자동차 벨트 텐셔너 풀리 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)

Automotive Belt Tensioner Pulleys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1959597

리서치사:Global Market Insights Inc.

발행일:2026년 02월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

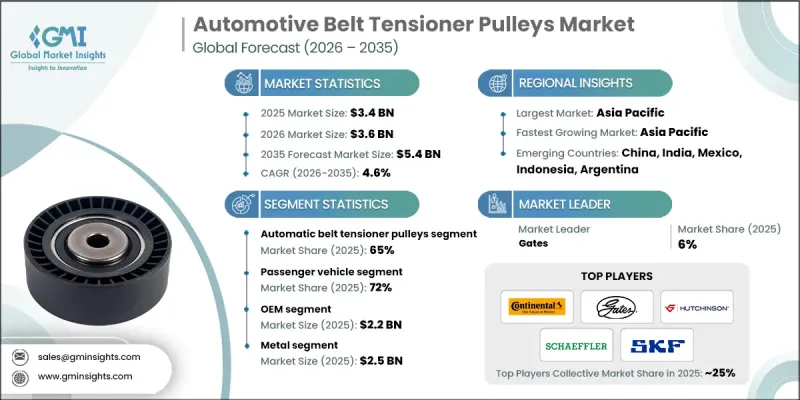

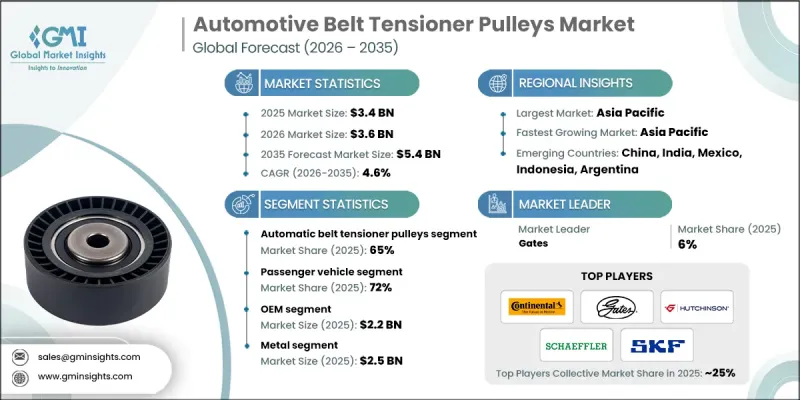

세계의 자동차 벨트 텐셔너 풀리 시장은 2025년에 34억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%로 성장하여 54억 달러에 이를 것으로 예측됩니다.

시장 성장은 내연기관차와 하이브리드 차량의 지속적인 우위에 의존하고 있으며, 이 두 차종은 중기적으로 전 세계 운행 차량의 대부분을 차지할 것입니다. 이러한 차량 플랫폼은 안정적인 기계적 성능을 위해 벨트 구동 시스템에 의존하고 있으며, 벨트 텐셔너 풀리는 신뢰성과 효율성의 중요한 구성 요소입니다. 전기차의 존재감이 계속 확대되는 가운데 하이브리드 플랫폼은 전통적인 벨트 구조를 유지하고 있으며, 이는 전체 수요의 안정화에 기여하고 있습니다. 이 시장은 차량의 긴 수명주기, 안정적인 교체 수요, 내구성과 성능을 향상시키는 지속적인 기술 개선의 혜택을 누리고 있습니다. 현대 파워트레인의 기계적 복잡성이 증가함에 따라 벨트 시스템에 높은 작동 부하가 가해지기 때문에 정밀하게 설계된 텐션 솔루션의 필요성이 증가하고 있습니다. 그 결과, 지역별로 자동차 생산량이 변동하는 가운데서도 OEM 수요와 견조한 교체주기에 힘입어 시장은 꾸준히 확대되고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

34억 달러

예측 금액

54억 달러

CAGR

4.6%

자동차 벨트 텐셔너 풀리는 지속적인 작동 스트레스로 인해 점진적인 기계적 열화가 발생하기 때문에 차량 수명 기간 동안 교체가 필수적입니다. 전 세계 자동차 보유량 증가, 특히 선진국과 신흥 지역의 노후화된 차량군 증가는 애프터마켓 수요를 지속적으로 뒷받침하고 있습니다. 이러한 교체 수요로 인한 소비는 수익의 안정성을 제공하고, 신차 생산량의 단기적인 변동성을 상쇄하여 장기적인 성장 전망을 강화합니다.

자동 벨트 텐셔너 풀리 부문은 2025년 65%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.1%의 성장률을 보일 것으로 예측됩니다. 이 시스템은 최적의 벨트 장력을 자동으로 유지하는 기능으로 인해 현대 내연기관 및 하이브리드 차량에 표준으로 장착되어 있습니다. 이를 통해 작동 위험을 줄이고 부품 수명을 연장하는 동시에 전체 시스템의 신뢰성을 향상시킵니다.

OEM 부문은 2025년 22억 달러에 달했습니다. OEM 수요는 엔지니어링 협력, 비용 효율성, 품질 준수, 차량 개발 프로그램에 대한 초기 단계의 통합을 중시하는 장기 공급업체 계약에 힘입어 내연기관 및 하이브리드 자동차의 세계 생산과 연계된 상태로 유지되고 있습니다.

