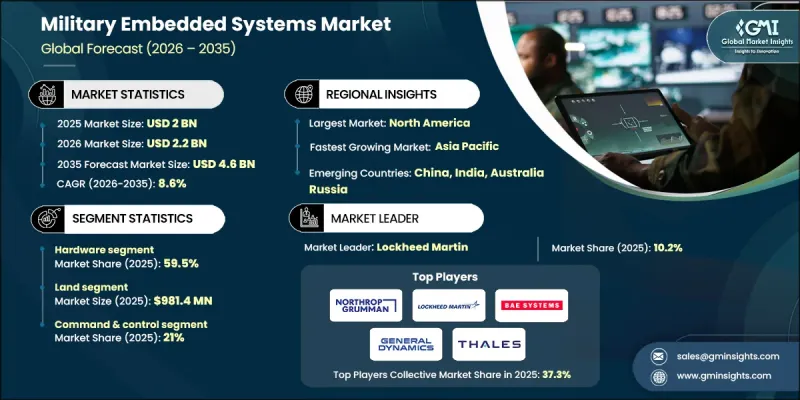

세계의 군용 임베디드 시스템 시장은 2025년에 20억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.6%로 성장하여 46억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 복잡한 작전 환경에서 미션 크리티컬 데이터의 신속한 실시간 처리에 대한 수요 증가가 있습니다. 전 세계 군는 속도, 정확성, 작전 회복력을 보장하기 위해 임베디드 컴퓨팅에 의존하는 현대적 디지털 전투 능력에 대한 투자를 확대하고 있습니다. 무인 플랫폼, 자율 전투 시스템, 디지털 통합형 국방 인프라의 도입 증가로 첨단 임베디드 솔루션에 대한 수요가 크게 증가하고 있습니다. 각 군의 현대화 계획은 전장 인식 능력과 의사결정 능력을 향상시키기 위해 데이터 중심의 전쟁 수행, 인공지능 통합, 엣지 기반 처리에 중점을 두고 있습니다. 주요 군사 강국 및 동맹국들의 국방 예산 증가는 육상, 항공, 해상, 우주 영역에서 대응성, 생존성, 임무 수행 능력을 향상시키는 임베디드 기술에 대한 장기적인 투자를 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 20억 달러 |

| 예측 금액 | 46억 달러 |

| CAGR | 8.6% |

이러한 시장 역학은 역동적인 전투 환경에서 빠르고 안정적인 상황 인식을 제공하는 임베디드 컴퓨팅 플랫폼에 대한 수요가 증가함에 따라 더욱 강화되고 있습니다. 국방 기관은 의사결정 지연을 줄이고, 센서 데이터 통합을 개선하며, 작전 조정을 강화하는 데이터 기반 지휘 구조를 우선시하고 있습니다. 임베디드 시스템은 무인 및 자율 플랫폼의 핵심이 되고 있으며, 인력의 위험에 노출될 위험을 최소화하면서 작전 범위를 확장할 수 있게 해줍니다. 군가 자율 및 원격 제어 시스템에 대한 의존도가 높아짐에 따라 견고하고 안전하며 고성능의 임베디드 솔루션에 대한 수요는 계속 증가하고 있습니다.

소프트웨어 분야는 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 9.2%로 확대될 것으로 예측됩니다. 국방 시스템 내 인공지능 처리, 엣지 분석, 사이버 보안 기능에 대한 수요 증가가 성장을 견인하고 있습니다. 소프트웨어 기반 임베디드 솔루션은 적응성, 보안 통신, 예지보전, 자율적 의사결정을 제공하며, 차세대 디지털 전장 아키텍처에 필수적인 요소입니다.

지휘통제 분야는 2025년 21%의 점유율을 차지하며 전략적 중요성으로 인해 주도적인 위치를 유지하고 있습니다. 임베디드 시스템은 전체 방어 플랫폼의 작전 조정, 정보 처리, 보안 통신 관리에서 중요한 역할을 합니다. 실시간 데이터 처리 및 고급 분석 기술이 이 응용 분야의 지속적인 수요를 주도하고 있습니다.

북미 군용 임베디드 시스템 시장은 견조한 국방 지출, 첨단 현대화 프로그램, 지능형 처리 기술의 급속한 통합에 힘입어 2025년 42.6%의 점유율을 차지할 것으로 예측됩니다. 이러한 지역적 성장은 다중 도메인 군사 작전에서 자율성, 보안 네트워크, 고속 정보 처리에 대한 관심이 높아진 것을 반영합니다.

