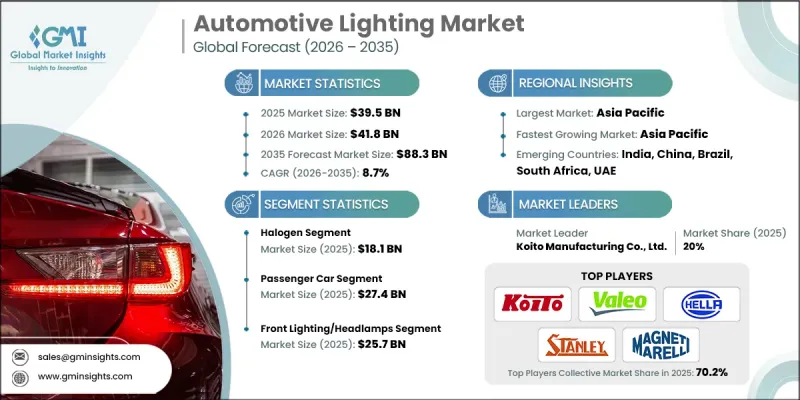

세계의 자동차 조명 시장은 2025년에 395억 달러로 평가되었고, 2035년까지 883억 달러에 이를 전망이며, CAGR 8.7%로 성장할 것으로 예측됩니다.

이 산업의 성장은 LED 및 적응형 조명 시스템 채택 확대, 차량 안전 기준 및 배기가스 규제 강화, 전기 및 자율주행차 보급 확대, 에너지 절약 및 스타일리시한 조명에 대한 소비자 수요, 신흥 시장에서의 자동차 제조 확대 등에 의해 주도되고 있습니다. 세계 안전 기준과 에너지 절약 의무에 대한 규제 준수는 첨단 조명 기술의 통합을 촉진하여 운전자의 가시성 향상, 눈부심 감소, 차량 전체의 효율성 향상에 기여하고 있습니다. 전동화 및 자율주행으로의 전환은 현대 자동차의 안전, 에너지 관리 및 미적 디자인의 중요한 구성 요소로서 첨단 조명 솔루션의 활용을 더욱 확대시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 395억 달러 |

| 예측 금액 | 883억 달러 |

| CAGR | 8.7% |

할로겐 부문은 2025년 181억 달러를 차지할 것으로 예상되며, 낮은 생산 비용, 간편한 제조 공정, 기존 차량 전기 시스템과의 폭넓은 호환성으로 인해 견조한 수요를 유지할 것으로 보입니다. 할로겐 조명은 LED 및 적응형 시스템과 같은 프리미엄 조명 기술이 아직 표준으로 장착되지 않은 보급형 및 중급 차량에 널리 사용되고 있으며, 기본적인 안전 요구 사항을 손상시키지 않으면서도 비용 효율적인 솔루션을 제공합니다. 그 중요성은 애프터마켓용 교체 부품에도 적용되며, 전 세계 자동차 보유대수 증가로 인해 구형 차량에 대한 개조 수요는 안정적으로 유지될 것으로 예측됩니다. 또한 할로겐 전구는 다양한 주행 조건에서도 신뢰성을 발휘하고 최소한의 유지보수가 필요하기 때문에 비용 효율성이 우선시되는 차량 사업자, 상용차, 개발도상국 시장에서 선호되는 선택이 되고 있습니다.

승용차 부문은 2025년 274억 달러 규모에 달할 것으로 예상되며, 안전성과 시각적 매력을 동시에 만족시키는 어댑티브 LED 매트릭스 시스템 등 첨단 조명 기능에 대한 강력한 수요가 주도하고 있습니다. 이러한 기술은 동적 빔 조정, 야간 시인성 향상, 마주 오는 차량에 대한 눈부심 감소를 실현하여 운전 안전도 평가 향상에 기여하고 있습니다. 또한, 승용차 구매자들은 차량 디자인과 브랜드 아이덴티티의 일부로 조명의 미학을 중시하는 경향이 증가하고 있으며, 자동차 제조업체들은 독특한 조명 패턴으로 모델 차별화를 꾀하고 있습니다. 주요 시장의 규제 프레임워크(주간주행등 의무화, 어댑티브 헤드램프, 에너지 효율 기준 등)도 도입에 더욱 박차를 가하고 있습니다.

