기관, 기타 조직

표준

Porter's Five Forces 분석

주요 이해관계자와 구매 프로세스

구매 프로세스의 주요 이해 관계자

구입 기준

해저 케이블 시스템 시장에 대한 AI/생성형 AI의 영향

소개

주요 최종 용도 용도에 대한 AI/생성형 AI의 영향

AI/생성형 AI 이용 사례

해저 케이블 시스템 에코시스템에서 AI/생성형 AI의 미래

해저 케이블 시스템 시장에 대한 2025년 미국 관세의 영향

소개

주요 관세율

가격의 영향 분석

국가/지역에 미치는 영향

최종 용도 용도에 대한 영향

제6장 해저 케이블 시스템 시장 : 케이블 유형별

소개

통신 케이블

전력 케이블

제7장 해저 통신 케이블 시장 : 컴포넌트별

소개

건식 플랜트 제품

습식 플랜트 제품

제8장 해저 통신 케이블 시장 : 서비스 제공별

소개

부설 및 시운전

유지보수

시스템 업그레이드

제9장 해저 전력 케이블 시장 : 유형별

소개

단심

다심

제10장 해저 전력 케이블 시장 : 전압별

소개

중전압

고전압

제11장 해저 전력 케이블 시장 : 절연체별

소개

가교 폴리에틸렌(XLPE)

오일 함침지(OIP)

수지 함침지(RIP)

수지 함침 합성(RIS)

제12장 해저 전력 케이블 시장 : 최종 용도별

소개

해외 풍력 발전소

국가 및 섬간 접속

해양 석유 및 가스 플랜트

제13장 해저 전력 케이블 시장 : 지역별

소개

북미

미국

캐나다

멕시코

유럽

영국

독일

덴마크

네덜란드

노르웨이

프랑스

기타 유럽

아시아태평양

중국

일본

한국

말레이시아

인도네시아

베트남

기타 아시아태평양

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

앙골라

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제14장 해저 통신 케이블 시장 : 지역별

소개

대서양 횡단

태평양 횡단

아시아내

아메리카

유라시아

유럽, 중동 및 아프리카

제15장 경쟁 구도

개요

주요 참가 기업의 전략/강점(2021-2025년)

수익 분석(2020-2024년)

시장 점유율 분석(2024년)

기업 평가 및 재무 지표

제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제16장 기업 프로파일

주요 기업

ALCATEL SUBMARINE NETWORKS

PRYSMIAN SPA

SUBCOM, LLC

NEC CORPORATION

NEXANS

HENGTONG GROUP CO., LTD.

ZTT

NKT A/S

SUMITOMO ELECTRIC INDUSTRIES LTD.

LS CABLE & SYSTEM LTD.

기타 기업

CORNING INCORPORATED

NINGBO ORIENT WIRES & CABLES CO. LTD.

TAIHAN CABLE & SOLUTION CO., LTD.

QINGDAO HANHE CABLE CO., LTD.

FURUKAWA ELECTRIC CO., LTD.

HEXATRONIC GROUP

APAR INDUSTRIES LTD.

TFKABLE

AFL

HELLENIC CABLES

SHANGHAI QIFAN CABLE CO., LTD.

SSGCABLE

OCC CORPORATION

FRIGATE ENGINEERING SERVICES PVT LTD

TRATOS

제17장 부록

JHS

영문 목차

영문목차

At a CAGR of 11.1%, the global submarine cable system market is anticipated to grow from USD 19.95 billion in 2025 to USD 33.75 billion by 2030. 5G allows mobile handsets and Internet of Things (IoT) devices to accommodate multiple connections simultaneously while improving speed, latency, reliability, and power consumption.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Cable Type, Component, Service Offering, Type, Voltage, Insulation, End-use Application, and Region

Regions covered

North America, Europe, APAC, RoW

The auctions for spectrum have nearly finished, 5G-ready handsets have been released, and network implementation has begun globally. Most 5G developments are focused on the business-to-consumer (B2C) market, owing to the efforts of network operators to reduce operational costs. With the growing demand for data fueled by bandwidth-intensive applications, such as video and audio streaming services, coupled with the continued shift toward cloud services and 5G, there is a growing need for fiber optic interconnectivity, which will drive the submarine cable systems market growth.