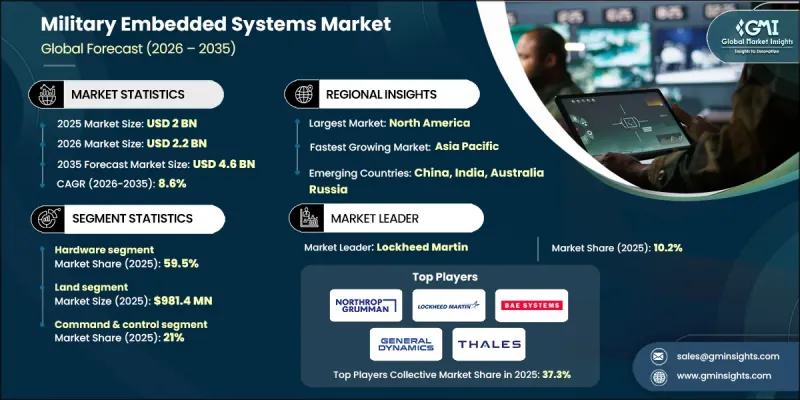

The Global Military Embedded Systems Market was valued at USD 2 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 4.6 billion by 2035.

Market expansion is driven by the growing requirement for rapid, real-time processing of mission-critical data in complex operational environments. Armed forces worldwide are increasingly investing in modern digital combat capabilities that rely on embedded computing for speed, accuracy, and operational resilience. Rising adoption of unmanned platforms, autonomous combat systems, and digitally integrated defense infrastructure is significantly increasing demand for advanced embedded solutions. Modernization initiatives across military forces are emphasizing data-centric warfare, artificial intelligence integration, and edge-based processing to enhance battlefield awareness and decision-making. Growing defense budgets among major military powers and allied nations are further supporting long-term investment in embedded technologies that improve responsiveness, survivability, and mission effectiveness across land, air, sea, and space domains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 8.6% |

Market momentum is reinforced by the rising need for embedded computing platforms capable of delivering fast and reliable situational awareness in dynamic combat conditions. Defense organizations are prioritizing data-driven command structures that reduce decision latency, improve sensor data integration, and enhance operational coordination. Embedded systems are becoming central to unmanned and autonomous platforms, enabling extended operational reach while minimizing personnel exposure. As militaries expand their reliance on autonomous and remotely operated systems, demand for rugged, secure, and high-performance embedded solutions continues to grow.

The software segment is expected to grow at a CAGR of 9.2% during 2026-2035. Growth is supported by increasing demand for artificial intelligence processing, edge analytics, and cybersecurity capabilities within defense systems. Software-driven embedded solutions offer adaptability, secure communications, predictive maintenance, and autonomous decision-making, making them essential to next-generation digital battlefield architectures.

The command-and-control segment accounted for 21% share in 2025, maintaining its leading position due to its strategic importance. Embedded systems play a critical role in managing operational coordination, intelligence processing, and secure communications across defense platforms. Real-time data handling and advanced analytics continue to drive sustained demand in this application area.

North America Military Embedded Systems Market held a share of 42.6% in 2025, supported by strong defense spending, advanced modernization programs, and rapid integration of intelligent processing technologies. Regional growth reflects increasing focus on autonomy, secure networks, and high-speed information processing across multi-domain military operations.

Key companies active in the Global Military Embedded Systems Market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, BAE Systems plc, Thales Group, Leonardo S.p.A., Saab AB, Rheinmetall AG, General Dynamics Corporation, Boeing Defense Space & Security, L3Harris Technologies Inc., Collins Aerospace, Elbit Systems Ltd., Curtiss-Wright Corporation, Honeywell International Inc., Intel Corporation, Renesas Corporation, Harris Corporation, and ABB Ltd. Companies operating in the Military Embedded Systems Market are strengthening their competitive position through sustained investment in research and development focused on artificial intelligence, edge computing, and secure system architectures. Many players are forming long-term defense contracts and strategic alliances to support large-scale modernization programs. Localization of production and compliance with military-grade certification standards are being prioritized to meet procurement requirements. Firms are also expanding modular and scalable embedded platforms to support multi-domain operations.