북미 자동차 조명 시장은 2025년 18.5%의 점유율을 차지할 것으로 예상되며, 차량 전동화, LED 및 스마트 적응형 조명 시스템의 보급 확대, 연방 조명 및 안전 표준에 대한 엄격한 준수 등이 견인 요인으로 작용할 것으로 보입니다. 이 지역의 선진적인 자동차 제조 생태계, 강력한 규제 집행 시스템, 고성능 및 에너지 절약형 조명 솔루션에 대한 소비자 선호도가 시장 확대를 뒷받침하고 있습니다. 첨단 전방 조명 시스템, 매트릭스 LED, 레이저 기반 기술은 신형 승용차 및 소형 상용차 모델에 표준으로 장착되어 가시성 향상, 전력 소비 감소, 운전 안전성 향상을 돕고 있습니다. 또한, 북미 제조업체들은 자율주행과 스마트 모빌리티 인프라에 대한 관심이 높아짐에 따라 센서와 IoT 기술을 통합한 지능형 커넥티드 조명 솔루션의 연구개발에 많은 투자를 하고 있으며, 이를 통해 적응형 자율 주행 차량용 조명을 구현하고 있습니다.

The Global Automotive Lighting Market was valued at USD 39.5 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 88.3 billion by 2035.

The industry's growth is driven by increasing adoption of LED and adaptive lighting systems, stricter vehicle safety and emissions regulations, rising popularity of electric and autonomous vehicles, consumer demand for energy-efficient and stylish lighting, and expansion of automotive manufacturing in emerging markets. Regulatory compliance with global safety standards and energy-efficiency mandates is encouraging the integration of advanced lighting technologies, enhancing driver visibility, reducing glare, and contributing to overall vehicle efficiency. The shift toward electrification and autonomous driving has further amplified the use of sophisticated lighting solutions as critical components of safety, energy management, and aesthetic design in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.5 Billion |

| Forecast Value | $88.3 Billion |

| CAGR | 8.7% |

The halogen segment accounted for USD 18.1 billion in 2025, maintaining strong demand due to its low production costs, straightforward manufacturing processes, and broad compatibility with existing vehicle electrical systems. Halogen lighting continues to be widely used in entry-level and mid-segment vehicles where premium lighting technologies like LEDs or adaptive systems are not yet standard, offering a cost-effective solution without compromising basic safety requirements. Its relevance extends to aftermarket replacements, supported by the growing global vehicle parc, which ensures a consistent demand for retrofitting older vehicles. Additionally, halogen bulbs provide reliability under diverse driving conditions and require minimal maintenance, making them a preferred choice for fleet operators, commercial vehicles, and markets in developing regions where cost efficiency remains a priority.

The passenger car segment reached USD 27.4 billion in 2025, driven by strong demand for advanced lighting features such as adaptive, LED, and matrix systems, which enhance both safety and visual appeal. These technologies provide dynamic beam adjustments, improved nighttime visibility, and glare reduction for oncoming traffic, contributing to higher driving safety ratings. Furthermore, passenger car buyers increasingly consider lighting aesthetics as part of vehicle design and brand identity, pushing automakers to differentiate their models with signature lighting patterns. Regulatory frameworks in major markets, including mandatory daytime running lights, adaptive headlamps, and energy-efficiency standards, further accelerate adoption.

North America Automotive Lighting Market held an 18.5% share in 2025, driven by rising vehicle electrification, widespread adoption of LED and smart adaptive lighting systems, and strict compliance with federal lighting and safety standards. The region's advanced automotive manufacturing ecosystem, strong regulatory enforcement, and consumer preference for high-performance, energy-efficient lighting solutions underpin market expansion. Advanced front lighting systems, matrix LED, and laser-based technologies are becoming standard in new passenger and commercial vehicle models, supporting enhanced visibility, reduced power consumption, and improved driving safety. Additionally, North American manufacturers are investing heavily in R&D for intelligent and connected lighting solutions, integrating sensors and IoT technologies to enable adaptive, autonomous vehicle-ready lighting that aligns with the growing focus on automated driving and smart mobility infrastructure.

Prominent players in the Global Automotive Lighting Market include Continental AG, General Electric Company, HELLA GmbH & Co. KGaA, Hyundai Mobis Co., Ltd, Ichikoh Industries, Ltd., Koito Manufacturing Co., Koninklijke Philips N.V., Lumax Industries, Magnetti Marelli S.p.A, Namyung Lighting, OSRAM GmbH, Robert Bosch GmbH, Samsung Electronics Co., Ltd., Seoul Semiconductor, Stanley Electric Co., Ltd., Tungsram Group, Valeo Visibility Systems, Varroc Lighting Solutions, Zizala Lichtsysteme GmbH, and ZKW Lichtsysteme GmbH. Companies in the Automotive Lighting Market are focusing on strategic initiatives such as expanding R&D for LED and adaptive systems, forming partnerships with OEMs to integrate intelligent lighting technologies, optimizing supply chains for global distribution, investing in sustainable energy-efficient solutions, launching aftermarket programs to capture legacy vehicle demand, and adopting digital and IoT-enabled lighting innovations. Emphasis on design differentiation, regulatory compliance, and modular, scalable solutions helps manufacturers strengthen market presence, improve brand recognition, and secure long-term contracts with automotive producers worldwide.