"Dry plant products segment captured second-largest share of submarine cable systems market for communication cables in 2024"

The dry plant products of submarine communication cables, comprising submarine line monitors (SLE), power feeding equipment (PFE), and submarine line terminal equipment (SLTE), cover the stage between beach manholes and cable landing stations. The demand for dry plant products in the submarine cable system market is driven by the need to support and optimize the performance of undersea cable networks once they reach the shore. The rapid expansion of data centers and the proliferation of broadband services require robust terrestrial infrastructure.

"Installation & commissioning segment to witness highest CAGR in market for submarine communication cables between 2025 and 2030"

Installation & commissioning are anticipated to witness the highest CAGR during the forecast period in the submarine communication cable market. Several key factors propel the installation and commissioning of submarine cables in the market. Firstly, the increasing global demand for high-speed and reliable connectivity drives the need for efficient installation and commissioning processes to deploy submarine cable networks swiftly. Secondly, advancements in installation technologies, such as remotely operated vehicles (ROVs) and specialized vessels, enable faster and more accurate cable laying in challenging underwater environments, contributing to reduced installation times and costs.

"Rising interest towards offshore infrastructure to position Asia Pacific as the second-largest submarine power cable market in 2024"

The submarine power cable market in Asia Pacific, which includes China, Japan, South Korea, Malaysia, Vietnam, Indonesia, and Rest of Asia Pacific, has been thoroughly assessed. According to projections from the Global Wind Energy Council (GWEC), the Asia Pacific is expected to dominate offshore wind energy expansion throughout this decade. China is emerging as a dominant player in the global submarine power cable market, driven by its aggressive push toward renewable energy and offshore infrastructure development. The country has set a target to add 64 GW of offshore wind power capacity within the next five years, aiming to reduce its dependence on fossil fuels and achieve carbon neutrality.

Breakdown of Primaries

Various executives from key organizations operating in the submarine cable systems market, including CEOs, marketing directors, and innovation and technology directors, were interviewed in-depth.

By Company Type: Tier 1 - 40%, Tier 2 - 25%, and Tier 3 - 35%

By Designation: Directors - 25%, C-level Executives - 45%, and Others - 30%

By Region: North America - 55%, Europe - 10%, Asia Pacific - 25%, the Middle East & Africa - 5%, and South America - 10%

Note: Three tiers of companies have been defined based on their total revenue as of 2024: tier 3: revenue less than USD 500 million; tier 2: revenue between USD 500 million and USD 1 billion; and tier 1: revenue more than USD 1 billion. Other designations include sales managers, marketing managers, and product managers.

Major players profiled in this report are Alcatel Submarine Networks (France), Prysmian S.p.A (Italy), SubCom, LLC (US), NEC Corporation (Japan), Nexans (France), HENGTONG GROUP CO., LTD. (China), NKT A/S (Denmark), ZTT (China), LS Cable & System Ltd. (South Korea), Sumitomo Electric Industries, Ltd.(Japan), Corning Incorporated (US), Ningbo Orient Wires &Cables Co.,Ltd. (China), Taihan Cable & Solution Co., Ltd. (South Korea), Qingdao Hanhe Cable Co., Ltd. (China), Furukawa Electric Co., Ltd. (Japan), Hexatronic Group (Sweden), APAR Industries Ltd. (India), TFKable (Poland), AFL (US), Hellenic Cables (Greece), Shanghai Qifan Cable Co.,Ltd. (China), SSGCABLE (China), OCC Corporation (Japan), Tratos (UK), and Frigate Engineering Services Pvt Ltd (US). These leading companies possess a broad portfolio of products and establish a prominent presence in established and emerging markets.

The study provides a detailed competitive analysis of these key players in the submarine cable systems market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report segments the submarine cable systems market based on cable type, component, service offering, type, end-use application, voltage, insulation, and region. The cable type segment includes communication cables and power cables. The component segment includes wet plant products and dry plant products.