미국 자동차 벨트 텐셔너 풀리 시장은 2025년 7억 9,310만 달러 규모에 달할 것으로 예측됩니다. 높은 기계적 하중을 받는 차량에 대한 수요가 증가하고 있으며, 이로 인해 첨단 텐셔너 설계와 고부가가치 부품에 대한 요구가 증가하고 있습니다. 또한, 정비된 애프터마켓 기반이 교체 수요를 더욱 강화하여 전국적인 시장 안정성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 차량별, 2022-2035

제7장 시장 추산 및 예측 : 재료별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 판매채널별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH

영문 목차

영문목차

The Global Automotive Belt Tensioner Pulleys Market was valued at USD 3.4 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 5.4 billion by 2035.

Market growth remains tied to the continued dominance of internal combustion engines and hybrid vehicles, which together represent many vehicles in operation worldwide over the medium term. These vehicle platforms depend on belt-driven systems for consistent mechanical performance, making belt tensioner pulleys a critical component for reliability and efficiency. While electric vehicles continue to expand their presence, hybrid platforms retain conventional belt architectures, helping stabilize overall demand. The market benefits from long vehicle life cycles, steady replacement requirements, and ongoing engineering refinements that improve durability and performance. Growing mechanical complexity within modern powertrains places higher operational stress on belt systems, increasing the need for accurately engineered tensioning solutions. As a result, the market continues to show steady expansion supported by both original equipment demand and a resilient replacement cycle, even as vehicle production volumes fluctuate across regions.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$3.4 Billion

Forecast Value

$5.4 Billion

CAGR

4.6%

Automotive belt tensioner pulleys experience gradual mechanical degradation due to constant operational stress, making replacement essential over a vehicle's lifetime. An expanding global vehicle population, particularly aging fleets in developed and emerging regions, continues to support consistent aftermarket demand. This replacement-driven consumption provides revenue stability and offsets short-term variations in new vehicle output, reinforcing the long-term growth outlook.

The automatic belt tensioner pulleys segment accounted for 65% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. These systems have become standard across modern internal combustion and hybrid vehicles due to their ability to maintain optimal belt force automatically, reducing operational risk and extending component lifespan while improving overall system reliability.

The OEM segment reached USD 2.2 billion in 2025. OEM demand remains aligned with global production of internal combustion and hybrid vehicles, supported by long-term supplier agreements that emphasize engineering collaboration, cost efficiency, quality compliance, and early-stage integration into vehicle development programs.

United States Automotive Belt Tensioner Pulleys Market generated USD 793.1 million in 2025. Demand is supported by vehicles operating under higher mechanical loads, which increases requirements for advanced tensioner designs and higher-value components. A well-developed aftermarket infrastructure further strengthens replacement demand and enhances market stability nationwide.

Key companies operating in the Global Automotive Belt Tensioner Pulleys Market include Schaeffler, Gates, Continental, SKF, NTN, Dayco Products, Hutchinson, Aisin Seiki, Litens Automotive, and NSK Automation. Companies in the automotive belt tensioner pulleys market are reinforcing their market position through product innovation, material advancements, and close collaboration with vehicle manufacturers. Many suppliers are investing in next-generation designs that enhance durability, reduce noise, and improve thermal performance. Expansion of manufacturing capacity in key automotive regions is helping companies optimize costs and ensure supply reliability. Firms are also strengthening aftermarket distribution networks to capture recurring replacement demand.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research approach

1.2 Quality Commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research Trail & Confidence Scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data Collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022-2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Vehicle

2.2.4 Material

2.2.5 Application

2.2.6 Sales Channel

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Key decision points for industry executives

2.4.2 Critical success factors for market players

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.1.1 Manufacturers

3.1.1.2 Component suppliers

3.1.1.3 Service providers

3.1.1.4 Distributors

3.1.1.5 End-users

3.1.2 Cost structure

3.1.3 Profit margin

3.1.4 Value addition at each stage

3.1.5 Factors impacting the supply chain

3.1.6 Disruptors

3.2 Impact on forces

3.2.1 Growth drivers

3.2.1.1 Continued dominance of ICE and hybrid vehicle parcels

3.2.1.2 Large and aging global vehicle fleet driving aftermarket demand

3.2.1.3 Increasing accessory load and engine complexity

3.2.1.4 OEM focus on NVH reduction and durability

3.2.2 Industry pitfalls & challenges

3.2.2.1 Accelerating electrification of vehicle powertrains

3.2.2.2 Rapid decline of hydraulic power steering systems

3.2.3 Market opportunities

3.2.3.1 Expansion of hybrid vehicle production

3.2.3.2 Growth in aftermarket repair kits and system solutions

3.2.3.3 Vehicle production growth in emerging markets

3.2.3.4 Innovation in lightweight and low-friction pulley designs

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 FMVSS (Federal Motor Vehicle Safety Standards - United States)

3.4.1.2 EPA Emission Regulations (United States)

3.4.1.3 CARB Emission Standards (California Air Resources Board)

3.4.2 Europe

3.4.2.1 EU Type Approval Framework (Regulation (EU) 2018/858)

3.4.2.2 Euro 6 and Euro 7 Emission Standards

3.4.2.3 End-of-Life Vehicles (ELV) Directive

3.4.2.4 REACH Regulation

3.4.2.5 OEM-Specific NVH and Durability Compliance Standards

3.4.3 Asia Pacific

3.4.3.1 Bharat Stage VI (BS VI) Emission Norms - India

3.4.3.2 Automotive Industry Standards (AIS) - India

3.4.3.3 China VI Emission Standards

3.4.3.4 China Compulsory Certification (CCC)

3.4.3.5 Japan Automotive Standards and Regulations (JASO / MLIT)

3.4.4 Latin America

3.4.4.1 PROCONVE Emission Standards - Brazil

3.4.4.2 Inmetro Automotive Certification - Brazil

3.4.4.3 NOM Vehicle Safety and Emission Standards - Mexico