The end-use application segment comprises offshore wind power generation plants, intercountry & island connections, and offshore oil & gas plants. The type segment includes single core and multicore. The service offerings segment covers the installation & commissioning, maintenance, and system upgrades. The voltage segment includes medium-voltage and High-voltage. The insulation segment includes cross-linked polyethylene, oil-impregnated paper, resin-impregnated paper, and resin-impregnated synthetics. The market for submarine power cable has been segmented into five regions-North America, Asia Pacific, Europe, the Middle East & Africa, and South America. The market for submarine communication cable has been segmented into five regions: Transatlantic, Transpacific, Intra-Asia, Americas, EMEA, and Europe-Asia.

Reasons to Buy the Report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the submarine cable systems market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

Analysis of key drivers (Expanding offshore wind power, Cost-effective access to internet connectivity, Cost-effective access to internet connectivity, Transition to 5G technology and cloud-based services, Growing demand for internet connectivity across the Transpacific region, Rising need for electrical power supply on islands ), restraints (Significant upfront investments and associated maintenance expenses, Engagement of several jurisdictions), opportunities (Implementation of HVDC power transmission technology, Rising participation of OTT players), challenges (Shortage of commissioning, maintenance, and repair activities for vessels, Rise of alternative technologies) influencing the growth of the submarine cable systems market

Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the submarine cable systems market

Market Development: Comprehensive information about lucrative markets, including the analysis of the submarine cable systems market across varied regions

Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in submarine cable systems

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, including Alcatel Submarine Networks (France), Prysmian S.p.A (Italy), SubCom, LLC (US), NEC Corporation (Japan), and Nexans (France).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of primary interview participants

2.1.3.2 Key data from primary sources

2.1.3.3 Key industry insights

2.1.3.4 Breakdown of primaries

2.2 MARKET SIZE ESTIMATION METHODOLOGY

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to derive market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to derive market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SUBMARINE CABLE SYSTEMS MARKET

4.2 SUBMARINE CABLE SYSTEMS MARKET, BY CABLE TYPE

4.3 SUBMARINE COMMUNICATION CABLES MARKET, BY COMPONENT

4.4 SUBMARINE POWER CABLES MARKET, BY INSULATION

4.5 SUBMARINE POWER CABLES MARKET IN EUROPE, BY END-USE APPLICATION AND COUNTRY

4.6 SUBMARINE POWER CABLES MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising need for reliable power transmission amid expanding offshore wind power capacity

5.2.1.2 Increasing bandwidth usage due to high access to affordable internet connectivity

5.2.1.3 Rapid transition toward 5G technology and cloud-based services

5.2.1.4 Mounting demand for high-speed internet connections across Transpacific region

5.2.1.5 Rising need for electrical power supply in islands

5.2.2 RESTRAINTS

5.2.2.1 Significant upfront investments and associated maintenance expenses

5.2.2.2 Requirement for permits for submarine cable installations

5.2.3 OPPORTUNITIES

5.2.3.1 Evolving HVDC power transmission technology

5.2.3.2 Increasing investment in submarine cable projects by over-the-top (OTT) players

5.2.4 CHALLENGES

5.2.4.1 Lack of commissioning, maintenance, and repair activities for vessels

5.2.4.2 Growing reliance on satellite internet technology

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 PRICING RANGE OF SUBMARINE CABLE SYSTEMS, BY CABLE TYPE, 2024

5.4.2 AVERAGE SELLING PRICE TREND OF SUBMARINE COMMUNICATION CABLES, 2021-2024

5.4.3 PRICING RANGE OF SUBMARINE CABLE SYSTEMS OFFERED BY KEY PLAYERS, BY CABLE TYPE, 2024

5.4.4 AVERAGE SELLING PRICING TREND OF SUBMARINE POWER CABLES, BY REGION, 2021-2024

5.5 VALUE CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 INVESTMENT AND FUNDING SCENARIO

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Wavelength division multiplexing

5.8.1.2 P-Laser cable technology

5.8.1.3 Open cables

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Subsea robotics

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Remote sensing and satellite communication

5.9 PATENT ANALYSIS

5.10 TRADE ANALYSIS

5.10.1 IMPORT SCENARIO (HS CODE 8544)

5.10.2 EXPORT SCENARIO (HS CODE 8544)

5.11 KEY CONFERENCES AND EVENTS, 2025-2026

5.12 CASE STUDY

5.12.1 CAMBRIDGE MANAGEMENT CONSULTING, PELAGIAN, AND BAKER BOTTS PROVIDE RESILIENT, HIGH-CAPACITY FIBER CONNECTIVITY SOLUTIONS IN TURKS & CAICOS ISLANDS

5.12.2 TRATOS SUPPLIES SUBMARINE CABLE COMPONENTS TO ADDRESS SPECIFIC REQUIREMENTS OF ENI'S MEXICO AREA 1 DEVELOPMENT PROJECT

5.12.3 XTERA AND GCS PARTNER TO DEPLOY SUBMARINE CABLES TO ENHANCE CONNECTIVITY BETWEEN GALAPAGOS ISLANDS AND ECUADOR

5.12.4 CORAL SEA CABLE SYSTEM (CS2) PROJECT ENABLES FASTER INTERNET CONNECTIVITY IN PAPUA NEW GUINEA AND SOLOMON ISLANDS

5.12.5 N-SEA BOOSTS PROJECT RESILIENCE USING SINAY'S METOCEAN ANALYTICS FOR WEATHER RISK MANAGEMENT

5.13 REGULATORY LANDSCAPE

5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.2 STANDARDS

5.14 PORTER'S FIVE FORCES ANALYSIS

5.14.1 INTENSITY OF COMPETITIVE RIVALRY

5.14.2 BARGAINING POWER OF SUPPLIERS

5.14.3 BARGAINING POWER OF BUYERS

5.14.4 THREAT OF SUBSTITUTES

5.14.5 THREAT OF NEW ENTRANTS

5.15 KEY STAKEHOLDERS AND BUYING PROCESS

5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2 BUYING CRITERIA

5.16 IMPACT OF AI/GEN AI ON SUBMARINE CABLE SYSTEMS MARKET

5.16.1 INTRODUCTION

5.16.2 IMPACT OF AI/GEN AI ON KEY END-USE APPLICATIONS

5.16.2.1 Offshore wind power generation plants

5.16.2.2 Offshore oil & gas plants

5.16.3 AI/GEN AI USE CASES

5.16.4 FUTURE OF AI/GEN AI IN SUBMARINE CABLE SYSTEMS ECOSYSTEM

5.17 IMPACT OF 2025 US TARIFF ON SUBMARINE CABLE SYSTEMS MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE APPLICATIONS

6 SUBMARINE CABLE SYSTEMS MARKET, BY CABLE TYPE

6.1 INTRODUCTION

6.2 COMMUNICATION CABLES

6.2.1 RISING ADOPTION OF CONNECTED DEVICES TO BOOST SEGMENTAL GROWTH

6.3 POWER CABLES

6.3.1 INCREASING OFFSHORE WIND FARM INSTALLATIONS TO ACCELERATE SEGMENTAL GROWTH

7 SUBMARINE COMMUNICATION CABLES MARKET, BY COMPONENT

7.1 INTRODUCTION

7.2 DRY PLANT PRODUCTS

7.2.1 GROWING DEMAND FOR ADVANCED TERRESTRIAL EQUIPMENT TO MANAGE DATA TRAFFIC AND ENSURE SEAMLESS CONNECTIVITY TO DRIVE MARKET

7.2.2 SUBMARINE LINE TERMINAL EQUIPMENT

7.2.3 SUBMARINE LINE MONITORS

7.2.4 POWER FEEDING EQUIPMENT

7.3 WET PLANT PRODUCTS

7.3.1 REPEATERS

7.3.1.1 Optimal amplification and resistance to water pressure to foster segmental growth

7.3.2 BRANCHING UNITS

7.3.2.1 Ability to handle cable breaks to contribute to segmental growth

7.3.3 CABLES

7.3.3.1 Use to address rising global connectivity demand to accelerate segmental growth

7.3.4 OTHER WET PLANT PRODUCTS

8 SUBMARINE COMMUNICATION CABLES MARKET, BY SERVICE OFFERING

8.1 INTRODUCTION

8.2 INSTALLATION & COMMISSIONING

8.2.1 RISING GLOBAL DEMAND FOR FAST AND RELIABLE CONNECTIVITY TO BOLSTER SEGMENTAL GROWTH

8.3 MAINTENANCE

8.3.1 INCREASING SUBMARINE CABLE DAMAGE FROM HUMAN ACTIVITIES TO AUGMENT SEGMENTAL GROWTH

8.4 SYSTEM UPGRADE

8.4.1 ADOPTION OF COHERENT TRANSMISSION TECHNOLOGY TO OFFER GROWTH OPPORTUNITIES

9 SUBMARINE POWER CABLES MARKET, BY TYPE

9.1 INTRODUCTION

9.2 SINGLE CORE

9.2.1 EXPANDING USE IN OFFSHORE WIND FARMS AND REMOTE ISLANDS FOR POWER DISTRIBUTION TO FUEL SEGMENTAL GROWTH

9.3 MULTICORE

9.3.1 CAPABILITY OF LEAD SHEATHS TO PREVENT WATER INGRESS TO EXPEDITE SEGMENTAL GROWTH

10 SUBMARINE POWER CABLES MARKET, BY VOLTAGE

10.1 INTRODUCTION

10.2 MEDIUM-VOLTAGE

10.2.1 RISING NEED FOR CONNECTIONS BETWEEN GENERATORS ON WIND FARMS AND OFFSHORE OIL & GAS PLATFORMS TO DRIVE MARKET

10.3 HIGH-VOLTAGE

10.3.1 INCREASING OFFSHORE RENEWABLE POWER GENERATION TO ACCELERATE SEGMENTAL GROWTH

11 SUBMARINE POWER CABLES MARKET, BY INSULATION

11.1 INTRODUCTION

11.2 CROSS-LINKED POLYETHYLENE (XLPE)

11.2.1 CAPABILITY TO PROVIDE HIGH ELECTRICAL AND MECHANICAL STRENGTH TO BOOST SEGMENTAL GROWTH

11.3 OIL-IMPREGNATED PAPER (OIP)

11.3.1 INCREASING USE IN HIGH-VOLTAGE DC TRANSMISSION LINES TO CONTRIBUTE TO SEGMENTAL GROWTH

11.4 RESIN-IMPREGNATED PAPER (RIP)

11.4.1 CAPABILITY TO ENDURE HARSH ENVIRONMENTAL CONDITIONS TO AUGMENT SEGMENTAL GROWTH

11.5 RESIN-IMPREGNATED SYNTHETIC (RIS)

11.5.1 EXPLOSION-PROOF PROPERTIES TO ACCELERATE SEGMENTAL GROWTH

12 SUBMARINE POWER CABLES MARKET, BY END-USE APPLICATION

12.1 INTRODUCTION

12.2 OFFSHORE WIND POWER GENERATION PLANTS

12.2.1 GROWING NEED FOR LONG-DISTANCE POWER TRANSMISSION TO FUEL SEGMENTAL GROWTH

12.3 INTERCOUNTRY & ISLAND CONNECTION

12.3.1 RISING DEMAND FOR CLEAN AND RENEWABLE ENERGY TO DRIVE MARKET

12.4 OFFSHORE OIL & GAS PLANTS

12.4.1 INCREASING USE OF SATELLITE WELLS IN SUBSEA FIELD DEVELOPMENT TO BOOST SEGMENTAL GROWTH

13 SUBMARINE POWER CABLES MARKET, BY REGION

13.1 INTRODUCTION

13.2 NORTH AMERICA

13.2.1 US

13.2.1.1 Rising government initiatives to promote offshore wind energy to accelerate market growth

13.2.2 CANADA

13.2.2.1 Growing emphasis on building clean economy through renewable energy technologies to drive market

13.2.3 MEXICO

13.2.3.1 Increasing offshore oil activities to contribute to market growth

13.3 EUROPE

13.3.1 UK

13.3.1.1 Growing emphasis on achieving net-zero emission targets to boost market growth

13.3.2 GERMANY

13.3.2.1 Government initiatives to support renewable energy adoption to fuel market growth

13.3.3 DENMARK

13.3.3.1 Increasing investment in offshore wind sector to accelerate market growth

13.3.4 NETHERLANDS

13.3.4.1 Growing reliance on sustainable energy sources to drive market

13.3.5 NORWAY

13.3.5.1 Increasing production of offshore oil and gas to bolster market growth

13.3.6 FRANCE

13.3.6.1 Growing construction of offshore wind farms to contribute to market growth

13.3.7 REST OF EUROPE

13.4 ASIA PACIFIC

13.4.1 CHINA

13.4.1.1 Strong focus on reducing reliance on fossil fuels to augment market growth

13.4.2 JAPAN

13.4.2.1 Increasing installation of offshore wind capacity to foster market growth

13.4.3 SOUTH KOREA

13.4.3.1 Government-driven initiatives to promote renewable energy to fuel market growth

13.4.4 MALAYSIA

13.4.4.1 Escalating offshore oil production to contribute to market growth

13.4.5 INDONESIA

13.4.5.1 Rising implementation of favorable laws to promote carbon capture to accelerate market growth

13.4.6 VIETNAM

13.4.6.1 Strong commitment to achieving net-zero carbon emissions using renewable energy to expedite market growth

13.4.7 REST OF ASIA PACIFIC

13.5 MIDDLE EAST & AFRICA

13.5.1 UAE

13.5.1.1 Increasing investment to accelerate oil and gas production to drive market

13.5.2 SAUDI ARABIA

13.5.2.1 Growing emphasis on offshore oil and gas exploration activities to boost market growth

13.5.3 ANGOLA

13.5.3.1 Increasing focus on offshore crude oil and natural gas production to accelerate market growth

13.5.4 REST OF MIDDLE EAST & AFRICA

13.6 SOUTH AMERICA

13.6.1 BRAZIL

13.6.1.1 Emergence as significant hub for wind energy to contribute to market growth

13.6.2 ARGENTINA

13.6.2.1 Rising implementation of legislation to support renewable energy initiatives to fuel market growth

13.6.3 REST OF SOUTH AMERICA

14 SUBMARINE COMMUNICATION CABLES MARKET, BY REGION

14.1 INTRODUCTION

14.2 TRANSATLANTIC

14.2.1 MOUNTING DEMAND FOR LOW-LATENCY COMMUNICATION TO CREATE MARKET GROWTH OPPORTUNITIES

14.3 TRANSPACIFIC

14.3.1 RISING INITIATIVES TO CONNECT MAJOR ECONOMIC AND DATA CENTER HUBS TO DRIVE MARKET

14.4 INTRA-ASIA

14.4.1 GROWING FOCUS ON ENHANCING DIGITAL CONNECTIVITY TO FUEL MARKET GROWTH

14.5 AMERICAS

14.5.1 FLOURISHING MOBILE DATA INDUSTRY TO CONTRIBUTE TO MARKET GROWTH

14.6 EURASIA

14.6.1 GROWING ADOPTION OF MOBILE AND CLOUD SERVICES TO BOLSTER MARKET GROWTH

14.7 EMEA

14.7.1 INCREASING EXECUTION OF SUBMARINE COMMUNICATION CABLE PROJECTS TO FOSTER MARKET GROWTH

15 COMPETITIVE LANDSCAPE

15.1 OVERVIEW

15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

15.3 REVENUE ANALYSIS, 2020-2024

15.4 MARKET SHARE ANALYSIS, 2024

15.5 COMPANY VALUATION AND FINANCIAL METRICS

15.6 PRODUCT COMPARISON

15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

15.7.1 STARS

15.7.2 EMERGING LEADERS

15.7.3 PERVASIVE PLAYERS

15.7.4 PARTICIPANTS

15.7.5 COMPANY FOOTPRINT: KEY PLAYERS IN SUBMARINE POWER CABLES MARKET, 2024

15.7.5.1 Company footprint

15.7.5.2 Region footprint

15.7.5.3 Type footprint

15.7.5.4 End-use application footprint

15.7.6 COMPANY FOOTPRINT: KEY PLAYERS IN SUBMARINE COMMUNICATION CABLES MARKET, 2024

15.7.6.1 Company footprint

15.7.6.2 Region footprint

15.7.6.3 Component footprint

15.7.6.4 Service offering footprint

15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024